3d Stacking Market Size by Interconnecting Technology, Device Type, Method, End-User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

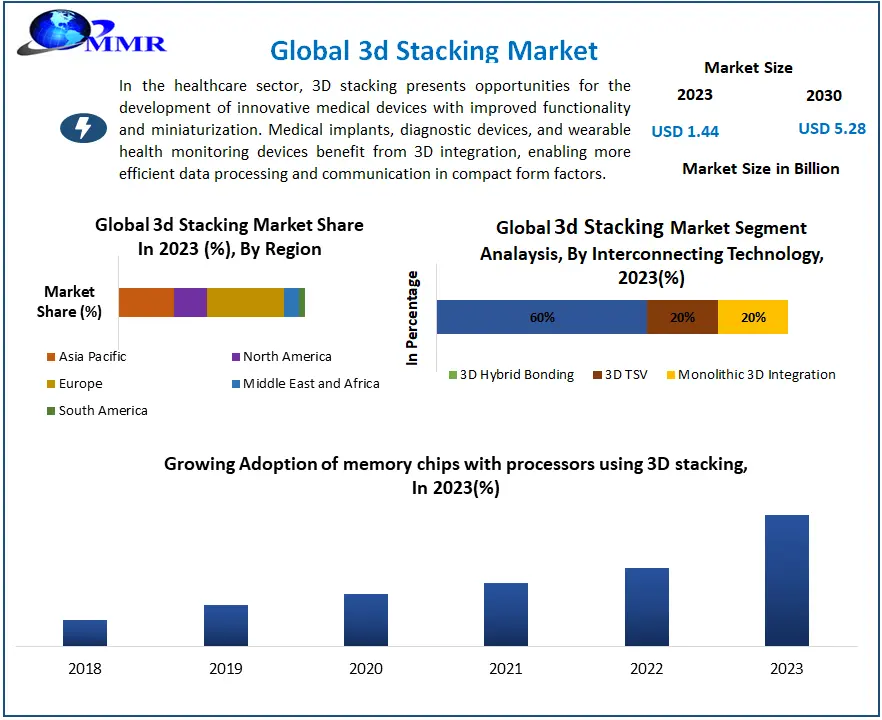

The 3d Stacking Market size was valued at USD 1.44 Billion in 2023 and the total 3d Stacking revenue is expected to grow at a CAGR of 20.4 % from 2024 to 2030, reaching nearly USD 5.28 Billion in 2030.

3d Stacking Market Overview

The MMR report provides a detailed analysis of 3D Stacking technology, and its significance across various industries, and outlines the objectives and scope of the study. The analysis of the market includes the global market size, growth projections, drivers, challenges, opportunities, and recent trends. It also offers an overview of 3D Stacking techniques in the technology landscape, detailing their advantages, limitations, and emerging innovations. Also, the report examines market segmentation by technology, application, end-user, and region, with a detailed analysis of each segment's market size, growth, and potential. It also provides a detailed examination of key application areas, market trends, drivers, and challenges, along with insights from end-user industries, including requirements, challenges, and adoption trends. The increasing demand for high-density, high-bandwidth memory, such as 3D NAND flash and HBM, drives significant investment. Emerging applications such as automotive electronics, AR/VR gadgets, and AI accelerators provide significant opportunities. Investing in technology improvements such as TSVs, interface innovations, and innovative materials can yield large benefits. Additionally, supporting infrastructure, design tools, and standardization projects in the ecosystem development space offer significant investment opportunities. These developments highlight a dynamic environment filled with potential for investors looking to profit from the growing market for memory devices and related technologies in a variety of application fields.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Continuous innovation is driven by ongoing improvements in 3D Stacking technology, materials, and design techniques. The growing desire for smaller, lighter, and more powerful electronic equipment in a variety of applications drives the trend toward miniaturization. Also, integrating many components involving as CPUs, memory, and sensors into a single container allows for increased functionality and performance. Government measures in China and South Korea promote chip development and advanced packaging technologies, creating an atmosphere conducive to technological advancement and commercial expansion.

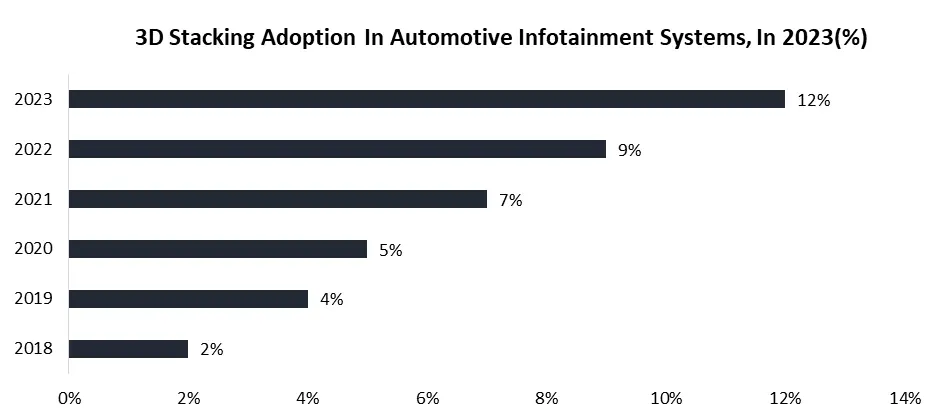

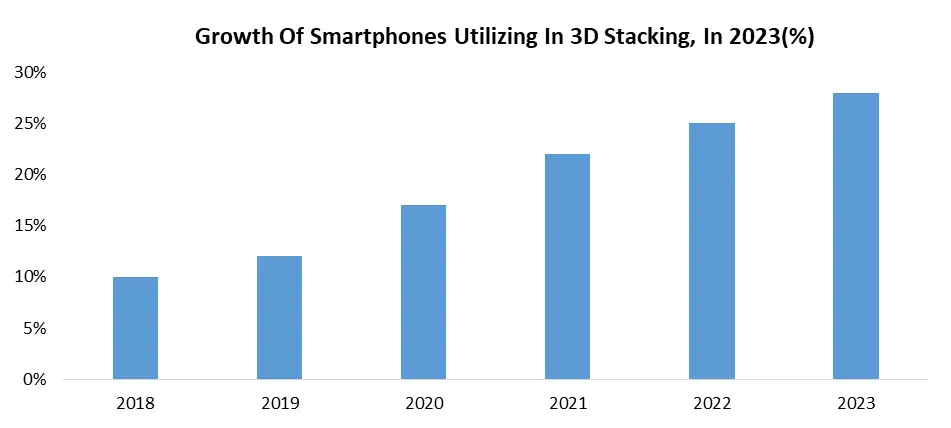

These variables combine to create a dynamic ecosystem marked by rapid technical change and promising potential for industry stakeholders. 3D Stacking technology gains popularity in smartphones, wearables, and mobile devices, then grows into car electronics for ADAS and autonomous driving, and finally into AR/VR, medical devices, and industrial automation. It aims to reduce costs and improve thermal management, as well as standardize interfaces and design standards to facilitate ecosystem development.

3d Stacking Market Dynamics

Miniaturization and Form Factor Reduction

Stacking different components such as as processors, memory, and sensors in a single stack improves the capability of tiny devices. It minimizes device size and weight, which are essential to mobile, wearable, and IoT applications. Shorter signal paths inside a stack improve data transmission rates and device performance. Investments in downsizing drive developments in 3D Stacking technologies including through-silicon vias and interposers. 3D Stacking has uses beyond smartphones and PCs, including wearables, AR/VR devices, and IoT sensors. Established heavyweights such as TSMC and Samsung fight with start-ups, resulting in a dynamic market landscape.

Growth of Venture capital funding in 3D Stacking start-ups

Integration of Diverse Functionalities

The 3D Stacking market's disruptive opportunity derives from its capacity to vertically stack several chip functionalities, revolutionizing gadget capabilities. Devices grow more feature-rich and functional by combining varied components such as processors, memory, sensors, and RF in a single box. Furthermore, shorter interconnects inside the stack improve data transfer speeds and overall device performance as compared to typical side-by-side positioning. Also, this technology improves the range of applications, making it easier to construct AI-powered devices, autonomous systems, and linked medical devices with a variety of features in small form factors. 3D Stacking's expansion into non-traditional sectors including automotive, healthcare, and AR/VR, driven by its capacity to integrate diverse functionalities, creates new market segments. The diversification amplifies market size, driven by the escalating demand for feature-rich devices across industries, anticipated to reach USD 47.4 billion by 2030. The pursuit of integrated solutions spurs innovation in 3D Stacking technologies, intensifying competition and developing a dynamic competitive landscape with the emergence of new players. The ecosystem of innovation and competition drives the continuous evolution and adoption of 3D Stacking across a broad spectrum of applications and industries.

Lack of Standardization and Ecosystem Development

Limited interoperability due to the absence of standard protocols deters collaboration and wider adoption. Custom design efforts and increased costs arise from the lack of standards, complicating deployment. Market growth is slowed because of interoperability issues and ecosystem fragmentation, deterring investment in technology with uncertain compatibility. Despite technological advancements, concerns about interoperability limit widespread implementation. Investors are concerned about the lack of rules, which might stifle funding and innovation. The fragmented environment, defined by proprietary solutions from various competitors, results in a fractured market landscape with little collaboration. The absence of coordination stunts industry growth and impedes the development of complete solutions. To address these difficulties, we must work together to define common standards, encourage stakeholder collaboration, and promote investment in interoperable technologies. Only via such measures the sector overcome deployment bottlenecks, increase investor confidence, and realize the full potential of emerging technology.

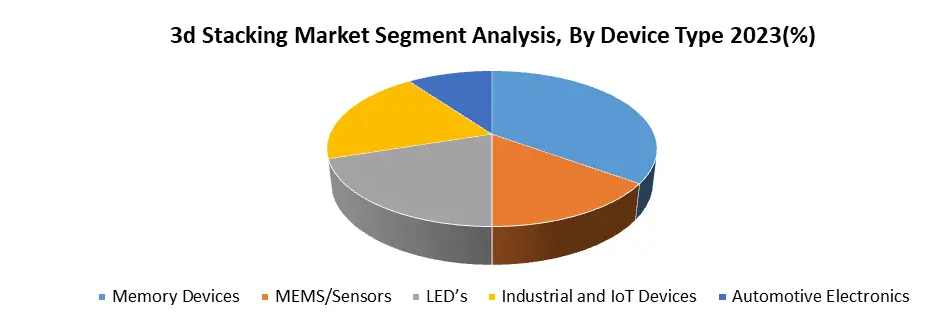

3d Stacking Market Segment Analysis

By Device Type, the Memory Devices segment accounts for an estimated 35% of the overall 3d Stacking Market. The increasing demand for memory in AI, high-performance computing, and mobile devices has outpaced the capacity of traditional 2D memory technology. To solve this, 3D Stacking encourages research and development in critical areas. TSVs provide vertical connections between memory levels, increasing density and bandwidth. Advances in interfaces such as CXL (Compute Express Link) are critical for efficient data transfer between stacked memory and CPUs.

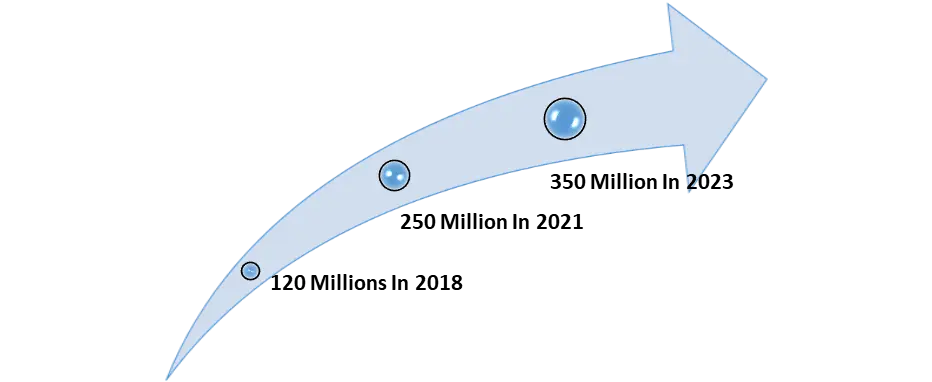

The ongoing research into new materials and technologies aims to provide denser and more efficient memory cells, satisfying the demand for high-density and high-bandwidth memory solutions in a variety of applications. Memory devices account for more than 30% of the 3D Stacking market, with significant expenditures from industry players such as Samsung, SK Hynix, Micron, and TSMC. Growing demand pushes funding for start-ups and collaborations between memory makers and system integrators to create and integrate 3D memory systems. 3D stacked memory improves high-performance computing (HPC) by making servers denser and faster, which is necessary for complicated simulations and data analysis. Integrated memory in mobile devices improves performance, power efficiency, and multitasking capabilities. In addition, 3D memory shows promise in emerging applications such as AI accelerators, driverless vehicles, and AR/VR devices, which require high bandwidth and density.

3d Stacking Market Regional Insights

Asia Pacific accounted for over 45% of global 3D Stacking market revenue. The region has a strong electronics manufacturing sector, with companies including TSMC and Samsung driving innovation in technologies such as 3D Stacking. The strong basis encourages the deployment of innovative semiconductor solutions. The region's rapidly increasing demand for smartphones, smartwatches, and other electronic gadgets focuses on the importance of downsizing and improved performance, both of which 3D Stacking efficiently addresses. Also, government support from countries such as China and South Korea, in the form of financial incentives and infrastructure improvements, accelerates domestic chip development and the advancement of innovative packaging technologies, contributing to the electronics industry's long-term growth. TSMC has allocated USD 25 billion for 3D Stacking technology, increasing regional capacity and R&D. China increases 3D NAND flash output, increasing its market share. South Korea supports heterogeneous integration, which combines many chip types in a single stack to increase application potential while increasing industry focus on advanced semiconductor solutions. China influences the regional market share thanks to a strong manufacturing sector, government support, and rising domestic electronics demand. However, South Korea, Taiwan, and Japan show significant development potential, with increasing investments in 3D Stacking technologies, indicating more competition and innovation in the market.

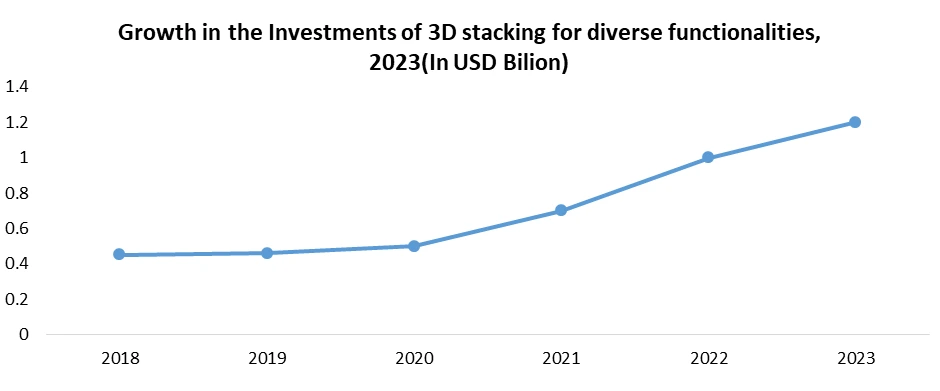

1. According to MMR Analysis, Nikkei Asia's total investment in 3D Stacking start-ups in Asia Pacific reached 2.6 Billion in 2023 as compared to USD 1.1 Billion in 2020.

3d Stacking Market Competitive Landscape

In 2022, Taiwan-based TSMC announced a significant USD XX billion investment in 3D Stacking technology, indicating a strong commitment to progress in this industry. The expenditure seeks to increase TSMC's production capacity, improve its R&D activities, and strengthen its market position in the region. Similarly, Samsung of South Korea has budgeted USD XX billion for a new chip production plant in 2022, with a focus on advanced packaging, including 3D Stacking. The huge investment improves Samsung's production capacity and increases its competitiveness in the 3D Stacking market.

In Japan, JCET (Jiangsu Changjiang Electronics Technology) has secured a USD XX Billion investment from the Development Bank of Japan in 2023 to assist in the development of 3D Stacking technology. The funding allows JCET to focus on research and development, potentially positioning them as a major competitor in the market. Ultimately, JCET in China received a significant USD 3.2 billion in government financing in 2021 to develop advanced packaging technologies such as 3D Stacking. It demonstrates substantial government backing for local chip development and establishes JCET as a major player in China's fast-growing 3D Stacking industry. Overall, these investments demonstrate the growing importance and competition among important companies in the worldwide 3D Stacking market.

3D Stacking Industry Ecosystem

3d Stacking Market Scope:Inquire Before Buying

| Global 3d Stacking Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 1.44 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 20.4% | Market Size in 2030: | US $ 5.28 Bn. |

| Segments Covered: | by Interconnecting Technology | 3D Hybrid Bonding 3D TSV Monolithic 3D Integration |

|

| by Device Type | Memory Devices Opto-electronics Processors and Logic Devices MEMS/Sensors Power Management Devices Others |

||

| by Method | Die-to-Die Die-to-Wafer Wafer-to-Wafer Chip-to-Chip Others |

||

| by End-User | Consumer Electronics Automotive Manufacturing Communication Healthcare and Medical Devices Others |

||

3d Stacking Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players in the 3d Stacking Market

1. TSMC (Taiwan Semiconductor Manufacturing Company)

2. Intel Corporation

3. Samsung Electronics Co., Ltd.

4. Advanced Micro Devices (AMD)

5. Micron Technology, Inc.

6. STMicroelectronics N.V.

7. Qualcomm Incorporated

8. Texas Instruments Incorporated

9. Broadcom Inc.

10. NVIDIA Corporation

11. Hynix Semiconductor Inc.

12. GlobalFoundries Inc.

13. ON Semiconductor Corporation

14. Renesas Electronics Corporation

15. ASML Holding N.V.

16. Infineon Technologies AG

17. Analog Devices, Inc.

18. IBM Corporation

19. NXP Semiconductors N.V.

20. Sony Semiconductor Solutions Corporation

FAQs:

1. What are some of the challenges associated with 3D Stacking implementation?

Ans. Challenges of 3D Stacking implementation include technical hurdles such as thermal management, alignment and bonding issues, manufacturing complexity, cost considerations, and compatibility with existing semiconductor fabrication processes.

2. Which industries are driving the adoption of 3D Stacking technology?

Ans. Industries such as consumer electronics, data centers, automotive, medical devices, industrial automation, and artificial intelligence (AI) accelerators are driving the adoption of 3D Stacking technology due to its potential to address the growing demand for higher-performance and compact electronic systems.

3. What is the projected market size & and growth rate of the 3D Stacking Market?

Ans. The 3D Stacking Market size was valued at USD 1.44 Billion in 2023 and the total 3D Stacking revenue is expected to grow at a CAGR of 20.4% from 2023 to 2030, reaching nearly USD 5.28 Billion in 2030.

4. What segments are covered in the 3D Stacking Market report?

Ans. The segments covered in the 3D Stacking market report are Interconnecting Technology, Device Type, Method and End-Users.