Global Methanol Market by Feedstock, Derivatives, Grade, End-User, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

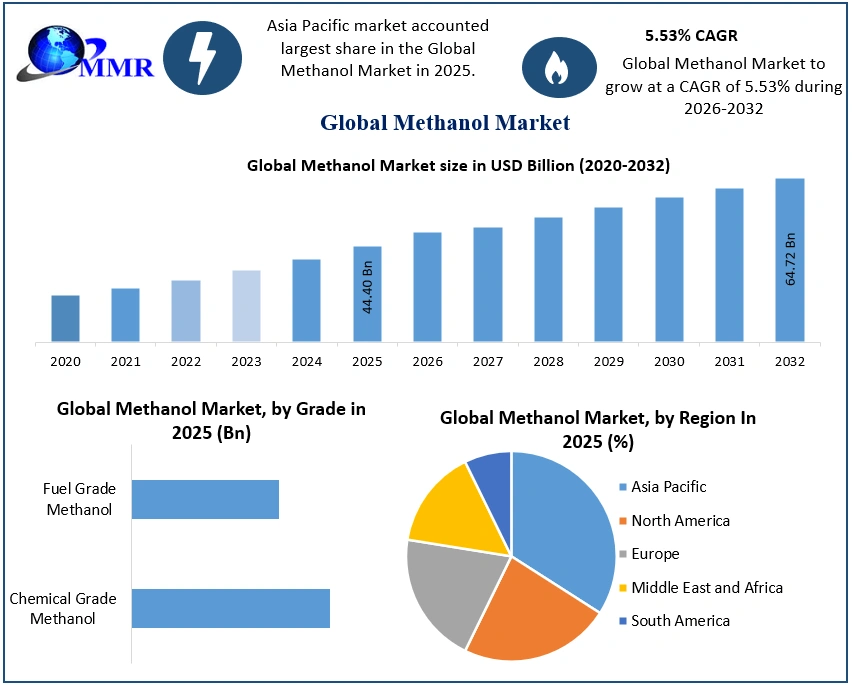

The Methanol Market size was valued at USD 44.40 Billion in 2025 and the total Methanol revenue is expected to grow at a CAGR of 5.53% from 2025 to 2032, reaching nearly USD 64.72 Billion by 2032.

The strong growth reflects rising demand for methanol across chemicals, fuels, energy applications, and emerging clean-technology markets.

Methanol Market Overview:

Methanol is a simple alcohol (CH₃OH) that is colorless, volatile, and highly flammable, widely used as a feedstock in chemicals, fuels, and industrial applications. It is produced mainly from natural gas or coal and serves as a key ingredient in formaldehyde, acetic acid, plastics, and clean-fuel technologies. The global production landscape includes more than 90 operational methanol plants, offering a combined capacity of 110–140 million tons, with Asia-Pacific particularly China accounting for over 50% of total consumption due to extensive methanol-to-olefins (MTO) and methanol-to-propylene (MTP) operations.

Traditional methanol applications such as formaldehyde, acetic acid, MTBE, DME, plastics, adhesives, paints, and resins continue to dominate demand; however, the fastest-growing category is fuel-grade methanol, driven by its adoption in marine fuel, power generation, gasoline blending, and hydrogen carrier technologies. The shift toward sustainable production is accelerating the growth of green methanol, bio-methanol, e-methanol, and blue methanol. The maritime industry is the catalyst for this shift. Leading shipping operators have placed large orders for methanol-powered vessels, anticipating that green methanol could supply up to 13% of global bunker fuel by 2050. The investments in CO₂-to-methanol, waste-to-methanol, and hydrogen-based e-methanol technologies are reshaping the global supply chain and reducing dependence on fossil-based feedstocks. With rising adoption in chemicals, automotive, construction, packaging, textiles, electronics, marine fuel, and clean energy systems, the Methanol Market is transitioning from a conventional petrochemical commodity to a strategic low-carbon energy carrier.

To know about the Research Methodology :- Request Free Sample Report

Methanol Market Trends:

| Methanol Market Trend | Description | Impact on Market |

| Green Methanol Expansion | Rapid growth of e-methanol & bio-methanol using CO₂ + green hydrogen, fueled by global decarbonization goals. | Expected 30–40% CAGR; major investments in Denmark, China, Mexico. |

| Methanol as Marine Fuel | Adoption by global shipping companies to meet IMO 2030/2050 mandates; >200 methanol-powered vessels on order. | Projected to supply 13% of marine fuels by 2050. |

| Methanol-to-Olefins (MTO/MTP) Growth | China leading expansion of methanol-to-ethylene & propylene plants for plastics and polymers. | Drives 50%+ of APAC demand growth. |

| Waste-to-Methanol & Biomass Methanol | Conversion of municipal waste, agricultural residues & biomass into methanol. | Fastest-growing renewable feedstock segment. |

| Digital Methanol Trading Platforms | Shift toward AI-enabled procurement, digital contracts & predictive logistics. | 30% of B2B buyers using digital platforms by 2025. |

Methanol Market Dynamics:

Energy Transition, Clean Fuels, Technological Innovation, and Expanding Petrochemical Demand Accelerating Growth of the Global Methanol Market Across Industrial, Marine, and Renewable Applications

The Methanol Market is experiencing accelerated global growth driven by soaring demand for clean fuels, expanding petrochemical production, and rapid adoption of renewable methanol in the energy transition. More than 40% of global methanol consumption is tied to downstream chemical manufacturing, formaldehyde, acetic acid, MTBE, and olefins, highlighting its central role in plastics, construction materials, automotive components, and electronics. In China, where MTO/MTP plants dominate, methanol-based olefin production meets 20% of the country’s ethylene and propylene needs, reinforcing methanol’s strategic importance in the global plastics value chain.

The growing shift toward green methanol, bio-methanol, and e-methanol, fueled by international decarbonization targets. The maritime sector is leading this transition: more than 200 methanol-powered vessels are currently on order globally, and methanol is expected to supply up to 13% of global marine fuel demand by 2050, driven by IMO emission mandates. Shipping giants such as Maersk, COSCO, and CMA CGM are signing long-term offtake agreements for renewable methanol, accelerating methanol market penetration across Asia, Europe, and North America.

Digital commerce trends impacting industrial procurement are reshaping methanol trading. Nearly 30% of bulk chemical buyers prefer digital procurement platforms for transparent pricing, logistics visibility, and secure contracting mirroring the shift seen in other B2B commodity markets. The industrial consumption is rising as methanol becomes increasingly integrated into gasoline blending, biodiesel production, fuel cells, hydrogen storage solutions, and power generation, with fuel-grade methanol market demand growing at over 8% annually.

Sustainability, Regulatory Pressures, and Supply Chain Challenges Redefining the Methanol Industry Amid Transition to Renewable Feedstocks and Carbon-Neutral Production Pathways

Despite strong growth, the Methanol Market faces critical challenges. Over 70% of global methanol production still relies on natural gas or coal, exposing the industry to volatile feedstock prices and high CO₂ emissions. Coal-based methanol alone emits 3x more CO₂ than natural gas-based production, prompting governments and industries to accelerate the shift toward blue methanol (with CCS) and green methanol. Rising environmental scrutiny and carbon taxation especially in Europe are pushing manufacturers toward low-emission technologies, but production costs for green methanol remain 2–4x higher than conventional methanol, slowing mass adoption.

Global supply chains are under strain. Methanol prices fluctuate sharply based on natural gas supply, geopolitical tensions, shipping bottlenecks, and plant outages. During 2023–2025, price volatility in key regions exceeded 25–30%, creating uncertainty for downstream chemical producers. Capacity expansion remains geographically concentrated more than 60% of new methanol capacity additions are located in China and the Middle East, leading to regional imbalances in supply and trade.

Sustainability trends are transforming long-term opportunities. Renewable methanol (bio + e-methanol) is projected to exceed 20 million tons of demand by 2035, driven by adoption in marine fuel, aviation e-fuels, industrial heating, and green chemical production. At the same time, advanced technologies such as CO₂-to-methanol, modular methanol reformers, AI-enabled process optimization, and next-generation catalysts are increasing production efficiency by 15–25%, reducing energy intensity and accelerating the shift toward cleaner pathways.

Opportunities: Renewable Methanol, CO₂-to-Methanol Technologies, Marine Fuel Adoption, and Low-Carbon Industrial Transformation

The Methanol Market offers significant long-term opportunities driven by sustainability, technological upgrades, and energy transition policies. The largest opportunity lies in renewable methanol (bio + e-methanol), which is projected to exceed 20 million tons of demand by 2035, driven by adoption in marine fuel, aviation e-fuels, industrial heating, green chemicals, and net-zero manufacturing. As shipping decarbonizes, demand for green methanol marine fuel is expected to surge, with global shipping lines planning 500+ methanol-capable vessels by 2030. Breakthrough technologies such as CO₂-to-methanol conversion, modular methanol reformers, and hydrogen-based e-methanol plants are reducing carbon intensity and attracting heavy investments from energy companies. Carbon capture integration is improving operational efficiency by 15–25%, positioning blue methanol as a major transitional fuel. Governments worldwide are offering incentives, tax credits, and green fuel subsidies, creating new growth opportunities for producers. Growing applications in fuel cells, power generation, hydrogen carriers, clean mobility, and emissions-efficient chemical production further broaden market potential. With its versatility, lower emissions profile, and alignment with global net-zero pathways, methanol is emerging as one of the most attractive opportunities in the clean energy and sustainable petrochemical market.

Methanol Market Segment Analysis:

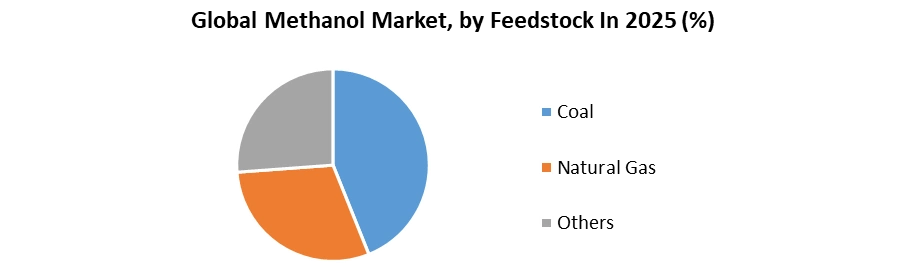

Based on Feedstock, the Methanol Market is segmented into Coal-Based Methanol, Natural Gas-Based Methanol, and Others (Biomass, CO₂ + Hydrogen, and Waste-Based Methanol). The Natural Gas-Based Methanol segment dominated the Methanol market in 2025, accounting for the largest share due to its lower carbon intensity, cost-effective production, and wide availability of natural gas in regions such as the Middle East, North America, and Russia. Natural gas remains the most preferred raw material for global methanol production, especially for formaldehyde, acetic acid, MTBE, olefins, solvents, and clean-fuel applications. The stability, scalability, and high energy efficiency of natural gas-based processes make this segment the backbone of global methanol supply, particularly for export-oriented producers.

The Coal-Based Methanol segment held a significant share, driven primarily by China, where coal accounts methanol production. Coal-to-methanol plants support large-scale downstream applications, especially in MTO/MTP units for plastics and petrochemicals. However, high CO₂ emissions from coal-based production continue to create environmental concerns and regulatory pressure.

The Others segment, which includes biomass, renewable hydrogen + captured CO₂ (e-methanol), and waste-to-methanol, is the fastest-growing category. The smaller in volume, this segment is expanding rapidly due to the rising global demand for green methanol and sustainable fuel alternatives in marine shipping, power generation, and low-carbon chemical manufacturing.

Based on End-User, the Methanol Market is segmented into Construction, Automotive, Electronics, Appliances, Paints & Coatings, Insulation, Pharmaceuticals, Packaging (PET Bottles), Solvents, and Others. The Construction segment dominated the market in 2025, accounting for the largest share due to methanol’s extensive use in producing formaldehyde-based resins, adhesives, laminates, plywood, MDF boards, and insulation materials. These methanol-derived products serve as critical inputs for infrastructure development, housing construction, interior furnishing, and engineered wood applications. Rapid urbanization in Asia-Pacific, rising commercial construction, and growing demand for affordable housing continue to boost methanol consumption in the construction value chain.

The Automotive and Paints & Coatings segments represent major growth contributors, driven by methanol’s role in manufacturing acetic acid, MTBE, DME, and specialty solvents used in fuels, lubricants, coatings, and lightweight plastics. The Electronics and Appliances sectors rely on methanol-based intermediates for producing polymers, insulating foams, and specialty adhesives, supporting the global market demand for consumer electronics.

The Pharmaceuticals and Packaging (PET bottles) segments utilize methanol for synthesizing active ingredients, intermediates, and PET resin, while the Solvents segment benefits from methanol’s role as a cost-effective industrial solvent across chemicals, agrochemicals, and cleaning industries. Together, these diverse applications reinforce methanol as a cornerstone raw material across industrial, commercial, and consumer product ecosystems.

Methanol Market Regional Analysis:

The Asia-Pacific (APAC) region dominated the Methanol Market in 2025, accounting for over 55% of global methanol consumption and nearly 60–65% of global production capacity. China is the undisputed leader, contributing more than 50% of global methanol demand and nearly 60% of global output, driven by its vast coal-to-methanol (CTM) infrastructure and extensive methanol-to-olefins (MTO/MTP) capacity used for producing ethylene and propylene for plastics, packaging, and textiles. Rapid industrialization, strong expansion in the construction, automotive, paints & coatings, and electronics sectors, and increasing adoption of methanol for fuel blending and power generation have strengthened APAC’s leadership.

Countries such as China, India, Indonesia, and Japan are also investing heavily in green methanol, e-methanol, and renewable hydrogen, accelerating the shift toward sustainable chemical production. APAC’s methanol imports and domestic consumption continue to rise steadily, supported by large-scale petrochemical complexes and growing demand for formaldehyde, acetic acid, solvents, adhesives, and resins. With rising energy needs, government-backed decarbonization programs, and expanding downstream manufacturing, the Asia-Pacific region is expected to maintain its dominant position through 2032, driving the majority of global methanol market growth.

Competitive Landscape

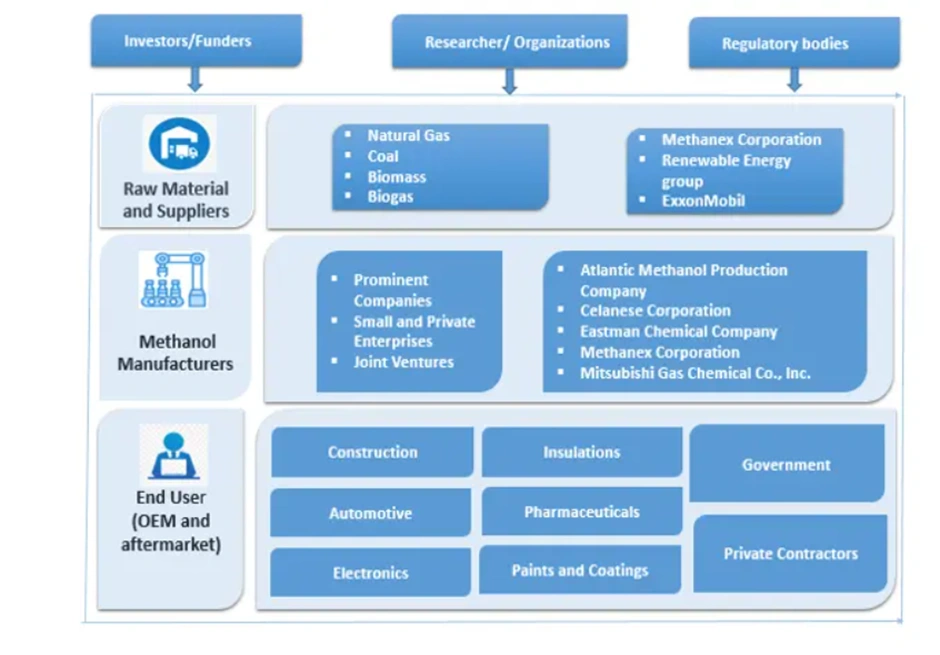

The Global Methanol Market is highly competitive and dominated by major producers across North America, Asia-Pacific, the Middle East, and Europe. Key players such as Methanex Corporation, Celanese Corporation, Atlantic Methanol, Natgasoline LLC, PETRONAS, SABIC, BASF SE, and Mitsubishi Gas Chemical control significant production capacities and global supply networks. China remains a powerhouse with companies like Yanzhou Coal Mining, Ningxia Baofeng Energy, Mitsui & Co. China, and Shanghai Huayi, supported by massive coal-to-methanol operations. Producers in Iran, Saudi Arabia, Trinidad & Tobago, and Russia strengthen regional supply, while global players focus on green methanol, e-methanol, and low-carbon technologies to gain competitive advantage.

Recent Development

On 27 June 2025, Methanex Corporation finalized the acquisition of OCI Global’s international methanol assets, strengthening its position as the world’s largest methanol producer and supplier. This strategic move expanded Methanex’s production footprint across North America, Europe, and the Middle East, while enhancing its long-term supply security for key customers in chemicals, fuels, and marine-energy sectors. The deal also improved operational efficiencies through integrated logistics networks, upgraded storage terminals, and diversified feedstock access. With this acquisition, Methanex aims to accelerate investments in low-carbon methanol, including blue and renewable methanol technologies, aligning with global decarbonization trends in shipping and industrial fuels in methanol market.

On 13 May 2025, Mitsui & Co. and European Energy inaugurated the world’s first commercial-scale e-methanol plant in Kassø, Denmark. Designed to produce 42,000 metric tons annually, the facility uses captured CO₂ and renewable hydrogen to create ultra-low-carbon methanol for global shipping and industrial applications. The project marks a major breakthrough in the green methanol market and provides long-term supply to Maersk and other major maritime operators converting vessels to methanol propulsion. This development demonstrates rapid commercialization of electrofuel technologies, supporting global IMO 2030/2050 decarbonization goals and positioning Denmark as a key hub for sustainable methanol market.

On 28 July 2025, China’s Windey Energy Technology Group Co., Ltd. shortlisted engineering firms for its 180,000-ton-per-year biomass-to-methanol project in Handan, Hebei. The project integrates agricultural residues, advanced gasification, and carbon-reduction technologies to produce low-emission green methanol for chemical and fuel applications. This marks one of China's most ambitious bio-methanol initiatives, supporting the nation’s goal of reducing coal dependency in methanol production. The development also reinforces China’s leadership in renewable methanol, with the facility expected to support downstream MTO/MTP units and emerging methanol marine fuel demand across East Asia.

On 3 November 2025, Oswal Energies Ltd signed a landmark MoU with India’s Deendayal Port Authority (Kandla-Gandhidham) to develop integrated facilities for green methanol, green hydrogen, and green ammonia, alongside a 100 MLD desalination plant. This project supports India’s National Green Energy Mission and aims to establish one of the country’s first large-scale renewable methanol production hubs. The planned facility will supply green fuels for shipping, industrial heating, and chemical applications, accelerating India’s transition toward low-carbon energy. The MoU positions Oswal Energies as a major future player in South Asia’s renewable methanol and hydrogen economy.

Methanol Market Scope: Inquire before buying

| Global Methanol Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 44.40 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 5.53% | Market Size in 2032: | USD 64.72 Bn. |

| Segments Covered: | by Feedstock | Coal Natural Gas Others |

|

| by Derivatives | Gasoline MTO/MTP Formaldehyde Methyl Tertiary Butyl Ether (MTBE) Acetic Acid Dimethyl Ether (DME) Methyl Methacrylate (MMA) Biodiesel Others |

||

| by Grade | Chemical Grade Methanol Fuel Grade Methanol |

||

| by End-User | Construction Automotive Electronics Appliances Paints & Coatings Insulation Pharmaceuticals Packaging (PET bottles) Solvents Others |

||

Methanol Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Methanol Market, Key Players:

1. Atlantic Methanol Production Company (Texas)

2. Celanese Corporation (Texas)

3. Eastman Chemical Company (United States)

4. Methanex Corporation (Canada)

5. Mitsubishi Gas Chemical Co., Inc. (United States)

6. Southern Chemical Corporation (Texas)

7. Natgasoline LLC (Texas)

8. BASF SE (Germany)

9. Methanol Holdings Limited (Trinidad & Tobago)

10. HELM AG (Hamburg)

11. Simalin Chemical Industries Pvt Ltd. (Vadodara)

12. Metafrax Chemicals (Russia)

13. Zagros Petrochemical Company (Iran)

14. SABIC (Saudi Arabia)

15. Mitsui & Co., Ltd (China)

16. Yanzhou Coal Mining Company Ltd. (China)

17. Shanghai Huayi (Group) Company (China)

18. Ningxia Baofeng Energy Group Co. Ltd (China)

FAQs:

1] What segments are covered in the Global Methanol Market report?

Ans. The segments covered in the Methanol Market report are based on Feedstock, Derivatives, Grade, End-User and Region.

2] Which region is expected to hold the highest share in the Global Methanol Market?

Ans. APAC region is expected to hold the highest share of the Methanol Market.

3] What is the market size of the Global Methanol Market by 2032?

Ans. The market size of the Methanol Market by 2032 is expected to reach USD 64.72 Bn.

4] What is the forecast period for the Global Methanol Market?

Ans. The forecast period for the Methanol Market is 2026-2032.

5] What was the Global Methanol Market size in 2025?

Ans: The Global Methanol Market size was USD 44.40 Billion in 2025.