Tesla and BYD Are Triggering the Biggest Auto Industry Shock Since Ford Invented Mass Production

Global EV sales are exploding, battery costs are collapsing, and traditional automakers are suddenly fighting for survival in a market racing toward USD 4.92 trillion by 2032.

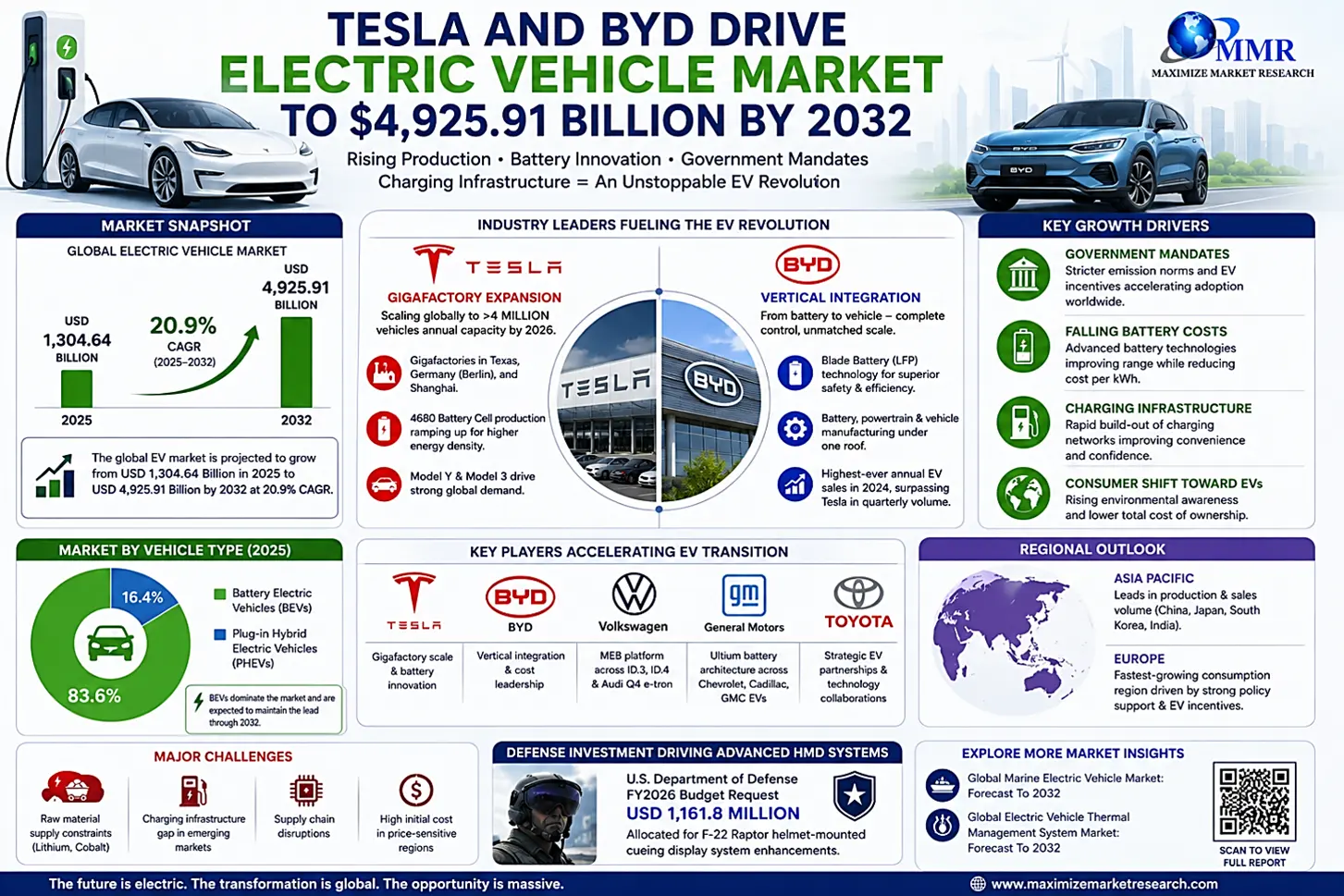

The electric vehicle war just entered a new phase. Tesla is expanding Gigafactories across Texas, Berlin, and Shanghai. BYD has now surpassed Tesla in quarterly EV unit sales globally. And legacy automakers are accelerating billion-dollar EV transitions faster than analysts expected.

The result?

The Global Electric Vehicle Market, valued at USD 1,304.64 billion in 2025, is projected to surge to USD 4,925.91 billion by 2032, growing at a staggering 20.9% CAGR, according to Maximize Market Research.

The Real EV War Is No Longer About Cars

Industry executives now believe the real battle is shifting away from vehicle design —

and toward batteries, raw materials, and manufacturing scale.

Tesla’s Berlin Gigafactory is ramping 4680 battery production targeting:

- lower battery costs

- longer range

- faster scalability

Meanwhile, BYD’s Blade Battery technology is rapidly gaining traction globally for its:

- thermal safety

- lower fire risk

- higher efficiency

The company’s vertically integrated structure — controlling battery cells, powertrains, and final assembly — is increasingly viewed as one of the strongest competitive models in the global EV race.

“Once EV range parity meets mass-market pricing, the biggest consumer barrier disappears,” said an industry analyst tracking European EV adoption.

Europe’s Auto Industry Is Under Pressure

The shift is becoming especially aggressive in Europe, where tightening emissions mandates and ICE phase-out policies are accelerating EV demand faster than many suppliers anticipated.

Volkswagen is rapidly expanding its MEB platform across ID-series vehicles, while General Motors continues scaling its Ultium battery architecture across Chevrolet, Cadillac, and GMC lineups.

At the same time, governments are pouring billions into:

- charging infrastructure

- battery supply chains

- EV incentives

- grid modernization

The objective is no longer “encouraging” electrification.

It is forcing it.

Asia Still Controls the Industry’s Center of Gravity

Asia-Pacific remains the world’s dominant EV production hub, led by:

- China

- South Korea

- Japan

But Europe is now emerging as the fastest-growing consumption market globally.

The problem?

Supply chains remain fragile.

Lithium shortages, cobalt dependency, and charging infrastructure gaps continue creating major pressure points across the industry.

That has transformed battery minerals into geopolitical assets.

Why Investors Are Flooding into EV Infrastructure

Analysts say the Electric Vehicle Market’s projected rise toward USD 4.92 trillion is now extending far beyond vehicle sales.

Growth is accelerating across:

- battery manufacturing

- charging networks

- energy storage systems

- EV software ecosystems

- autonomous mobility infrastructure

In other words:

The Electric Vehicle Market is no longer just an automotive industry story. It is becoming an energy and technology infrastructure story.

Final Take

The Global Automotive Industry spent more than 100 years optimizing combustion engines.

Now Tesla and BYD are forcing the entire sector to rebuild itself around batteries, software, and energy ecosystems – at a speed few traditional automakers expected. And as governments tighten mandates and battery costs continue falling, the companies controlling EV infrastructure may ultimately become the most powerful industrial players of the next decade.