US Processed Snacks Market Size, by Product Type, Nature, Packaging Type, Distribution Channel and End User

Overview

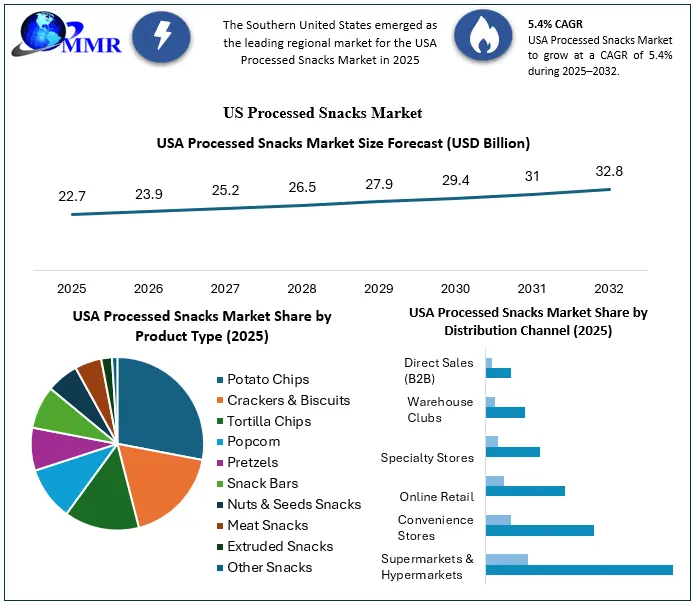

The US Processed Snacks Market was valued at USD 22.7 billion in 2025 and is projected to reach USD 32.8 billion by 2032, expanding at a CAGR of 5.4% during the forecast period (2025–2032). The market is witnessing steady growth due to increasing consumer demand for convenient, ready-to-eat snack products that align with fast-paced lifestyles and evolving dietary preferences. Rising consumption of healthier snack alternatives, including protein-rich, organic, gluten-free, and low-sugar products, is reshaping product innovation across the industry.

According to industry estimates, more than 90% of U.S. consumers purchase snack products at least once a week, while over 55% prefer healthier snack options featuring high protein, fiber, or natural ingredients. Additionally, online grocery and food sales account for over 15% of processed snack purchases, reflecting the growing influence of e-commerce and direct-to-consumer channels. Better-for-you snack categories, including baked chips, protein bars, trail mixes, and plant-based snacks, have recorded annual sales growth exceeding 8%, significantly outpacing conventional snack categories.

The growing popularity of on-the-go snacking, coupled with strong retail penetration through supermarkets, convenience stores, warehouse clubs, and online platforms, continues to support market expansion. Manufacturers are increasingly introducing clean-label products, functional ingredients, and sustainable packaging to meet changing consumer expectations. In addition, advancements in food processing technologies and flavor innovation have enabled companies to diversify their product portfolios and cater to a broad range of age groups and consumption occasions.

The market is also benefiting from increasing investments in premium snack brands, private-label offerings, and direct-to-consumer sales channels. Furthermore, rising health awareness, busy work schedules, and the expansion of online grocery shopping are expected to sustain long-term demand. Functional and fortified snacks now represent approximately one-fourth of new snack product launches in the U.S., while sustainable packaging initiatives have become a strategic priority for leading manufacturers. With continuous product innovation and a strong focus on nutrition, convenience, and sustainability, the US Processed Snacks Market is poised for stable growth throughout the forecast period.

To know about the Research Methodology :- Request Free Sample Report

US Processed Snacks Market Dynamics

Rising Demand for Convenient and Healthier Snacking Options

The increasing preference for convenient, ready-to-eat food products is a major driver of the US Processed Snacks Market. Busy lifestyles, higher workforce participation, and changing eating habits have significantly increased the consumption of on-the-go snacks. At the same time, consumers are shifting toward healthier alternatives, including protein-rich, low-sugar, gluten-free, organic, and plant-based snacks. In 2025, healthy and better-for-you snacks accounted for nearly 38% of the processed snacks market, while protein-based snacks contributed approximately USD 6.5 billion in revenue, reflecting strong demand for nutritious snacking solutions.

Growing Health Concerns and Regulatory Scrutiny

Despite robust market growth, increasing consumer awareness regarding obesity, diabetes, and cardiovascular diseases is limiting demand for traditional processed snacks with high sodium, sugar, and saturated fat content. Regulatory initiatives promoting transparent food labeling and restrictions on artificial additives are encouraging manufacturers to reformulate products, increasing production costs. Additionally, volatility in the prices of raw materials such as wheat, corn, edible oils, cocoa, and dairy ingredients continues to impact manufacturers' profit margins.

Expansion of Premium, Functional, and Plant-Based Snacks

The rapid growth of premium snack categories presents significant opportunities for market participants. Consumers are increasingly seeking snacks enriched with protein, probiotics, dietary fiber, and natural ingredients that support digestive health, immunity, and weight management. The functional snacks segment generated approximately USD 8.2 billion in 2025 and is expected to witness strong growth through 2032. Moreover, expanding e-commerce channels, subscription-based snack services, and innovations in sustainable packaging are creating new revenue opportunities for manufacturers and retailers.

Intense Market Competition and Changing Consumer Preferences

The market remains highly competitive, with established multinational brands, private-label products, and emerging health-focused startups continuously introducing innovative products. Manufacturers face the challenge of balancing product affordability with premium ingredients while adapting quickly to evolving consumer preferences. Maintaining clean-label formulations, ensuring supply chain resilience, and differentiating products through unique flavors, nutritional benefits, and environmentally friendly packaging remain critical challenges for industry participants throughout the forecast period.

US Processed Snacks Market Trends

The US Processed Snacks Market is undergoing a significant transformation as consumers increasingly prioritize health, convenience, and sustainability in their purchasing decisions. One of the most prominent trends is the rising demand for better-for-you snacks, including high-protein, low-sugar, gluten-free, keto-friendly, and plant-based products. In 2025, better-for-you snack products accounted for approximately 38% of the overall market, with demand continuing to rise among millennials and Gen Z consumers seeking healthier alternatives to traditional snacks.

Another notable trend is the growing popularity of functional snacks fortified with ingredients such as protein, probiotics, dietary fiber, omega-3 fatty acids, vitamins, and adaptogens. The functional snacks segment generated approximately USD 8.2 billion in 2025, driven by increasing consumer interest in products that support immunity, digestive health, and overall wellness. Manufacturers are also introducing clean-label formulations free from artificial preservatives, colors, and flavors to meet evolving consumer expectations.

Digital transformation is further reshaping the market, with online sales accounting for over 15% of processed snack purchases in 2025. Subscription snack boxes, direct-to-consumer (DTC) platforms, and personalized snack offerings are gaining traction, while AI-driven demand forecasting and smart packaging technologies are improving inventory management and consumer engagement.

Sustainability has become another defining trend, with leading manufacturers investing in recyclable packaging

US Processed Snacks Market Future Outlook

The US Processed Snacks Market is expected to witness steady growth through 2032, supported by evolving consumer lifestyles, increasing demand for healthier snacking options, and continuous product innovation. The market is projected to grow from USD 22.7 billion in 2025 to USD 32.8 billion by 2032, registering a CAGR of 5.4% during the forecast period. Manufacturers are expected to focus on expanding their portfolios with clean-label, protein-rich, plant-based, and functional snack products to meet rising consumer demand for nutritious and convenient food options.

The integration of advanced food processing technologies, AI-driven demand forecasting, and smart manufacturing practices will improve production efficiency and accelerate new product development. The growing adoption of sustainable packaging, environmentally responsible sourcing, and reduced food waste initiatives is also expected to become a key competitive differentiator. In addition, e-commerce, direct-to-consumer (DTC) platforms, and subscription-based snack services are likely to gain further momentum, enabling companies to strengthen customer engagement and expand their market reach.

Premiumization will remain a significant growth driver as consumers increasingly seek high-quality ingredients, unique flavors, and value-added nutritional benefits. Functional snacks enriched with protein, probiotics, fiber, vitamins, and natural ingredients are anticipated to record above-average growth, while private-label brands are expected to continue expanding their presence through competitive pricing and improved product quality. As health consciousness and demand for convenience continue to rise, the US Processed Snacks Market is well positioned for sustainable long-term growth, creating attractive opportunities for manufacturers, retailers, ingredient suppliers, and investors.

US Processed Snacks Market Competitive Insights

The US Processed Snacks Market is highly competitive, with the presence of established multinational food manufacturers, regional players, and emerging health-focused brands competing through product innovation, premiumization, and strategic retail expansion. Leading companies are continuously investing in research and development to introduce healthier snack alternatives, including high-protein, low-sugar, gluten-free, organic, and plant-based products, in response to changing consumer preferences. In 2025, the top 10 companies accounted for approximately 58–62% of the overall market revenue, reflecting a moderately consolidated competitive landscape.

Major market participants are strengthening their portfolios through mergers and acquisitions, strategic partnerships, and investments in advanced manufacturing technologies. Companies are also expanding their direct-to-consumer (DTC) capabilities and leveraging e-commerce platforms to enhance brand visibility and consumer engagement. Private-label brands offered by leading retail chains continue to gain market share by providing affordable, high-quality alternatives across multiple snack categories.

Product differentiation remains a key competitive strategy, with manufacturers focusing on clean-label formulations, functional ingredients, sustainable packaging, and innovative flavors inspired by global cuisines. Additionally, the adoption of AI-driven demand forecasting, automated production systems, and data-driven consumer analytics is helping companies optimize supply chains and respond more effectively to evolving market trends. As consumer demand for healthier, convenient, and premium snack products continues to increase, market participants are expected to intensify investments in innovation, sustainability, and omnichannel distribution to strengthen their competitive position through 2032.

US Processed Snacks Market Scope: Inquire before buying

| US Processed Snacks Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 22.7 Billion |

| Forecast Period 2026 to 2032 CAGR: | 5.4% | Market Size in 2032: | USD 32.8 Billion |

| Segments Covered: | By Product Type | Potato Chips Tortilla Chips Popcorn Crackers & Biscuits Pretzels Nuts & Seeds Snacks Meat Snacks Snack Bars Extruded Snacks Other Processed Snacks |

|

| By Nature | Conventional Organic Clean Label Gluten-Free Plant-Based |

||

| By Packaging Type | Flexible Pouches Bags Boxes & Cartons Cans Jars Sustainable Packaging |

||

| By Distribution Channel | Supermarkets & Hypermarkets Convenience Stores Specialty Stores Online Retail Warehouse Clubs Direct Sales (B2B) |

||

| By End User | Household Consumers Hotels & Restaurants Cafés & Bakeries Foodservice Industry Institutional Buyers Corporate Offices & Workplaces |

||

US Processed Snacks Market Key Players

| Sr. No. | Company | Region (USA) | Core Competencies |

| 1 | PepsiCo, Inc. | New York | Potato chips, tortilla chips, extruded snacks, product innovation |

| 2 | Kellanova | Illinois | Crackers, snack bars, savory snacks, brand portfolio |

| 3 | Mondelez International | Illinois | Biscuits, cookies, premium snacking, global distribution |

| 4 | The Hershey Company | Pennsylvania | Chocolate snacks, confectionery, protein snacks |

| 5 | General Mills, Inc. | Minnesota | Snack bars, cereals, healthy snacks, natural ingredients |

| 6 | Campbell's Company (Snyder's-Lance) | New Jersey | Pretzels, kettle chips, sandwich crackers |

| 7 | Conagra Brands, Inc. | Illinois | Frozen snacks, popcorn, packaged convenience foods |

| 8 | Hormel Foods Corporation | Minnesota | Meat snacks, protein-based snacks, value-added foods |

| 9 | Utz Brands, Inc. | Pennsylvania | Salty snacks, potato chips, pretzels |

| 10 | Jack Link's Protein Snacks | Wisconsin | Beef jerky, meat snacks, protein nutrition |

| 11 | Kind LLC | New York | Nut bars, healthy snacking, clean-label products |

| 12 | The J.M. Smucker Company | Ohio | Peanut butter snacks, fruit snacks, packaged foods |

| 13 | Blue Diamond Growers | California | Almond-based snacks, flavored nuts |

| 14 | Wonderful Pistachios & Almonds | California | Premium nuts, healthy snack products |

| 15 | Popchips Inc. | California | Better-for-you popped chips, low-fat snacks |

| 16 | LesserEvil LLC | Connecticut | Organic popcorn, clean-label snacks |

| 17 | SkinnyPop (Amplify Snack Brands) | Texas | Ready-to-eat popcorn, healthy snacking |

| 18 | Biena Snacks | Massachusetts | Roasted chickpea snacks, plant-based protein |

| 19 | Siete Foods | Texas | Grain-free chips, Mexican-inspired snacks |

| 20 | HIPPEAS | California | Organic chickpea puffs, sustainable snacks |

| 21 | Nature's Bakery | Nevada | Fig bars, whole grain bakery snacks |

| 22 | Clif Bar & Company | California | Energy bars, sports nutrition snacks |

| 23 | Quest Nutrition | California | High-protein snacks, keto-friendly products |

| 24 | RXBAR (Kellanova) | Illinois | Protein bars, clean-label ingredients |

| 25 | Dot's Pretzels | North Dakota | Gourmet pretzels, premium salty snacks |

| 26 | Pirate's Booty | New York | Baked cheese puffs, children's snacks |

| 27 | Herr Foods Inc. | Pennsylvania | Potato chips, popcorn, regional snack manufacturing |

| 28 | Wise Foods Inc. | New Jersey | Potato chips, popcorn, tortilla chips |

| 29 | Old Dutch Foods USA | Minnesota | Potato chips, popcorn, regional snack distribution |

| 30 | Boulder Canyon (Inventure Foods) | Arizona | Kettle chips, avocado oil chips, premium natural snacks |

Frequently Asked Questions

Q1. What is the current size of the US Processed Snacks Market?

The US Processed Snacks Market was valued at USD 22.7 billion in 2025 and is projected to reach USD 32.8 billion by 2032.

Q2. What is the expected CAGR of the US Processed Snacks Market during the forecast period?

The market is expected to grow at a CAGR of 5.4% from 2025 to 2032, driven by rising demand for convenient and healthier snack products.

Q3. What are the key factors driving the growth of the US Processed Snacks Market?

Key growth drivers include increasing demand for on-the-go snacks, growing consumer preference for healthier and functional snack options, expanding e-commerce channels, product innovation, and rising investments in premium snack offerings.

Q4. Which product categories are witnessing the fastest growth in the US Processed Snacks Market?

Healthy and functional snacks, including high-protein snacks, plant-based snacks, gluten-free products, organic snacks, protein bars, baked snacks, and low-sugar snack products, are experiencing the fastest growth.

Q5. Who are the major players operating in the US Processed Snacks Market?

Leading companies include PepsiCo, Inc., The Kraft Heinz Company, Kellogg Company (Kellanova), General Mills, Inc., Mondelez International, Campbell Soup Company (Snyder's-Lance), Conagra Brands, Hormel Foods Corporation, The Hershey Company, and Utz Brands, Inc.