Asia Pacific Online Grocery Shopping Market Product, Payment Method, End User and Region – Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2029

Overview

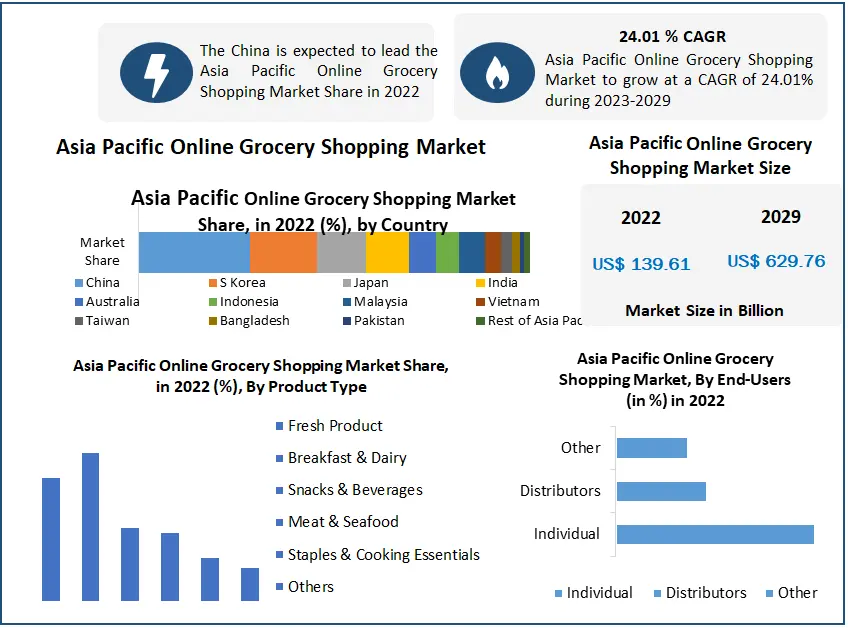

The Asia Pacific Online Grocery Shopping Market size was valued at USD 139.61 billion in 2022 and the total Asia Pacific Online Grocery Shopping Market revenue is expected to grow at a CAGR of 24.01 % from 2023 to 2029, reaching nearly USD 629.76 billion.

The Asia Pacific Online Grocery Shopping Market is a sector with immense potential, driven by factors such as changing consumer lifestyles, urbanization, and the digital transformation of retail. In APAC, fresh food shopping and meal preparation are integral aspects of consumers' lives, accounting for nearly 50% of their expenditures in categories such as food, groceries, and personal care. Despite the importance of fresh food, concerns about its quality, freshness, and fulfillment have historically hindered the adoption of online channels. There is a shift in consumer behavior towards digital solutions, driven by factors like urbanization, increased female workforce participation, and growing time constraints. As consumers embrace online shopping, the average shopping basket size increases, indicating a growing enthusiasm for e-commerce.

Asia Pacific Online Grocery Shopping Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

To tap into this opportunity effectively, businesses must cater to the diverse needs of different consumer archetypes, such as the Perfectionist, Influencer, Family-Centric User, and Loving Supporter. Despite promising growth, the sector faces challenges. These include intense competition in a complex market, uncertainties about profitability, and operational hurdles such as poor logistics infrastructure, regulatory challenges, and uneven digital payment adoption. Accumulation of excess inventory due to increased sales during the pandemic and high delivery costs in a geographically diverse country like Indonesia also pose challenges. Tech investors and e-commerce platforms have entered the online grocery space, leveraging their existing capabilities, such as logistics fleets, to expand into this market. However, the profitability of these ventures remains uncertain, with some experiencing high operating expenses. The Asia Pacific Online Grocery Shopping Market holds vast potential, but it also presents challenges that require innovative solutions. Success in this space will depend on the ability of market players to address operational efficiency, logistics, and payment issues while adapting to the evolving needs of consumers in this dynamic and rapidly growing market.

Asia Pacific Online Grocery Shopping Market Scope and Research Methodology:

The Asia Pacific Online Grocery Shopping Market represents a dynamic and rapidly evolving sector within the broader e-commerce landscape. This market encompasses the digital purchase of a wide range of grocery products, including fresh food, and household essentials in the Asia Pacific region. Our research methodology for understanding and analyzing this market involves a comprehensive approach. Gather data from different sources like industry reports, market research firms, government publications, and online databases. Primary research is conducted through surveys, interviews, online retailers, and consumers to gain insights into market trends, preferences, and challenges. We study market size, growth rates, and revenue projections, considering factors like consumer behavior, technology adoption, and economic conditions. Regional variations and market dynamics are also closely examined to provide a holistic view of the Asia Pacific Online Grocery Shopping Market. Our scope includes analyzing market drivers, such as urbanization, changing consumer lifestyles, and the impact of the COVID-19 pandemic, as well as challenges like logistics infrastructure and payment adoption. We aim to provide a thorough understanding of this market's current state, future potential, and the strategies employed by industry players to thrive in this rapidly evolving landscape.

Market Dynamics:

Pandemic Sparks Online Grocery Shopping Revolution in Asia Pacific:

The Asia Pacific Online Grocery Shopping Market region witnessed a phenomenal surge in 2022, with more than 154 million people embracing online shopping for the first time in a single year. This surge was primarily concentrated in Asia Pacific, accounting for a staggering 69 percent of all new online shoppers worldwide, with China alone contributing 53 percent to this surge. The region reported the slowest growth in online sales, but sales still skyrocketed to a remarkable US$230 billion. China played a pivotal role in this growth, contributing a third of the new turnover and dominating the region's online retail market with an 82 % share. The growth of e-commerce in Asia Pacific was driven by a 16 % increase in online sales, with the grocery category experiencing the most significant boost, surging by 46%. India emerged as the market, while Australia led the pack as the fastest-growing market.

This explosive growth in the online grocery shopping market was largely influenced by the COVID-19 pandemic, which forced people to turn to online shopping due to restrictions on physical store visits across various markets in the region. Pure-play grocery retailers attracted investments and launched online platforms, while established retailers entered the grocery sector, and brick-and-mortar players expanded their online presence to adapt to the changing landscape. For instance, in India, Flipkart expanded into grocery retail by launching a 90-minute delivery service during the pandemic. Tata Group acquired BigBasket, the nation's largest online grocery retailer, and Reliance Retail introduced JioMart grocery to serve demand in over 200 Indian cities. The retailers in the region have strategically leveraged offline stores to enhance their reach. Alibaba, for instance, took control of Sun Art Retail, China's largest supermarket chain, which has a significant presence in non-urban areas, allowing Alibaba to tap into the underserved non-urban consumer market. This synergy between online and offline retailing is poised to fuel further growth in the online grocery shopping market across Asia Pacific in the coming years.

Online Retail Sales, By Country, (in 2022)

Changing Lifestyles Drive APAC's Shift to Online Grocery Shopping:

The Asia Pacific Online Grocery Shopping Market (APAC) region presents a promising opportunity in the realm of fresh food. In APAC, fresh food shopping and meal preparation hold significant importance in consumers' lives, accounting for a substantial portion of consumer expenditures, nearly 50% in the categories of food, groceries, and personal care. Despite this, concerns regarding freshness, quality, and fulfillment have historically deterred shoppers from embracing online channels for fresh food purchases. There's a shift on the horizon, with new omnichannel propositions poised to bridge the gap between online and offline experiences. These innovative solutions have the potential to win over busy APAC consumers, who are increasingly turning to digital options for their daily transactions. Urbanization and a rising number of women in the workforce have led to busier lifestyles, longer work hours, and heightened traffic congestion, making online shopping an appealing alternative.

The average shopping basket expands significantly between a consumer's first and third online orders, indicating growing enthusiasm for online shopping. To tap into this opportunity effectively, it's crucial to cater to the diverse needs of different consumer archetypes, such as the Perfectionist, Influencer, Family-Centric User, and Loving Supporter, each requiring tailored experiences. Rather than traditional e-commerce platforms, grocery retailers must create services that seamlessly blend the digital and physical worlds. This evolution in the shopping offering should adapt to changes in consumers' lives and provide access to products, services, and information that traditional vendors cannot offer. The key to success lies in bridging the online and offline realms, offering a flexible yet standardized approach that caters to the unique needs of various shopper profiles. As the APAC market for fresh foods continues to grow, this holistic approach has the potential to redefine the online grocery shopping landscape, making it more accessible and convenient for discerning consumers in the region.

| Food | Instore | Digital Channel | |

| Fresh food | |||

| Vegetables | 92% | 3% | |

| Fruit | 89% | 3% | |

| Bakery | 87% | 5% | |

| Meat (Beef, Poultry, Pork, Chicken) | 87% | 3% | |

| Fish | 86% | 3% | |

| Diary (E.g. Milk, Cheese, Yogurt) | 83% | 6% | |

| Ready to Eat products | 83% | 5% | |

| Segments Covered: | |||

| Rice, noodles, potatoes, etc | 85% | 5% | |

| Beverages | 75% | 8% | |

| Canned or bottled foods 6 | 69% | 10% | |

| Boxed foods (like dry cereal or pasta) | 68% | 12% | |

| Healthcare (OTC drugs, plasters, braces, etc.) | 65% | 10% | |

| Supermarket non-food items (paper goods, laundry items, etc.) | 65% | 13% | |

| Personal care (soap, shampoo, toothpaste, cosmetics, etc.) | 58% | 14% | |

| Baby food | 40% | 13% | |

| Baby diapers | 33% | 19% |

Indonesia's Complex Grocery Landscape is a Challenge for Online Retail:

Indonesia boasts a diverse grocery shopping landscape, ranging from traditional markets to supermarkets, presenting a complex competitive environment. With a grocery industry valued at USD 169.4 billion in 2022, players, including tech investors and startups, are flocking to the sector, intensifying the competition. Despite promising sales figures, it remains uncertain whether tech-backed online groceries are profitable or continually bleeding money. High operating expenses, akin to China's Dingdong's case, can erode profits. Dingdong, despite revenue growth, posted significant losses due to narrow gross margins and expansion costs. Online grocers in Indonesia grapple with numerous operational challenges, including poor logistics infrastructure, regulatory hurdles, and uneven digital payment adoption. Smaller cities rely on cash on delivery (COD) due to a sizable population lacking bank accounts, which increases operational complexity.

Increased sales driven by the pandemic led to grocers accumulating large inventories. This surplus inventory can weigh down profit margins and hinder growth prospects, impacting the bottom line. Grocery delivery in a sprawling and geographically diverse country like Indonesia is cost-intensive. Ensuring timely and efficient deliveries while managing delivery costs poses a significant challenge. The online grocery market in Indonesia is expanding rapidly. These challenges raise important questions about its long-term profitability. Companies entering this space must address operational efficiency, logistics, and payment solutions to navigate these hurdles successfully. The future of the Asia Pacific Online Grocery Shopping Market in Indonesia hinges on the ability of market players to find sustainable business models amidst these complexities and uncertainties.

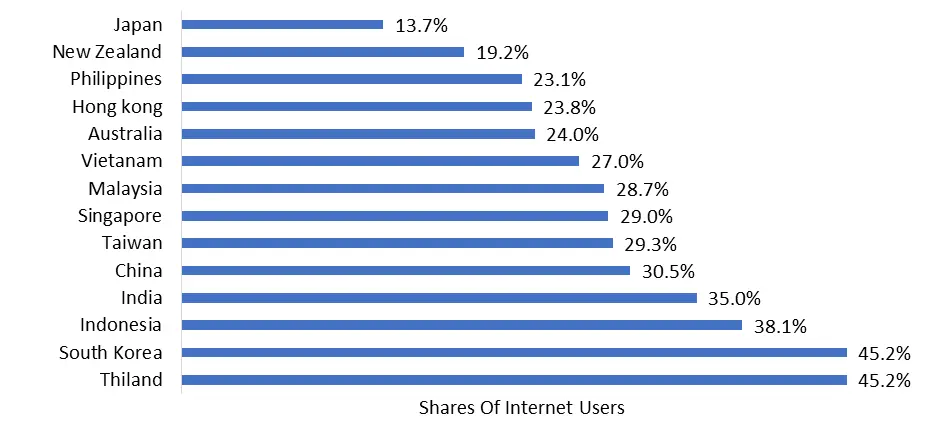

Share Of Internet Users Who Made Weekly Online Grocery Purchases In The Asia-pacific Region In 2022, By Country (%)

Asia Pacific Online Grocery Shopping Market Segment Analysis:

Based on End Users, In the Asia Pacific Online Grocery Shopping Market, the dominant segment is individuals, representing the largest consumer base and driving the majority of online grocery sales in the region. This segment primarily consists of regular consumers who purchase groceries for personal use. Their demand for convenience and time-saving options has played a pivotal role in the growth of online grocery shopping platforms. Individuals within this segment highly value the convenience offered by online shopping, particularly in their busy schedules.

They have access to a wide range of products and often benefit from tailored promotions and discounts. For instance, working professionals frequently turn to online platforms to order their weekly groceries, as it saves them time and helps them avoid crowded in-store experiences. Another significant segment includes businesses that procure groceries for resale or distribution to various outlets, including retailers, restaurants, and other establishments. Online platforms provide these businesses with efficiency and ease when sourcing products in bulk. For example, restaurant owners often utilize online platforms to purchase ingredients for their menu offerings, streamlining their supply chain operations. There is a miscellaneous segment that encompasses various unique end-user categories not covered by the primary segments. This diverse category may include organizations or specialized groups with distinct purchasing needs. For instance, non-profit organizations may utilize online platforms to source groceries for community events and charitable activities.

Asia Pacific Online Grocery Shopping Market Regional Insights:

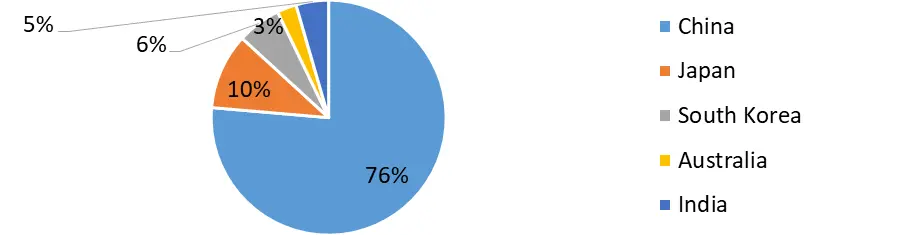

China has emerged as the undeniable leader, poised to dominate the sector by 2023. This dynamic landscape also sees Japan, South Korea, and Australia securing spots within the top 10 online grocery markets, according to insights from the Institute of Grocery Distribution (IGD). These top 10 markets are projected to experience substantial growth, with a value increase of US$227 billion expected by 2023. China, Japan, and South Korea are at the forefront of this online grocery shopping revolution in the Asia Pacific Online Grocery Shopping Market, demonstrating remarkable market share penetration. IGD's Asia Programme emphasizes the significance of these three countries, stating that physical retailers in China, having recognized the importance of online and digital channels, are collaborating with eCommerce and delivery partners to offer more targeted ranges, and promotions, and expand their omnichannel presence. This collaborative approach positions China as the global leader on this list.

China's online grocery market is expected to reach US$196.3 billion in the forecast years in 2023. This results in a CAGR of 31%, translating to an increase of US$145.4 billion from its current US$50.9 billion. This growth elevated China's share of the global online grocery shopping market to 11.2%, a significant leap from its current 3.8%. IGD draws attention to the fact that the Chinese online grocery shopping market's growth alone will match the combined market size of all ten countries in 2018. Japan secures the second-highest ranking on the list, anticipated to reach an estimated US$46.5 billion by 2023, resulting in a respectable 9.9% share of the online grocery channel. South Korea, ranked fifth overall, is poised to reach a value of US$21.3 billion by 2023 and is expected to lead the global list in terms of online grocery channel share at an impressive 14.2%. Japan and South Korea, with well-established online grocery operations, will experience steady growth in their market shares, albeit at a relatively slower pace compared to other markets in the region. Australia, ranked seventh, presents more modest growth predictions, expected to reach just US$4.2 billion by 2023. In contrast, France, ranked sixth, is estimated to reach US$17.2 billion.

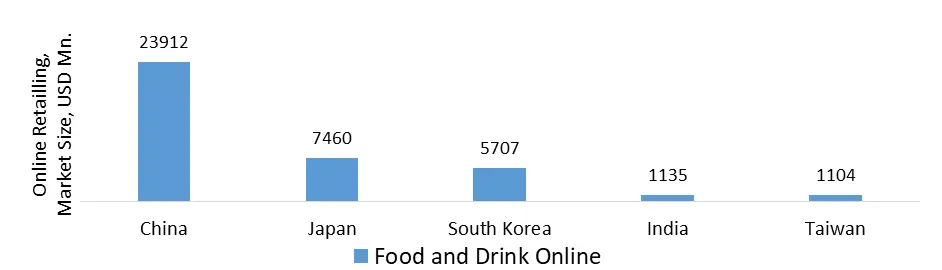

Online Grocery Retailing, In 2022 In USD Million

Competitive Landscape

Key Players of the Asia Pacific Online Grocery Shopping Market profiled in the report Alibaba, Amazon.com Inc., Carrefour S.A., Coles Group Ltd., Costco Wholesale Corp., Koninklijke Ahold Delhaize, Lulu Hypermarket, Rakuten, Reliance Retail Ltd. (Reliance Fresh), SPAR International, Supermarket Grocery Supplies Pvt. Ltd. (BigBasket), Target Corporation, Tesco, Walmart Inc. This provides huge opportunities to serve many End-users and customers and expand the Asia Pacific Online Grocery Shopping Market.

Alibaba Group Holding is expanding its Hema Fresh cashless supermarkets, aiming to open 100 stores in 2022, surpassing the initial target of 60. With over 65 stores already in operation, Hema Fresh lures consumers with its extensive range of fresh food, particularly seafood prepared on-site. This retail concept, blending online and physical stores, has significantly contributed to Alibaba's revenue growth, with sales from new retail quadrupling in the April-June quarter compared to the previous year. Alibaba's commitment to long-term growth is evident in its substantial investment cash flow, reaching 71.6 billion yuan ($10.5 billion) in the same quarter, approaching the previous fiscal year's annual total.

Asia Pacific Online Grocery Shopping Market Scope: Inquire Before Buying

| Asia Pacific Online Grocery Shopping Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 139.61 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 24.01% | Market Size in 2029: | US $ 629.76 Bn. |

| Segments Covered: | by Product | Fresh Produce Breakfast & Dairy Snacks & Beverages Meat & Seafood Staples & Cooking Essentials Others |

|

| by Payment Method | Online Offline (Cash on Delivery) |

||

| by End User | Individual Distributors Others |

||

Asia Pacific Online Grocery Shopping Market Key Players:

1. Alibaba

2. Amazon.com Inc.

3. Carrefore S.A.

4. Coles Group Ltd.

5. Costco Wholesale Corp.

6. Koninklijike Ahold Delhaize

7. Lulu Hypermarket

8. Rakuten

9. Reliance Retail Ltd. (Reliance Fresh)

10. SPAR International

11. Supermarket Grocery Supplies Pvt. Ltd. (BigBasket)

12. Target Corporation

13. Tesco

14. Walmart Inc.

FAQs:

1. What are the growth drivers for the Asia Pacific Online Grocery Shopping Market?

Ans. The pandemic sparked the Online Grocery Shopping Revolution in Asia Pacific and is expected to be the major driver for the Asia Pacific Online Grocery Shopping Market.

2. What are the major restraints for the Asia Pacific Online Grocery Shopping Market growth?

Ans. Indonesia's Complex Grocery Landscape is a Challenge for Online Retail and is expected to be the major restraint in the Asia Pacific Online Grocery Shopping Market.

3. Which country is expected to lead the Asia Pacific Online Grocery Shopping Market during the forecast period?

Ans. China is expected to lead the Asia Pacific Online Grocery Shopping Market during the forecast period.

4. What is the projected market size and growth rate of the Asia Pacific Online Grocery Shopping Market?

Ans. The Asia Pacific Online Grocery Shopping Market size was valued at USD 139.61 billion in 2022 and the total Asia Pacific Online Grocery Shopping Market revenue is expected to grow at a CAGR of 24.01 % from 2023 to 2029, reaching nearly USD 629.76 billion.

5. What segments are covered in the Asia Pacific Online Grocery Shopping Market report?

Ans. The segments covered in the Asia Pacific Online Grocery Shopping Market report are by Product Type, Payment Method, End-Users, and Region.