Synthetic Rubber Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

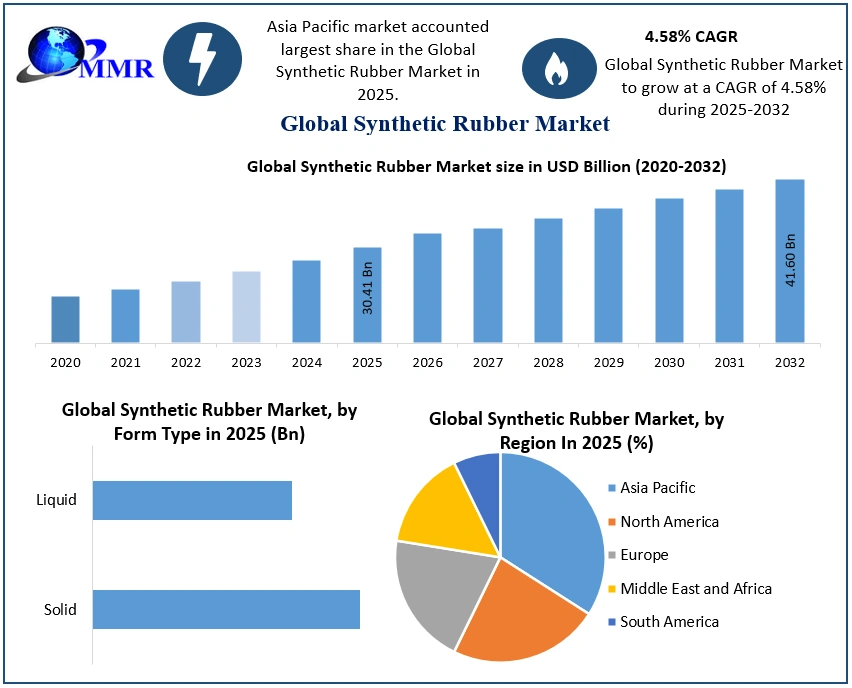

The Synthetic Rubber Market size was valued at USD 30.41 Billion in 2025 and the total Synthetic Rubber revenue is expected to grow at a CAGR of 4.58% from 2026 to 2032, reaching nearly USD 41.60 Billion by 2032.

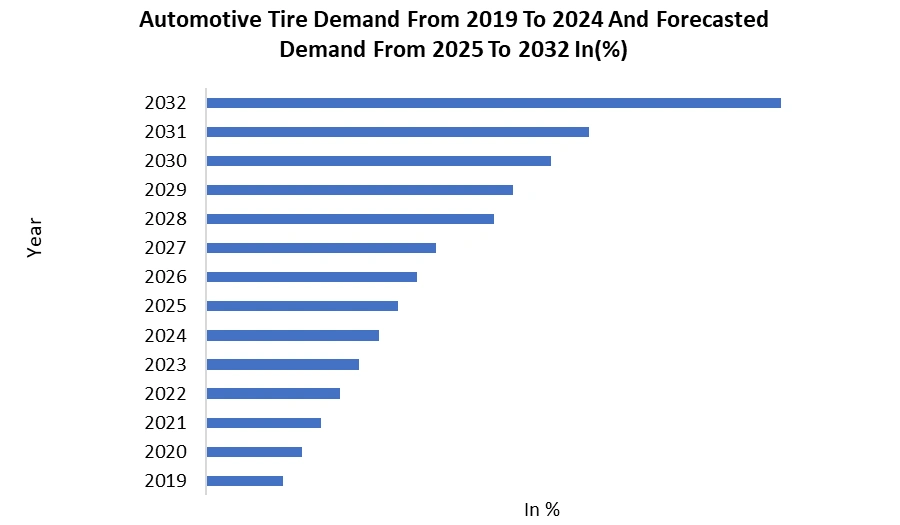

The global demand for synthetic rubber is witnessing significant growth as industries increasingly rely on high-performance elastomers for automotive, tire manufacturing, construction, and industrial applications. Key materials such as SBR, BR, NBR, EPDM, and IIR are widely used in tires, hoses, gaskets, seals, conveyor belts, and various industrial components. In 2025, global tire production surged, with countries such as China, India, and Japan leading the consumption China alone accounted for over 6 million tons of synthetic rubber, making it the largest global consumer.

Innovation is reshaping the synthetic rubber market, with companies like Bridgestone, Goodyear, and Michelin introducing eco-friendly tires using bio-based rubber, recycled carbon black, and sustainable elastomers. Goodyear, for instance, launched a tire composed of 70% sustainable materials, including soybean oil–based rubber. China’s petrochemical capacity projects, India’s Production-Linked Incentive (PLI) program for automotive components, and Japan’s green mobility initiatives are strengthening synthetic rubber production and R&D. Growing EV adoption and demand for heat-resistant, durable elastomers continue to drive robust Synthetic Rubber Market growth globally.

To know about the Research Methodology :- Request Free Sample Report

Synthetic Rubber Market Dynamics:

Rising Automotive Tire Demand and Advanced Mobility Trends to drive the Growth of Synthetic Rubber Market

The synthetic rubber market is primarily driven by the strong global demand for automotive tires, supported by rising vehicle production and the expansion of electric mobility. Synthetic rubber types such as SBR, BR, and NBR are essential for producing high-performance tires due to their abrasion resistance, flexibility, and durability. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached around 93.5 million units in 2023, reflecting steady recovery in automotive manufacturing. Tire manufacturers like Bridgestone, Michelin, and Goodyear are scaling production to meet increasing replacement and OEM tire demand. Additionally, the EV sector is accelerating market growth, as electric vehicles require low-rolling-resistance tires to improve battery efficiency. For instance, EV sales crossed 14 million units in 2023, with China contributing nearly 60% of global EV demand, directly boosting demand for advanced synthetic rubber formulations. Growth in commercial vehicle fleets for logistics, especially in India, China, and Brazil, further strengthens consumption. This sustained automotive momentum, combined with performance-driven tire innovations, continues to fuel consistent demand for synthetic rubber worldwide.

Volatile Raw Material Prices and Environmental Concerns Limits the synthetic rubber market Growth

One of the major restraints impacting the synthetic rubber market is the high volatility in raw material pricing, particularly butadiene, styrene, and other petrochemical feedstocks derived from crude oil. Fluctuations in oil prices create instability in production costs, limiting profitability for manufacturers. For instance, butadiene prices surged over 30% in 2023 due to refinery shutdowns in Europe and supply disruptions in Asia, affecting companies like Sinopec, LG Chem, and Arlanxeo. Environmental regulations also pose challenges, as synthetic rubber production generates emissions and waste that must comply with stricter government standards. The EU’s Green Deal and China’s updated emission norms (2024 revision) require manufacturers to invest heavily in cleaner technologies. Additionally, concerns about microplastic release from tire wear estimated at 1 million tonnes annually worldwide are increasing regulatory pressure on rubber producers. These sustainability issues are prompting industries to shift toward eco-friendly alternatives, thereby slowing adoption in some regions. High energy costs, feedstock shortages, and regulatory compliance expenses continue to restrain growth, especially for small and mid-sized rubber processing units.

Expansion of Bio-Based Synthetic Rubber and Sustainable Tire Solutions creates lucrative growth opportunities to the market growth

Sustainability-driven innovations are creating significant opportunities for the synthetic rubber market, particularly in bio-based materials, recycled rubber, and low-emission manufacturing technologies. Global tire companies are aggressively investing in renewable rubber materials to meet their 2030–2050 sustainability goals. For example, Michelin and Bridgestone are developing bio-SBR and bio-butadiene using plant-based feedstocks. Michelin announced that it aims to produce tires made of 100% sustainable materials by 2050, and in 2023, it successfully tested tires containing 45% recycled and renewable materials. Similarly, Goodyear introduced a tire made with 70% sustainable materials in 2023, including soybean oil-based rubber and recycled plastics. Governments are also supporting sustainable rubber initiatives—Japan and the EU invested over USD 150 million combined in synthetic rubber decarbonization programs in 2024. Growth in green construction materials, medical elastomers, and high-performance seals further adds opportunities for EPDM, NBR, and other advanced polymers. As industries aim to reduce carbon footprints, demand for bio-based and circular-economy-aligned rubber solutions is expected to expand rapidly, opening new revenue channels for manufacturers globally.

Synthetic Rubber Market Segment Analysis:

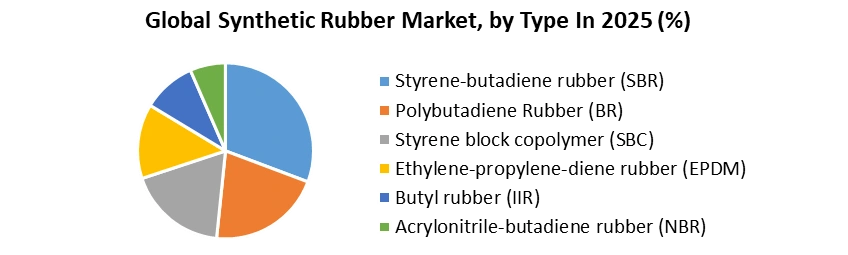

Based on Type, the Synthetic Rubber Market is segmented into Synthetic Rubber Market, Polybutadiene Rubber (BR), Styrene block copolymer (SBC), Ethylene-propylene-diene rubber (EPDM), Butyl rubber (IIR), and Acrylonitrile-butadiene rubber (NBR). Styrene-Butadiene Rubber (SBR) dominated the Synthetic Rubber Market in year 2025.Due to its extensive use in automotive tires, strong performance characteristics, and cost-effectiveness. SBR is the preferred material for tire treads because it offers excellent abrasion resistance, durability, and heat stability qualities essential for passenger cars, commercial vehicles, and electric vehicles. With global tire production rising sharply across China, India, Japan, and South Korea, SBR demand continued to outpace other segments such as Polybutadiene Rubber (BR), Styrene Block Copolymer (SBC), EPDM, Butyl Rubber (IIR), and Acrylonitrile-Butadiene Rubber (NBR).

SBR holds the largest share as nearly 50–60% of total synthetic rubber consumption in automotive applications comes from this material. Leading tire manufacturers like Michelin, Bridgestone, Goodyear, and Apollo Tires rely heavily on SBR to produce high-performance and low-rolling-resistance tires. The rapid shift toward EVs further boosts synthetic rubber market demand, making SBR the dominant segment due to its balanced cost, performance, and availability in major production hubs across the Asia-Pacific region.

Synthetic Rubber Market Regional Analysis:

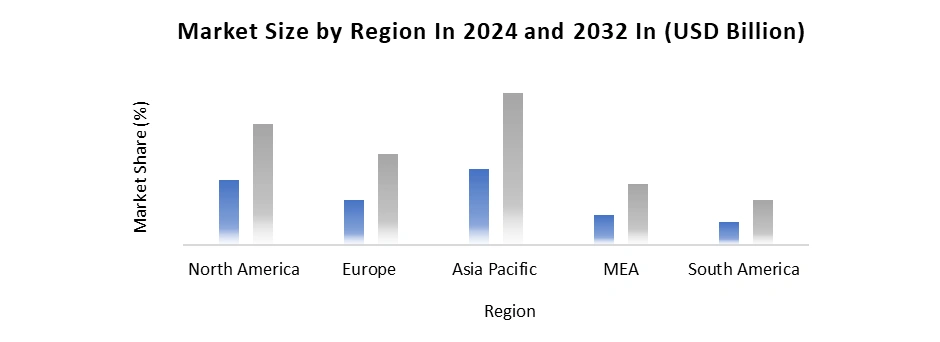

Asia Pacific Dominated the Synthetic Rubber Market in year 2025. Due to its strong manufacturing ecosystem, high automotive production, and expanding tire industry, all of which significantly boosted synthetic rubber demand, especially for SBR, BR, NBR, and EPDM grades. China remained the largest contributor, driven by massive automotive output and tire manufacturing hubs supplying both domestic and export markets. Japan and South Korea also played a key role with advanced synthetic rubber production capabilities, producing high-quality EPDM and specialty elastomers used in automotive seals, industrial belts, and electronics.

India recorded rapid growth, as rising vehicle sales and infrastructure expansion increased demand for industrial rubber and automotive tires. Southeast Asian countries like Thailand, Indonesia, and Vietnam strengthened their presence through growing import volumes and expanding rubber-processing industries. Major manufacturers such as Sinopec, LG Chem, Arlanxeo, and Kumho Petrochemical continued capacity expansion across Asia, attracting tire companies such as bridgestone, Goodyear, and Michelin. Strong industrialization, cost-effective production, and growing EV adoption collectively positioned Asia-Pacific as the global leader in the synthetic rubber industry.

Synthetic Rubber Market Competitive Landscape:

The Synthetic Rubber Market is highly competitive, driven by global synthetic rubber manufacturers, integrated petrochemical companies, and leading tire producers expanding their SBR, BR, NBR, and EPDM portfolios. Key players such as Sinopec, Arlanxeo, Lanxess, Kumho Petrochemical, JSR Corporation, LG Chem, Synthos, Reliance Industries, Shell, and ExxonMobil focus on strengthening production of styrene-butadiene rubber, butadiene rubber, and industrial rubber used across automotive, construction, and manufacturing sectors. Companies are investing heavily in sustainable synthetic rubber, bio-based rubber, and recycled rubber solutions to meet rising demand for EV tire materials, low-rolling-resistance tires, and eco-friendly elastomers.

Global tire leaders including Bridgestone, Goodyear, and Michelin are partnering with chemical companies to develop advanced synthetic rubber for automotive tires, enhancing durability, heat resistance, and performance for electric and hybrid vehicles. Several producers are expanding capacity in Asia-Pacific due to strong synthetic rubber market demand from China, India, and Southeast Asia. Strategic moves include acquisitions, capacity expansions, long-term supply contracts, and innovations in synthetic rubber production, helping companies strengthen market share in this highly evolving synthetic rubber industry.

Synthetic Rubber Market: Recent Development

1. In June 2023: Apcotex Industries Limited invested USD 24.13 million to expand two of its rubber manufacturing projects. This strategic investment aims to strengthen the company’s production capabilities and increase revenue from its synthetic rubber segment.

2. In April 2023: Sinopec announced an expansion of its styrene-butadiene (SBC) production capacity by 170,000 tons per year at its facilities in Hainan, China. This move is intended to enhance Sinopec’s market presence and support the growing synthetic rubber demand within China.

Synthetic Rubber Market Scope: Inquiry Before Buying

| Synthetic Rubber Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 30.41 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.58% | Market Size in 2032: | USD 41.60 Bn. |

| Segments Covered: | by Type | Styrene-butadiene rubber (SBR) Polybutadiene Rubber (BR) Styrene block copolymer (SBC) Ethylene-propylene-diene rubber (EPDM) Butyl rubber (IIR) Acrylonitrile-butadiene rubber (NBR) |

|

| by Form Type | Solid Liquid |

||

| by Application | Tire Automotive Footwear Industrial Goods Consumer Goods Textile Others |

||

| by End User | Transportation Building & Construction Medical Textile & Apparel Food & Beverage Other |

||

Synthetic Rubber Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Synthetic Rubber Key Players

1. Sinopec

2. Arlanxeo

3. Kumho Petrochemical

4. JSR Corporation

5. LG Chem

6. Lanxess AG

7. ExxonMobil Chemical

8. Shell Chemicals

9. Synthos S.A.

10. Reliance Industries Limited (RIL)

11. Bridgestone Corporation

12. Michelin Group

13. Goodyear Tire & Rubber Company

14. Indian Oil Corporation Limited (IOCL)

15. Apcotex Industries Limited

16. Versalis (ENI Group)

17. Sibur (Russia)

18. Zeon Corporation

19. Nizhnekamskneftekhim (NKNK)

20. Trinseo

21. Kraton Corporation

22. TSRC Corporation (Taiwan Synthetic Rubber Corp.)

23. Lion Elastomers

24. Korea Kumho Petrochemical Company (KKPC)

25. Formosa Petrochemical Corporation

26. PetroChina Company Limited

27. Hainan Rubber Group

28. Shanxi Synthetic Rubber Group

29. Yokohama Rubber Company

30. Huntsman Corporation

Frequently Asked Questions:

1. Which region has the largest share in Global Synthetic Rubber Market?

Ans: Asia Pacific region held the highest share in 2025.

2. What is the growth rate of Global Synthetic Rubber Market?

Ans: The Global Synthetic Rubber Market is growing at a CAGR of 4.58 % during forecasting period 2026-2032.

3. What is scope of the Global market report?

Ans: Global market report helps with the PESTEL, PORTER, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global market?

Ans: The important key players in the Global Synthetic Rubber Market are Sinopec, Arlanxeo, Kumho Petrochemical, JSR Corporation, LG Chem and Others

5. What was the Global Synthetic Rubber Market size in 2025?

Ans: The Global Synthetic Rubber Market size was USD 30.41 Billion in 2025.