Automotive Wheel Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

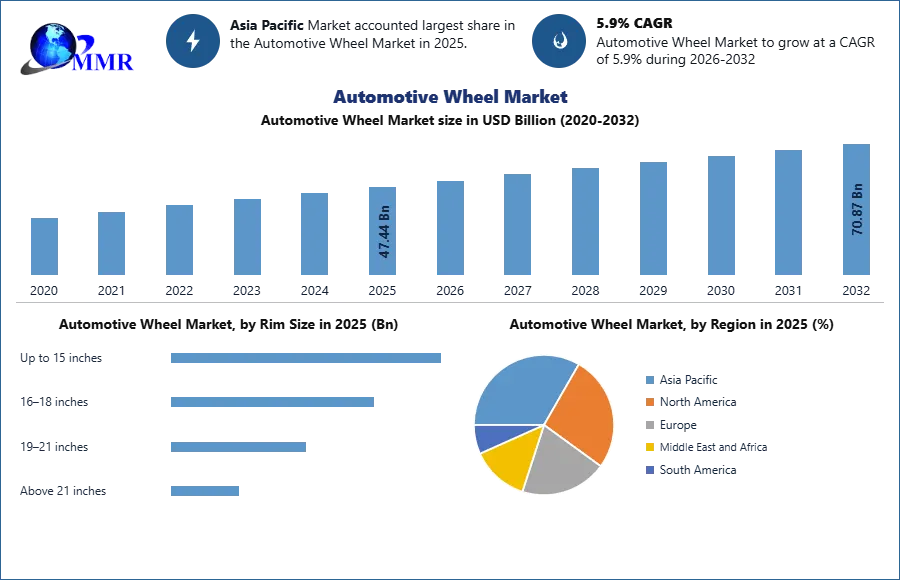

The Automotive Wheel Market size was valued at USD 47.44 Billion in 2025 and the total Automotive Wheel revenue is expected to grow at a CAGR of 5.9% from 2026 to 2032, reaching nearly USD 70.87 Billion.

Automotive Wheel Market Overview:

The digital era, also known as the 4.0 industry, is present in all sectors of the economy, making significant contributions to its growth. The automotive industry is undergoing transformation, which is affecting all of its sub-industries, including the automotive tire business. The industry is witness to a process in which huge corporations no longer offer simple vehicles or tires, but instead, use new technology and digitalization to sell complicated services suited to clients' demands. Connectivity, mobility, and autonomy have emerged as key pillars in the development of such solutions integrated into the existing market.

The tire sector is today classified as volatile, as it is strongly tied to automotive manufacturing, but also other variables such as raw materials, their availability, and their unpredictable prices. Companies now operating in the sector face not just financial and manufacturing constraints, but also a large surge of new rivals from Asia, namely China. The ambitions of this industry, the newest generation of techniques utilized, and the implementation of the vehicle tire production processes all highlight the significance of this field. As a result, new technology and innovation play a crucial role in the whole automotive sector, compelling firms to reconsider their business strategies.

Report Scope:

The Automotive Wheel market is segmented based on Rim Size, Material, Vehicle, End-User, and Region. The growth of various segments helps report users in acquiring knowledge of the many growth factors expected to be prevalent throughout the market and develop different strategies to help identify core application areas and the gap in the target market. The report provides an in-depth analysis of the market and contains meaningful insights, facts, historical data, and statistically supported and industry-validated market statistics. It also includes estimates based on an appropriate set of assumptions and methodologies.

A bottom-up approach has been used to estimate the market size. Key Players in the Automotive Wheel market are identified through secondary research and their market revenues are determined through primary and secondary research. Secondary research included a review of annual and financial reports of leading manufacturers, while primary research included interviews with important opinion leaders and industry experts such as skilled front-line personnel, entrepreneurs, and marketing professionals. Some of the leading key players in the global Automotive Wheel market include Iochpe-Maxion, Superior Industries International, and Accuride Corporation. They are continuously strategizing on mergers and acquisitions, strategic alliances, joint ventures, and partnerships for the growth of their market shares.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Automotive Wheel Market Dynamics:

The varying rim sizes across regions create scope for product innovation:

In Europe, 16- and 17-inch wheels are standard on top-selling passenger vehicles, although 18- and 19-inch wheels are more common in the US market. The continuous premiumization trend in India will be a significant impetus for alloy wheel companies and an important opportunity for overseas manufacturers, as competition is currently relatively restricted. In the United States, where it has been the best-selling vehicle for 44 straight years, the F-150 has up to five alloy wheel choices, with sizes ranging from 17 to 22 inches. Silver-painted aluminum wheels are popular with other OEMs, and there is an increasing demand for machined aluminum wheels. Due to the prevalence of sedans in China, 14-16-inch silver painted alloy wheels are more prevalent in the top ten best-selling automobiles.

More than 90% of top-selling automobiles in Japan have 14-16 inch wheels, owing to a high percentage of kei cars. 17-inch wheels are commonly found on MPVs and SUVs such as the Toyota Vellfire and Subaru Forester. Wheel manufacturers are responding to fleets' increased use of onboard telematics by creating solutions that integrate with tires and vehicle systems.

The regional laws and regulations to impact market growth:

The production of vehicle tires is governed by a variety of variables such as:

Instability of raw material prices, as well as utilities entering the manufacturing process, such as steel, natural gas, and oil;

Global business growth and improved economic conditions;

Imposing new tariffs or revising existing ones, including antidumping and countervailing duties on imported tires from China or the United States;

Capital and financial market insecurity

In Romania, for example, the introduction of required winter tires was another contributor to raising the demand for tires. Drivers must have winter tires on their vehicles when traveling on public roads covered in snow or ice, according to the Law. At the European level, there are laws governing the territories that have implemented the law - according to the specialist site Oponeo.co.uk, 16 countries require winter tires.

Open markets are critical to the future outlook:

Local regulations on foreign involvement, joint venture arrangements, and market access have a significant impact on how multinational automakers compete in emerging countries such as China, Brazil, and Mexico. While robust growth is simply the "plus side" of high volatility, the car sector has relied on rising demand in those areas for over a decade. In several of these markets, automotive sales growth slowed in 2020, although long-term prospects remain bright. China's significance in the car sector extends far beyond local sales. Many automakers are seeking economies of scale/proximity by meeting high local demand with local plants, but also by exploiting China as an Asian assembly center. China now produces more automobiles than any other country on the planet. If China modifies its present laws for foreign corporations, the impact on the automotive sector would be significant, whether the changes are more liberal or more restrictive.

Automotive Wheel Market Segment Analysis:

By Material, the alloy segment is expected to grow at a CAGR of 4.8% during the forecast period. Alloy wheels are frequently acquired for cosmetic purposes (visible repairs), even though the lesser alloys used are typically not corrosion-resistant. Alloys enable the adoption of appealing bare-metal finishes, which must be sealed with paint or wheel covers. Even if well covered, the wheels in use will rust after 3 to 5 years, however, refurbishment is now widely available at a price. Alloy wheels are prone to galvanic corrosion, which can cause tire air leaks if proper precautions are not followed. Furthermore, when bent, alloy wheels are harder to fix than steel wheels, although their greater price generally makes repairs less expensive than replacement.

Because alloy wheels are more expensive to build than normal steel wheels, they are sometimes sold as optional add-ons or as part of a more expensive trim package rather than as standard equipment. However, alloy wheels have grown much more prevalent, now being offered on economy and subcompact automobiles, as opposed to a decade ago when alloy wheels were frequently not factory choices on low-cost vehicles. Alloy wheels have traditionally been standard on higher-priced luxury or sports automobiles, with larger-sized or "special" alloy wheels available as extras. Because alloy wheels are expensive, they are appealing to thieves; to combat this, automakers and dealers frequently add locking lug nuts or bolts that require a special key to remove.

Automobile owners who desire lighter, more aesthetically appealing, rarer, and/or larger wheels on their automobiles can choose from a broad assortment of alloy wheels ranging in size from 14 to 15 inches to 16, 17, 18, 19, 20, 21, 22, 24, 26, and 28 inches. With the bigger alloy wheels came alloy Tru-Spinners, which were intrinsic to the alloy wheel and would free-spin once the alloy wheel came to rest. Some Tru-Spinner alloy wheels would also spin reverse while moving forward.

Automobile owners who desire lighter, more aesthetically appealing, rarer, and/or larger wheels on their automobiles can choose from a broad assortment of alloy wheels ranging in size from 14 to 15 inches to 16, 17, 18, 19, 20, 21, 22, 24, 26, and 28 inches. With the bigger alloy wheels came alloy Tru-Spinners, which were intrinsic to the alloy wheel and would free-spin once the alloy wheel came to rest. Some Tru-Spinner alloy wheels would also spin reverse while moving forward.

Although replacing typical steel wheel and tire combinations with lighter alloy wheels and perhaps lower profile tires might result in improved performance and handling, this is not always the case when larger wheels are used. Car and Driver research involving a variety of various-sized alloy wheels ranging from 16 to 19 in (41 to 48 cm) all supplied with the same make and type of tires revealed that bigger wheels reduced acceleration and fuel efficiency. They also remarked that the bigger wheels had a detrimental impact on ride comfort and noise.

Automotive Wheel Market Regional Insights:

Because of greater fleet utilization, fewer cars will be required in the future. According to PwC Autofacts, Europe's present inventory of little over 280 million automobiles may be reduced to roughly 200 million by 2030. This would represent a drop of more than 25%. In the United States, a 22% decline to 212 million automobiles is expected. Despite increased utilization, the inventory in China might increase by over 50% in the same period due to different market conditions.

Despite declining inventories, automobile sales would rise noticeably. Vehicles utilized in a typical manner will be in the inventory for a rather long time. In contrast, autonomous cars particularly shared autonomous vehicles, will be replaced much more frequently, resulting in higher sales statistics. Across Europe, new car sales might increase by 34% over the transition period, from roughly 18 million to slightly more than 24 million units. PwC Autofacts forecasts a 20% increase and over 22 million new automobile sales in the United States by 2030. China is expected to boost sales by more than 30% to 35 million units.

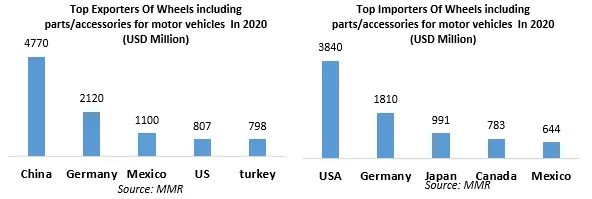

List of Top 10 countries by motor vehicle production (In Units)

| Sr. No. | Country | 2021 | 2020 |

| 1. | China | 26,082,220 | 25,225,242 |

| 2. | United States | 9,167,214 | 8,822,399 |

| 3. | Japan | 7,846,955 | 8,067,557 |

| 4. | India | 4,399,112 | 3,490,000 |

| 5. | South Korea | 3,462,404 | 3,506,774 |

| 6. | Germany | 3,308,692 | 3,742,454 |

| 7. | Mexico | 3,145,653 | 3,176,600 |

| 8. | Brazil | 2,248,253 | 2,014,055 |

| 9. | Spain | 2,098,133 | 2,268,185 |

| 10. | Thailand | 1,685,705 | 1,427,074 |

Already, it is apparent that the car sector will begin to invest less in the product range. PwC Strategy estimated that investment in this industry might shrink by 19% by 2025 as part of the Global Innovation research. This, however, is not always a bad omen. The survey concluded that firms who invest their R&D expenditure in software solutions rather than product lines are already growing faster than their competitors.

Manufacturers and suppliers, in particular, face shrinking margins between 2020 and 2025, while also investing extensively in customer-oriented developments. Traditional automakers must decide how much they are willing to invest in mobility services to avoid a deterioration in their primary business. At the same time, more investment in manufacturing capacity for the essential "hardware" is required, and enterprises that adopt flexible and scalable concepts now will be able to play an active part in defining the future of the industry.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 29 November 2026 | European Commission | The Euro 7 Regulation (EU) 2024/1257 went into effect for new M1/N1 vehicle types, mandating stricter standards for wheel coatings. | This regulation forces manufacturers to adopt advanced, durable surface treatments capable of withstanding increased thermal cycling and reducing particulate-abrasion. |

| 08 December 2025 | Superior Industries International | The company completed a debt-to-equity conversion with investors including Oaktree Capital Management and appointed Michael Dorah as CEO. | The restructuring significantly strengthens the company’s balance sheet, enabling increased investment in regional supply capabilities and long-term strategic expansion. |

| 03 November 2025 | Iochpe-Maxion (Maxion Wheels) | Announced a strategic expansion in South America by acquiring a 50.1% stake in Polimetal, Argentina and redeploying global assets to Brazilian plants. | This initiative increases aluminum wheel production capacity in the Mercosur region to meet rising OEM demand for lightweight passenger car components. |

| 15 September 2025 | Alcoa Corporation | Finalized the installation of low-carbon smelting technology at key facilities to produce "Eco-Ultra" aluminum for forged wheel applications. | The development allows the company to capture the growing sustainable OEM market by offering wheels with significantly lower lifecycle CO2 emissions. |

| 12 June 2025 | Carbon Revolution Limited | Commercialized a new autoclave-free resin transfer molding process, reducing the production cost of carbon-fiber wheels by over 20%. | By lowering costs, this technology accelerates the adoption of carbon-fiber wheels beyond luxury segments into high-volume electric vehicle models. |

Automotive Wheel Market Scope: Inquire before buying

| Automotive Wheel Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 47.44 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.9% | Market Size in 2032: | 70.87 USD Billion |

| Segments Covered: | by Rim Size | Up to 15 inches 16–18 inches 19–21 inches Above 21 inches |

|

| by Material | Steel Wheels Aluminum Alloy Wheels Carbon Fiber Wheels Others |

||

| by Vehicle | Passenger Vehicles Light Commercial Vehicles Heavy Commercial Vehicles |

||

| by End-User | OEM Aftermarket |

||

Automotive Wheel Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Automotive Wheel Market Report in Strategic Perspective:

- Iochpe-Maxion

- CITIC Dicastal

- Ronal Group

- Superior Industries International

- Borbet GmbH

- Accuride Corporation

- Topy Industries

- Enkei Corporation

- Alcoa Corporation

- Steel Strips Wheels Ltd.

- Zhejiang Wanfeng Auto Wheel Co., Ltd.

- Central Motor Wheel of America

- YHI International Limited

- Lizhong Group

- Zhejiang Jinfei Kaida Wheel Co., Ltd.

- Foshan Nanhai Zhongnan Aluminum Wheel Co., Ltd.

- BBS Autotechnik GmbH

- OZ S.p.A

- RAYS Co., Ltd.

- Carbon Revolution Limited

- Super Alloy Industrial Co Ltd

- Wheel Pros LLC

- American Eagle Wheels Corp

- ALCAR Holding

- Jingu Group