Pig Iron Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

The Pig Iron Market size was valued at USD 10.45 Billion in 2024 and the total Pig Iron Market revenue is expected to grow at a CAGR of 7.8% from 2025 to 2032, reaching nearly USD 19.06 Billion

Pig iron is the result of the smelting process, wherein iron ore (including ilmenite) is fused with a high-carbon fuel and a reducing agent like coke, often in conjunction with limestone to serve as a fluxing agent. Alternative fuel and reductant sources such as charcoal and anthracite are also employed. The production of pig iron is achieved through two primary methods: one involves the smelting of iron ore in blast furnaces, while the other entails the smelting of ilmenite in electric furnaces. The industry's performance is primarily influenced by the ever-expanding construction and infrastructure sectors, which demand substantial quantities of pig iron for structural components and reinforcement materials.

Furthermore, the automotive industry's growing need for high-strength iron and steel has bolstered market growth. Recent advancements in blast furnace technology and increased recycling initiatives have also contributed to sustainable production methods, adding an eco-friendly dimension to the market. Key market players such as ArcelorMittal, Nucor Corporation, and Tata Steel have been pivotal in driving innovation and expansion, focusing on enhancing production efficiency and minimizing environmental impacts. A notable recent development in the pig iron market includes the adoption of advanced smelting techniques to reduce carbon emissions, aligning with global sustainability goals.

Additionally, the increasing shift towards electric arc furnace-based pig iron production methods, which are more energy-efficient and environmentally friendly, is poised to reshape the market landscape. These transformations are set to bring sustainable growth and increased competitiveness in the pig iron market, making it an exciting space to watch for both industry players and investors.

According to MMR analysis, in July 2023, American steel firms raised their imports of pig iron from Ukraine by 40.2% in comparison to the preceding month, reaching a total of 119.6 thousand tons. When compared to July 2022, the supply of these raw materials surged by 4.7 times. Between January and July 2023, American steel manufacturers utilized 748,400 tons of pig iron produced in Ukraine, marking a 2.3-fold increase compared to the same period in 2022. However, in contrast to the pre-war year 2021, the import of Ukrainian pig iron to the USA saw a decrease of 32.5%. Notably, Ukrainian pig iron exports to the USA have witnessed a substantial surge in 2023. In January and February, shipments reached 116.9 thousand tons and 156 thousand tons, respectively.

Additionally, volumes exceeding 100 thousand tons were recorded in May and July, with figures of 123.95 thousand tons and 119.6 thousand tons, respectively. The March export figure was the highest since September 2021 when Ukraine dispatched 185.6 thousand tons of pig iron to the United States. Throughout 2022, the monthly shipment average stood at 45.85 thousand tons, a number that has substantially risen to 106.9 thousand tons in 2023, compared to 140.2 thousand tons in 2021. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Market Dynamics:

Drivers:

Infrastructure and construction sectors are pivotal drivers, as countries invest in building and upgrading their urban landscapes, increasing demand for pig iron. Simultaneously, the automotive industry's expansion necessitates high-quality pig iron for critical components, exemplified by Germany's demand for automotive manufacturing. Technological advancements in blast furnace operations enhance efficiency and reduce emissions, with innovations like ArcelorMittal's Top Gas Recovery Turbine contributing to sustainability and cost-effectiveness. Recycling initiatives aimed at sustainability and circular economies are gaining traction, exemplified by Nucor Corporation's recycling endeavors. The shift to electric arc furnace (EAF) production methods is revolutionizing the market, led by companies like Gerdau, fostering demand for pig iron produced via EAF.

Global urbanization trends, particularly in countries like India, amplify the need for pig iron in construction and infrastructure development. The economic growth of emerging markets, including BRICS countries, fuels their manufacturing sectors' reliance on pig iron, evident in Brazil's thriving steel industry. Stricter environmental regulations and emissions reduction targets, such as the EU's commitment to carbon neutrality, are reshaping the industry towards sustainability.

Supply chain resilience, underscored by global disruptions like the COVID-19 pandemic, prompts companies to diversify supply sources, driving growth in the pig iron market. Innovation and product development remain crucial, with companies like Tata Steel pioneering new pig iron grades for specialized applications, contributing to market expansion. In conclusion, the pig iron market's growth is a dynamic outcome of a complex interplay of these ten drivers, each playing a unique role in shaping its trajectory and ensuring its relevance in the ever-evolving steel production supply chain.

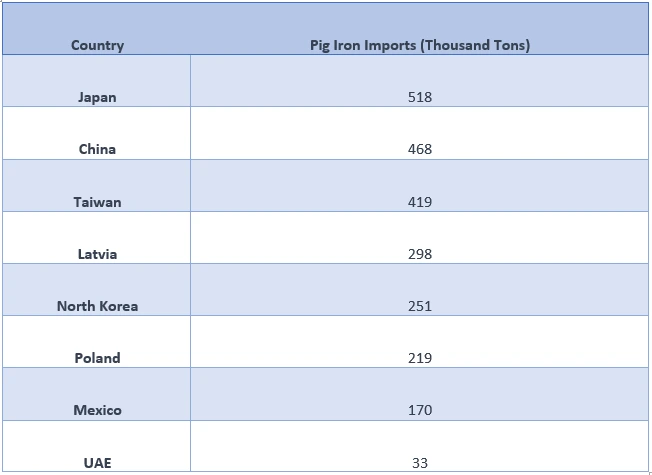

For instance, Italian metallurgists have imported 3.8 million tons of pig iron from Russia in the span of seven months, while an additional 1.2 million tons of this vital product were shipped to Turkey. Notably, Italy played a substantial role in this trade, as it constituted more than 50% of Russia's pig iron exports, totaling 3.81 million tons in the first seven months of 2023. In total, Russia's pig iron exports reached 7.52 million tons during this period, as reported by SteelRadar. Furthermore, Turkey received 1.2 million tons of Russian-made pig iron, accounting for 15.8% of the overall exports. In essence, the combined imports of pig iron by Italy and Turkey represented over 66% of Russia's total exports of this commodity.

Importers of Pig Iron from Russia in January-July 2023

Restrains:

Stricter environmental regulations, exemplified by the European Union's emission targets, demand substantial investments in emissions control and cleaner practices. Economic fluctuations and the economic impact of events like the COVID-19 pandemic pose uncertainty and can lead to reduced pig iron demand. The availability of alternative materials, trade barriers, and tariffs can disrupt market access, while the cyclicality of end-use industries, iron ore price volatility, and energy cost fluctuations impact production costs and profitability. Overcapacity and technological advancements in steel production, including cleaner methods like hydrogen-based reduction, can challenge traditional pig iron production. Additionally, geopolitical instability and trade tensions can disrupt market stability. Overcoming these obstacles and adapting to evolving market conditions is essential for the pig iron industry's sustainable growth and success.

Opportunities:

The ongoing expansion of global infrastructure projects, exemplified by China's ambitious "Belt and Road Initiative," presents a substantial avenue for increased pig iron demand. Urbanization trends worldwide further bolster this demand, as urban development requires vast quantities of pig iron for construction and infrastructure. Moreover, the evolving automotive industry, particularly the transition to electric vehicles, offers a unique opportunity for pig iron as it plays a crucial role in the production of electric vehicle components like motor casings.

For instance, Jindal Stainless has recently entered into a joint venture agreement with a subsidiary of Eternal Tsingshan to establish a greenfield nickel pig iron plant in Indonesia, with a production capacity of 200,000 metric tonnes. Jindal Stainless is set to invest $157 million (approximately Rs 1,290 crore) in the project over the next two years, securing a 49% equity stake, while the remaining stake will be held by New Yaking Pte, a subsidiary of Eternal Tsingshan. This strategic move underscores Jindal Stainless' commitment to expanding its presence in the nickel pig iron market and reinforces their investment in sustainable and efficient production processes.

The burgeoning renewable energy sector, reliant on pig iron for wind turbines and solar panel supports, creates yet another growth avenue. Additionally, a growing emphasis on sustainability and recycling introduces the concept of recycled pig iron, aligning with environmental goals and opening new markets. Research and development efforts aimed at enhancing blast furnace efficiency and reducing emissions can boost cost-effectiveness and sustainability in pig iron production.

Furthermore, global trade agreements, technological advancements like hydrogen-based direct reduction, resilient supply chains, and the expansion of emerging markets like India and Brazil collectively contribute to the pig iron market's promising growth prospects, making it an industry with exciting opportunities on the horizon. In 2021, US Steel has revealed multiple plans aimed at expanding pig iron production capacity within the United States. Their primary objective is to bolster the supply of pig iron to support their electric arc furnace operations at the Big River Steel facility located in Arkansas.

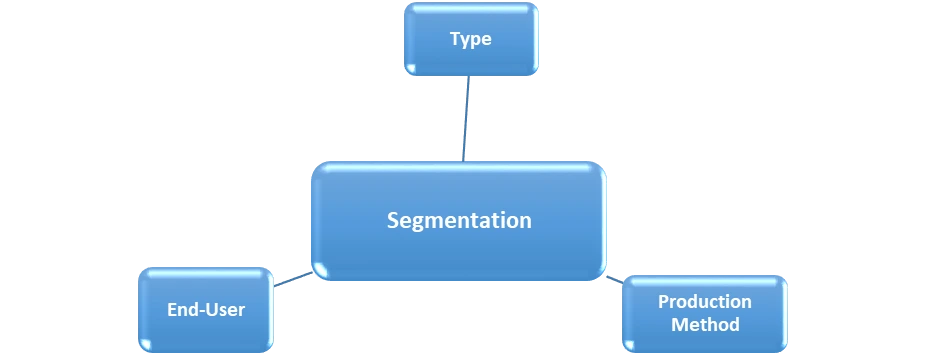

Pig Iron Market Segmentation Analysis:

Based on Type, the market has been divided into Basic Pig Iron, Foundry Pig Iron, and Nodular Pig Iron. Among these, the Nodular Pig Iron sub-segment is projected to generate the maximum revenue in 2024. Nodular pig iron finds its primary use in the automotive industry, where it is crucial for the production of cast iron parts with enhanced ductility and strength. Its adoption in this sector is substantial, as it contributes to the development of critical components like engine blocks and crankshafts. This is a high-purity iron designed specifically for the production of Nodular or Ductile irons.

Its classification is based on its Phosphorus content, and its composition analysis allows foundries to meet the stringent application requirements set by their clients. Additionally, the construction industry utilizes nodular pig iron for manufacturing structural elements, such as beams and columns, owing to its remarkable structural properties. The adoption in this subsegment is driven by the construction sector's continued growth and the need for robust and durable materials.

Additionally, nodular pig iron plays a role in the manufacturing of pipes, providing corrosion-resistant solutions for various industries. Overall, nodular pig iron exhibits varying degrees of adoption within these subsegments, primarily based on the specific requirements of each application, indicating its adaptability across diverse sectors.

Based on Production method, the market has been divided into Blast Furnace, and Direct Reduction. Among these, the Blast Furnace sub-segment is projected to generate the maximum revenue in 2024. Hot metal and pig iron, produced through the time-tested method of Blast Furnace ironmaking, play an indispensable role in the global steel industry, constituting a staggering 60% of all steel products consumed by the world's population. This remarkable statistic underscores the enduring significance of Blast Furnace technology in the modern steel production landscape. Blast Furnace ironmaking has a rich history, dating back to its inception in the 14th century, and it remains at the core of steel production.

Despite its deep historical roots, the technology continues to adapt and innovate, making it one of the most versatile and adaptable methods for winning the primary metal required for a multitude of essential applications. From construction to machinery, tools, healthcare equipment, vehicles, and household appliances, the products of Blast Furnace ironmaking find their way into numerous aspects of our daily lives. The technology's resilience and ability to meet diverse industrial needs make it a linchpin of the steel industry.

In construction, hot metal and pig iron serve as the foundational materials for structural elements like beams, columns, and girders. Their strength and durability are key attributes that ensure the integrity of buildings and infrastructure projects. Machinery and tools rely on these iron products to create components and machinery parts that are robust and long-lasting. This durability is critical in manufacturing and industrial settings, ensuring that equipment operates efficiently over extended periods. Healthcare equipment, including specialized devices and instruments, often incorporates pig iron due to its precise and reliable properties, vital in maintaining the highest standards of patient care and medical diagnostics.

Vehicles, from automobiles to heavy-duty trucks, benefit from the use of hot metal and pig iron in engine components such as engine blocks and crankshafts, contributing to fuel efficiency, performance, and longevity. Even household appliances, such as ovens, refrigerators, and washing machines, feature components made from these iron products, ensuring their durability and dependability in daily household use.

Regional Insights of Pig Iron Market:

The pig iron market exhibits distinct regional insights, characterized by variations in large producing regions, significant consuming areas, and the dynamics of import and export activities. Large producing regions are often anchored in countries with robust steel industries. Notably, China, as the world's largest steel producer, plays a pivotal role in pig iron production, contributing to a considerable share of the global market. Additionally, Russia, Brazil, and India are prominent pig iron producers, with their steel sectors driving domestic pig iron manufacturing.

Conversely, large consuming regions encompass countries with flourishing construction, automotive, and industrial sectors, such as the United States, Japan, and Germany, where pig iron is integral for manufacturing durable components. Regional import and export data is equally influential, with some nations like Italy and Turkey being substantial importers of Russian pig iron. These countries account for a significant portion of Russian pig iron exports, reflecting the global trade dynamics that underpin the market. On the other hand, countries with significant exports, such as Brazil and Ukraine, contribute to the international pig iron trade, while their production capacities meet both domestic and foreign demands. The pig iron market's regional insights are shaped by a complex interplay of production, consumption, and trade dynamics, reflecting the market's global reach and its essential role in various industrial sectors.

Competitive Landscape

The competitive landscape in the pig iron market is shaped by a diverse group of global players, each with its own strengths and strategies. ArcelorMittal, headquartered in Luxembourg, is a key leader known for its extensive global reach and innovative approaches to sustainability, as it seeks to reduce its carbon footprint. Nucor Corporation, a U.S.-based giant, stands out for its focus on electric arc furnace (EAF) technology, emphasizing energy efficiency and environmental responsibility. South Korea's POSCO, renowned for its advanced steelmaking techniques, brings cutting-edge expertise to the market.

Brazil's Vale S.A. boasts a significant presence and a strong commitment to sustainable mining and metal production. Meanwhile, ThyssenKrupp AG from Germany is known for its diversified portfolio and technological advancements. India's Tata Steel, a major player in the global steel industry, continuously expands its operations and embraces innovation. Baowu Steel Group, the largest steel producer in China, combines its extensive production capacity with efforts to reduce emissions.

To illustrate, China's leading steelmaker, China Baowu Group, has declared a collaboration with Vale and Shandong Xinhai Technology to venture into the production of nickel pig iron (NPI), a crucial raw material for stainless steel, in Indonesia. Through its subsidiary, Taigang Iron and Steel, one of China's top stainless steel producers, a framework agreement has been signed with PT Vale Indonesia (PTVI) and NPI manufacturer Xinhai to jointly operate the Bahodopi nickel processing facility in Morowali, Sulawesi. Vale will retain a 49% stake in the project, with the facility anticipated to yield approximately 73,000 tonnes of NPI annually based on nickel content.

The remaining 51% ownership will be divided between China Baowu and Xinhai. Indonesia, a significant global nickel ore producer, has been attracting substantial Chinese investments in its nickel sector, imposing a ban on nickel ore exports since 2020 to encourage domestic processing and downstream industry development.

Pig Iron Market Scope: Inquire before buying

| Pig Iron Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | US $ 10.45 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 7.8 % | Market Size in 2032: | US $ 19.06 Bn. |

| Segments Covered: | by Type | Basic Pig Iron Foundry Pig Iron Nodular Pig Iron |

|

| by Production Method | Blast Furnace Direct Reduction |

||

| by End User | Construction and infrastructures. Automotive Transportation Energy industry |

||

Pig Iron Market Regional Insights:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Pig Iron Market Key Players:

1. Nucor Corporation (USA)

2. Steel Dynamics, Inc. (USA)

3. ArcelorMittal (Canada)

4. Tata Steel(India)

5. Baosteel Group Corporation(Shanghai, China)

6. JSW Steel Ltd((Mumbai)

7. Magnitogorsk Iron and Steel Works (Magnitogorsk, Russia)

8. HBIS Group(Shijiazhuang, China)

9. Erdemir Group (Ereğli, Türkiye)

10. Evraz Group(London, United Kingdom)

11. Severstal(Cherepovets, Russia)

FAQs:

1. What are the growth drivers for the Pig Iron Market?

Ans. The growth drivers for the Pig Iron Market include increased demand from the construction and automotive industries, the growth of urbanization and infrastructure projects, and its use as a raw material in steel production, which drives the demand for pig iron.

2. What is the major Opportunity for the Pig Iron Market growth?

Ans. One major opportunity for Pig Iron Market growth is the increasing emphasis on sustainable and environmentally friendly manufacturing processes. Pig iron producers can explore more eco-friendly production methods, recycling, and reducing carbon emissions to meet evolving sustainability standards and capture market share. Additionally, the demand for pig iron in emerging markets with expanding industrial sectors offers growth prospects.

3. Which Region is expected to lead the global Pig Iron Market during the forecast period?

Ans. North America is expected to lead the Pig Iron Market during the forecast period.

4. What is the projected market size and growth rate of the Pig Iron Market?

Ans. The Pig Iron Market size was valued at USD 10.45 Billion in 2024 and the total Pig Iron Market revenue is expected to grow at a CAGR of 7.8% from 2025 to 2032, reaching nearly USD 19.06 Billion.

5. What segments are covered in the Pig Iron Market?

Ans. The segments covered in the Pig Iron Market report are Type, Production Method, End User, and Region.