Automotive Suspension Market Size by System, Component, Suspension Type, Vehicle Type, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2034

Overview

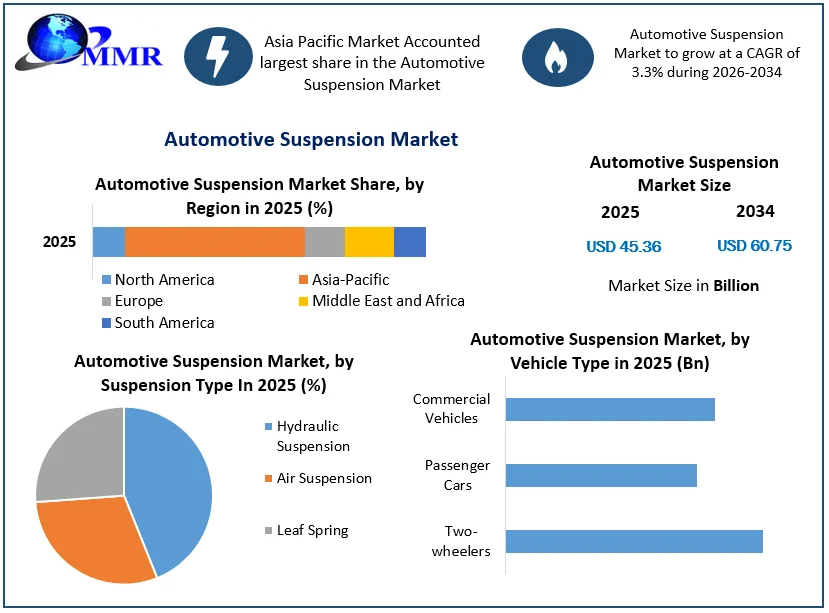

The Automotive Suspension Market size was valued at USD 45.36 Billion in 2025 and the total Automotive Suspension Market size is expected to grow at a CAGR of 3.3 % from 2026 to 2034, reaching nearly USD 60.75 Billion in 2034.

The Automotive Suspension Market report has covered analysis in terms of both quantitative and qualitative data with a forecast period of the report extending from 2026 to 2034. The report is prepared to take into consideration various factors such as Product pricing, Products or services, market penetration at both country and regional levels, Country GDP, market dynamics, major players, consumer buying behavior, and many others. The report is divided into various segments to offer a detailed analysis of the market. The market outlook section gives a detailed analysis of market evolution, growth drivers, restraints, opportunities, and challenges, Porter’s 5 Forces, Pestel, SWOT analysis Framework, macroeconomic analysis, value chain analysis, and pricing analysis.

Automotive Suspension Market Growth and Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Automobile suspension is a system of interconnected components that connect a vehicle to its wheels. It includes springs, shock absorbers, and linkages. It connects a vehicle to its wheels, ensuring a smooth ride, stable handling, and good control. The main objective of a suspension system is to enhance passenger comfort by reducing the impact of road imperfections, and vibrations, ultimately providing a smoother ride.

1.According to MMR, the world exports a major part of its automotive suspension to countries such as Australia, India, and the United States.

Major companies in the Automotive Suspension Market include Friedrichshafen AG, Continental AG, Mando Corporation, ThyssenKrupp AG, Morelli Corporation, KYB Corporation, Tenneco Inc., Banterer International AG, NHK Spring, and Sogefi S.P.A.. Product launches have been an important strategic step for the major players in the Automotive Suspension Market to remain competitive in the global market.

North America is the fastest-growing region in the Automotive Suspension Market with a large market share of about XX% in 2025 and is expected to grow at a CAGR of 3.3 % during the forecast period and maintain its dominance by 2034. North America is the fastest- growing thanks to increasing innovation in the automotive industry leading to the adoption of new suspension technologies like active suspension systems, which improve handling. Consumer preferences to increasing interest in comfortable rides and good handling, especially in SUVs and luxury cars.

Automotive Suspension Market Dynamics:

Increase in demand for luxury & comfort in vehicles

The increase in demand for high-end features and convenience in cars is linked to various factors in the current automotive industry. With advancements in technology and design, consumers are increasingly looking for vehicles that not only provide efficient transportation but also enhance the feeling of luxury and convenience. As urbanization continues, people spend more time in their vehicles, turning them into personal sanctuaries where comfort and style are essential. Globally, with increasing disposable incomes, a larger group of consumers is giving importance to luxuries and prestige in that the improved upscale features model in vehicles. Automobile manufacturers are incorporating luxurious features into their vehicles at different price ranges, from opulent interiors and innovative entertainment systems to advanced driver-assistance technologies, in response to the growing demand for luxury in the market. Modern consumers expect a continuous balance of performance, sophistication, and convenience in their automotive experience, leading to increased demand for luxury and comfort in vehicles. In automated vehicles, an air compressor allows for precise adjustments to the ride height and ensures a smooth and stable ride despite the car performing automated maneuvers.

Automotive Suspension Market Restraints:

High-cost expenses linked to installing new or advanced suspension systems result in a high increase in vehicle costs, which is expected to hamper the growth of the market. The insertion of premium type of features in vehicles poses added costs to consumers through hardware, applications, and telecom service charges are constraining market growth The serviceability of vehicles with advanced components and sensors is challenging and requires skilled workers. The complex structure of these systems reduces the service life of vehicles, resulting in high initial costs and a negative impact on the growth of the global automotive suspension market.

Automotive Suspension Market Segment Analysis:

Based on the System, the Passive system segment holds the largest market share of about 42.4% in the Automotive Suspension Market in 2025. According to the MMR analysis, the segment is expected to grow at a CAGR of 3.3 % during the forecast period and maintain its dominance till 2034. The passive system segment is attributed to its wider use across various vehicles, from passenger cars to commercial vehicles. The popularity of passive systems in the market is oues to their simple design and lower maintenance costs, making them an attractive choice for manufacturers.

The growing demand to improve the quality of rides and occupant comfort is a significant factor, which driving the market for active suspension systems. The high-end luxury & sports cars and some medium-range cars with few commercial vehicles mainly use active suspension systems. The active system acquires a high cost but is the most advanced and comfortable suspension system. The active systems include various brand names, such as PASM Porsche Active Suspension Management by Porsche. Active and semi-active suspension systems provide good comfort and handling, but their higher pricing inhibits the growth of the market.

Based on the Suspension type, the Leaf Spring accounted for the largest market share in the Automotive Suspension Market in 2025 and is expected to maintain its dominance till 2034. The dominance of Leaf Springs in the automotive suspension market is oues to their durability, cost-effectiveness, and commonly used in various vehicle types like passenger cars, trucks, and containers. Leaf springs offer strong support, effectively dampen shocks, and require less maintenance, making them a preferred choice for manufacturers and consumers. Advancements in material technology have increased the performance and lifespan of leaf springs, solidifying their position as a leading suspension component in the automotive industry.

Automotive Suspension Market of Regional Analysis:

Asia Pacific dominates the Automotive Suspension Market, which holds the largest market share accounting for 34.6% in 2025, the region is expected to grow during the forecast period and maintain its dominance by 2034. Asia Pacific is a dominating region thanks to cost-effective manufacturing capabilities in countries like China, Japan, and South Korea. The rapid development of the automotive suspension systems market in the Asia Pacific is being driven by increasing vehicle production. Asia Pacific emerges as the top-selling region in the automation suspension market, showcasing robust demand and significant growth. The Asia Pacific region is experiencing significant growth in the automotive suspension systems market, rising disposable incomes, urbanization and development in infrastructure contribute to increasing regional demands for both passenger and commercial vehicles. China is a magnet for investments from automotive OEMs and suppliers driving the growth and acceptance of suspension systems. Government initiatives promoting vehicle safety and emissions reduction also influence the adoption of advanced suspension technologies in the region. Asia Pacific dominates both import and export activities in the automation suspension market, highlighting its significant position as a key centre for manufacturing and distribution in the region.

Europe presents as a mature market for the Automotive Suspension Market holds a market share of XX % and is significantly growing during its forecast period. Europe has a strong presence of automotive OEMs and suppliers. The automotive suspension market growth is driven by technological advancements, replacement demand from a large existing vehicle fleet, and consumers prioritizing comfort and handling performance is leading to demand for advanced suspension systems in passenger cars.

Competitive Landscape for the Automotive Suspension Market:

A key Company's strategy is its constant commitment to research and development (R&D) to maintain a leading position in technological development. The competitive landscape of the Automotive Suspension Market includes a mix of established companies focusing on research and development to enhance efficiency and performance. Product launches have been an important strategic step for the major players in the Automotive Suspension Market to remain competitive in the global market.

The leading companies are adopting strategies such as acquisition, agreement, expansion, partnership, contracts, and product launches to strengthen their market position.

1. April 2023- ZF Friedrichshafen AG reported opening a new research and development center for car suspension systems. The center is in the United States, and its main job will be creating new self-driving car technologies.

2. May 2023- Hitachi Ltd. said that it had made a new type of active suspension system that uses artificial intelligence. The new system is meant to make the ride more comfortable and improve the way the car handles all driving situations.

3. May 2023, LG Electronics Inc. launched a connected vehicle alarm system, LG My Car Alarm Service. It integrates with Infoconn, the connected car service as the mobile application of KG Mobility & developed in response to increasing demand from automotive companies and consumers for vehicle-integrated mobility services.

4. October 2022, Continental AG developed a connected infotainment box that enables the use of digital services such as e-calls, turn-by-turn navigation, and stolen vehicle tracking. Along with that, it provides optional features such as stolen vehicle tracking.

5. July 2022, Thales developed & offers a secure connectivity solution to bring drivers, passengers, and maintenance teams greater access to useful information. This seamless connectivity management solution enables drivers and passengers to access e-Call (automatic EU emergency call in case of an accident), remote software updates

6. July 2022 – ZF Friedrichshafen AG showcased its new EasyTurn suspension, allowing incredible mobility for vehicles to improve their turning. This unique design allows the vehicle to rotate its front wheels up to 80 degrees, drastically reducing the difficulties in rotating the wheels during parallel parking.

Automotive Suspension Market Recent Development

| Exact Date | Company Name | Recent Industry Development | Strategic Impact / Market Relevance |

|---|---|---|---|

| 24 June 2026 | Tenneco Inc. | Tenneco completed a fully automated production line at its Suzhou facility in China to manufacture Monroe® Full Active Suspension (FAS) actuators for new energy vehicles. | The expansion accelerates local production of electronically controlled damping systems, targeting rapid adoption in high-end electric vehicles across the Asian region. |

| 21 February 2025 | Gabriel India Limited | Gabriel India signed a technical agreement with Tractive Suspension BV granting exclusive rights to produce and distribute TracTive's electronic suspension adjustment technologies in India. | The partnership drives localized production of advanced adaptive dampers, helping the company meet growing demand for high-performance automotive chassis systems. |

| 12 May 2025 | Gabriel India Limited | Gabriel India acquired key manufacturing assets from Marelli Motherson Auto Suspension Parts Pvt. Ltd., a joint venture between Marelli and Samvardhana Motherson. | The strategic asset acquisition significantly boosts Gabriel's production capacity for shock absorbers and gas springs, solidifying its market leadership. |

| 15 April 2025 | Marelli | Marelli was awarded the 2025 Automotive News PACEpilot Award in Detroit for its groundbreaking Fully Active Electromechanical Suspension system. | The recognition underscores industry transition toward fluidless active chassis controls and intelligent electronic suspension systems. |

| 03 November 2025 | China Automotive Systems, Inc. | China Automotive Systems signed a strategic cooperation MoU with KYB-UMW to establish joint manufacturing operations at the new SP25 facility in Malaysia. | The alliance expands regional manufacturing capability for integrated chassis and suspension systems across ASEAN markets. |

Automotive Suspension Market Scope: Inquire before buying

| Automotive Suspension Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 45.36 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 3.3% | Market Size in 2034: | US $ 60.75 Bn. |

| Segments Covered: | by System | Active Passive Semi-active |

|

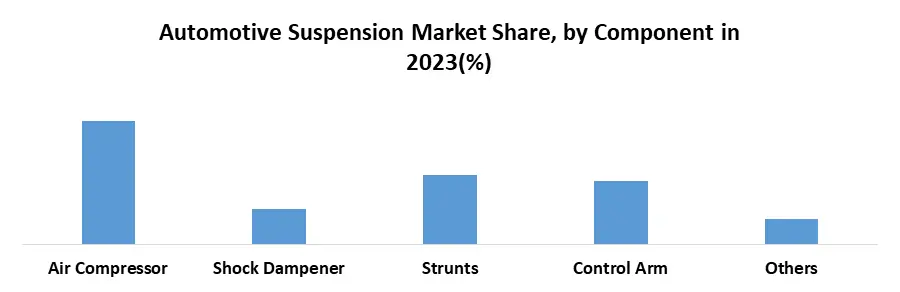

| by Component | Air Compressor Shock Dampener Struts Control Arm Others |

||

| by Suspension Type | Hydraulic Suspension Air Suspension Leaf Spring |

||

| by Vehicle Type | Two-wheelers Passenger Cars Commercial Vehicles |

||

Automotive Suspension Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Automotive Suspension Market Key Players:

The Automotive Suspension Market encompasses the design, manufacturing, and sales of the interconnected mechanical, hydraulic, and electronic components that link a vehicle's wheels to its structure. Its primary purpose is to absorb road shocks, support vehicle weight, and maintain tire contact to ensure optimal handling and passenger comfort.

| Company Name | Headquarters | Core Competencies |

| Tenneco Inc. | United States | Shock absorbers, struts, suspension systems, and ride performance technologies (Monroe brand) |

| ZF Friedrichshafen AG | Germany | Chassis systems, active suspension, steering systems, and vehicle dynamics technologies |

| KYB Corporation | Japan | Hydraulic shock absorbers, suspension systems, steering dampers, and ride control technologies |

| Hitachi Astemo, Ltd. | Japan | Advanced suspension systems, chassis control, steering systems, and vehicle dynamics technologies |

| Marelli Holdings Co., Ltd. | Japan | Suspension systems, chassis technologies, and integrated automotive components |

| Sogefi S.p.A. | Italy | Suspension components, coil springs, air springs, and chassis solutions |

| NHK Spring Co., Ltd. | Japan | Coil springs, stabilizer bars, suspension springs, and precision automotive components |

| Benteler International AG | Austria | Chassis modules, suspension components, and lightweight automotive structures |

| BWI Group | China | Active suspension systems, semi-active suspension, and chassis control technologies |

| HL Mando Corporation | South Korea | Suspension systems, braking systems, steering systems, and vehicle control technologies |

| Gabriel India Limited | India | Shock absorbers, struts, front forks, and ride control products |

| FOX Factory Holding Corp. | United States | High-performance suspension systems, shocks, and off-road vehicle suspension technologies |

| Hendrickson USA, L.L.C. | United States | Heavy-duty suspension systems, air suspensions, axle systems, and commercial vehicle solutions |

| Rassini S.A.B. de C.V. | Mexico | Leaf springs, coil springs, suspension components, and lightweight chassis technologies |

| BILSTEIN | Germany | High-performance shock absorbers, damping technologies, and suspension systems for OEM and aftermarket applications |

Frequently Asked Questions:

1] What is the growth rate of the Automotive Suspension Market?

Ans. The Automotive Suspension Market is expected to grow at a CAGR of 3.3 % during the forecast period of 2026 to 2034.

2] Which region is expected to hold the highest share in the Automotive Suspension Market?

Ans. Asia Pacific is expected to hold the highest share of the Automotive Suspension Market.

3] What is the market size of the Automotive Suspension Market?

Ans. The Automotive Suspension Market size was valued at USD 45.36 billion in 2025 reaching nearly USD 60.75 billion in 2034.

4] What is the forecast period for the Automotive Suspension Market?

Ans. The forecast period for the Automotive Suspension Market is 2026-2034.

5] What segments are covered in the Automotive Suspension Market report?

Ans. The segments covered in the Automotive Suspension Market report are based on system, component, suspension, and Vehicle Type.