Autonomous / Self-Driving Cars Market Size by Component, Mobility, Level of Autonomy, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

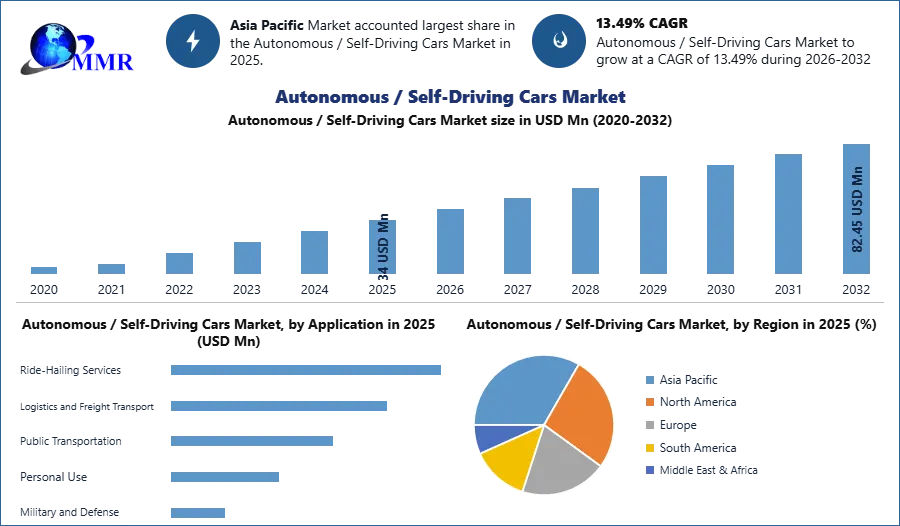

Autonomous / Self-Driving Cars Market volume was at 34 Million Units in 2025 and the total revenue is expected to grow at 13.5% of CAGR through 2026 to 2032, reaching nearly 82.45 Million Units.

Autonomous / Self-Driving Cars Market Overview:

Cars or trucks that can run safely without a human driver at the wheel are known as self-driving vehicles. These vehicles are sometimes referred to as autonomous or "driverless," A vehicle that combines a collection of sensors, cameras, radar, and artificial intelligence (AI) to move between locations without a human driver is referred to as a self-driving car (also known as an autonomous car or driverless car). A vehicle must be capable of navigating to a predefined location across roads that have not been modified for its usage in order to be considered completely autonomous. Audi, BMW, Ford, Google, General Motors, Tesla, Volkswagen, and Volvo are among the companies developing and/or testing autonomous/self-driving vehicles.

Autonomous cars are being manufactured with extremely advanced equipment connected with smartphones, creating opportunities for market companies to attract customers. Government restrictions are becoming more strict with a focus on boosting road safety. Manufacturers have been able to improve self-driving capabilities in automobiles thanks to recent technological developments in the sectors of artificial intelligence, machine learning, and other sensors including RADAR, LIDAR, GPS, and computer vision these are driving market growth in the forecast period. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Autonomous / Self-Driving Cars Market Dynamics:

High demand for luxury cars is making future

During the forecast period, demand for luxury vehicles is expected increase demand for self-driving cars. Mercedes-Benz, BMW, and Audi are just a few of the German manufacturers that dominate the world's luxury automobile industry. Global sales of luxury automobiles have benefited from the shift in customer tastes, which has raised a demand for superior products.

In spite of the global automotive market's slump, big BMW's automotive sector saw growth in 2020. The division had a 6.8% increase in growth in 2020 because of rising premium car category deliveries. When compared to 4,194 units sold the year before, its subsidiary, Rolls Royce, sold 5,100 units, a rise of 21.6%, while production output grew by 25.3%. In a similar fashion, the company sold more cars with the BMW brand in 2020 than in 2019. Luxury and premium automobile classes are where safety advancements are initially implemented, and this increase in sales will play a key role in the market for self-driving cars.

Can robotaxi change market strategies and the future?

Robotic taxi (robotaxi) deployments are rising rapidly as a result of advancements in self-driving automobile technology and advancements in automated driving system (ADS) technology. Robotaxis offers the potential to increase vehicle accessibility, and safety by reducing human error-related accidents, and sustainability by boosting the chances that there will be more electric vehicles on the road.

As developments in the autonomous vehicle market led to more robotaxi deployments, players in this industry must handle local restrictions, deal with challenging data challenges and develop connected car ecosystems in order to drive towards a new era of future mobility. robotaxi deployments are expanding quickly for a variety of reasons, including technological improvement, legislative reforms, a focus on sustainability, and a movement in the transportation sector to concentrate on the possibility of scaling autonomous cars. Additionally, in order to attract more customers, robotaxi ride rates are now significantly reduced. The technology will definitely be a big source of revenue for businesses once it is widely used.

AutoX now provides a commercial driverless ride-hailing service in Shenzhen, China, after receiving the first-ever license to operate fully driverless on public roads in that nation. Waymo launched its fully driverless commercial taxi in Phoenix, Arizona, the US, in 2020. Larger OEMs are also positive about the future of AV technology. Volvo predicts that 1 million cars will be delivered by 2025 with Level 4 AD, while Volkswagen plans to introduce a self-driving electric van in 2025. More micro-level data about investments and the future of self-driving Robo taxis are covered in the report. Also, as per MMR findings, the autonomous/self-driving car market holds a huge future in the forecast period and the detail is covered in the report.

Potential loss of privacy and licensing infrastructure

Self-driving vehicles are overflowing with highly advanced technology, which makes them so fascinating, but all of this technology is now excessively costly. Self-driving vehicles may ultimately be something that anybody can buy because, in general, technology becomes less expensive the longer it is available to the general public. However, the majority of businesses have not yet disclosed pricing for their autonomous vehicles.

The licensing system at the state and federal levels is also challenged by self-driving automobiles. With the manufacturers' claim to the contrary, it is up to government organizations to keep drivers safe. Our local auto licensing agencies must not only ensure that these vehicles live up to their promises, but also find a rapid and effective method for authorizing and managing them. Public safety may be at risk if modern technology and desire for these automobiles exceed our capacity to examine and approve them. Employing a self-driving car would provide a stranger the chance to observe your movements, according to firms developing the technology. Due to customer reaction, many businesses will probably keep away from this, but there has still been a significant loss of privacy.

Autonomous / Self-Driving Cars Market Segment Analysis:

by Component, the Autonomous / Self-Driving Cars Market is segmented into Camera Units, LiDAR, Radar Sensor, Ultrasonic Sensor, and Infrared sensors. Based on component type camera unit held the highest market share in 2022. Cameras are the most accurate way to capture images of the world in both photographs and videos, especially for self-driving automobiles. In order to provide a 360-degree vision of their surroundings, autonomous cars depend on cameras mounted on every side, including the front, back, left, and right. Some have a shorter range and a wider field of view, up to 120 degrees. Others focus on a narrow perspective to produce long-range images. Some cars even offer features with fish-eye cameras, which have very wide lenses and offer a panoramic view, to provide a complete image of what is behind the vehicle so that it can park itself.

Cameras have inherent limits, despite the fact that they deliver precise images. Although they are able to detect little features in the surroundings, it is necessary to compute the distances between items in order to know exactly where they are. In poor visibility situations like fog, rain, or the dark, it is also more challenging for camera-based sensors to detect things. due to these features boosting the self-driving market forecast period. numerous tier-1 suppliers and autonomous / self-driving car developers are concentrating on the development and adoption of AI-based cameras.

One of the largest manufacturers of camera systems for autonomous and self-driving automobiles, Robert Bosch, has created the AI-based camera MPC3 for these vehicles. The MPC3 represents a significant advancement toward autonomous or self-driving cars, one mostly driven by artificial intelligence. The Bosch team developed the camera using a multi-path strategy. Its engineers and programmers developed a software architecture, put it on a high-performance system-on-chip (SoC), with an integrated CPU, and combined traditional image-processing algorithms with AI-driven techniques.

by Mobility, based on mobility personal mobility held the maximum market share in 2025. Personal mobility is subdivided into commercial mobility. Commercial mobility is expected to grow fast during the forecast period. The commercial mobility category takes into account ride-sharing, robot-taxi, industrial transportation, and other commercial activities.

The introduction of robo-taxis is expected to offer up some new difficulties for mobility as a service model or for automobile ownership. Companies that manufacture both generic and robo-taxis are implementing cutting-edge production techniques. Testing for automobiles in robo-taxis is more stringent than for big transport vehicles. Waymo was one of the first businesses to charge passengers for trips in its self-driving Waymo One, which included human backup drivers. Thousands of Chrysler Pacifica minivans have been provided to Waymo by Chrysler. The partnership is expected to provide businesses working on or developing Robo-taxis access to a new revenue model. Some of the businesses selling autonomous vehicles as robot taxis are AutoX and Optimus Ride.

Robo-taxis are available from businesses including AutoX, Baidu, Waymo, EasyMile, Navya, Optimus Ride, and Yandex and may be utilized for passenger transportation. As one of the first companies to test customized autonomous cars for last-mile delivery services starting in 2020, Pony.ai. By 2022, the business also plans to launch a driverless robotic taxi service in California. Governments in developing nations are prepared to upgrade the traffic and transportation systems in cities. Governments are investing a lot of money in creating smart roads, smart traffic signal systems, stronger wireless connections, new road sensors, and better road signs due to the growing urbanization and greater adoption of smart cities.

Based on the Level of Autonomy, the Autonomous / Self-Driving Cars Market is segmented into Level 1, Level 2, Level 3, Level 4, and Level 5. Level 3 cars are capable of "environmental sensing" and autonomous decision-making, like as accelerating past a stationary object. Level 4 automation includes the capability for Level 4 vehicles to step in if something goes wrong or a system fails. In this way, these automobiles often don't need to contact people. An individual can still manually overrule, though.

Vehicles at Level 4 are capable of operating autonomously. But they can only do it in a small region while laws and infrastructure remain the same (usually in an urban environment where top speeds reach an average of 30mph). It's called geofencing. The majority of Level 4 cars on the road today are designed with ridesharing in mind. With Level 5 cars, the "dynamic driving task" is no longer necessary. Level 5 vehicles won't even have pedals for accelerating or braking or steering wheels. They will be unrestricted by geofencing, able to travel anywhere, and capable of carrying out any task that a skilled human driver can. Several regions of the world are testing fully autonomous vehicles, but none are presently accessible to the general public.

Autonomous / Self-Driving Cars Market Regional Insights:

The Asia Pacific region dominated the market with xx % share in 2025. The Asia Pacific region is expected to witness significant growth at a CAGR of xx% through the forecast period. The market for autonomous / self-driving cars is being driven by factors such as increased consumer demands for a safe, effective, and convenient driving experience, rising disposable income in countries, and strict safety rules throughout the globe. Due to increasing collaborations taken by Autonomous / Self-driving car technology providers in this region, the market in the Asia Pacific is expected to grow at the highest rate throughout the forecast period. China held the highest market share in 2025.

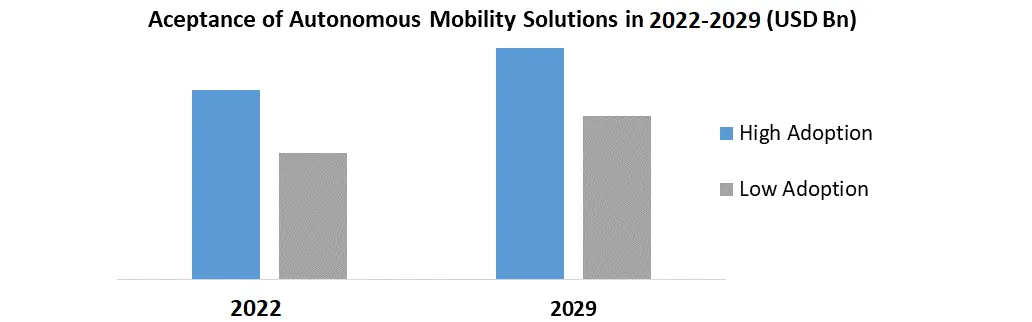

Self-driving vehicles may push China's automotive sector forward. Autonomous vehicles (AVs) will transform on-road driving, modify the automotive and transportation sectors, and extend from driverless cabs to automated cargo trucks. they think that AV companies in China, ranging from component vendors to mobility service providers, may generate billions of dollars in revenue within this environment of opportunity and risk. As per the MMR survey of the automotive market in china A high adoption rate of 62 percent will be reached by passenger vehicles utilized for mobility services like "robot-taxis," with private luxury vehicles (51 percent) and private mass-market automobiles following (38 percent). Due to the expected higher utilization of the autonomous vehicle (almost 24/7 operation) and cheaper labor costs, mobility services will take the lead (no drivers). Using the same logic, commercial vehicles (CVs) are adopted at a rate of 67 percent and city and county buses at 69 percent.

China’s automotive industry is high in demand due to software and service The mobility profit share in the Chinese autonomous vehicle market would increase by at least $60 billion as compared to its current value with the introduction of autonomous cars. With a profit share of $50 billion to $60 billion, the value chain's total profit share will continue to be dominated by the auto industry.

However, the revenues from mobility services will increase to 25 to 30 % of the whole profit pool (which includes cars, parts, mobility services, and fleet management) and may even exceed those from car sales, particularly if the MaaS market is less competitive (for example, if government cooperated with mobility players). AV technology and system integration, on the other hand, will create $15 billion to $20 billion in profits, or between 50 and 60 % of the whole auto-components profit share. Profit share will vary depending on the number of competitors. The alternative is that Robo-taxis will be run by regional government joint ventures. More details are covered in the report.

Massive investment by top key players

There are many investment possibilities to think about because self-driving cars will impact every area of the economy. The management of vehicle autonomy data and software, as well as the autonomous cars themselves, will heavily depend on the cloud, thus it is beneficial to invest in cloud computing companies. Since battery-powered drivetrains fundamentally rethink the design and build of cars, self-driving capabilities are also indissolubly linked with electric vehicles (along with the lithium manufacturing business supplying ingredients for battery technology).

Alphabet -- parent organization of Google is a top player in self-driving cars. Self-driving vehicles are all about data, especially gathering data from the roadways to develop an AI system to navigate a vehicle. All kinds of organizations manage autonomous car design and manufacture, train self-driving AI algorithms, and handle vehicle software upgrades using subsidiary Google Cloud. Waymo, a leading startup in driverless vehicles, is one of the investments in Alphabet.

Amazon is far more than an e-commerce giant Smart investors are aware that Amazon's success as a technology company is largely due to its development of AWS (Amazon Web Services), the first public cloud computing platform. AWS also includes a self-driving car section that aids automakers and other vehicle innovators in managing their autonomous driving data, as is to be expected with other cloud platforms. There's more, though. Additionally, Amazon owns Zoox, a start-up in autonomous ride-hailing that it bought in 2020. Beyond robotaxis and other consumer-facing automobile technologies, developing vehicle autonomy attracts Amazon.

Tesla’s work to accelerate the electric vehicle movement is undeniable, but its work on full self-driving capabilities is a bit more controversial. Autopilot, an advanced driver-assist system (ADAS) that includes adaptive cruise control and auto-steer that maintains the vehicle's lane, is standard equipment on every Tesla. More functions are included in the company's Full Self-Driving (FSD) upgrade package, but a driver must still be alert and prepared to take the wheel. Tesla is working to develop self-driving technology without lidar, and the company has said it would let other companies utilize Dojo to create autonomous vehicles as well.

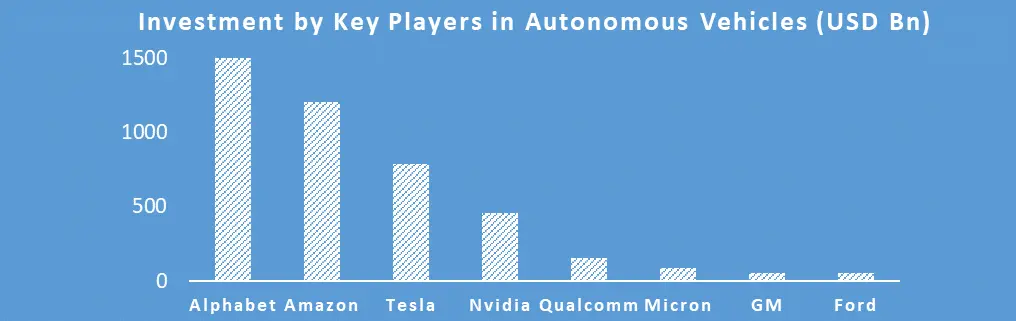

Leading companies and their investment in the self-driving car market are covered in the report.

| Company | Market Investment |

| Alphabet | $1.5 trillion |

| Amazon | $1.2 trillion |

| Tesla | $783 billion |

| Nvidia | $456 billion |

| Qualcomm | $156 billion |

| Micron | $83 billion |

| General Motors | $55 billion |

| Ford | $54 billion |

Strategic alliances and fresh market approaches are expected to grow in this new environment. While concurrently developing new skills, players could think about altering their organizational and go-to-market strategies. These players could look for new ways to raise and use cash as a result of the transformation brought on by developments in autonomous driving technology, including M&A. Players in good facilities are also going to be impacted.

Autonomous / Self-Driving Cars Market Recent Industry Developments (2025–2026)

| Date | Company | Development | Impact |

|---|---|---|---|

| 05 February 2026 | Waymo LLC | Completed a $16 billion funding round led by Alphabet and external investors like Sequoia Capital. | Elevated the company's valuation to $126 billion, solidifying its position as the world's most valuable Robotaxi entity. |

| 22 January 2026 | Toyota Motor Corporation | Launched the Arene OS software platform globally, debuting in the 2026 RAV4 model. | Integrates Toyota Safety Sense 4.0 with 5G connectivity to enable software-defined vehicle capabilities and over-the-air updates. |

| 09 December 2025 | Tesla, Inc. | Released the 2025 Holiday Update (v2025.44.25.1) featuring advanced FSD (Full Self-Driving) refinements. | Introduced Parked to Parked functionality and improved pothole avoidance for newer Hardware 4 (AI 4) vehicle platforms. |

| 23 October 2025 | General Motors (Cruise) | Announced a strategic expansion of its unsupervised autonomous testing program into secondary U.S. markets. | Aims to scale driverless ride-hailing services following rigorous safety protocol updates and regulatory clearance. |

| 22 September 2025 | Nissan Motor Co., Ltd. | Commenced public demonstrations of next-generation ProPILOT technology using Wayve AI Driver software in Tokyo. | Leverages Ground Truth Perception and next-gen LiDAR to handle complex urban driving scenarios ahead of a 2027 commercial launch. |

Autonomous / Self-Driving Cars Market Scope: Inquire before buying

| Autonomous / Self-Driving Cars Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 34 USD Mn |

| Forecast Period 2026-2032 CAGR: | 13.49% | Market Size in 2032: | 82.45 USD Mn |

| Segments Covered: | by Component | Camera Unit LiDAR Radar Sensor Ultrasonic Sensor Infrared Sensor |

|

| by Mobility | Shared Mobility Personal Mobility |

||

| by Level of Autonomy | L1 L2 L3 L4 L5 |

||

| by Vehicle Type | Passenger Cars Commercial Vehicles Robotaxis Autonomous Trucks Autonomous Buses and Shuttles |

||

| by Application | Ride-Hailing Services Logistics and Freight Transport Public Transportation Personal Use Military and Defense |

||

Autonomous / Self-Driving Cars Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Manufacturing Competitors in the Autonomous / Self-Driving Cars Market are:

1. Audi AG (Germany)

2. BMW AG (Germany)

3. Mercedes-Benz Group AG (Germany)

4. Volkswagen AG (Germany)

5. Jaguar Land Rover Limited (UK)

6. Groupe Renault (France)

7. Volvo Car Corporation (Sweden)

8. 2GetThere B.V. (Netherlands)

9. Aptiv PLC (Ireland)

10. Ford Motor Company (US)

11. General Motors Company (US)

12. Waymo LLC (US)

13. Tesla, Inc. (US)

14. Honda Motor Co., Ltd. (Japan)

15. Nissan Motor Co., Ltd. (Japan)

16. Mitsubishi Motors Corporation (Japan)

17. Toyota Motor Corporations (Japan)

18. Beijing Idriveplus Technology Co., Ltd. (China)

19. BYD Auto Co., Ltd. (China)

20. SAIC Motor Corp. (China)

21. Tata Elxsi (India)

22. Hyundai Motor Group (South Korea)