Automotive Fintech Market Size by Vehicle Type, Propulsion Type, Application, End-Use, Channel, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

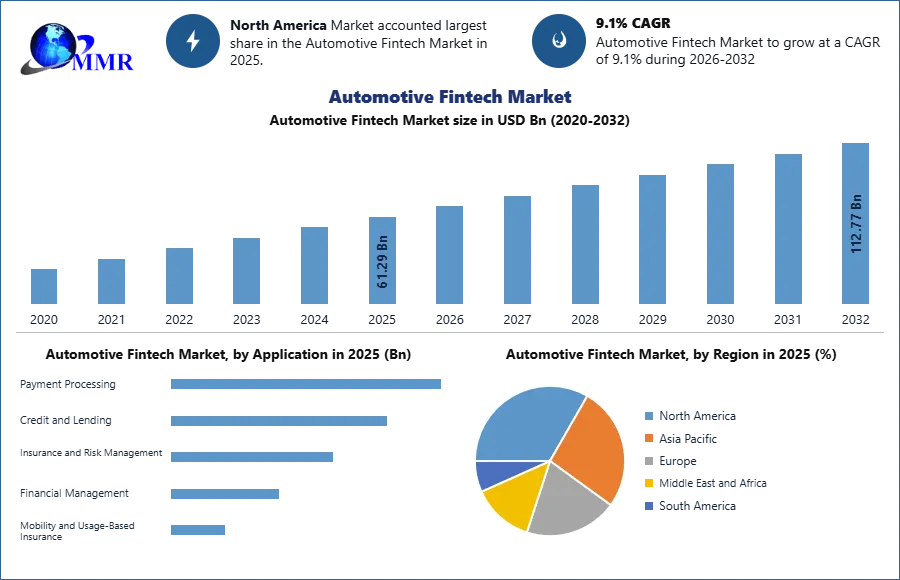

The Automotive Fintech Market size was valued at USD 61.29 Billion in 2025 and the total Automotive Fintech Market revenue is expected to grow at a CAGR of 9.1 % from 2026 to 2032, reaching nearly USD 112.77 Billion.

Fintech has become an integral part of every industry, offering faster, cheaper, and easier services for organizations and their customers. The automotive industry has also benefited from the growth of Automotive Fintech Market. As more devices become digital and interconnected, exchanging data becomes easier. Vehicles now send and receive data across the internet, providing consumers with a more convenient and seamless experience. Payments have been a clear way that Fintech has impacted the auto industry.

In-car payment technology has risen, with OEMs partnering with payment solutions to offer services such as paying for gas and parking. Established players such as SAP, Volkswagen, Ford, GM, Daimler, Visa, Jaguar, and BMW have all taken significant steps in this area. Payment solution providers like Cardtek are also exploring new models for in-car payment, including an IoT platform that interfaces with merchant devices, an integrated mobile wallet, and a personal POS terminal for transactions.

The new transportation-sharing economy, which includes on-demand transportation, car-sharing, and ride-sharing services, has opened up opportunities for growth in digital leasing and lending in Automotive Fintech Market. This shift in consumer behaviour has been driven by the popularity of sharing services, which have challenged traditional car ownership. This has led to a surge in on-demand transportation, with companies like Uber, Lyft, Didi, and Grab changing the transportation landscape across the globe in Automotive Fintech Market.

As a result, there is an increasing demand for specialized financial services for on-demand platforms, such as vehicle leasing for on-demand platforms (Drover, HyreCar), and commercial insurance for drivers in the on-demand economy (Inshur, Zego). With digital transactions becoming more efficient, next-generation car rental players are providing consumers with flexible options, including the ability to rent out their own cars. This sector is evolving, with new players using subscription-based pricing or shared ownership models to gain Automotive Fintech Market share.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Automotive Fintech Market Dynamics:

Online Car Buying Surges, Unlocking Lucrative Opportunities in Fintech Market

The digitalization of the automotive industry presents numerous revenue opportunities in the near future in Automotive Fintech Market. The digitalization of the automotive industry has also created opportunities in digital financing in Automotive Fintech Market, with automakers and fintech lenders partnering to offer the best rates and incentives. Nevertheless, many OEMs are reluctant to relinquish a lucrative part of their business to third-party fintech companies. Despite the challenges, the automotive industry is ripe for development, and the recent acceleration in online car shopping is evidence of this.

Connected Cars are fuelling the Growth of the Automotive Fintech Industry

As cars continue to advance technologically, they are increasingly becoming a new source of payment and data. The increasing collaborations and initiatives from stakeholders in the industry. Connected cars have the potential to revolutionize how people transact, create new business models, and provide new opportunities for stakeholders in the industry, which increases the Automotive Fintech Market demand during the forecast period. In terms of payment, connected cars offer opportunities in both the business-to-consumer (B2C) and the business-to-business (B2B) fields.

In B2C, a mobile wallet integrated into a connected car enables drivers to make seamless transactions, including paying for coffee, parking spaces, or their car loan monthly payments. Manufacturers and dealerships can also use a car wallet to enable electrical charging deposits and trade-in credits for use in an ecosystem, improving customer retention and providing better ownership and mobility experiences, which drive the Automotive Fintech Market growth. In B2B, a car wallet can be used by businesses to pay for their employees' travel and expenses, reducing the need to report expenses separately and mitigating fraud. Connected cars have the potential to become a new channel for marketplaces and e-commerce activities, connecting drivers to retailers, gas stations, and service providers through their dashboards.

Connected cars also offer data monetization opportunities for auto manufacturers, allowing them to gain deeper insights into their customers and offer personalized services. Growing demand for the Automotive Fintech Market in Insurance companies could also use this data to offer pay-as-you-go insurance coverage, personalized pricing options, and improve the overall claims process.

Digital Finance Drives Growth and Transformation in the Automotive Fintech Industry

Digital finance has been a major driver of growth in the Automotive Fintech Industry. The use of digital technologies to facilitate financial transactions in the automotive industry has transformed the way people buy and finance cars. One of the key ways that digital finance is driving growth in the Automotive Fintech Industry is by making it easier and more convenient for consumers to finance their car purchases. Digital platforms and apps are allowing consumers to complete the entire car-buying process online, from browsing inventory to securing financing.

The automobile financing transformation is being driven by new business models, including Fintech, which promise to make the industry more efficient and dynamic. As auto financing becomes increasingly digitized, with advanced technologies such as artificial intelligence, Fintech are poised to become a crucial component of the auto lending ecosystem. By accelerating loan processing times and reducing costs for both auto lenders and consumers, companies that partner with Fintech will likely dominate the market. While some traditional lenders have been slow to embrace Fintech, those that fail to adapt may struggle to remain competitive.

Digital finance has enabled the development of new financing models, such as peer-to-peer lending and crowd-sourced financing. These models allow individuals to invest in and finance automotive purchases, bypassing traditional banks and financial institutions, which drive the Automotive Fintech Market. Furthermore, the use of digital finance is also facilitating the development of new financial products and services, such as usage-based insurance and car-sharing programs. These products and services are appealing to a new generation of consumers who are looking for more flexibility and customization in their automotive purchases.

Automotive Fintech Market Segment Analysis:

By End-Use Type: the Automotive Fintech Market is segmented into In-vehicle payments, Online Leasing, Digital Loans and Purchas, Online Insurance. Digital Loans and Purchase segment is expected to dominate the Automotive Fintech Market during the forecast period. Digital loan and purchase in the automotive Fintech market refer to the use of technology and digital platforms to offer financing solutions for the purchase of vehicles. In recent years, there has been a surge in the number of Fintech companies offering digital lending solutions for automotive purchases.

Digital lending in the automotive Fintech market typically involves an online application process that is quick and convenient. The applicant provides their personal information, financial information, and information about the vehicle they wish to purchase. The Fintech Company then uses artificial intelligence and machine learning algorithms to assess the applicant's creditworthiness and risk profile. Based on the assessment, the Fintech Company may offer a loan approval and provide the funds necessary to purchase the vehicle.

One of the major benefits of digital lending in the automotive Fintech market is the speed and convenience it offers. Applicants can apply for a loan and receive a loan decision within minutes, which makes it easier for them to purchase the vehicle they want without having to go through a lengthy and tedious application process. Additionally, digital lending often results in lower interest rates and fees compared to traditional lending methods, as Fintech companies are able to offer more competitive rates due to their lower overhead costs. Report covered the detailed analyses of each market segment with micro details.

Automotive Fintech Market Regional Insights

North America dominated Automotive Fintech Market in 2025 and is expected to continue its dominance over the forecast period. The growing segment of the broader financial technology and automotive industries, driven by increasing consumer demand for digital financing, embedded insurance, and online leasing solutions. North America has historically been a leading region globally, with the United States and Canada dominating adoption due to advanced digital infrastructure, high vehicle financing penetration, and strong collaborations between OEMs, banks, and fintech firms that streamline loan approvals and personalized finance offers at point of sale. The market is expanding as more dealerships integrate digital solutions, AI‑driven risk assessment tools improve underwriting, and in‑vehicle payment systems and subscription‑based services gain traction, fostering seamless end‑to‑end customer experiences.

In Asia Pacific, the rapid growth and evolution of the Asian market has made it a leader in adopting and revolutionizing new technologies, and Automotive Fintech market. The growth of Automotive Fintech products in the Asia Pacific region can be attributed to various factors, including positive government initiatives, multiple investors interested in Fintech, a large unbanked population, and a general openness to new financial technologies. The governments in the region differ in their support of Automotive Fintech industry adoption, resulting in variations in the number of Fintech start-ups and investment attracted in different regions.

Recent Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 12 February 2026 | Grab Holdings Inc | Grab announced the acquisition of Stash Financial, Inc., a U.S.-based digital investing platform, to accelerate its financial services roadmap and integrate AI-driven guidance. | The move expands Grab’s fintech ecosystem into wealth management, complementing its existing automotive lending and insurance products in Southeast Asia. |

| 09 February 2026 | Cars24 | The online marketplace rolled out a major brand identity refresh and shifted to a relationship-driven model in preparation for its upcoming IPO. | This evolution signals a transition toward a full ownership ecosystem, integrating captive financing (CredMate) and value-added services as primary revenue drivers. |

| 28 January 2026 | AutoFi Inc | AutoFi launched a new customer-centric Showroom solution, a digital tool designed to streamline in-store financing and deal estimation for dealerships. | The platform reduces sales cycle times by unifying the digital and physical showroom experience, driving higher conversion rates for automotive retailers. |

| 01 December 2025 | Creditas Soluções Financeiras | Creditas finalized the acquisition of Bank Andbank Brasil and secured US$108 million in a Series G funding round to scale its collateralized lending operations. | The acquisition provides a banking license that lowers funding costs and strengthens Creditas' ability to offer competitive auto equity and finance products in Latin America. |

| 14 July 2025 | Creditas Soluções Financeiras | The company launched a new R$800 million FIDC (Structured Fund) specifically dedicated to boosting its Auto Equity and Auto Finance business units. | Heavy oversubscription by institutional investors provides stable capital for the fintech to expand its asset-backed lending portfolio amid rising market demand. |

| 10 April 2025 | AutoFi Inc | AutoFi announced a strategic integration with DriveCentric, bringing AI-powered CRM capabilities directly into its commerce and lending platform. | This partnership eliminates data silos between sales and finance teams, enabling real-time customer profile imports and faster loan approvals at the point of sale. |

Automotive Fintech Market Scope: Inquire before buying

| Automotive Fintech Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 61.29 USD Bn |

| Forecast Period 2026-2032 CAGR: | 9.1% | Market Size in 2032: | 112.77 USD Bn |

| Segments Covered: | by Vehicle Type | Passenger Car Commercial Vehicle |

|

| by Propulsion Type | ICE Electric |

||

| by Channel | On Demand Subscription |

||

| by Application | Payment Processing Credit and Lending Insurance and Risk Management Financial Management Mobility and Usage-Based Insurance |

||

| by End Use | In vehicle payments Online Leasing Digital Loans and Purchase Online Insurance Others |

||

Automotive Fintech Market Regional Insights:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key players/Competitors profiles covered in the Automotive Fintech Market report in a strategic perspective

- AutoFi Inc

- The Savings Group, Inc

- Blinker, Inc

- By Miles Ltd

- Creditas Soluções Financeiras

- Cuvva Limited

- Grab Holdings Inc

- RouteOne LLC

- Euroclear SA NV

- Kuwy Technology Services Pvt Ltd

- ACKO

- Marshmallow

- Clearcover

- Cambridge Mobile Telematics

- Roojai

- com

- Cars24

- RoadLoans

- Pagaya Technologies

- Kavak

- Bumper

- Carmoola

- OTO

- CreditWise Capital

- Bike Bazaar

- CreditMate

- VOOM

- Revfin

- Revv

- CarDekho Group