Autogas Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

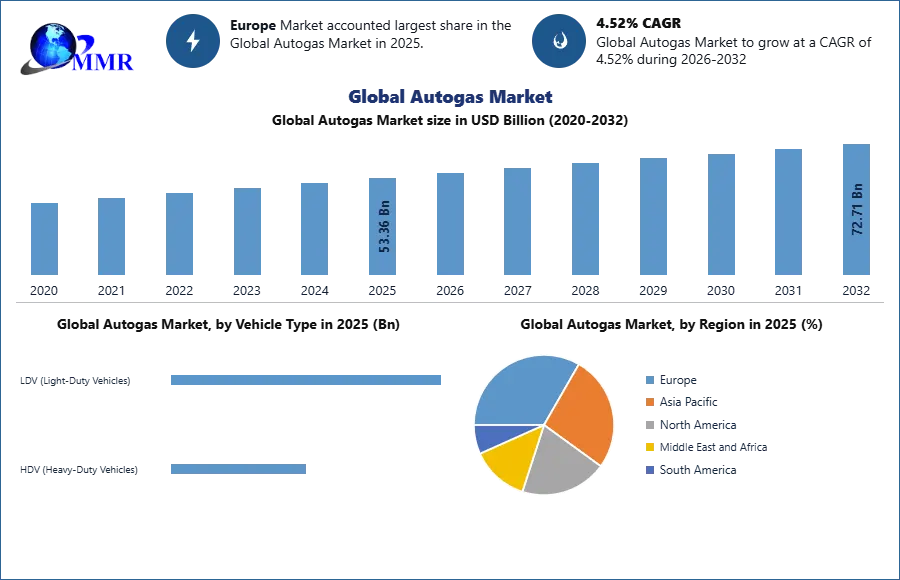

Autogas Market size was valued at USD 53.36 Bn. in 2025 and the Autogas is expected to grow by 4.52 % from 2026 to 2032, reaching nearly USD 72.71 Bn by 2032.

Autogas Market Overview:

The Autogas market, also known as the liquefied petroleum gas (LPG) market for automotive applications, revolves around the utilization of LPG as a fuel for vehicles. LPG, derived from natural gas processing and crude oil refining, primarily consists of propane and butane. Autogas has garnered considerable attention as a viable alternative fuel option due to its favorable attributes such as reduced carbon emissions and cost-efficiency when compared to conventional gasoline and diesel fuels. In recent years, the Autogas market has witnessed steady growth, propelled by factors such as environmental concerns, governmental regulations, and economic benefits. LPG is recognized as a cleaner-burning fuel with lower carbon dioxide (CO2) emissions than gasoline and diesel, making it an appealing choice for mitigating greenhouse gas emissions. Additionally, Autogas presents a more economical alternative by offering lower fuel prices and reduced vehicle maintenance expenses owing to cleaner combustion. This comprehensive overview aims to delve into a detailed analysis of the Autogas market, encompassing its present state, primary drivers, emerging market trends, challenges, and future prospects.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Market Trends in the Autogas Industry:

Vehicle Conversions

One significant trend in the Autogas market is the conversion of existing gasoline and diesel vehicles to run on LPG. Conversion kits are widely available, and many vehicle owners are opting to retrofit their cars to take advantage of the cost and environmental benefits offered by the Autogas market.

OEM Adoption

Original equipment manufacturers (OEMs) have started offering Autogas-powered vehicles as factory-fitted options. This trend has gained traction in Europe, where several major automakers, including Volkswagen, Ford, and Dacia, offer LPG variants of their popular models. OEM adoption plays a crucial role in increasing the availability and acceptance of Autogas vehicles and is expected to boost the Autogas market during the forecast period.

Infrastructure Development

The expansion of refueling infrastructure is crucial for the widespread adoption of Autogas. Governments and private entities are investing in the establishment of LPG refueling stations, both standalone and as part of existing fuel stations, to enhance the accessibility and convenience of Autogas for vehicle owners.

Autogas Market Dynamics:

Drivers of the Autogas Market:

Environmental Concerns

Growing awareness about climate change and air pollution is a major driver for the Autogas market. The lower carbon emissions of Autogas compared to gasoline and diesel make it an attractive option for reducing greenhouse gas emissions and improving air quality. Example: The European Union's emission reduction targets and regulations incentivize the adoption of cleaner fuels like Autogas, leading to increased demand for LPG-powered vehicles.

Government Incentives and Regulations

Governments worldwide are implementing policies and incentives to promote the use of Autogas. These measures include tax exemptions, subsidies, and favorable regulations for vehicle conversions and refueling infrastructure. For Example, In Turkey, the government provides financial incentives for vehicle owners to convert their vehicles to Autogas, leading to a significant increase in LPG-powered vehicles on the road.

Cost-effectiveness

Autogas offers cost advantages over gasoline and diesel. It often provides lower fuel prices and can result in lower vehicle maintenance costs due to cleaner combustion and reduced wear on engine components. For Example, In India, Autogas is significantly cheaper than gasoline and diesel, making it an attractive option for price-conscious consumers and fleet operators.

Restraints of the Autogas Market:

Limited Refueling Infrastructure

The availability of Autogas refueling stations is limited in some regions, which can discourage potential consumers from adopting LPG-powered vehicles due to concerns about refueling convenience. Example: In certain rural areas or developing countries, the lack of Autogas refueling infrastructure can be a significant restraint, limiting the widespread adoption of LPG vehicles.

Perception and Awareness

Misconceptions and lack of awareness about Autogas can act as a restraint. Some consumers may be hesitant to switch to LPG-powered vehicles due to concerns about safety, performance, or limited knowledge about the benefits of Autogas. Example: In North America, where the Autogas market is relatively smaller compared to other regions, the lack of awareness and misconceptions about LPG as a vehicle fuel can hinder its growth.

Challenges of the Autogas Market:

Electric Vehicle Competition

The increasing popularity of electric vehicles poses a challenge to the Autogas market. The rapid development of electric vehicle technology and expanding charging infrastructure can divert consumer attention and investment away from Autogas. Example: In countries like Norway, where electric vehicle adoption is high and supported by government incentives, the demand for Autogas vehicles may face challenges due to strong competition from EVs.

Infrastructure Development

The establishment of a robust refueling infrastructure for Autogas is a significant challenge. Expanding the number of refueling stations requires substantial investments and coordination between government bodies, fuel providers, and private entities. Example: Developing countries with limited resources may face difficulties in rapidly expanding Autogas refueling infrastructure, leading to slower adoption rates.

Opportunities in the Autogas Market:

Emerging Economies

Rapid urbanization and increasing vehicle ownership in emerging economies present significant growth opportunities for the Autogas market. These regions often struggle with air pollution, and Autogas can provide a cleaner and more affordable fuel option. Example: In countries like India and China, where there is a high demand for cost-effective and environmentally friendly transportation, the Autogas market has significant growth potential.

Technological Advancements

Ongoing advancements in Autogas fuel systems and engine technologies can enhance the performance and efficiency of LPG-powered vehicles. Integration of Autogas with hybrid technologies and the use of bio-LPG, a renewable form of LPG, provide opportunities for further development. Example: European automotive manufacturers are investing in research and development to improve the efficiency of Autogas engines and develop hybrid LPG-electric vehicles, expanding the range of options available to consumers.

Autogas Market Segment Analysis:

The Autogas market can be segmented based on various factors, including vehicle type, conversion type, end-use, and geography. A comprehensive segment analysis helps to understand the market dynamics, target specific customer groups, and identify growth opportunities within each segment. Here is an in-depth analysis of the key segments in the Autogas market:

The Autogas market is divided on the basis of the Vehicle Type which is further subdivided into the IDV and HDV. IDV segment includes cars, SUVs, vans, and other vehicles used for personal transportation. Autogas, also known as liquefied petroleum gas (LPG), is an alternative fuel option for IDVs. It offers several benefits such as lower emissions, cost-effectiveness, and wide availability in many regions. Autogas can be used as a standalone fuel or as a dual-fuel system in IDVs, where vehicles can run on both gasoline and LPG. The IDV segment is significant in terms of the Autogas market, as many individuals choose LPG as a fuel option for their personal vehicles. This segment is expected to hold the largest share of the Autogas market within the forecast period.

Also, the HDV segment encompasses vehicles such as trucks, buses, and commercial vehicles used for the transportation of goods or passengers. Autogas has also gained popularity as an alternative fuel for heavy-duty vehicles. It offers advantages such as reduced fuel costs, lower emissions, and comparable performance to diesel fueling the Autogas market growth. Autogas-powered HDVs often use dedicated LPG systems or bi-fuel systems that allow vehicles to switch between Autogas and diesel. This segment is important in the Autogas market due to the significant fuel consumption and emissions associated with heavy-duty transportation.

The Autogas market is divided on the basis of the Conversion Type which is further subdivided into the Original Equipment Manufacturer, Retrofitted/Converted. The original Equipment Manufacturer (OEM) Fitted segment includes vehicles that come factory-fitted with Autogas systems. OEM-fitted Autogas vehicles provide consumers with the convenience of purchasing vehicles that are already optimized to run on LPG. Another is the Retrofitted/Converted segment includes vehicles that are converted from gasoline or diesel to Autogas through retrofitting or conversion kits. Vehicle owners can modify their existing vehicles to run on Autogas, enabling them to get the benefits of LPG without purchasing a new vehicle. For Example, Many individuals and fleet operators choose to convert their vehicles to Autogas in countries like Italy and Poland to save costs and reduce emissions. With the advantage such as retrofitting many individuals are attracted to the benefits of Autogas which is expected to boost the Autogas market during the forecast period.

The Autogas market is divided on the basis of the End-Use which is further subdivided into Private Use, Commercial Use. The private Use segment includes Autogas vehicles used by individual owners for personal transportation purposes. Private vehicle owners may be attracted to Autogas due to its cost-effectiveness, environmental benefits, and long-term fuel savings which are expected to show exponential growth during the forecast period. Also, the commercial Use segment comprises Autogas vehicles used by businesses and organizations for various commercial purposes, such as transportation services, delivery, and logistics. Fleet operators often choose Autogas for their commercial vehicles due to lower operating costs and reduced environmental impact. For Example, Delivery companies and taxi services in urban areas often opt for Autogas vehicles to lower their fuel expenses and reduce their carbon footprint.

Autogas Market Regional Insights:

The Autogas market exhibits varying dynamics and growth patterns across different regions of the world. Factors such as government policies, infrastructure development, consumer preferences, and economic conditions influence the adoption and growth of Autogas as a vehicle fuel.

Europe has been a prominent market for Autogas, with several countries leading the adoption of LPG-powered vehicles. Turkey stands out as one of the largest Autogas markets globally, driven by a combination of government incentives, a well-established refueling infrastructure, and a strong LPG supply chain. Poland and Italy are also significant markets, with a substantial number of Autogas conversions and OEM-fitted LPG vehicles. The Netherlands has a high penetration of Autogas, primarily due to favorable tax policies and strong government support.

The Asia Pacific region presents significant growth opportunities for the Autogas market. India has a considerable Autogas market, driven by a large number of retrofitted vehicles and OEM-fitted LPG variants. The availability of LPG as a byproduct of natural gas extraction and refining contributes to the growth of the Autogas market in countries like China, South Korea, and Thailand. Government policies, such as subsidies and tax exemptions, aim to promote Autogas as a cleaner and more affordable alternative to conventional fuels in this region.

North America:

The Autogas market in North America is relatively smaller compared to other regions, but it is gradually gaining attention. The United States and Canada have seen an increase in the adoption of Autogas, particularly in the commercial sector. School buses, delivery fleets, and government vehicles are among the primary users of Autogas in North America. The availability of LPG as a byproduct of natural gas production and ongoing efforts to expand refueling infrastructure contribute to the market's growth potential.

Autogas Market Competitive Landscape:

The Autogas market is characterized by intense competition among various players, including fuel providers, vehicle manufacturers, conversion companies, and infrastructure developers. These players aim to capture market share by offering Autogas products, services, and solutions that cater to the growing demand for cleaner and more cost-effective transportation options.

Fuel Providers

Fuel providers play a crucial role in the Autogas market by supplying LPG to refueling stations and end-users. These companies may have their own distribution networks or collaborate with gas suppliers and energy companies to ensure a reliable and consistent supply of Autogas. Key players in this segment include national and international oil and gas companies that have ventured into the LPG business. For Example, Shell, BP, Total, Gazprom, ExxonMobil

Vehicle Manufacturers

Automotive companies that offer Autogas variants or convert their vehicles to run on LPG contribute to the competitive landscape of the market. These manufacturers design and produce vehicles that are optimized for Autogas use, thereby providing consumers with a convenient option to purchase LPG-powered vehicles directly from the showroom. For Example, Volkswagen, Ford, Opel, Hyundai, Dacia.

Autogas Market Recent Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 07 March 2026 | Indian Oil Marketing Companies | The government directed oil refiners to prioritize propane and butane streams for LPG production over petrochemical feedstocks to ensure supply security. | This strategic shift protects domestic autogas and cooking fuel availability amid supply chain disruptions caused by regional geopolitical tensions. |

| 27 January 2026 | Indian Auto LPG Coalition | The coalition formally petitioned the Petroleum and Natural Gas Regulatory Board (PNGRB) to include Auto LPG in the national comparative assessment study of vehicular fuels. | Advocacy efforts aim to secure technology-neutral policy recognition for autogas as an immediately deployable low-emission transport fuel. |

| 25 September 2025 | Westport Fuel Systems | The company participated in AUTOGASDAY 2025 in Rio de Janeiro to present the latest LPG fuel system innovations and decarbonization pathways. | Engagement at the summit underscored the growing global adoption of autogas by OEMs and its viability as an affordable alternative fuel solution. |

| 15 January 2025 | Linde plc | The entity completed the integration of its industrial gas portfolio following corporate restructuring to optimize LPG supply chain logistics. | Streamlined operations improve distribution efficiency, lowering costs for commercial autogas fleet operators and industrial end-users. |

Autogas Market Scope: Inquire Before Buying

| Global Autogas Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 53.36 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.52% | Market Size in 2032: | 72.71 USD Billion |

| Segments Covered: | by Vehicle Type | LDV (Light-Duty Vehicles) HDV (Heavy-Duty Vehicles) |

|

| by Conversion Type | Original Equipment Manufacturer Retrofitted/Converted |

||

| by End User | Private Use Commercial Use |

||

| by Distribution Channel | LPG Filling Stations OEM / Dealerships Aftermarket Conversion Providers |

||

Autogas Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Autogas Market, Key Players are

1. BP plc

2. Chevron Corporation

3. Exxon Mobil Corporation

4. Shell plc

5. TotalEnergies SE

6. Gazprom

7. Hindustan Petroleum Corporation Limited

8. Bharat Petroleum Corporation Limite

9. Indian Oil Corporation Limited

10. SHV Energy N.V.

11. Aygaz A.S.

12. Flogas Britain Limited

13. Westfalen AG

14. China Petroleum & Chemical Corporation (Sinopec)

15. PetroChina Company Limited

16. Repsol S.A.

17. Eni S.p.A

18. UGI Corporation

19. DCC plc

20. Kleenheat Gas

21. Primagasnergie GmbH

22. Vitol Grou

23. Origin Energy Limited

24. Auto Gas Energy India

25. Likitgaz Dagitim ve Endustri A.S.

26. PTT Oil and Retail Business Public Company Limited

27. Phillips 66 Company

28. Calor Gas Limited

29. LPG Distribution Network (various regional operators)

30. Petron Corporation

Others