Processed Animal Protein Market Size by Source, Form and Region - Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

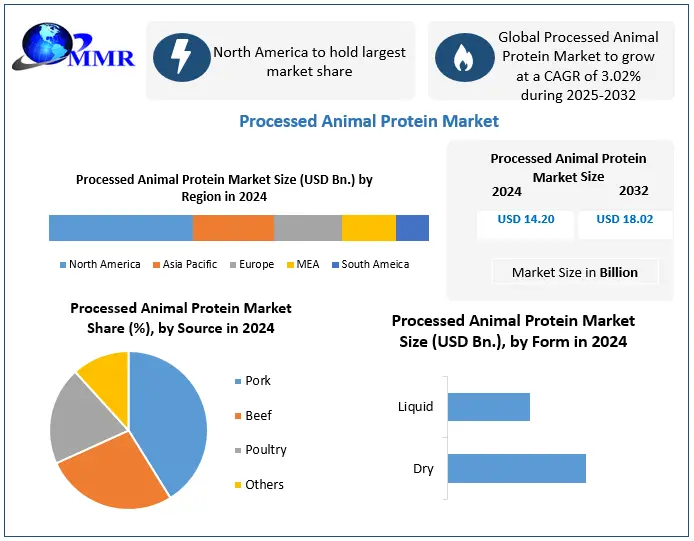

The Global Processed Animal Protein Market was valued at approximately USD 14.2 billion in 2024. It is projected to reach USD 18.02 billion by 2032, exhibiting a CAGR of 3.02% during the forecast period 2025-2032

Processed Animal Protein Market Overview

Processed Animal Protein (PAP) refers to protein-rich products derived from animal by-products, such as meat meal, bone meal, and feather meal, primarily used in animal feed. These products are obtained through rendering processes, ensuring nutritional value and safety for livestock, aquaculture, and pet food applications.

The Processed Animal Protein Market is growing due to its high protein content and cost-effectiveness in feed formulations. Demand is particularly strong in the livestock and aquaculture sectors, where protein-rich feed is essential for growth and productivity. Supply is closely tied to the meat industry by-products, with regulatory frameworks ensuring quality and preventing risks like disease transmission.

North America is a key player in the PAP market, supported by a well-established meat industry and high demand for animal feed. The U.S. and Canada are dominated by their large-scale livestock production and advanced rendering technologies. Regulatory frameworks, like FDA and CFIA guidelines, ensure high-quality standards, boosting market growth. Also, increasing aquaculture activities and pet food demand further drive PAP consumption in the region.

Major players in the industry include Tyson Foods, and Sonac BV invests in sustainable production and expanding into high-growth regions. End-use sectors, poultry, swine, aquaculture, and pet food are primary contributors to PAP demand by their need for high-quality, protein-rich feed solutions.

The report also helps in understanding the Global Processed Animal Protein Market dynamics, structure by analyzing the market segments and projecting the Global market. Clear representation of competitive analysis of key players by Application, price, financial position, Product portfolio, growth strategies, and regional presence in the Global Processed Animal Protein Market makes the report an investor’s guide. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Processed Animal Protein Market Dynamics

Growing animal waste and increased meat consumption are the two factors driving the growth of the Processed Animal Protein Market. The amount of meat consumption has risen considerably in recent years. The rise in processed meat consumption has resulted in an increase in animal waste creation, which needs efficient treatment. However, getting rid of waste products from animals is a costly procedure that requires manpower, raw materials, logistics, and available land. Additionally, there are various environmental concerns linked with the disposal of such trash owing as it may contaminate nearby air, water, or ground.

The cost associated with the disposal of animal waste increased, owing to the stringent regulatory measures adopted by different regions. To decrease the wastage of such animal waste, the rendering process helps and divides them into valuable products such as feather meal, blood meal, bone meal, and fat, among others. Animal feed manufacturers and pet products manufacturing industries use rendered protein meals and fat products. Owing to these increased generations of animal waste and a rise in meat consumption are boosting the growth of the processed animal protein market.

Market Growth Restraints

The processed Animal Protein Market is hampered by stringent regulatory measures. To ensure the superior quality of dry and wet animals, the government across various regions has set up stringent rules. To develop products that adhere to the regulatory bodies’ rules and help them receive the necessary certification required for marketing the products, the strict government rules prompt companies. For example, all feed items for farm animals must be certified by the FDA under the Federal Food, Drug, and Cosmetic Act, passed by the United States Food and Drug Administration (FDA).

Similarly, the government has just legalized the use of processed animal proteins in European markets. Processed animal proteins are still restricted in cattle and sheep under the new rule, but they are fed to non-ruminants like pigs and poultry. Such stringent regulatory standards are likely to have an impact on the growth of the processed animal protein market. Among the buyers of pet food products, the demand for pet food products with processed animal protein increased.

Market Growth Opportunities

Increased adoption of pets is expanding the processed animal protein market. The rapid spread of the COVID-19 pandemic forced the government to impose a lockdown in several countries across the world. During the pandemic, the adoption of pets rose considerably, resulting in the demand for nutritious pet food products, especially in Europe and the U.S.

To develop pet food products rich in flavor and nutrition, the use of updated technology in the meat processing companies is enabling. It also offers an environmentally friendly option to the environmentally aware consumer, as it has a lower carbon footprint than plant-based feed products, which have caused deforestation in many countries. To promote the health of pets, companies are creating new product formulations such as spray-dried plasma powder (SDP) and hemoglobin powder with specific functional qualities.

As a result, the participants in the processed animal protein market are concentrating on developing and selling new product formulations rich in amino acids and other critical elements for body growth. Manufacturing businesses used acquisition and merger tactics to expand their production capacity and develop new goods.

Processed Animal Protein Market Segment Analysis

Based on the Source, the poultry products segment held the largest market share of 31.9 % in 2024. The demand for poultry-based feed products has increased rapidly in recent years. The growth that is in demand can be credited to the processed animal protein market’s increasing demand for egg and poultry meat products. Chicken-based feed products, which are consumed by the consumer, do not cause any disease; cattle-based products cause disease with the outbreak of Bovine Spongiform Encephalopathy (BSE). Owing to these for feeding farm animals most countries allow the use of poultry-based processed animal protein.

Based on the Application, the Dry segment held the largest market share of 34.3 % in 2024. In the processed animal protein market, animal feed products such as feathers and blood, and meals are primarily available in pellets and powder feed. Dry forms are preferred by animal owners, as they are easily dissolved in water and mixed with other products. Liquid processed animal protein is challenging to transport and store compared to the feed products available in granular or solid form.

Processed Animal Protein Market Regional Analysis

The North America region dominated the market with a 40 % share in 2024. In North America, the US is the largest market. Owing to these, animal by-products are processed into feather meals, blood meals, and other parallel products to reduce the ecological impact of animal waste. These animal protein products also help to produce supplements that have applications in the feed industry. Moreover, with the growth in the demand among pet owners for nutritious products and pet food products to maintain pet health, the demand for processed animal protein in the American pet products industry is growing rapidly.

Owing to the considerable livestock production in the region, the Asia Pacific is one of the key markets. China, Japan, and India are significant manufacturers of beef, pork, and chicken products and depend on the excellent quality of animal feed to increase their production yield. By launching innovative and cost-effective solutions for the farmer, this market acts as an opportunity for the processed animal protein manufacturer to increase their profit margin.

The European Union’s supportive regulations are to start PAPs in animal feed to drive the region’s growth. With the emerging technology and science, PAPs’ influence on animals has been safe in recent years. Owing to these, the European government is prompted to lift the ban on the use of PAP as animal feed for animals other than cattle. The use is still banned due to causing bovine spongiform encephalopathy (BSE) disease. New safety regulations enable farm owners to adopt them as an alternative to plant-based products used as animal feed in the processed animal protein market.

The objective of the report is to present a comprehensive analysis of the Global Processed Animal Protein Market to the stakeholders in the industry. The past and current status of the industry, with the forecasted market size and trends, are presented in the report, with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Processed Animal Protein Market dynamics, structure by analyzing the market segments and projecting the Processed Animal Protein Market size. Clear representation of competitive analysis of key players by Vehicle type, price, financial position, product portfolio, growth strategies, and regional presence in the Processed Animal Protein Market makes the report an investor’s guide.

Processed Animal Protein Market Competitive Landscape

The competitive landscape of the Processed Animal Protein market in North America is dominated by key players like Tyson Foods, led by its vertically integrated operations, strategic acquisitions, and strong investments in sustainability and innovation. Cargill operates closely with its expansive global footprint, advanced animal nutrition solutions, and food safety. Smithfield Foods, a global pork processing leader, capitalizes on its robust supply chain and wide international market access. Valley Proteins and Sanimax focus on rendering and transforming animal by-products into high-value protein meals, offering tailored feed solutions.

Companies collectively grow by leveraging economies of scale, technological advancements, and environmental compliance. Also, investments in alternative protein technologies, digital supply chain systems, and sustainable rendering practices position them at the forefront of industry transformation. Market remains highly competitive with continuous innovation and consolidation shaping its future.

Processed Animal Protein Market Key Trends

| Key Trends | Details |

| Shift Toward Sustainable Protein Sources | Demand is increasing for eco-friendly alternatives like insect protein and algae-based meals to reduce environmental impact and reliance on soy or meat. |

| Rising Use in Pet Food and Aquaculture | High nutritional value and digestibility make processed animal protein a preferred ingredient in premium pet food and aquafeed formulations. |

| Stringent Regulations and Traceability | Regulatory bodies are enforcing strict standards on sourcing, quality, and safety, driving companies to improve traceability and product certification. |

| Innovation in Blended & Value-Added Products | Companies are developing hybrid products that combine animal and plant proteins, offering cost-effective, functional, and sustainable solutions. |

Processed Animal Protein Market Recent Development

• On June 18, 2025, Wen’s Food Group (China) significantly reduced soymeal usage in its feed formulations and advanced the use of insect protein and synthetic amino acids to comply with China's national feed reform, alongside Muyuan Foods.

• On November 20, 2024, BRF S.A. (Brazil) signed a binding agreement to acquire a processed foods plant in Henan, China, for US$ $43 million, with an additional $36 million investment planned to double production capacity by Q1 2025, aiming to strengthen its direct presence in the Chinese market.

• On March 14, 2025, BioMar (Denmark) announced the full acquisition of LetSea, reinforcing its leadership in aquafeed R&D and supporting the advancement of sustainable seafood production.

• In April 2025, Packaged Feeds & FreezeM (UK/Germany) launched modular Black Soldier Fly (BSF) insect protein farms using FreezeM’s PauseM breeding technology, with the capacity to process over 15,000 tons of organic waste annually.

• On February 27, 2025, Calysseo (China) launched FeedKind Pet, a fermentation-derived alternative protein for pet food, and began exports to the EU, UK, and Canada after receiving necessary regulatory approvals.

Processed Animal Protein Market Scope: Inquiry Before Buying

| Processed Animal Protein Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 14.20 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 3.02% | Market Size in 2032: | USD 18.02 Bn. |

| Segments Covered: | by Source | Pork Beef Poultry Others |

|

| by Form | Liquid Dry |

||

Processed Animal Protein Market, by Region

North America (United States, Canada, Mexico)

Europe (Germany, United Kingdom, France, Italy, Spain, Netherlands, Sweden, Switzerland, Belgium, Russia, Poland, Finland, Norway, Austria, Ireland, Greece)

South America (Brazil, Argentina, Chile, Colombia, Peru, Paraguay, Bolivia, Venezuela)

Asia Pacific (China, India, Japan, Australia, South Korea, New Zealand, Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines, Bangladesh)

Middle East and Africa (Saudi Arabia, Qatar, Kuwait, Oman, South Africa, Nigeria, Israel, Jordan)

Processed Animal Protein Market key players

North America

1. Tyson Foods (USA)

2. Valley Proteins (USA)

3. Boyer Valley Company (USA)

4. Cargill (USA)

5. Smithfield Foods (USA)

6. National Beef Packing Co. (USA)

7. Perdue Farms (USA)

8. Sanimax (Canada)

9. West Coast Reduction (Canada)

Europe

10. Sonac – Darling Ingredients (Netherlands)

11. Leo Group (UK)

12. Tönnies Holding (Germany)

13. PHW Group (Germany)

14. Lactalis International (France)

15. Arla Foods (Denmark)

16. Glanbia (Ireland)

Asia Pacific

17. Ridley Corporation (Australia)

18. Muyuan Foodstuff (China)

19. Wen’s Food Group (China)

20. Nordfeed (Turkey)

21. Nippon Suisan Kaisha (Japan)

22. GFPT Public Company (Thailand)

South America

23. BRF S.A. (Brazil)

24. JBS S.A. (Brazil)

25. Marfrig Global Foods (Brazil)

26. FASA Group (Brazil)

27. Terramar Chile (Chile)

Middle East & Africa

28. Nordfeed (Turkey)

29. Al-Watania Agriculture (Saudi Arabia)

30. Atyab Foodtech (Egypt)

Frequently Asked Questions

1. Which region has the largest share in the Global Processed Animal Protein Market?

Ans: The North America region held the highest share in 2024.

2. What is the growth rate of the Global Processed Animal Protein Market?

Ans: The Global Processed Animal Protein Market is growing at a CAGR of 3.02% during the forecasting period 2025-2032.

3. What is the scope of the Global Processed Animal Protein Market report?

Ans: The Global Processed Animal Protein Market report helps with the PESTEL, Porter's, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in the Global Processed Animal Protein Market?

Ans: The important key players in the Global Processed Animal Protein Market are – Sanimax, FASA Group, Leo Group Ltd., Valley Proteins, West Coast Reduction, Nordfeed, BOYER VALLEY COMPANY, LLC, Ridley Corporation Limited, Sonac, Tyson Foods, Inc, JBS USA Holdings Inc., Cargill Meat Solutions Corp., SYSCO Corp., Smithfield Foods Inc., Hormel Foods Corp., National Beef Packing Co. LLC, Perdue Farms Inc., and OSI Group LLC

5. What is the study period of this Market?

Ans: The Global Processed Animal Protein Market is studied from 2024 to 2032.