ADC Technology Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2030

Overview

The Global ADC Technology Market size was valued at USD 8.32 Bn in 2023 and is expected to reach USD 15.82 Bn by 2030, at a CAGR of 9.6 %.

Overview of the ADC Technology Market

Antibody-drug conjugates (ADCs) are designed to achieve selective and precise delivery of cytotoxic drugs, primarily to tumor cells expressing specific antigens, utilizing the specificity of monoclonal antibodies (mAbs). In contrast to conventional cytotoxic drugs, ADCs enhance the effectiveness of their payload while reducing its toxicity. This targeted approach to delivering cytotoxic drugs to cancer cells increases the proportion of drug molecules reaching the tumor site, consequently reducing the minimum effective dose required and raising the maximum tolerated dose. The graphical representation and structural exclusive information showed the dominating region of the ADC Technology Market. The detailed and constructive formation of key drivers, opportunities, and unique segmentation outputs structural and optimistic data. Validated using primary as well as secondary research methodology and scope of the ADC Technology Market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

ADC Technology Market Dynamics

The Increasing Prevalence of Oncological Disorders and the Demographic Shift toward an Aging Population are Major Drivers of the ADC Technology Market

The rising incidence and prevalence of oncological disorders on a global scale serve as a primary catalyst for the ADC technology market. With cancer continuing to be a significant global health challenge, there is an urgent demand for more effective and precisely targeted therapeutic interventions. The demographic transition toward an aging population is contributing to a heightened demand for innovative cancer treatments. Older individuals are more susceptible to cancer, emphasizing the critical role of advanced therapies like ADCs in addressing the healthcare needs of this demographic segment. Researchers are demonstrating an increasing interest in exploring innovative therapeutic approaches, with ADCs emerging as a particularly promising avenue.

This heightened interest stems from the potential of ADCs to provide targeted and potent treatment options across a wide spectrum of tumor Targets. ADCs represent an emerging category of highly potent pharmaceutical drugs that combine elements of immunotherapy and chemotherapy. Their distinctive mode of action and the ability to precisely target specific antigens make them an appealing choice for cancer treatment. ADCs have demonstrated their effectiveness by precisely targeting specific antigens, including ERBB2, CD33, CD19, CD22, MSLN (mesothelin), and numerous others. This versatility in targeting antigens enhances the applicability of ADCs across various cancer Targets in the ADC Technology Market.

Off-target toxicities, Aggregation, Drug Resistance, and Stability Testing are the major challenges in the ADC technology Market

A significant impediment in ADC development revolves around off-target toxicities stemming from the premature release of cytotoxic small molecules into the bloodstream. The risk of off-target toxicities is compounded when the cytotoxic small molecules possess a higher inherent toxicity in the ADC Technology Market. Resolving this issue is imperative for augmenting the safety profile of ADCs. ADCs are susceptible to aggregation, a phenomenon that can result in structural alterations impeding their capacity to bind to the intended target antigen. Aggregation poses a substantial obstacle, particularly in the initial phases of ADC development. Mitigating this challenge necessitates meticulous formulation and engineering efforts to pre-empt such complications. The degradation induced by aggregation introduces complexities in meeting stability testing requirements, which are indispensable for securing regulatory approval and the registration of ADC-based pharmaceuticals. Balancing long-term stability with the preservation of therapeutic efficacy remains a critical concern in this regard. ADCs are not immune to drug resistance, which curtails their duration of effectiveness.

The persistence of drug resistance has been a vexing issue impeding the clinical success of ADC therapies. However, the modular nature of ADCs offers avenues for the modification of components, facilitating the creation of novel compounds capable of circumventing resistance mechanisms. Elevated expression of drug efflux pumps stands as one of the prevalent mechanisms contributing to ADC resistance, underscoring the need for innovative strategies to combat this challenge and extend the clinical utility of the ADC Technology Market.

ADC Technology Market Segment Analysis

By Target: When it comes to selecting targets for ADCs, several sub-categories are notable in the ADC Technology Market. Antibody-Protein Toxin Conjugates involves the linkage of monoclonal antibodies to protein toxins, facilitating precise cell destruction. Antibody-chelated radionuclide Conjugates utilize antibodies as vehicles to deliver radionuclides to tumor cells, enabling localized radiation therapy. Antibody-Small-Molecule Drug Conjugates employ antibodies to selectively transport small-molecule drugs to cancer cells. Antibody-enzyme conjugates entail the coupling of antibodies with enzymes to initiate specific biochemical reactions within target cells. In the ADC technology market, Adcertis and Kadcyla stand out as prominent examples, each possessing unique characteristics and End-Users.

Additionally, there are other ADC products contributing to the continuously evolving landscape. ADCs hinge on the specificity of antibodies to target cancer cells. Notable examples of mechanisms of action include CD30 Antibodies and HER2 Antibodies. These antibodies pinpoint specific antigens present on the surface of cancer cells, enabling precise and targeted drug delivery. ADCs find End-User in the treatment of a wide spectrum of cancers. Notable indications include Lymphoma, Breast Cancer, Brain Tumor, Lung Cancer, Ovarian Cancer, and several others. The targeted therapeutic potential of ADCs benefits patients across diverse cancer Targets.

By Distribution Channel: The Distribution Channels of ADC technology span a spectrum, including Hospitals, Specialty Clinics, and other healthcare facilities. These institutions play a pivotal role in the administration and management of ADC-based treatments in the ADC Technology Industry, ensuring that patients receive the intended therapies effectively. The distribution channels for ADC products encompass Hospital Pharmacies, Retail Pharmacies, and various other avenues. Effective distribution mechanisms are essential to ensure that ADC therapies reach their intended patients efficiently. The ADC technology market derives strength from various technological platforms. Key players like Immunogen Technology, Seattle Genetics Technology, and Immunomedics Technology employ distinct approaches to ADC development, driving innovation within the field. Emerging technologies further contribute to the advancement of ADCs.

ADC Technology Market Regional Analysis

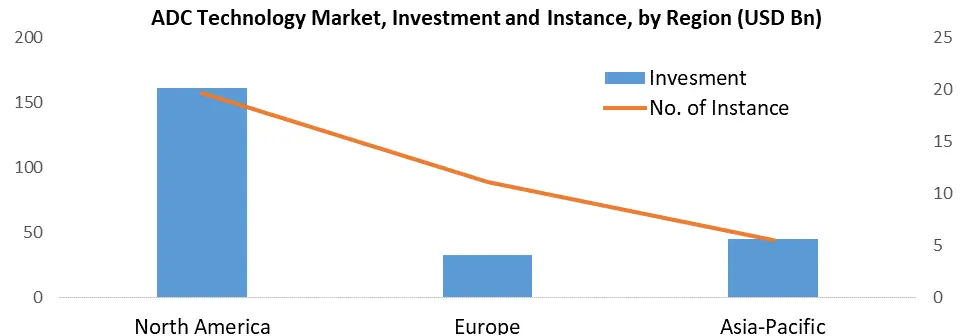

In recent years, the ADC (Antibody-Drug Conjugate) technology market has witnessed significant growth, particularly driven by the emergence of well-funded start-ups and small companies specializing in advanced linkers and potent warheads for ADCs. A mainstream of these advanced firms are grounded in North America, demonstrating the region's dominance in this sector. The United States Food and Drug Administration (FDA) has been prominently involved in swotting and approving ADC therapeutics for cancer treatment, therefore contributing to the region's prominence in the ADC technology landscape. One of the important key drivers for the of antibody-drug conjugates (ADC Technology Market) in North America is the upscaling incidence of cancer, prominently in the United States. On the basis of the data from the American Cancer Society, an estimated 1.9 million cancer diagnoses were projected in the US for the year 2023.

This alarming statistic underscores the pressing need for advanced therapeutic options, like ADCs, to combat this growing health challenge effectively. Several risk factors contribute to the high cancer incidence in North America, including tobacco use, excess body weight, excessive alcohol consumption, and exposure to infectious agents. These factors collectively propel the growth of the North American antibody drug conjugate market throughout the forecast period. The region's healthcare landscape is keenly focused on addressing these risk factors and improving cancer care, further facilitating the integration of ADCs into treatment protocols. To enhance the adoption of antibody-drug conjugates among the target population, ADC developers in North America are actively offering patient assistance and support programs. These initiatives play a crucial role in helping patients manage the often substantial medical expenses associated with cancer treatment in the ADC Technology Market. Notable examples of such programs include the Ambrx patient assistance program, Bayer oncology patient assistance program, and Genentech patient assistance program, which underscore the commitment of ADC Technology industry stakeholders to improving patient outcomes.

ADC Technology Market Competitive Landscape Analysis

In July 2023, AstraZeneca and Daiichi Sankyo's datopotamab deruxtecan emerged as a prominent ADC program. However, investor confidence wavered due to reports of "some" patient fatalities during its initial Phase 3 trial. Nevertheless, the study successfully met its objective by demonstrating that the drug improved progression-free survival compared to standard chemotherapy in second-line non-small cell lung cancer. In May 2023, Sony Corporation and Astellas Pharma Inc. entered a collaborative research agreement aimed at discovering a novel Antibody-Drug Conjugate (ADC) platform for oncology in the ADC Technology Market.

Leveraging Sony's unique polymeric material, KIRAVIA ADC is anticipated to selectively deliver anti-cancer drugs to target cells, thereby enhancing efficacy while reducing the side effects associated with anti-cancer drugs attacking normal cells. In April 2023, Germany's BioNTech inked a partnership with the Chinese biotech company DualityBio to jointly develop and commercialize two cancer antibody drug candidates, DB-1303 and DB-1311, as part of a combination therapy for solid tumors. DualityBio will retain commercial rights for mainland China, the Hong Kong Special Administrative Region, and the Macau Special Administrative Region, while BioNTech will have commercial rights for the rest of the world.

In January 2023, Bridge Biotherapeutics and Pinotbio signed a memorandum of understanding (MoU) to collaborate on the development of new therapeutic cancer candidates using the antibody drug conjugates platform technology. Under the agreement, Bridge Biotherapeutics will contribute private anticancer targets, while Pinotbio will provide linkers and drugs. In August 2022, GSK made a cash payment of $100 million to Mersana Therapeutics to expand its portfolio by adding a second ADC in the ADC Technology Market. This addition complements GSK's existing approved multiple myeloma drug, Blenrep. The agreement encompasses XMT-2056, Mersana's preclinical ADC asset designed for the treatment of various HER-2 cancers.

The global agreement grants GSK an exclusive option to co-develop and commercialize XMT-2056. In July 2023, Ambrx announced that the FDA had granted Fast Track designation to ARX517, its proprietary investigational anti-PSMA antibody-drug conjugate therapy. This designation is for the treatment of patients with metastatic castration-resistant prostate cancer (mCRPC) who have progressed on an androgen receptor pathway inhibitor. In July 2023, Mersana Therapeutics disclosed the publication of the topline data from the UPLIFT clinical trial, which focused on patients with platinum-resistant ovarian cancer. Additionally, the company announced strategic reprioritization efforts in the ADC Technology Industry.

ADC Technology Market Scope: Inquiry Before Buying

| ADC Technology Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 8.32 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 9.6% | Market Size in 2030: | US $ 15.82 Bn. |

| Segments Covered: | by Target | Antibody-Protein Toxin Conjugates Antibody-Chelated Radionuclide Conjugates Antibody-Small-Molecule Drug Conjugates Antibody-Enzyme Conjugates |

|

| by Product | Adcertis Kadcyla Others |

||

| by Mechanism of Action | CD30 Antibodies HER2 Antibodies |

||

| by Technology | Cleavable linkers Non-cleavable linkers Chemical conjugation Enzymatic conjugation |

||

| by Indication / Application | Lymphoma Breast Cancer Brain Tumor Lung Cancer Ovarian Cancer Others |

||

| by End-Users | Hospitals Specialty Clinics Others |

||

| by Distribution Channel | Hospitals Speciality clinics Retail Pharmacy Other healthcare facilities |

||

ADC Technology Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

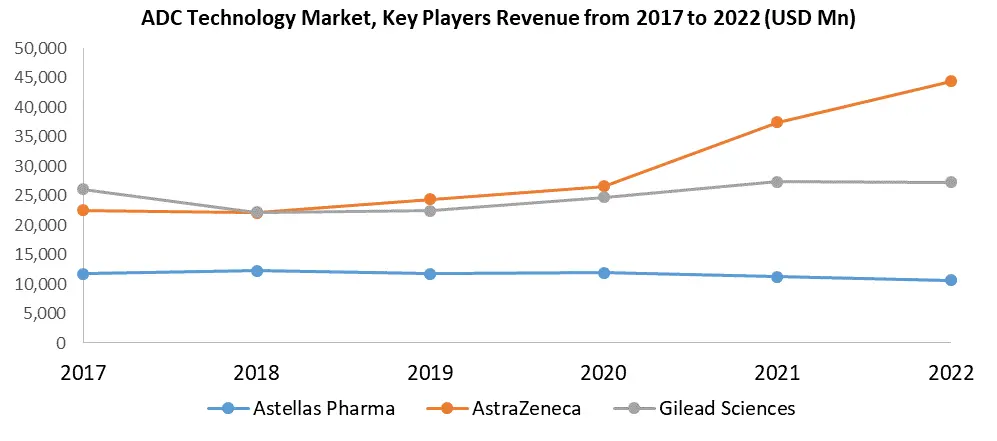

Key Players of the ADC Technology Market

1. ADC Therapeutics

2. Astellas Pharma

3. AstraZeneca

4. Byondis

5. Daiichi Sankyo

6. Genentech

7. Gilead Sciences

8. ImmunoGen

9. Pfizer

10. RemeGen.

11. BioNTech

12. DualityBio

13. Bridge Biotherapeutics

14. Pinotbio

15. GSK

16. Mersana Therapeutics

Frequently Asked Questions and Answers about ADC Technology Market

1. What is the ADC Technology Market?

Ans: ADC technology, or Antibody-Drug Conjugate technology, is a cutting-edge approach in the field of cancer therapeutics that combines monoclonal antibodies with cytotoxic drugs for targeted cancer treatment.

2. Why is ADC technology significant in the market?

Ans: ADC technology is significant because it offers precise and targeted delivery of cancer drugs to tumor cells, reducing side effects and increasing treatment efficacy.

3. What is the market size for the ADC Technology Market?

Ans: The ADC Technology Market CAGR 9.6 % with 15.82 Bn in 2030.

4. Which regions are driving the growth of the ADC technology market?

Ans: North America, with a high incidence of cancer and FDA approvals, is a major driver of ADC technology market growth.

5. What are the primary benefits of ADC technology for cancer treatment?

Ans: ADC technology offers benefits such as reduced toxicity, precise targeting of cancer cells, and increased treatment effectiveness, making it a promising avenue for cancer therapy.