Indian FMCG Market Size by Product Type, Demographics, Price Segment, Distribution Channel, End User-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

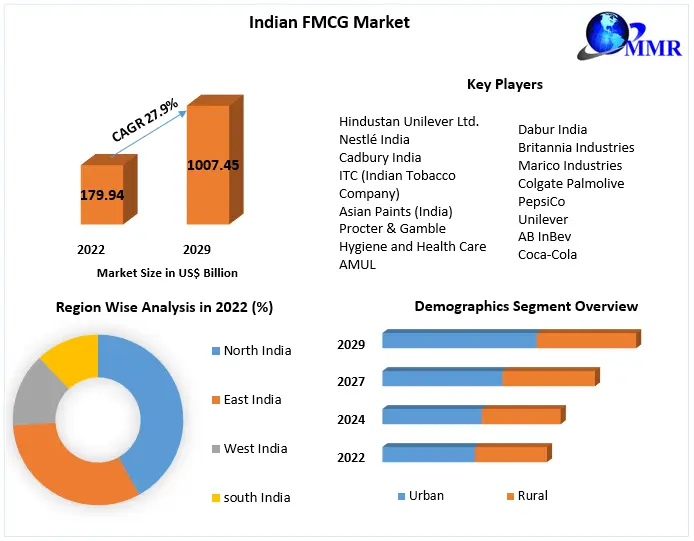

The Indian FMCG Market size was valued at USD 376.47 Billion in 2025 and the total Indian FMCG revenue is expected to grow at a CAGR of 18.8% from 2025 to 2034, reaching nearly USD 2974.82 Billion by 2034.

Indian FMCG Market Overview

FMCG products are referred to as "Fast-Moving" because customers frequently use them, which makes them quickly disappear from the store or supermarket shelves. The Indian FMCG market, known for its rapid pace, continues to increase, fueled by a surge in consumer demand, production growth, and strategic innovations. The increasing middle class, urbanization, and rising disposable incomes are significant contributors to the demand for Indian FMCG products across categories such as food and beverages, personal care, and home care. Leading Indian FMCG players like Hindustan Unilever, Nestlé India, and ITC have strengthened their market presence by offering a variety of products that cater to the evolving preferences of consumers who are seeking health, convenience, and sustainability. Enhanced production capabilities and streamlined supply chains are key factors bolstering the performance of the Indian FMCG market, ensuring a seamless supply of goods across urban and rural regions.

A notable growth driver in the Indian FMCG market is the increasing penetration in rural areas and the consumer shift towards premium and organic offerings. Innovations in packaging, product formulations, and the adoption of digital marketing have become essential to meet the changing demands of consumers. Additionally, the rise of e-commerce and direct-to-consumer models has opened up new avenues for growth, with brands like Dabur leveraging the digital shift to tap into online retail. The Indian FMCG industry is set for continued growth, shaped by demographic changes, technological progress, and a focus on consumer-centric innovations. Key trends influencing this growth include wellness, sustainability, and the digital transformation of product delivery and customer engagement.

To know about the Research Methodology:- Request Free Sample Report

Indian FMCG Market Dynamics

India FMCG Market Trend

The key trend in the India FMCG Market is the rapid shift toward premiumization, small-pack consumption, digital-first purchasing, and quick-commerce-led availability. Indian consumers are increasingly buying branded FMCG products in smaller, affordable packs while also upgrading to premium products in categories such as beauty, personal care, packaged foods, beverages, health supplements, and home care. Its growth outpaced overall volume growth, indicating stronger consumer preference for smaller packs and low-ticket SKUs.

This trend is highly visible across both rural and urban markets. Rural consumers are driving demand for affordable, small-sized packs of shampoo, biscuits, tea, detergent, oral care, edible oils, and packaged snacks. Urban consumers, especially Generation Z and Millennials, are shifting toward premium skincare, healthy snacking, ready-to-eat foods, functional beverages, organic products, and sustainable packaging.

Quick commerce has become one of the strongest trends shaping FMCG distribution. Platforms such as Blinkit, Zepto, Swiggy Instamart, BigBasket, and Flipkart Minutes are changing consumer purchase behavior by enabling the delivery of daily essentials within minutes. Flipkart Minutes expanded to 1,000 fulfilment centres across 130 cities, reflecting the scale of competition in India’s instant delivery market.

India FMCG Market Opportunity

A major opportunity in the India FMCG Market lies in the expansion of rural consumption, quick commerce, premium products, and regional product customization. Rural India is becoming a high-potential growth zone as rising farm income, better road connectivity, digital payment penetration, and wider distribution networks improve access to branded FMCG products. In Q1 2025, rural demand grew nearly four times faster than urban demand, highlighting the shift in consumption momentum from metros to smaller towns and villages.

This creates strong opportunities for companies such as HUL, Dabur, Britannia, Marico, ITC, Nestlé India, Tata Consumer, Amul, Emami, and Patanjali, especially in low-unit-price packs, sachets, small SKUs, regional flavors, herbal personal care, health foods, and daily nutrition products. For example, rural consumers continue to prefer economy and mid-range packs, while urban consumers are increasingly buying premium, convenience-led, and health-oriented products.

Another major opportunity is the growth of online retail and quick commerce. In urban India, e-commerce accounted for 6% of FMCG sales, while it reached 14% across metros and 18% in the top eight metros. Quick commerce contributed more than three-fourths of e-commerce FMCG sales, making it a key opportunity for brands focused on instant delivery, impulse purchases, beverages, snacks, personal care, and household essentials.

India FMCG Market Restraint

A major restraint in the India FMCG Market is the pressure from inflation, raw material price volatility, intense competition, margin compression, and uneven rural purchasing power. FMCG companies depend heavily on commodities such as palm oil, crude oil derivatives, milk, wheat, sugar, tea, coffee, packaging materials, and transportation fuel. Any price increase in these inputs directly affects production cost, distribution cost, and retail pricing.

This restraint is more visible in rural and lower-income markets, where consumers are highly price-sensitive. If FMCG companies increase prices aggressively, rural consumers may shift to smaller packs, local brands, unorganized products, or delay discretionary purchases. This affects categories such as premium personal care, packaged snacks, beverages, branded staples, and household cleaning products.

Small and regional FMCG players are gaining share in rural markets due to lower pricing, local distribution strength, and flexible product offerings. NielsenIQ noted that small players were gaining ground in 2025 due to changing market dynamics and a low base.

India FMCG Market Segment Analysis

By product type, the food & beverages segment dominated the Indian FMCG Market in 2025 due to high consumption frequency and wide product coverage across packaged foods, dairy, biscuits, snacks, beverages, tea, coffee, edible oils, confectionery, and ready-to-eat foods. The food & beverages are the most attractive segment for companies such as Amul, Britannia, Nestlé India, Parle Products, ITC, Tata Consumer, Coca-Cola India, PepsiCo India, and Patanjali. Rising demand for protein-based foods, dairy products, packaged snacks, healthy beverages, frozen foods, and convenience-led meal solutions is strengthening this segment.

By demographics, Millennials and Generation Z are emerging as the most influential consumer groups. They are driving demand for digital-first FMCG purchases, premium personal care, beauty products, healthy foods, functional beverages, and sustainable brands. Flipkart reported 50% year-on-year growth in its beauty and personal care category, with Gen Z contributing nearly 60% of beauty purchases on the platform.

India FMCG Market Regional Insights

Regionally, the Indian FMCG Market is led by North India and West India in terms of large-scale consumption, retail density, population base, and brand penetration. North India dominated the Indian FMCG Market in 2025, benefits from high demand across Uttar Pradesh, Delhi-NCR, Punjab, Haryana, Rajasthan, and Uttarakhand, where packaged foods, dairy, personal care, oral care, beverages, and household products have strong penetration. West India, especially Maharashtra and Gujarat, is a key FMCG hub due to higher urbanization, stronger modern retail networks, manufacturing presence, and higher disposable income.

However, South India is emerging as the most digitally advanced FMCG region. NielsenIQ reported that southern metros surpassed 21% e-commerce share in FMCG sales, making the region a leader in online FMCG adoption. Cities such as Bengaluru, Chennai, Hyderabad, Kochi, and Coimbatore are driving demand for premium foods, health products, beauty and personal care, ready-to-cook foods, organic products, and quick-commerce purchases.

East India is gaining importance due to improving rural consumption, rising branded product penetration, and expansion of distribution networks in West Bengal, Odisha, Bihar, Jharkhand, and Assam. Although the region remains more price-sensitive, it provides strong long-term growth potential for economy packs, sachets, affordable nutrition, oral care, hair care, tea, biscuits, and household essentials.

Recent Developments

ITC Limited – July 25, 2025

In July 2025, ITC Limited announced a medium-term investment plan aimed at strengthening its presence across fast-moving consumer goods (FMCG), sustainable packaging, agri-business, and digital-enabled manufacturing operations. The investment strategy reflected the company's long-term commitment to expanding domestic manufacturing capacity while improving supply chain resilience and product availability across urban and rural markets. As part of this expansion, ITC confirmed the commissioning of eight new manufacturing facilities located across different regions of India, supporting higher production volumes and reducing logistics costs. The new facilities are expected to enhance capacity for packaged foods, personal care products, dairy, snacks, and paper-based sustainable packaging solutions.

Tata Consumer Products Limited – October 24, 2025

In October 2025, Life Insurance Corporation of India (LIC) increased its shareholding in Tata Consumer Products Limited to 8.64%, signaling growing institutional confidence in the company's long-term growth prospects and diversified consumer business strategy. The increased investment reflects positive market sentiment toward Tata Consumer's consistent financial performance, successful portfolio diversification, and expanding presence across beverages, packaged foods, health products, ready-to-cook meals, and premium consumer goods. Institutional investors typically increase holdings when they anticipate sustainable earnings growth, operational efficiency improvements, and long-term value creation, making LIC's investment a strong indicator of confidence in the company's strategic direction.

Indian FMCG Market Scope: Inquire before buying

| Indian FMCG Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 376.47 USD Billion |

| Forecast Period 2026-2034 CAGR: | 18.8% | Market Size in 2034: | 1774.51 USD Billion |

| Segments Covered: | by Product Type | Traditional Cigarettes Bidis Cigars Smokeless Tobacco E-Cigarettes & Vapes Heated Tobacco Products (HTPs) Nicotine Pouches Others |

|

| by Demographics | Generation Z (18–27 Years) Millennials (28–43 Years) Generation X (44–59 Years) Baby Boomers (60+ Years) |

||

| by Price Segment | Economy Mid-Range Premium Luxury |

||

| by Distribution Channel | Supermarkets & Hypermarkets Convenience Stores Tobacco Specialty Stores Online Retail Duty-Free Stores Others |

||

Key players/Competitors profiles covered in the Indian FMCG Market report from a strategic perspective

- ITC Limited

- Amul

- Bajaj Consumer Care Ltd.

- Britannia Industries Ltd.

- Coca-Cola India

- Colgate-Palmolive (India) Limited

- Dabur India Limited

- Emami Limited

- Godrej Consumer Products Limited

- Hindustan Unilever Limited (HUL)

- Marico Limited

- Nestlé India

- Parle Products Pvt. Ltd.

- Patanjali Ayurved Limited

- PepsiCo India

- Procter & Gamble (P&G)

- Reliance Industries Limited

- Tata Consumer Products Limited