Water Treatment Chemicals Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

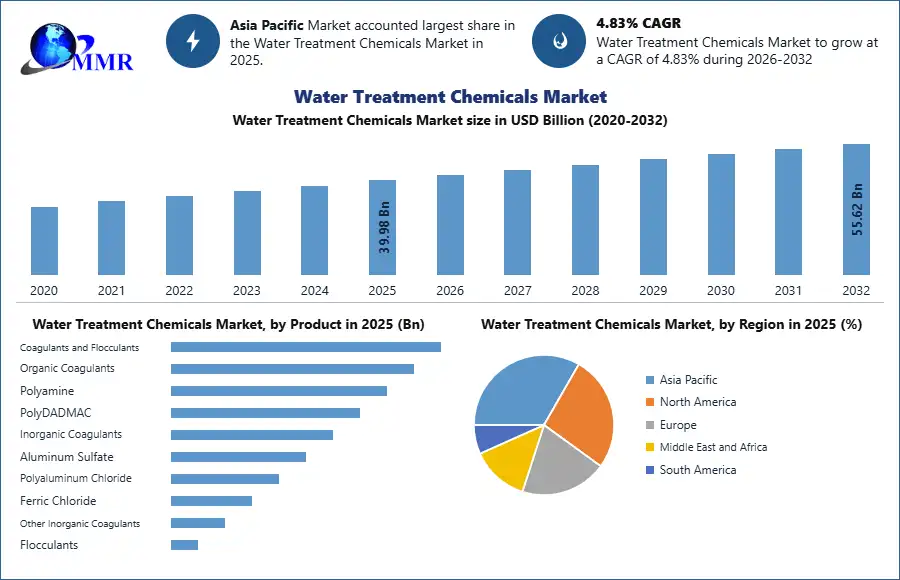

Global Water Treatment Chemicals Market size was valued at USD 39.98 Bn. in 2025, and the total Water Treatment Chemicals Market revenue is expected to grow by 4.83% from 2026 to 2032, reaching nearly USD 55.62 Bn.

Water Treatment Chemicals Market Overview:

Water treatment chemicals serve to ensure that water is safe, pure, and suitable for a multitude of by Sources from municipal water treatment, power generation, oil and gas, food and beverage, and pharmaceuticals. In general terms, water treatment chemicals are used to eliminate contaminants, address scale and corrosion, control microbial growth, and enhance the quality of the water. Water treatment chemicals have come a long way from simple disinfectants (i.e., chlorine) to anti-scalants, coagulants & flocculants, to pH modifiers, biocides, and all of these additions are due to advancing technology coupled with stricter compliance to environmental regulations.

Furthermore, with the rising urbanization and industrialization around the world, and growing awareness of the health effects of waterborne illness, the growth of the global water treatment chemical market looks promising. The call for clean water is the loudest in some of the Asia Pacific region, where a recent surge of industrialization, combined with government action, has impacted both the water treatment chemical growth drivers in general as well as coatings, cooling tower treatments, and fire-hot water tank treatments.

In North America and Europe, strict environmental policies and movement toward sustainable solutions place demand for eco-friendly and bio-based water treatment chemicals on the rise, sometimes creating opportunities for industrial byproducts with renewable alternatives like polyaspartic acid or chitosan as natural biodegradable scale inhibitors.

The report Water Treatment Chemicals Market covered a detailed overview of high-level drivers such as advancements in water treatment technologies and services by Sources, along with market conditions regarding increasing opportunities across all end-use industries, along with investment in wastewater treatment systems to assist in delivering strategic third-party use. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Water Treatment Chemicals Market Dynamics

RiSinging Water Contamination and Regulatory Pressures to Drive Growth in the Water Treatment Chemicals Market

The water treatment chemicals market is expanding significantly, with factors such as rising contamination levels of water, along with an increase in global water consumption, driving the demand for water treatment and reuse solutions in municipal, industrial, and residential sectors. As governments increasingly regulate water quality, industrial and municipal users of water must implement a new generation of water treatment chemicals to meet total suspended solids (TSS) and pollutant levels; this is supporting growth in the water treatment chemicals market. Rapid industrialization (particularly in developing economies) coupled with the increase of global populations, is creating a greater need for treated water in key global industries in medicine, energy, food & beverage, and pharmaceuticals, all of which are critical to quality and regulatory compliance.

High Costs and Technological Shifts to Restrain Water Treatment Chemicals Market

The market for water treatment chemicals faces a number of limitations in terms of growth, including the high cost of raw materials and specialty chemicals, driving end-users to consider cheaper options, leading to potential reductions in demand. The adoption of advanced treatment technologies such as membrane filtration, UV treatment, and electrochemical processes reduces the use of its conventional chemical solutions and constitutes an opposition to its growth. The enhanced water quality requirements have also increased scrutiny of biocides, which are now seen as possible contaminants and less as treatment options, especially in industries that require ultra-pure water, such as pharmaceutical and electronic manufacturing. Taken together, these factors inhibit the development of this market for water treatment chemicals and their eventual usage.

Water Treatment Chemicals Market Segment Analysis

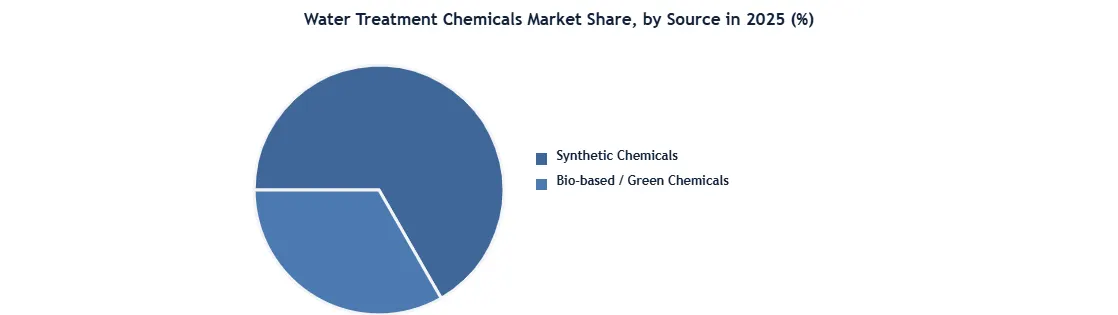

By source,The synthetic chemicals segment dominates the global water treatment chemicals market, accounting for the largest share due to its widespread use in municipal and industrial treatment systems. These chemicals include coagulants, flocculants, biocides, corrosion inhibitors, and pH stabilizers manufactured from petrochemical and inorganic feedstocks. Their strong performance, lower cost, and established supply chains make them the preferred option across power plants, manufacturing units, oil & gas, and municipal utilities. In 2025, synthetic chemicals represented the overwhelming majority of market demand because conventional treatment infrastructure globally is designed around these formulations. Their effectiveness in removing contaminants, controlling scaling, and maintaining system efficiency continues to support dominance, especially in large-scale industrial operations and developing economies expanding wastewater treatment capacity.

The bio-based/green chemicals segment is smaller but expanding at a faster growth rate due to increasing sustainability targets and stricter environmental regulations. These chemicals are derived from renewable sources such as plant extracts, chitosan, starch, enzymes, and biodegradable polymers. Demand is rising in regions such as Europe and North America where industries are shifting toward low-toxicity, eco-friendly treatment solutions. Bio-based chemicals are gaining adoption in food processing, municipal treatment, and environmentally sensitive industrial applications because they reduce sludge generation and lower environmental impact. Although still niche compared to synthetic products, this segment is expected to grow rapidly as governments encourage green chemistry adoption and companies invest in circular water treatment technologies.

By Product Type, the water treatment chemicals market is segmented into flocculants & coagulants, biocides & disinfectants, defoamers & defoaming agents, pH adjusters & softeners, and corrosion inhibitors. The flocculants & coagulants segment dominated the water treatment chemicals market in 2025, due to the important function they fulfil in municipal and industrial wastewater treatment for the removal of suspended solids and organic contaminants. Biocides & disinfectants play equally crucial roles with respect to microbial control; however, they are presently experiencing scrutiny from regulators. Defoamers & anti-foaming agents have been gaining steady demand by numerous industries for the ease and operational consistency they provide with foam from operational functions. pH adjusters & softeners remain critical in boiler and cooling water treatments, and corrosion inhibitors are still mission-critical to protect major industrial infrastructure. While traditional chemical products are dominant today in the market, growing concerns for the environment have inspired innovation for more environmentally friendly products.

Water Treatment Chemicals Market Regional Insights

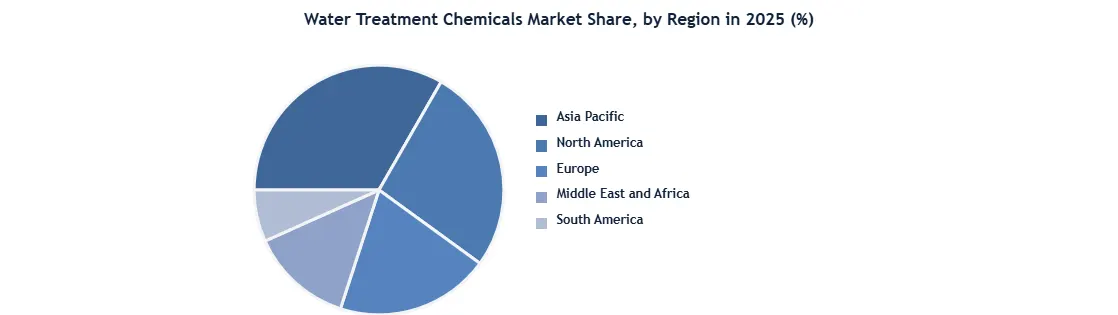

Asia-Pacific dominates the global water treatment chemicals market and accounted for the leading share in 2025. The region’s growth is driven by rapid industrialization, urban expansion, and rising investments in municipal wastewater treatment infrastructure. Countries such as China, India, and Japan are increasing demand due to stricter wastewater discharge norms and expanding industrial sectors including power, textiles, chemicals, and manufacturing. Large-scale public water projects and desalination investments continue to support market expansion. Asia-Pacific represented the largest regional demand globally, with nearly 40% market share in 2025.

North America held a significant market share due to mature municipal water systems and strict environmental compliance standards. The United States leads regional demand because of aging infrastructure replacement, industrial wastewater treatment, and stringent EPA regulations. Increased adoption of advanced specialty chemicals in power generation, food processing, and oil & gas supports continued market growth. Digital monitoring and smart dosing systems also strengthen demand for premium chemical solutions.

Europe shows steady growth driven by sustainability goals, circular water management, and strict industrial effluent regulations. Major countries including Germany, France, and United Kingdom are focusing on eco-friendly and bio-based treatment chemicals. Strong industrial recycling programs and regulations under EU water directives continue to increase specialty chemical adoption.

Middle East & Africa and Latin America are emerging markets due to increasing desalination, water reuse projects, and industrial water treatment investments. Countries such as Saudi Arabia, South Africa, and Brazil are investing in water security and municipal treatment systems, creating new opportunities for suppliers.

Water Treatment Chemicals Market Competitive Landscape

The global water treatment chemicals market is characterized by intense competition among established market participants such as Ecolab Inc., SUEZ SA, Kemira Oyj, BASF SE, and Solenis, who utilize technological innovations, strategic acquisitions, and global distribution channels to maintain their leading position. Ecolab leads the market through Nalco Water and advanced digital monitoring systems.

SUEZ is focused on progress in its circular water solutions portfolio and bio-based chemicals. Kemira's focus is on the pulp & paper industry, and BASF is leveraging its chemicals expertise for corrosion inhibitors and scale control. The market also continues to see increasing competition in Asia-Pacific from regional players, especially Chinese companies like SNF Floerger, which are positioned as low-cost alternatives.

Competitive marketing strategies, include R&D direction in green chemistry potential, as well as relationship and partnership building with industrial end-users. Water scarcity in emerging markets is an expanding opportunity for companies. Companies are also exploring sustainability initiatives and compliance with stringent environmental regulations because customers are increasingly focused on environmentally friendly water treatment solutions.

Water Treatment Chemicals Market Key Developments

• SUEZ SA (France) announced in April 2025 the development of a new bio-based flocculant, BioFloc, made from plant extracts, to comply with the more stringent sustainability standards imposed by the EU for the municipal wastewater market. In testing, BioFloc was noted to reduce sludge volume by 30% relative to synthetic flocculants.

• Kemira Oyj (Finland) launched Kemira ASF 4600, an anti-scalant for high-temperature desalination plants, in March 2025, to provide a solution for mineral fouling in the Middle East and North African markets. Its phosphate-free formula is compliant with discharge norms, which are especially stringent in the region.

• BASF SE (Germany) announced the expansion of its Sokalan polymer product line in 2024 with Sokalan ECO, a biodegradable corrosion inhibitor for cooling towers. This biodegradability has become increasingly important for power plants under mandate by the EPA to use more environmentally friendly materials based on EPA scrutiny.

• Solenis LLC (USA) entered into a partnership with Samsung C&T in April 2025 to provide green biocides to smart cities in Southeast Asia that emphasize closed-loop water recycling in high-rise buildings.

• In May 2025, Ecolab Inc. (USA) launched an AI-powered water management platform, Nalco Water Vision, featuring real-time analytics and predictive maintenance capabilities for industrial water systems. Nalco Water Vision is being adopted by major food & beverage and pharmaceutical manufacturers to reduce water waste and optimize chemical dosing.

Water Treatment Chemicals Market Key Trends

| Category | Key Trend | Example Product/Initiative | Market Impact |

| Bio-Based Chemicals | Shift toward sustainable, plant-derived formulations | SUEZ BioFloc™ bio-based flocculant | 25% growth in EU/NA markets, driven by stricter environmental regulations (2025) |

| Smart Water Solutions | AI-driven dosing and real-time monitoring | Ecolab Nalco Water Vision™ | 20% efficiency gains in industrial plants; reduces chemical waste by 15–30% |

| High-Efficiency Coagulants | Demand for rapid heavy metal removal | SNF Floplus™ Giga (mining sector) | 50% faster sludge precipitation; adopted in Latin American mining (2025) |

| Ultrapure Water Tech | Low-residue chemicals for semiconductors | Lonza Hydropure™ biocide | Growing demand from chipmakers (e.g., TSMC, Intel) amid the global semiconductor boom |

Water Treatment Chemicals Market Scope: Inquire before buying

| Water Treatment Chemicals Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 39.98 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.83% | Market Size in 2032: | 55.62 USD Billion |

| Segments Covered: | by Product | Coagulants and Flocculants Organic Coagulants Polyamine PolyDADMAC Inorganic Coagulants Aluminum Sulfate Polyaluminum Chloride Ferric Chloride Other Inorganic Coagulants Flocculants Anionic Flocculants Cationic Flocculants Non-Ionic Flocculants Amphoteric Flocculants Defoamers and Antifoaming Agents Oxygen Scavengers Corrosion Inhibitors Anodic Inhibitors Cathodic Inhibitors Biocides and Disinfectants Oxidizing Non-Oxidizing Disinfectants Sludge Conditioners Scale Inhibitors Phosphonates Carboxylates / Acrylic Other Scale Inhibitors Activated Carbon / Odor Removal Chemicals Other Product Types |

|

| by Source | Synthetic Chemicals Bio-based / Green Chemicals |

||

| by Treatment Stage | Primary (Coagulation-Flocculation) Secondary (Biological Adjunct Chemicals) Tertiary and Advanced (AOPs, Disinfection) Sludge Handling and Conditioning |

||

| by Application | Effluent Water Treatment Boiler Cooling Water Desalination Raw Water Treatment Others |

||

| by End-Use Industry | Municipal Power Generation Oil & Gas Chemical Manufacturing Mining & Metals Food & Beverage Pulp & Paper Textile Pharmaceuticals Others |

||

Water Treatment Chemicals Market, by Region:

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

North America (United States, Canada, and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Water Treatment Chemicals Market Key Players:

- Suez SA

- BASF SE

- Solenis

- Nouryon

- Kemira

- Baker Hughes Company

- Dow

- SNF

- Cortec Corporation

- Ecolab

- Aditya Birla Chemicals

- AECI Water

- Albemarle

- Buckman

- Chemtrade Logistics

- DuPont

- Genesys RO

- Ion Exchange

- Kurita Water Industries

- Lanxess

- Solvay

- Sudoc

- Thermax

- GE Water

- Veolia Water Technologies

- Watch Water

- Akzo Nobel NV

- LG Chem Ltd.

- Merck KGaA

- Evonik Industries AG

- Mitsubishi Chemical Corportion

- Huntsman Corporation

- Clariant AG

- Arkema S.A.

- Accepta Ltd

- Aries Chemical

- BWA Water Additives

- H2O Innovation

- Feedwater Ltd

- Calgon Carbon

- IDE Technologies

- Toshiba Water Solutions

- Metito

- Remondis Industrial

- Organica Water

- Samco Technologies

- Hindustan Dorr-Oliver

- Triveni Engineering

- WesTech Engineering

- Gradiant

- RWL Water (merged w/ Fluence)

- Driplex Water Engineering

- Voltas Water (Tata Group)

- Aquaflow Systems

- SFC Environmental

- Others