Super Apps Market Scope Market Size by Service Type, Business Model Type, User Base, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

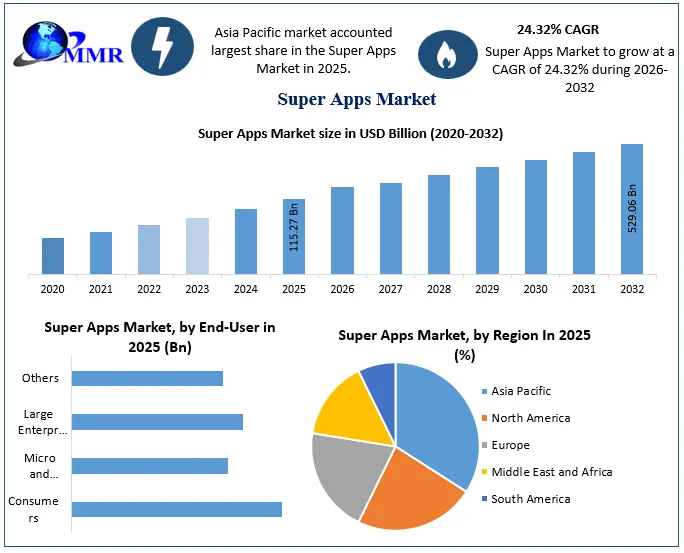

The Super Apps Market size was valued at USD 115.27 Bn. in 2025, and the total Super Apps revenue is expected to grow at a CAGR of 24.32% from 2026 to 2032, reaching nearly USD 529.06 Bn.

Super Apps Market Overview

A super app is a mobile or web application that combines multiple services, such as payments, banking, e-commerce, and ride-hailing, into a single platform, offering an all-in-one experience.

The e-commerce boom, with 72% of sales made via mobile ($4.5T), and shifting consumer preferences, 68% of whom prefer all-in-one platforms for convenience, drive the Super Apps Market. However, technological limitations in mid/low-end smartphones (e.g., 62% with <4GB RAM) restrain the Market growth. Opportunities lie in embedded finance (65% of users prefer in-app payments) and urbanization-driven demand. While high development costs challenge scalability. While Asia-Pacific leads adoption (1.8 B+ digital payment users), with giants like WeChat ($80B revenue) and Alipay. North America grows steadily, fueled by tech-savvy users and expanding ecosystems like Uber.

Super Apps Market Recent Development

| Company | Date (2024) | Region | Country | Recent Development |

| Revolut | June 20 | Europe | UK | Added Revolut Stays, offering hotel bookings & rewards within its finance super app, marking a recent development in the super app market. |

| Gojek (Go To) | June 18 | Southeast Asia | Indonesia | Partnered with Samsung Pay to enable seamless Go Pay transactions on Samsung devices, marking a recent development in the super app market. |

| WeChat (Tencent) | June 12 | East Asia | China | Launched AI-powered shopping assistants within mini-programs & expanded cross-border payments to 10 new super apps, reflecting ongoing innovation by super app suppliers. |

| Grab | June 5 | Southeast Asia | Singapore | Introduced the Grab Ultimate subscription plan, bundling ride-hailing, food delivery, and fintech discounts, showcasing strategic expansion by a leading super app manufacturer. |

To know about the Research Methodology :- Request Free Sample Report

Super Apps Market Dynamics

Growing E-Commerce Sector to Boost Super Apps Market Growth

Mobile-aided shopping has driven rapid growth in the e-commerce market in recent years. Smartphones allow users to browse and select products easily. As m-commerce apps become more popular, the super apps market is expected to grow significantly.

E-Commerce Growth Fueling Super Apps Market

| Driver | Global Impact (2024) |

| Mobile Shopping Boom | 72% of e-commerce sales via mobile ($4.5 trillion) |

| Social Commerce Surge | $1.2 trillion GMV from super app social features |

| Embedded Payments | 65% of super app users pay via in-app wallets |

| Ultrafast Delivery Demand | 55% of users expect delivery in <2 hours (e-grocery) |

| BNPL Adoption | 30% of super app transactions use buy-now-pay-later |

| Cross-Border Shopping | 40% growth in international purchases via super apps |

Inadequate Technological Advancements in Smartphones to Create the market Restraints

Smartphone manufacturers find it hard to keep up with mobile app developers. Many apps need advanced device features, which limits market growth. To solve this, consumers need to switch to more advanced devices that can run these apps smoothly.

Global Smartphone Limitations Impacting the Super Apps Market

| Constraint | High-End Devices | Mid/Low-End Devices | Impact on Super Apps |

| Devices with <4GB RAM | 5% | 62% | 40% higher crash rates |

| 4G-Only Devices | 8% | 82% | 5 G-only features (e.g., AR shopping) fail |

| Storage <64GB | 3% | 58% | 25% uninstall rate due to app bloat |

| No AI Chipset (NPU) | 12% | 85% | AI-driven recommendations lag |

| Battery <4000mAh | 18% | 67% | 30% of users abandon apps due to drain |

Changing Lifestyle and Consumer Preferences to Create Super Apps Market Opportunity

Changing lifestyles and digital-first habits are boosting super app use, as 68% of users now prefer all-in-one platforms. Busy urban lives increase demand, with 55% of millennials using super apps for daily tasks and 42% valuing time-saving features. Buy Now, Pay Later use in super apps grew 90% year-over-year. Companies tapping into these trends see 30% more user engagement than single-service apps.

High Cost of Super App Development to Create Super Apps Market Challenges

Besides facilitating user activities with technological support, super apps require a high investment for their development. As smartphone super apps gain popularity, so does the demand for associated services, such as administration, maintenance, and infrastructure. All these factors are creating challenges in market growth.

Super Apps Market Segment Analysis

Based on Service Type, the Super Apps Market is segmented into Payments & Financial Services, Commerce & Retail, Mobility & Logistics, Social & Communication, and Utilities & Lifestyle. The Payments & Financial Services segment dominated the Super Apps Market in 2025 and is expected to hold the largest market share over the forecast period. Due to holding over 45% of revenue share, driven by digital payment adoption and embedded finance. With 3.8 B+ global digital wallet users, super apps like Alipay and Paytm lead by integrating payments and insurance, boosting user retention. Mobile wallet transactions hit $14T in 2024, while 65% of super app users prefer in-app financial services. This dominance stems from high-frequency usage, regulatory push for cashless economies, and cross-selling fintech products.

Based on the Business Model, the Super Apps Market is segmented into Transaction Fees, Subscription Services, Advertising, and Commission-Based. The Transaction Fees segment dominated the Super Apps Market in 2025 and is expected to hold the largest market share over the forecast period. Due to driven by digital payments and embedded finance. Government cashless policies (e.g., India’s UPI) boosted adoption, while BNPL grew 90% YoY. Subscriptions (15% share) and ads (12%) lagged due to low emerging-market uptake and ad fatigue. Commission-based models (8%) faced margin pressures. The dominance stems from high-frequency micropayments, though diversification into subscriptions and ads is rising for future growth. Based on End User, the market is segmented into Consumers (B2C) and Businesses (B2B). The consumers (B2C) segment dominated the Super Apps Market in 2025 and is expected to hold the largest market share over the forecast period. Due to the mass adoption of digital payments, shopping, and lifestyle services. Over 4.1B consumers used super apps for daily transactions (Statista), compared to only 22% B2B penetration (GSMA). Governments accelerated this via cashless initiatives (e.g., India’s UPI, Brazil’s Pix), while B2B growth lagged due to slower SME onboarding.

Based on End User, the market is segmented into Consumers (B2C) and Businesses (B2B). The consumers (B2C) segment dominated the Super Apps Market in 2025 and is expected to hold the largest market share over the forecast period. Due to the mass adoption of digital payments, shopping, and lifestyle services. Over 4.1B consumers used super apps for daily transactions (Statista), compared to only 22% B2B penetration (GSMA). Governments accelerated this via cashless initiatives (e.g., India’s UPI, Brazil’s Pix), while B2B growth lagged due to slower SME onboarding.

Super Apps Market Regional Analysis

Asia-Pacific Region Dominated the Global Super Apps Market in 2025

The Asia Pacific region dominates the global market and is poised for significant growth, driven by platforms like WeChat, Alipay, and Grab, which offer a wide range of services such as social networking and digital payments. Innovations are emerging, such as Indian Railways' super app, which consolidates multiple railway services, enhancing customer convenience and generating revenue. Collaborations among key players further stimulate market expansion, exemplified by Tencent Cloud's partnership with TribunNews to enhance the TribunX Super App in Indonesia.

Asia-Pacific (APAC) Dominates Global Super Apps Market in 2024 – Key Statistics & Growth Drivers

| Factor | APAC Data | Global Comparison | Key Insight |

| Mobile Penetration | 95% smartphone adoption | Global avg: 78% | High accessibility to super apps |

| Digital Payment Users | 1.8 B+ (75% of global users) | LatAm: 380M, Africa: 330M | UPI (India), Alipay/WeChat Pay (China) drive adoption |

| Super App Adoption Rate | 68% of internet users | North America: 32% | Cultural preference for all-in-one apps |

| E-Commerce GMV via Super Apps | $2.8T (70% of global) | Europe: $420B | Integrated shopping, payments, and logistics |

| Government Support | UPI (India), Digital Yuan (China) | Fragmented policies in the West | National digital infrastructure boosts growth |

| Fintech Integration | 80% of super apps offer loans | LatAm: 55%, Africa: 40% | Embedded lending/insurance increases retention |

North America Is the Growing Region

North America is witnessing steady growth, with companies like Uber expanding their service ecosystems. Despite slower adoption compared to Asia, the region's tech-savvy consumers and high smartphone usage present opportunities for super app development, although regulatory and cultural factors will influence market dynamics. Overall, both regions are experiencing unique trajectories in the market, highlighting diverse opportunities and challenges.

Super Apps Market Competitive Landscape

The global super app landscape is dominated by WeChat (Tencent) and Alipay (Ant Group), both headquartered in China. WeChat, with over $80 billion annual revenue, integrates messaging, payments, e-commerce, and mini-programs, serving 1.3 billion users. Alipay, generating $20+ billion yearly, leads in digital payments, lending, and lifestyle services with 1.2 billion users. While WeChat excels in social-commerce synergy, Alipay dominates financial services. Both face regional rivals like Grab (Southeast Asia) and Mercado Pago (South America), but their scale and ecosystem integration keep them unmatched in revenue and market penetration.

Super Apps Market Scope: Inquire before buying

| Super Apps Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 115.27 USD Billion |

| Forecast Period 2026-2032 CAGR: | 24.32% | Market Size in 2032: | 529.06 USD Billion |

| Segments Covered: | by Platform Type | Android IOS Others |

|

| by Deployment Type | Cloud On-Premise |

||

| by Device Type | Smartphones Tablets Others |

||

| by Application | Digital Payments Mobile Banking Lending and Credit Services Insurance Services Investment Services Others |

||

| by End-User | Consumers Micro and Small Businesses, Large Enterprises Others |

||

Super Apps Market by Regions

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam,

Philippines, Thailand, and the Rest of Asia Pacific)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Super Apps Market by Key Companies are:

1. ALIPAY

2. PAYTM

3. PhonePe

0. Revolut

5. Opay

6. Rappi

7. Careem

8. Gojek

9. Orami

10.Kakao Corp.

11.M‑Pesa (Safaricom / Vodacom)

12.ShopeePay

13.Sea Group

14.Maya

15.AirAsia Super App

16.Tata Neu

17.SBI Yono

18.Flipkart

19.Navi

20.Uber

21.Google Pay

22.Samsung Wallet / Samsung Pay

23.Mercado Pago

24.Kaspi.kz

25.UnionPay App

26.WeChat (Tencent)

27.Grab

28.GCash

Frequently Asked Questions

Q1. What was the Market Size of Super Apps Market in 2025?

Ans. The global super apps market size was estimated at USD 115.27 billion in 2025.

Q2. What is the Rate of super apps market growth?

Ans. The super apps market is projected to grow at a compound annual growth rate of 24.32% from 2026 to 2032.

Q3. Which region accounts for the largest super apps market share?

Ans. On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East, and Africa, where Asia Pacific currently dominates the global market.

Q4. Which are the leading Key Players in the global super apps market?

Ans. Some of the major players in the global Super Apps market include Alipay (Alibaba Group Holding Limited), Gojek Tech (Go to), Grab, Kakao Corp.