Automotive Market in UK - Industry Structure Evaluation, Demand Drivers Analysis, Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2029

Overview

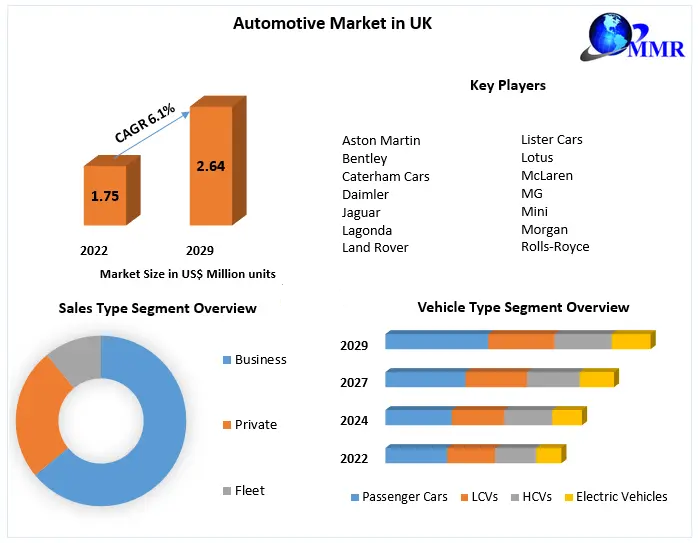

Automotive Market in UK was accounted at 1.75 Mn. units in 2022. Automotive Market in UK size is estimated to grow at a CAGR of 6.1% over the forecast period.

Automotive Market in UK Overview:

In response to COVID-19 and repositioning for BREXIT repercussions, the UK automotive sector is facing some of the most significant difficulties in its history. Many problems remain unanswered in the automobile sector due to the interdependence of UK manufacturers and EU partners.

Original equipment manufacturers' supply lines have been disrupted, underlining their vulnerability and reliance on non-UK areas. Cash flow and the ever-present pressures of sustainability have also increased. Furthermore, a drop in client trust is affecting new automobile sales. To fight this, dealerships are moving at digital solutions, and the market will be further disrupted by digital-first merchants and new virtual automobile purchase experiences.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

2022 is considered as a base year to forecast the market from 2023 to 2029. 2022’s market size is estimated on real numbers and outputs of the key players and major players across the globe. Past five years' trends are considered while forecasting the market through 2029. 2020 is a year of exception and analysis especially with the impact of lockdown by region.

Automotive Market in UK Dynamics:

The government has set lofty targets to reach Net Zero while also levelling the country by distributing skills, resources, and opportunities. Both goals are centered on the automotive industry. Moving away from the Internal Combustion Engine (ICE) is a critical next step on the UK's journey to Net Zero, and the UK has set one of the most aggressive objectives for phasing out ICE vehicles, with a passenger car end-of-sale date of 2030. In locations where genuinely skilled jobs are few and far between, the automotive sector employs skilled employees of all kinds - from PhDs in design to apprenticeships and BTECs in engineering.

While the cost of producing zero-emission vehicles is decreasing, it is not fast enough for the sector to meet the 2030 target while maintaining its global market share and production volume. Unlike other major nations, the UK has yet to match its ambition with equal investment in battery manufacturing incentives, charging networks, and affordable sustainable energy. According to independent researchers, the UK will only have 12 GWh of lithium-ion battery capacity by 2025, compared to 164 GWh in Germany, 91 GWh in the United States, and 32 GWh in France.

Bringing the United Kingdom up to par:

The automotive industry directly contributes £15 billion in GVA to the UK economy, with the majority of the value created outside of the South East. We predict that if the automotive industry did not exist, the economic difference between London and the North East would widen by 9%, and the gap between London and the West Midlands would widen by 3%. Over 80% of cars and 60% of commercial vehicles produced in the UK are exported, with the UK selling into 150 markets across the world. The automotive industry is the UK's most important source of goods exports.

Export volumes are down in absolute terms in all regions, including the EU, North America, Asia, Europe (outside the EU), Oceania, and Africa. Despite a -2.5% loss, the EU continues to be the most important market for UK manufacturers, with North America coming in second with a -2.7% decline. Exports to Asia and non-EU European countries were also higher than the previous year on a percentage basis. Because of the smaller year-on-year loss, non-EU European countries might be regarded the more stable export zone, but Asia has two highly important growth markets in China and South Korea.

However, when looking at the total volume of the UK's export footprint, more than 80% of automobile exports are sent to the broader European region (EU, other Europe) and North America, highlighting the importance of these regions as significant market centres. Unless growth in Asian markets compensates for the loss of Honda's sales in the United States as a result of the company's decision to stop producing cars in the UK, the EU and other European countries will likely acquire an even higher share of UK car exports in the future.

Trends in Market:

The UK vehicle market sought to rebound from the pandemic collapse of 2020 this year, reporting positive results only in Q2 because to the extremely low levels reached in Q2 2020, while all other quarters saw double-digit declines. The national automobile sector was at the pinnacle of its glory when the BREXIT referendum was held in 2016. Following five years of straight growth, the light vehicle market reached an all-time high of 3.06 million units in that year, making it the fourth largest in the world.

Following the vote, the industry's path matched that of the British economy, and a protracted period of decline began. Indeed, the light vehicle market shrank in both 2017 and 2018, while the rest of Europe grew steadily, with 2.72 million units sold in 2018, 2.36 of which were car passengers. With 2.64 million units sold in 2019, registrations were at their lowest point in the prior five years. The finalized BREXIT process has raised concerns about the economy's prognosis, which has had a significant impact on the relevant automotive industry, as well as fears that production activity wilal migrate from the UK to the continent, as Honda and JLR have already determined. In 2020, sales totaled 1,631,064, a decrease of 29.4% from the previous year.

The year 2021 began badly for the UK market, with 425,525 units sold in Q1, a 12% fall in sales compared to Q1 2020, however Q2 sales soared by 185.1%, with 484,448 units sold. With 406,641 units sold in Q3, sales began to tumble in double digits again, falling 31.1%, followed by a 14.7% drop in Q4 with only 330,567 units sold. Indeed, full-year sales for 2021 were 1.65 million, representing a 1% rise over 2019.

Competitive landscape of Automotive Market in UK (2021):

In terms of brand share, the new leader Volkswagen (-0.3%) lost 0.1% market share this year, while Audi (+9.4%) gained 0.5%. BMW stayed in third place, with a 1% rise. Ford, the previous leader, had the poorest result, plunging 23.9%, followed by Toyota, which gained 9.9% and moved up two ranks.

Mercedes dropped two ranks and plummeted 11.7%, followed by Opel, which dropped one slot and sank 4.2%, and Kia, which jumped one spot and increased sales by 28.7%. Topping the list is Hyundai, which has risen four ranks this year, with a gain of 46.7%, and Nissan, which has dropped two spots with a loss of 4.8%. The Opel Corsa (-14.2%) is the most popular vehicle this year, with 40,914 units sold, followed by the Tesla Model 3 (up 11 positions), which gained 58.2% with 34,783 new sales. The Ford Focus (-16.9%) rounds out the top three, moving one rank to 32,704 units sold.

Automotive Market in UK Segment Analysis:

The Automotive Market in UK is being driven by the Passenger cars Segment:

Based on vehicle type, market is segmented into passenger cars, commercial vehicles, and Electric vehicles. Passenger cars segment is accounted for 60% market share owing to increasing penetration of Volkswagen and Ford motor company’s passenger vehicles on the UK roads. Moreover, UK has higher production capacity of passenger cars rather than commercial vehicles as well as EVs. According to SMMA, 990,000 units were sold in 2021 registering 12% increase than 2022 with YOY rate of 18%.

On the plus side, British production of battery electric vehicles and hybrid automobiles (cars with both a combustion engine and a battery) set a new high in 2021, accounting for over a third of all cars produced in November and more than a quarter (26%) for the year.

Battery electric vehicle manufacturing increased by 53% to 10,359 units in November, reaching a new high of about 14% of total production, more than double the level a year ago. Nissan, MINI, and the London Electric Vehicle Company, all based in the United Kingdom, produced over 60,000 zero-emission vehicles in 2021. However, UK battery production is trailing behind substantial investment across the EU, which is seeking to be battery-independent by 2026 and has formed the European Battery Alliance with seven countries. While only one battery "gigafactory" has been confirmed in the UK, at least 15 are now under construction in countries such as Sweden, France, Germany, Hungary, and Poland.

Based on Sales Type, market is diversified into Private, Fleet and Business type. Fleet segment is dominating the market with 53.3% market share. Private and Business segments accounted for 44.1% and 2.6% market share in 2022. It is classified as a fleet sale if the car is being registered by a company that operates a fleet of 25 or more vehicles. This includes dealer demonstrators and automobiles leased through Mortability.

The objective of the report is to present a comprehensive analysis of the global Automotive Market in UK to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Automotive Market in UK dynamic, structure by analyzing the market segments and projecting the Automotive Market in UK size. Clear representation of competitive analysis of key players by Vehicle type, price, financial position, product portfolio, growth strategies, and regional presence in the Automotive Market in UK make the report investor’s guide.

Automotive Market in UK Scope: Inquiry Before Buying

| Automotive Market in UK | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | 1.75 Mn. units |

| Forecast Period 2023 to 2029 CAGR: | 6.1% | Market Size in 2029: | 2.64 Mn. units |

| Segments Covered: | by Vehicle Type | Passenger Cars LCVs HCVs Electric Vehicles |

|

| by Sales Type | Business Private Fleet |

||

Automotive Market in UK Key Players

1. Aston Martin

2. Bentley

3. Caterham Cars

4. Daimler

5. Jaguar

6. Lagonda

7. Land Rover

8. Lister Cars

9. Lotus

10. McLaren

11. MG

12. Mini

13. Morgan

14. Rolls-Royce

Frequently Asked Questions:

1] What segments are covered in the Global Automotive Market in UK report?

Ans. The segments covered in the Automotive Market in UK report are based on Vehicle Type and Sales Type

2] Which region is expected to hold the highest share in the Global Automotive Market in UK?

Ans. The Central England region is expected to hold the highest share in the Automotive Market in UK.

3] What is the market size of the Global Automotive Market in UK by 2029?

Ans. The market size of the Automotive Market in UK by 2029 is expected to reach 2.64 million units

4] What is the forecast period for the Global Automotive Market in UK?

Ans. The forecast period for the Automotive Market in UK is 2023-2029.

5] What was the market size of the Global Automotive Market in UK in 2022?

Ans. The market size of the Automotive Market in UK in 2022 was valued at US$ 1.75 Mn. units