Aerospace Composites Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

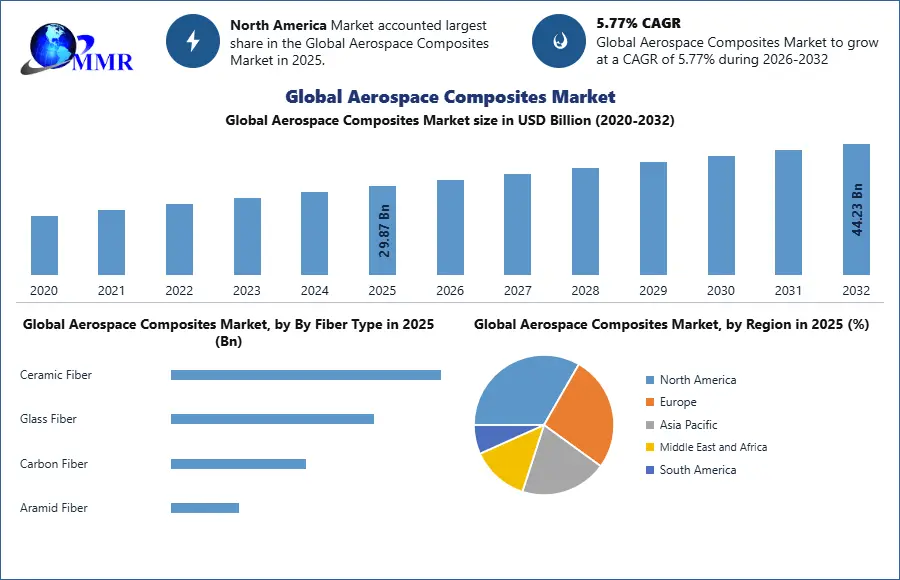

The Aerospace Composite Market size was valued at USD 29.87 billion in 2025 and the total Aerospace Composite revenue is expected to grow at a CAGR of 5.77% from 2026 to 2032, reaching nearly USD 44.23 Million.

Aerospace composites are advanced materials used in construction of aircraft and spacecraft. They are composed of two or more constituent materials with significantly different physical or chemical properties, which remain separate and distinct within finished structure. Common types of aerospace composites include carbon fiber reinforced polymers (CFRP), glass fiber reinforced polymers (GFRP), and aramid fiber reinforced polymers (AFRP). These materials offer superior strength-to-weight ratios, stiffness, and resistance to fatigue and corrosion compared to traditional materials like aluminum and steel. Aerospace composite market is experiencing robust growth, driven by increasing demand for lightweight, durable, and fuel efficient materials in aerospace industry.

Composites are essential in reducing weight of aircraft, which directly translates to improved fuel efficiency and lower emissions, aligning with industrys sustainability goals. Aerospace Composite Market includes a wide range of applications, including commercial aircraft, military aircraft, helicopters, and spacecraft. Primary drivers of aerospace composite market are need to reduce weight of aircraft. Composites are significantly lighter than traditional materials, which leads to improved fuel efficiency and reduced operational costs. Aviation industry is under constant pressure to reduce its carbon footprint, and use of composites plays a crucial role in achieving this goal.

Growth in air travel, particularly in emerging economies, has led to a surge in demand for commercial aircraft. Manufacturers in Aerospace Composite Market are increasingly using composite materials to enhance performance and efficiency of new aircraft models. For instance, Boeing 787 Dreamliner and Airbus A350 XWB are both designed with a high percentage of composite materials. Military sector also drives demand for aerospace composites due to their superior performance characteristics. Composites are used in various applications, including fighter jets, helicopters, and unmanned aerial vehicles (UAVs). Need for advanced materials that offer high strength, durability, and stealth capabilities is a significant growth factor in this segment.

Solvay and Spirit AeroSystems have strengthened their research and technology relationship by becoming strategic partners at Spirits Aerospace Innovation Centre (AIC) in Prestwick, Scotland. This collaboration focuses on developing advanced composite aerostructures to meet performance, cost, and production rate requirements of future Aerospace Composite Market. Partnership aims to innovate in composite fabrication, automation, and assembly technologies to shorten development cycles and de risk projects. ARRIS, a leader in advanced manufacturing of fiber reinforced composites, secured $34 million in funding to expand its operations and accelerate adoption in Aerospace Composite Market. This investment supports development of high performance composite materials at scale, which are critical for next-generation aerospace applications. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Aerospace Composite Market Dynamics:

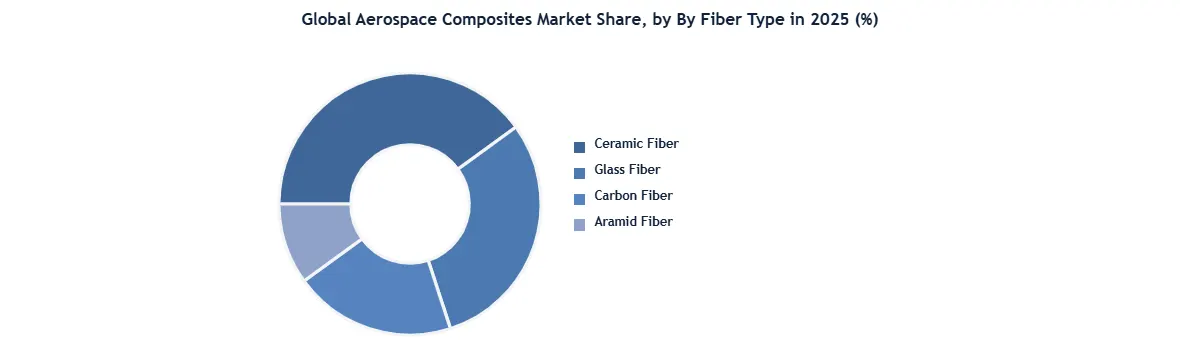

Based on Fiber Type :The Carbon Fiber segment dominated the Aerospace Composite Market owing to its superior strength-to-weight ratio, high durability, corrosion resistance, and fuel efficiency advantages in commercial and military aircraft applications. Carbon fiber composites are extensively used in aircraft fuselage structures, wings, tail sections, cabin interiors, and engine components because they significantly reduce aircraft weight while improving structural performance and fuel economy. The increasing production of next-generation aircraft, rising demand for lightweight aerospace materials, and growing focus on carbon emission reduction are further accelerating segment growth.

Meanwhile, the Glass Fiber segment maintains stable demand due to its cost-effectiveness and usage in secondary aircraft structures and interior applications. Ceramic Fiber composites are increasingly utilized in high-temperature aerospace environments such as engine insulation and thermal protection systems because of their superior heat resistance capabilities. In addition, the Aramid Fiber segment is witnessing steady growth in aerospace defense and ballistic protection applications due to its high impact resistance, lightweight properties, and durability in critical aircraft safety components.

.

Aerospace Composite Market Regional Insights:

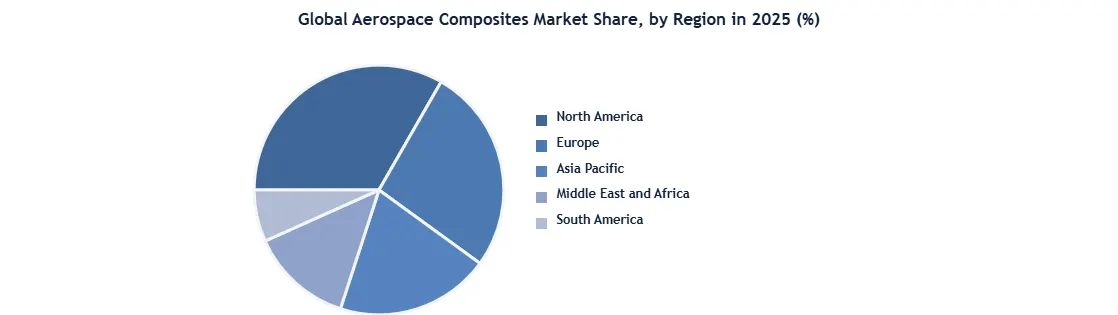

Aerospace Composite Market was predominantly led by North America, capturing a significant 35% market share in 2025. This dominance is attributed to region's robust aerospace and defense industry, presence of major aircraft manufacturers like Boeing, and extensive research and development activities focused on advanced composite materials. North Americas leadership in aerospace composites is further bolstered by strong investments in military aircraft, commercial aviation, and space exploration programs. region’s well-established supply chain and technological advancements also contribute to its leading position in Aerospace Composite Market.

Europe follows with a 27% market share in 2025, driven by presence of key players such as Airbus and numerous aerospace component manufacturers. The region's commitment to sustainable aviation and lightweight materials has spurred adoption of composites to enhance fuel efficiency and reduce emissions. Europe’s stringent environmental regulations and ambitious aerospace projects, including Clean Sky initiative, are significant drivers of growth in the Aerospace Composite Market. collaboration between government bodies, research institutions, and private companies in Europe further supports innovation and market growth.

Asia Pacific holding a 24% market share, is observed to be fastest growing region in aerospace composite market. The rapid growth is propelled by increasing demand for commercial aircraft due to rising air passenger traffic and economic growth in countries like China and India. The regions aerospace industry is witnessing substantial investments in manufacturing facilities and technological upgrades to meet growing demand. Companies in Asia Pacific are also focusing on enhancing their production capacities and entering strategic partnerships to leverage advanced composite technologies. The establishment of aerospace hubs, particularly in China, and regions integration into global supply chain are critical factors contributing to its swift Aerospace Composite Market growth.

Aerospace Composite Industry Ecosystem

Aerospace Composite Industry Competitive Landscape

The collaborations and investments in composite manufacturing are set to drive substantial Aerospace Composite Market growth. Solvay and Spirit AeroSystems' partnership will advance composite aerostructures, enhancing manufacturing technologies and efficiency for future aircraft. ARRIS’s $34 million funding will accelerate global scaling of its advanced composites platform, expanding its market reach in aerospace and consumer Resin Types. Moreover, Dufour Aerospace's choice of Aerolite for producing lightweight, high-quality Aero2 components highlights increasing demand for efficient, durable parts in aviation. These developments collectively foster innovation and growth in Aerospace Composite Market.

On June 21, 2023, Solvay and Spirit AeroSystems strengthened their partnership by making Solvay a strategic partner at Spirit’s Aerospace Innovation Centre (AIC) in Prestwick, Scotland. This collaboration focuses on advancing composite aerostructures, aiming to enhance sustainable aircraft technologies and processes. By developing advanced manufacturing concepts, both companies seek to improve composite fabrication, automation, and assembly technologies, thereby reducing development cycles and aligning on future innovation opportunities to meet demands of future aircraft.

On April 30, 2024, ARRIS a leader in advanced manufacturing of fiber reinforced composites, announced it secured $34 million in new funding. This investment round, supported by both new and existing investors like ST Engineering, Zebra Technologies and Bosch Ventures, aims to accelerate ARRIS's growth and expand its presence in aerospace and consumer markets. The funding will support ARRIS's global scaling of its next gen manufacturing platform, which promises to enhance adoption of high-performance composites across key sectors.

On July 14, 2023, Dufour Aerospace selected Aerolite AG as main supplier for composite structural parts for Aero2 aircraft. Aerolite will manufacture nacelles and tail components at its Horw, Switzerland facility. This partnership focuses on leveraging Aerolites expertise in producing lightweight, durable parts essential for aviation efficiency. Simon Bendrey from Dufour Aerospace praised Aerolite's established aerospace manufacturing experience and certifications, which will contribute significantly to high quality production and assembly of Aero2 components.

Aerospace Composite Industry Recent Development:

Aerospace Composites Market Scope: Inquire before buying

| Global Aerospace Composites Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 29.87 USD Billion |

| Forecast Period 2026-2032 CAGR: | 5.77% | Market Size in 2032: | 44.23 USD Billion |

| Segments Covered: | By Fiber Type | Ceramic Fiber Glass Fiber Carbon Fiber Aramid Fiber |

|

| By Resin Type | Epoxy Phenolic Polyester Polyimides Polyether Ether Ketone (PEEK) Polysulfone (PSU) Polyetherimide (PEI) Others |

||

| By Manufacturing Process | Lay-Up (Hand and Automated) Resin Transfer Molding (RTM) Filament Winding Injection/Compression Molding Automated Fiber Placement and Tape Laying Additive Manufacturing of Composites Others |

||

| By Aircraft Type | Commercial Aircraft Narrow-Body Wide-Body Regional Jets Freighters Business Jets Military Aircraft Fighter Jets Transport and Tanker Helicopters Spacecraft and Launch Vehicles Others |

||

| By Application | Exterior Fuselage Engine Wings Rotor blades Tail boom Interior Seats Cabin Sandwich panels Environmental control system (ECS) ducting |

||

| By End-User | OEM Aftermarket/MRO |

||

Aerospace Composites Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Aerospace Composite Market, Key Players:

- Avior Integrated Products

- Aernnova Aerospace

- Bally Ribbon Mills

- Barrday

- Collins Aerospace

- DuPont

- ÉireComposites

- Evonik Industries

- General Dynamics

- Hexcel Corporation

- Honeywell International

- Huntsman Corporation

- Isovolta

- JPS Composite Materials

- Kineco

- Lee Aerospace

- Materion Corporation

- Owens Corning

- Park Aerospace Corp.

- Renegade Materials Corporation

- Sekisui Aerospace

- SGL Carbon

- Solvay

- Spirit AeroSystems

- Teijin Limited

- Toray Advanced Composites

Others