Agritech Platforms Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

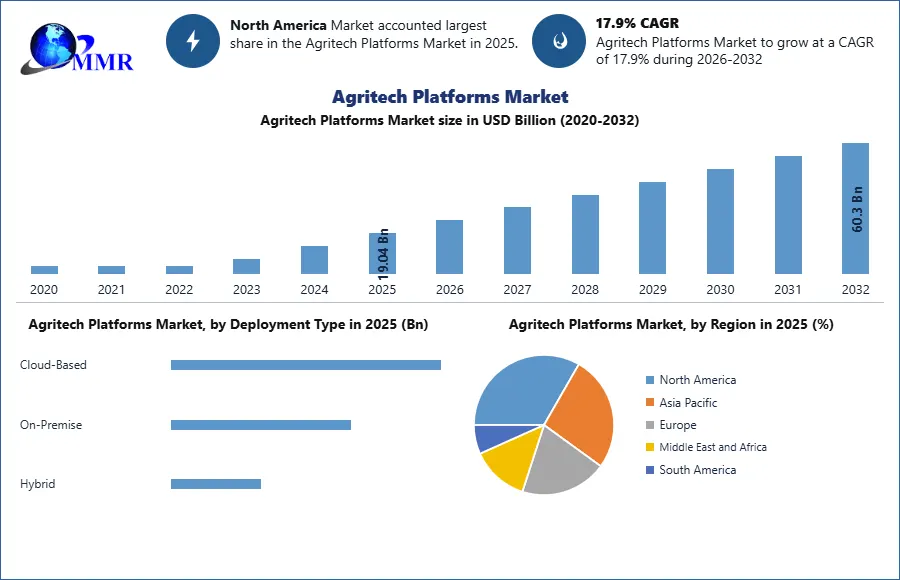

Agritech Platforms Market size was valued at USD 19.04 billion in 2025 and is expected to reach USD 60.3 billion by 2032, at a CAGR of 17.9%.

Agritech Platforms Market Overview

Agricultural technology, also known as agtech or agritech, involves using technology to enhance farming, horticulture, and aquaculture. Its goal is to boost crop yields, efficiency, and profitability. This technology includes products, services, or applications that improve agricultural processes. Agritech platforms specifically focus on using technology to enhance farming practices, helping farmers become more efficient, productive, and make informed decisions. They also aim to reduce labor costs, improve working conditions, and minimize environmental impact.

The Agritech Platforms Market is experiencing significant growth, driven by innovations in agriculture that are transforming traditional farming practices. Technologies like precision farming, IoT, AI, and robotics are playing a crucial role in improving efficiency, optimizing resource use, and boosting crop yields. The adoption of environmentally friendly technologies, like Bee Vectoring Technologies (BVT) and indoor vertical farming, is also contributing to market growth by offering sustainable solutions that reduce the need for chemical pesticides and conserve resources.

Regionally, North America leads the Agritech Platforms Market, driven by technological advancements and the high adoption of precision farming techniques. The United States is the major contributor to this growth, with a large number of agritech startups and significant government support for smart agricultural technologies.The competitive landscape of the agritech platforms market is marked by the presence of both well-established companies such as John Deere and emerging players like Fyllo and Zuari FarmHub. These companies are leveraging advanced technologies and strategic partnerships to offer a wide range of services that cater to the evolving needs of farmers. By integrating technologies such as IoT and AI into their offerings, these companies are not only improving productivity and sustainability but also positioning themselves as leaders in the rapidly growing agritech platforms market.

The agritech sector received a total of USD 1.15 billion in funding by 2022. Downstream agritech received USD 707 million in venture capital funding, the highest amount of any agritech sector. The downstream Agtech are mainly B2B or B2C platforms that connect farmers with businesses and consumers.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Agritech Platforms Market Dynamics

Agriculture Innovation and Its Impact on Agritech Platforms Market Growth

Agricultural innovations are significantly driving the growth of the agritech platforms market by enhancing farming practices and improving efficiency. Innovations such as precision farming, which uses GPS and data analytics to optimize field management, have significantly enhanced crop yields and resource efficiency. These technologies allow farmers to monitor soil health, weather conditions, and crop growth in real-time, leading to more informed decision-making and targeted interventions. For example, the use of drones for aerial imagery and data collection has revolutionized how farmers assess their crops, helping them identify problems like pest infestations or nutrient deficiencies early on.

Precision Farming Techniques can increase crop yields by 10-15% and reduce fuel and labour costs by 15-20%.

Bee Vectoring Technologies (BVT) is a noticeable innovation, which uses commercial bees to provide pest control solutions through pollination, eliminating the need for chemical pesticides. This technology not only protects honeybees, but also supports sustainable agricultural practices by reducing the environmental impact of traditional pest control methods. The BVT system is versatile and can be used for a variety of crops, such as blueberries and tomatoes, making it an attractive solution for farms of all sizes. The adoption of these environmentally friendly technologies is contributing to the expansion of the agritech platforms market as farmers are increasingly looking for solutions that improve crop yields and support sustainable agriculture.

In the United States, honeybees contribute about USD 20 billion to agricultural production annually.

Indoor vertical farming is another transformative innovation that is reshaping the agritech landscape. This technology allows the production of high-density plants in controlled environments, maximizing yield per unit of space and significantly reducing water consumption by up to 70%. Techniques such as hydroponics and aeroponics used in indoor farming offer substantial benefits, including the ability to control light, temperature and nutrient levels for optimal crop growth. The integration of automation and robotics also reduces labor costs and improves productivity. As this technology gains traction, it is driving Agritech Platforms market growth by providing scalable solutions to meet the growing demand for food in urban areas and regions with limited arable land.

1. AeroFarms, the leader in vertical farming, uses up to 95% less water than field-farmed food, without pesticides while achieving up to 390 times higher yield per square foot.

Agritech Platforms Market Opportunity

Role of AI in Shaping the Future of Agritech Platforms Market:

Artificial intelligence (AI) in agriculture is revolutionizing the agriculture sector by providing powerful tools that improve decision-making, optimize the use of resources and increase productivity. AI-based technologies such as machine learning, computer vision, and predictive analytics are integrated into agritech platforms, enabling farmers to collect and analyze large amounts of data from their fields in real time. These platforms can monitor crop health, predict weather conditions, and even identify pests and diseases at an early stage. For instance, AI algorithms can analyze satellite images and drone footage to detect subtle changes in plant health that could indicate the presence of pests or nutrient deficiencies, allowing farmers to take targeted action in advance so that the problem does not spread. This precision not only improves crop yield, but also reduces the need for excessive use of water, fertilizers, and pesticides, making agriculture more sustainable and profitable.

The growing adoption of AI in agriculture offers significant opportunities for agritech platforms market to grow and innovate. As AI technology becomes more accessible, platforms that offer AI-based solutions can capture a larger share of the market. These platforms can be differentiated by offering features such as automated irrigation systems, AI machines that can plant or harvest crops with high precision, and tools that provide personalized recommendations based on specific operating conditions. In addition, AI can help address labor shortages by automating repetitive tasks, allowing farmers to focus on more strategic aspects of farm management. With the global population expected to reach nearly 10 billion by 2050, the demand for efficient and scalable agricultural solutions will continue to grow, driving investment in AI-powered agritech platforms. This creates an exciting market opportunity for companies that can use artificial intelligence to provide innovative, user-friendly, and efficient solutions for farmers around the world.

In 2023, artificial intelligence (AI) was mostly used in field farming, livestock, and indoor farming. Field farming was the main area of AI use in agriculture, accounting for more than 60% of the market. The overall market for AI in agriculture was around USD 1.6 billion in 2023 and is expected to reach around USD 7.2 billion in 2030.

Agritech Platforms Market Segment Analysis:

Based On Application Areas, Agritech Platforms Market is segmented into Precision Farming, Livestock Monitoring, Smart Greenhouses, Supply Chain Management, and Others. The Precision Farming Segment held the largest market share of xx% in 2025 and it is expected to maintain its dominance till 2032. This is due to the increasing adoption of growing technologies that can improve agriculture productivity and resource efficiency. Precision farming uses data-driven insights, GPS, and sensors to optimize field management, allowing farmers to apply water, fertilizers, and pesticides more precisely. According to MMR, the precision farming market is valued at USD 8.5 billion in 2022 and is expected to grow at a CAGR of 12.5%. This is mainly due to government initiatives and subsidies that promotes the adoption of smart agricultural technologies particularly in North America and Europe where large-scale farming operations benefit from precision agriculture. For instance, the United States Department of Agriculture (USDA) actively supports the use of precision agricultural tools to improve the efficiency and sustainability of agriculture.

The growth in precision farming is driven by partnerships between agritech companies, which give farmers access to new technologies and expert knowledge. These collaborations lead to the development of advanced tools like IoT sensors, drones, and data analytics platforms that help farmers use resources more efficiently, boost crop yields, and reduce environmental impact. For instance, in August 2023, Zuari FarmHub in India partnered with CropX Technologies to introduce advanced real-time monitoring technology. This partnership offers farmers valuable data insights to enhance productivity and sustainability.

The dominance of the precision farming segment is boosted by its environmental benefits, which include a 4% increase in crop production, 7% better fertilizer efficiency, 9% less use of herbicides and pesticides, a 6% reduction in fossil fuel use, and a 4% decrease in water consumption.

Agritech Platforms Market Regional Insight

North America is the fastest-growing region in the global agritech platforms market, holding the largest share of XX% in 2025. This is due to technological advancements and the widespread adoption of precision farming techniques in this region. Innovations in IoT, AI, robotics, and data analytics help farmers to optimize resources and monitor crops effectively. The United States is the major contributor holding nearly xx% of the North American Agritech Platforms Market, largely due to the increasing number of Agritech Startups. There are 6,737 AgriTech startups in the United States which include The Climate, Trimble, Indigo, FBN, Corteva Agriscience. These companies offer a range of services, from online grain markets to microbiome therapy, further strengthening the region's market presence. Additionally, The growth of the agritech sector in North America is also driven by government initiatives and significant funding to promote precision agriculture and sustainable agricultural practices. For instance, the United States Department of Agriculture (USDA) supports the adoption of smart agricultural technologies through various subsidies and programs.

North American and European farmers are leading in the adoption of Agritech, with about 61% either using or planning to use an agtech product in next two years. Their main challenges are high costs and unclear returns on investment. European farmers also worry about high costs, but they face additional issues with setup and usability. In South America, 50% of farmers are adopting agtech, but they are concerned about the trustworthiness of online purchases. Adoption is lowest in Asia, where only about 9% of farmers are using or planning to use agtech, and this varies by country.

Agritech Platforms Market Competitive Landscape

The Agritech Platforms Market is highly competitive and a mix of well-established players and emerging players. Some of the major key players are John Deere, Trimble, Taranis, and Ag Leader. John Deere, a leader in agricultural machinery, integrates advanced technologies such as precision farming tools and IoT solutions into its equipment. The company focuses on products and services with high added value, leveraging its significant investments in research and development (R&D) to drive innovation. Trimble Inc. is known for its precision farming solutions, including GPS and data analysis tools, that help farmers optimize their operations. Trimble's user-friendly agricultural technologies help connect entire operations to make easier data-driven decisions through modern industrial solutions.

1. In October 2023, Zuari FarmHub, a top agritech company in India, partnered with CropX Technologies, a global leader in digital agronomic solutions. This collaboration is set to transform farming in India by introducing real-time monitoring technology, providing farmers with valuable data-driven insights to improve productivity and sustainability.

2. In August 2023, Fyllo, India's first precision agritech startup, announced a strategic partnership with Terraview, a global climate SaaS company. This collaboration aims to enhance the productivity of more than 100 wine producers across the US, Spain, and Australia.

3. In 2023, AGCO acquired digital assets from FarmFacts GmbH, a top farm management software company. This move is part of AGCO's strategy to enhance precision agriculture and follows its significant $2 billion deal with Trimble earlier in the year.

Agritech Platforms Market Scope: Inquire before buying

| Agritech Platforms Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 19.04 USD Billion |

| Forecast Period 2026-2032 CAGR: | 17.9% | Market Size in 2032: | 60.3 USD Billion |

| Segments Covered: | by Platform Category | Precision Farming Platforms Livestock Monitoring Platforms Supply Chain Management Platforms Marketplace Platforms Weather Forecasting Platforms Others |

|

| by Component | Software Big Data & Analytics IoT Platform Software Mobility Sensor Integration Software Others Service Integration & Implementation Consulting Services Support & Maintenance Others |

||

| by Deployment Type | Cloud-Based On-Premise Hybrid |

||

| by Farm Size | Small Medium Large |

||

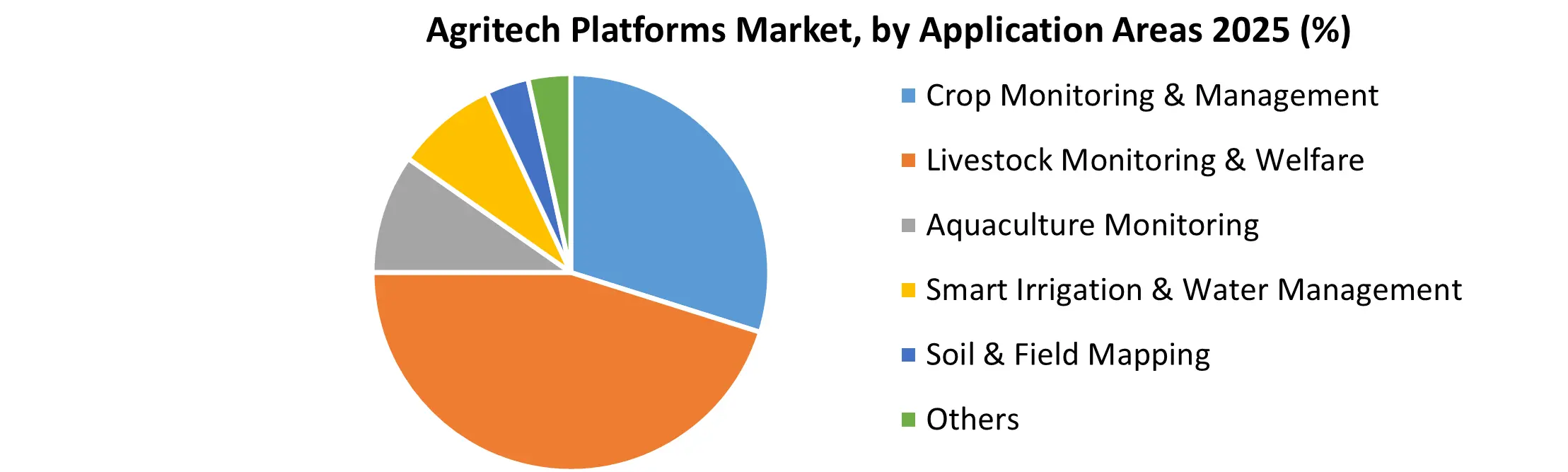

| by Application Areas | Crop Monitoring & Management Livestock Monitoring & Welfare Aquaculture Monitoring Smart Irrigation & Water Management Soil & Field Mapping Others |

||

Agritech Platforms Market, by Region:

North America (United States, Canada, Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (India, China, Japan, South Korea, Australia, ASEAN, and Rest of APAC)

Middle East and Africa (South Africa, GACC, Egypt, Nigeria, and Rest of ME & A)

South America (Brazil, Argentina, Columbia, and Rest of South America)

Agritech Platforms Market, Key Players

1. Trimble Inc.

2. Agworld Pty Ltd

3. Ceres Imaging

0. AGCO Corporation

5. Raven Industries

6. Cropin

7. IBM

8. AgroStar

9. ITC

10.DeHaat

11.Ninjacart

12.Jai Kisan

13.Indigo Ag

14.Syngenta

15.The Climate Corporation

16.Micron AgriTech

17.Satyukt

18.Ekobot

19.Farmer's Business Network (FBN)

20.Farmers Edge Inc.

21.Taranis

22.Semios

23.Gamaya Corp.

24.Hortau

25.Phytech

Frequently Asked Questions:

1. Which region has the largest share in the Agritech Platforms Market?

Ans: The North American region held the largest share in 2025.

2. What is the growth rate of the Agritech Platforms Market?

Ans: The Agritech Platforms Market is expected to grow at a CAGR of 17.9 % during the forecast period 2026-2032.

3. What are the different segments of the Agritech Platforms Market?

Ans. The Agritech Platforms Market is divided by Components and Application.

4. Who are the key players in the Agritech Platforms Market?

Ans: The major key players in the Agritech Platforms Market are John Deere, Trimble, Taranis, and Ag Leader.

5. What is the scope of the Agritech Platforms Market report?

Ans: The Agritech Platforms Market report helps with the PESTLE, PORTER, Recommendations for Investors & Leaders, and market estimation of the forecast period.