Virtual Schools Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

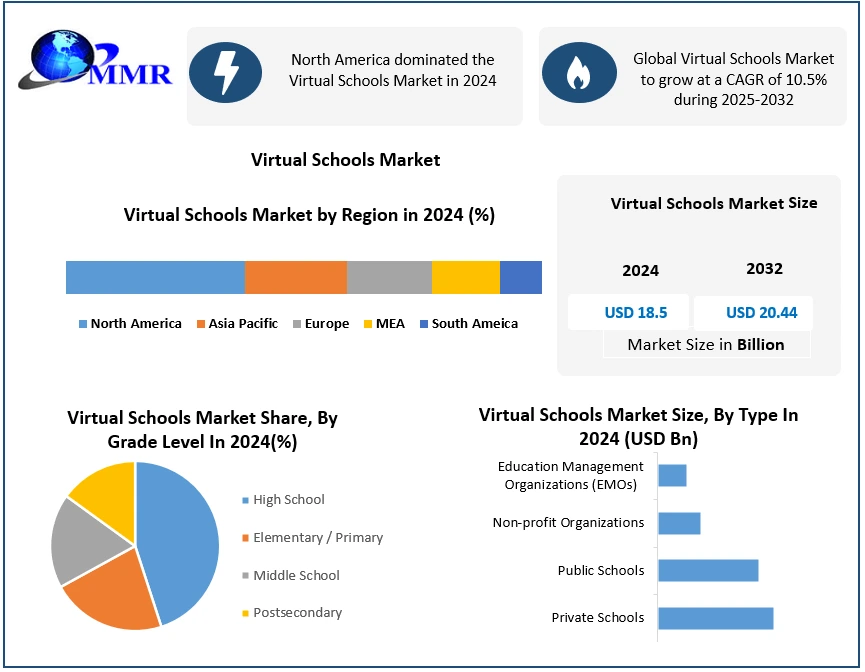

Virtual Schools Market was valued at USD 18.5 Billion in 2024, and total global Virtual Schools Market revenue is expected to grow at a CAGR of 10.5% from 2025 to 2032, reaching nearly USD 20.44 Billion. Rising digital adoption and demand for personalized learning.

The Virtual Schools Market has experienced rapid growth in recent years, driven by advancements in technology and evolving educational needs. Virtual schools, also known as online schools or cyber schools, are institutions that offer courses entirely or primarily through digital platforms, allowing students to attend classes remotely from anywhere with an internet connection. These schools cater to a wide range of students, including K-12 students, college students, and adult learners seeking professional development or continuing education.

Several factors are driving the growth of the virtual schools industry. The increasing adoption of technology in education has facilitated the development of sophisticated online learning platforms that offer interactive and engaging educational experiences are expected to be the major factor boosting the global virtual schools market growth. Additionally, the flexibility and accessibility provided by virtual schools appeal to students who require a more personalized learning environment, such as those with busy schedules, geographical constraints, or special learning needs. Moreover, the COVID-19 pandemic has accelerated the adoption of virtual schooling as traditional educational institutions shifted to remote learning to ensure continuity of education.

In addition, increasing demand for flexible learning solutions, rising internet penetration, and advancements in educational technology are expected to be major factors influencing the virtual schools market growth. Additionally, governments and educational institutions are increasingly recognizing the potential of virtual schools to improve access to quality education and bridge the gap in educational attainment. Key players such as K12 Inc., Connections Academy, and Florida Virtual School are significantly impacting the market growth by providing scalable, high-quality virtual education solutions.

Their innovative online platforms cater to diverse educational needs, driving adoption among students seeking flexible learning options. These players have expanded access to education, particularly during the COVID-19 pandemic, accelerating the shift towards virtual schooling. Additionally, their established reputations and widespread reach contribute to the overall credibility and growth of the virtual schools market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Virtual Schools Market Trends:

The rise of virtual K-12 schools

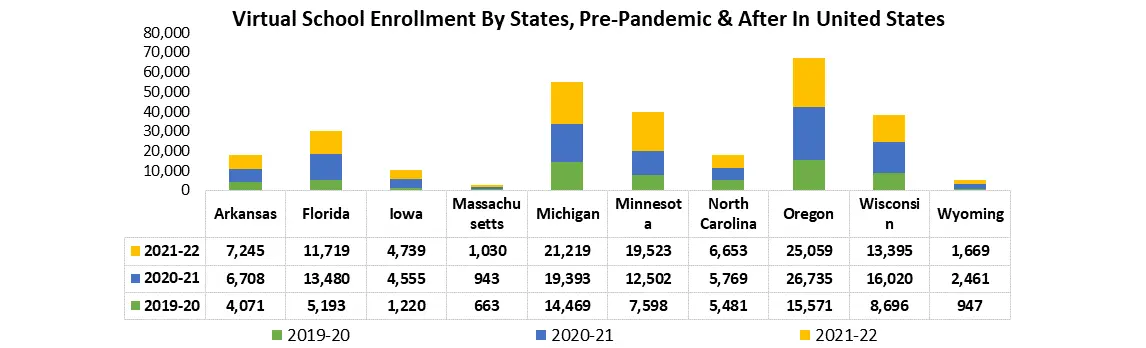

The rise of virtual-only K-12 schools is expected to be a significant factor driving the virtual schools market across the world. As education leaders and stakeholders navigate beyond the pandemic, an increasing number of students are opting for online learning as a permanent educational solution. This trend is exemplified by instances such as Fort Smith Public Schools in Arkansas, which experienced a surge in online enrollment from an initial expectation of 500 to a staggering 3,500 students. The district's response to this demand involved intensive training for staff, technological resource mobilization, and the implementation of a standardized virtual curriculum. Despite initial challenges, such as addressing the digital divide and ensuring equitable access to technology, school districts like Fort Smith have adapted by providing mobile hotspots, transforming school premises into Wi-Fi hubs, and ensuring device availability, such as Chromebooks, for all students.

Distribution of Virtual Schools and Students by Operator Status, In United States 2021- 22

| Total Number of Schools in 2021-22 | Percent of All Schools | Students | Percent of All Enrollment | Average Enrollment Per School | |

| Independent | 494 | 68.0% | 277,593 | 48.0% | 562 |

| Nonprofit EMO | 52 | 7.2% | 34,096 | 5.9% | 656 |

| For-profit EMO | 180 | 24.8% | 266,970 | 46.1% | 1,483 |

| Total for All Virtual Schools | 726 | 100.0% | 578,659 | 100.0% | 797 |

This shift towards virtual education is not limited to a single district; rather, it reflects a broader trend observed across the educational landscape. The pandemic has acted as a catalyst, accelerating plans for virtual-only schools that extend beyond the crisis period. According to an MMR analysis, 1 in 5 schools have either adopted or plan to adopt virtual schooling post-pandemic. This shift underscores a fundamental change in how education is delivered, with a growing recognition that virtual learning offers a viable alternative for many students. Factors driving this transition include the realization that virtual learning better accommodates diverse learning styles and preferences. Some students thrive in a virtual environment, finding it to be a better fit for their educational needs. These all factors collectively influenced the virtual schools market.

Additionally, the flexibility inherent in online learning allows for personalized, competency-based instruction, enabling students to progress at their own pace. For instance, schools like the Jordan School District in Utah are implementing competency-based learning models, emphasizing flexibility and individualized progress tracking. The growth of virtual-only K-12 schools is reflected in market data, with the number of full-time virtual school enrollments reaching 298,000 students in the U.S. before the pandemic. This figure is expected to rise further as more districts embrace virtual education. However, success in this endeavor hinges not only on technological infrastructure but also on robust teacher training and instructional design tailored to remote learning environments. As districts continue to refine their virtual education offerings, they are poised to shape the future of K-12 education by embracing innovation and meeting the evolving needs of students in the digital age, thereby aiding the virtual schools market growth.

Virtual Schools Market Dynamics:

Technological Advancements In Education System

The rapid surge in technological advancements within the education system driving the virtual schools market growth. These advancements encompass a wide array of innovations, ranging from sophisticated learning management systems (LMS) to immersive virtual reality (VR) experiences, all aimed at enhancing the delivery of education in digital environments. The integration of artificial intelligence (AI) and machine learning algorithms into educational platforms, enables personalized learning experiences tailored to individual student needs and preferences. Additionally, the advent of cloud computing has revolutionized the accessibility and scalability of educational resources, allowing virtual schools to offer a diverse range of courses and content to students regardless of geographical location.

Technological Advancements in the Education System

| Technology | Description | Impact |

| Virtual Reality (VR) | VR technology immerses students in simulated environments, enhancing learning experiences in subjects like science, history, and art. | Increased student engagement and motivation

Enhanced understanding of complex concepts through experiential learning |

| Artificial Intelligence (AI) | AI-powered adaptive learning platforms personalize instruction based on individual student needs and learning styles. | Customized learning experiences for each student

Real-time feedback and assessment to guide learning progress |

| Online Learning Platforms | Online platforms offer access to a vast array of educational resources, courses, and interactive tools, enabling flexible and self-paced learning. | Expanded access to education, including in remote or underserved areas

Opportunities for lifelong learning and skill development |

| Gamification | Gamification techniques incorporate game elements into educational content, making learning more interactive and enjoyable. | Increased student motivation and participation

Encouragement of problem-solving and critical thinking skills |

| Mobile Learning | Mobile devices enable learning anytime, anywhere, allowing students to access educational materials and collaborate with peers on the go. | Flexibility and convenience in learning

Facilitation of collaborative learning and communication |

| Augmented Reality (AR) | AR overlays digital content onto the physical world, creating interactive learning experiences that blend virtual and real-world elements. | Enhanced visualization and understanding of abstract concepts

Opportunities for hands-on exploration and experimentation |

Such innovations have significantly improved the quality and effectiveness of online education, thereby attracting a broader base of students seeking high-quality learning experiences outside of traditional classroom settings. Thus, the virtual schools market witnessed a significant growth rate in recent years. Features like interactive simulations, real-time feedback mechanisms, and collaborative online tools enhance student engagement and promote deeper learning outcomes. Moreover, the scalability and flexibility afforded by advanced technologies enable virtual schools to accommodate diverse learning styles and preferences, catering to the individualized needs of each student. As a result, virtual schools are better positioned to compete with traditional brick-and-mortar institutions, offering comparable or even superior educational experiences in terms of both academic rigor and student support services. Thus, this factor further boosts the virtual schools market revenue growth.

Furthermore, technological advancements have facilitated the expansion and diversification of virtual schools' offerings, fueling the virtual schools market size. The availability of innovative tools and platforms enables virtual schools to develop specialized programs in niche areas such as STEM education, language learning, and career readiness, thereby attracting students with specific interests or career aspirations. Additionally, advancements in educational technology have facilitated seamless integration with emerging trends such as competency-based learning, project-based assessments, and flipped classroom models, further enhancing the appeal and efficacy of virtual education. This diversification of offerings not only broadens the market reach of virtual schools but also fosters greater inclusivity and accessibility, empowering students from diverse backgrounds to access high-quality education regardless of geographical, socioeconomic, or physical constraints.

Increasing demand for personalized learning

Personalized learning aims to tailor educational experiences to individual students' unique needs, interests, and learning styles, moving away from the traditional one-size-fits-all approach to education. As a result, increasing demand for personalized learning positively impacted the global virtual schools market growth. Virtual schools, with their flexibility and adaptability, are well-positioned to meet this demand by offering customized learning pathways and instructional methods that cater to diverse student requirements. Through advanced learning management systems (LMS), data analytics, and adaptive learning technologies, virtual schools collect and analyze students' performance data in real-time, allowing educators to identify areas of strength and weakness and provide targeted interventions accordingly. Moreover, virtual schools can offer a wide range of courses and electives, enabling students to pursue their interests and passions in depth, regardless of geographical location or scheduling constraints.

Personalized learning enhances student engagement and motivation by empowering learners to take ownership of their educational journey and pursue topics that resonate with their interests and aspirations. By allowing students to work at their own pace and delve deeper into areas of personal interest, personalized learning fosters a sense of autonomy and intrinsic motivation, leading to improved academic outcomes and overall satisfaction with the learning experience. Additionally, personalized learning enables virtual schools to better accommodate diverse learning styles, preferences, and abilities, thereby fostering inclusivity and equity in education. Students with special needs, gifted learners, English language learners, and those who require additional support benefit from tailored instructional strategies and resources designed to meet their individual needs, ensuring that no student is left behind.

Furthermore, the growing demand for personalized learning is driving innovation and competition within the virtual schools market, spurring providers to develop and refine their offerings to better meet the evolving needs of students and educators. Virtual schools are increasingly incorporating adaptive learning technologies, interactive multimedia resources, and personalized learning plans into their curriculum, creating dynamic and responsive learning environments that adapt to each student's progress and proficiency level. This emphasis on personalized learning not only enhances the quality and effectiveness of virtual education but also expands its appeal and accessibility to a wider range of learners. As a result, the virtual schools market is experiencing rapid growth and diversification, with new providers entering the fray and existing ones increasing their offerings to capture a larger share of the burgeoning personalized learning market.

Virtual Schools Market Segment Analysis

Based on Type, in 2024, Private Virtual Schools emerged as the dominant segment by type in the global virtual schools market. These schools have seen strong enrollment growth as families increasingly seek personalized and high-quality online education experiences. Private providers leverage advanced learning management systems, interactive content, and experienced instructors to differentiate from public offerings, enabling them to command premium tuition fees. Their financial independence allows them to invest rapidly in emerging technologies like AI-driven adaptive learning and virtual reality classrooms, enhancing engagement and outcomes. Additionally, they are expanding aggressively across cross-border markets, offering international curricula (IB, Cambridge, etc.) to attract global students. This cross-regional scalability has further widened their reach compared to public and nonprofit players.

Based on Curriculum, STEM / AP / Advanced Learning programs held the largest market share in 2024. The surge in demand stems from a global emphasis on preparing students for high-paying and future-proof careers in technology, engineering, and the sciences. Virtual schools offering advanced placement and STEM-centric courses attract high-performing students seeking competitive academic credentials and university admissions advantages. These programs often partner with tech companies or universities to provide industry-relevant content, hands-on virtual labs, and certifications, making them more appealing to parents and students alike. Moreover, the flexibility of virtual formats aligns well with self-paced learning required for advanced subjects, allowing students to accelerate their studies. This strategic alignment with labor market trends has cemented STEM/Advanced Learning as the leading curriculum segment.

Virtual Schools Market Regional Insights:

The United States dominated the North America virtual schools market with the highest market share of more than 80% in 2023 and is expected to maintain its dominance by 2030. The United States virtual schools market has witnessed significant growth, particularly accelerated by the COVID-19 pandemic. Before the pandemic, virtual schooling was advocated by various entities including vendor corporations, tech industry associations, and venture capitalists. However, the sudden shift to remote learning during the pandemic highlighted both the potential and limitations of virtual education. While digital programs and platforms facilitated connectivity between educators and students, challenges such as cybersecurity threats, technological disparities among students, and the struggle to adapt to virtual learning were prevalent.

Despite these challenges, proponents of virtual education continued to advocate for its widespread adoption, framing it as the future of education even beyond the pandemic. This advocacy has been bolstered by financial incentives and aggressive promotion, particularly targeting full-time virtual schools, also known as virtual charter schools or cyber schools.

The growth of full-time virtual schools has attracted attention due to claims that they offer expanded student choices and improved efficiency in education delivery. Proponents argue that virtual schools tailor curriculum to individual students more effectively than traditional classrooms, potentially leading to greater academic achievement. However, research findings suggest otherwise. Most notably, evidence does not support claims that virtual education produces better student outcomes compared to traditional face-to-face instruction. Full-time virtual schools, in particular, have shown poor outcomes. Moreover, the use of digital platforms poses threats to the integrity of curriculum, student assessments, and data security. Despite these challenges, the virtual schools market in the United States continues to grow rapidly.

The growth of full-time virtual schools has attracted attention due to claims that they offer expanded student choices and improved efficiency in education delivery. Proponents argue that virtual schools tailor curriculum to individual students more effectively than traditional classrooms, potentially leading to greater academic achievement. However, research findings suggest otherwise. Most notably, evidence does not support claims that virtual education produces better student outcomes compared to traditional face-to-face instruction. Full-time virtual schools, in particular, have shown poor outcomes. Moreover, the use of digital platforms poses threats to the integrity of curriculum, student assessments, and data security. Despite these challenges, the virtual schools market in the United States continues to grow rapidly.

The number of students enrolled in virtual schools in the U.S. has been steadily increasing, with 477 full-time virtual schools enrolling 332,379 students in the 2019-20 academic year. Additionally, 306 blended-learning schools enrolled 152,530 students during the same period. For-profit education management organizations (EMOs) dominate the virtual schools market, enrolling significantly more students compared to nonprofit EMOs and independent virtual schools. Despite their large enrollments, virtual schools operated by for-profit EMOs have shown lower performance ratings compared to district-operated and nonprofit EMO-operated schools. Graduation rates in virtual and blended schools fall short of the national average, highlighting persistent challenges in virtual education.

Virtual Schools Market Scope: Inquire before buying

| Global Virtual Schools Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 18.5 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 10.5% | Market Size in 2032: | USD 20.44 Bn. |

| Segments Covered: | by Grade Level | Elementary / Primary Middle School High School Postsecondary |

|

| by Type | Public Schools Private Schools Non-profit Organizations Education Management Organizations (EMOs) |

||

| by Curriculum | General Education STEM / AP / Advanced Learning Remedial / Special Needs / Skill-Development Vocational |

||

| by Learning Model | Fully Virtual Hybrid virtual Supplemental / Part-time Virtual |

||

Virtual Schools Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of MEA)

South America (Brazil, Argentina Rest of South America)

Leading Virtual Schools Market, Key Players:

1. K12 Inc. (Herndon, VA)

2. Connections Academy (Maryland)

3. Mosaica Education (U.S.)

4. Pansophic Learning (Virginia)

5. Florida Virtual School(FLVS) (U.S.)

6. Charter Schools USA (U.S.)

7. Lincoln Learning Solutions (U.S.)

8. Inspire Charter Schools (U.S.)

9. Abbotsford Virtual Schools (Canada)

10. Alaska Virtual Schools

11. Basehor-Linwood Virtual School (U.S.)

12. Acklam Grange (U.K.)

13. Illinois Virtual School (IVS) (U.S.)

14. Virtual High School (VHS) (U.S.)

15. Aurora College (Canada)

16. Wey Education Schools Trust (U.K.)

17. N High School

18. Beijing Changping School (China)

19. Insight PA Cyber Charter School (U.S.)

20. Nevada Virtual Academy (U.S.)

FAQs:

1. Which region has the largest share in the Global Virtual Schools Market?

Ans: The North America region held the highest share in 2024.

2. What is the growth rate of the Global Virtual Schools Market?

Ans: The global market is growing at a CAGR of 10.5% during the forecasting period 2025-2032.

3. What are the growth drivers for the Virtual Schools market?

Ans. increasing adoption of technology in education, demand for flexible learning solutions, accelerated by the COVID-19 pandemic, and recognition of virtual schooling's potential to improve access to quality education are expected to be the major drivers for the Virtual Schools market.

4. What was the Global Virtual Schools Market size in 2024?

Ans: The Global Virtual Schools Market was valued at USD 18.5Bn. In 2024.

5. What are the major restraints for the Virtual Schools market growth?

Ans. limited access to technology and internet infrastructure, coupled with concerns about the quality and effectiveness of virtual learning compared to traditional classrooms, are major restraints for the Virtual Schools market growth.