Zero Trust Security Market by Authentication Type, Deployment Model, Solution Type, Industry Vertical and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

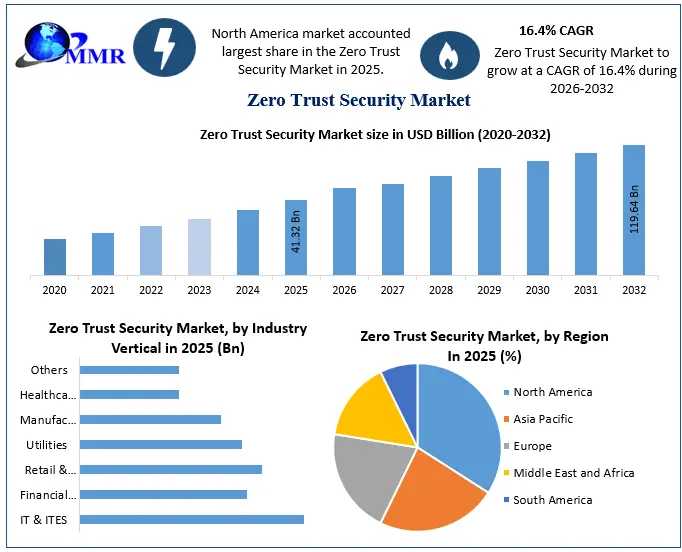

The Zero Trust Security Market size was valued at USD 41.32 Billion in 2025 and the total Zero Trust Security revenue is expected to grow at a CAGR of 16.4% from 2026 to 2032, reaching nearly USD 119.64 Billion by 2032.

Zero Trust Security Market Overview:

Zero Trust is a security framework requiring all users, whether in or outside the organization’s network, to be authenticated, authorized, and continuously validated for security configuration and posture before being granted or keeping access to applications and data. Zero Trust assumes that there is no traditional network edge; networks can be local, in the cloud, or a combination or hybrid with resources anywhere as well as workers in any location. The detailed and constructive formation of key drivers, opportunities, and unique segmentation outputs structural and optimistic data. Validated using primary as well as secondary research methodology and scope of the Global Zero Trust Security Market.

To know about the Research Methodology :- Request Free Sample Report

Zero Trust Security Market Competitive Landscapes:

Zero Trust Security Market Dynamics:

Zero Trust Security Market Growth Amid Remote Work Trends

The increase in remote work, intensified by the global pandemic, has exposed organizations to heightened cyber threats. The distributed nature of remote work, with employees accessing company resources from various locations and devices, poses challenges for traditional security models. Zero trust security has emerged as a solution to these challenges, operating on the fundamental principle of not automatically trusting anyone. This necessitates rigorous authentication and authorization for every user and device attempting to access company resources, significantly reducing the risk of unauthorized access and data breaches. The demand for zero trust security solutions has experienced a substantial surge as organizations prioritize securing remote access, contributing to the overall growth of the zero trust security market.

Balancing Security and User Experience in Zero Trust Security

While strict authentication measures are crucial for security, finding a balance to prevent user frustration and productivity issues is essential for the successful adoption of zero trust security. Organizations embracing this approach must prioritize user-friendly solutions with transparent access controls and intuitive interfaces. Education and training initiatives play a pivotal role in ensuring user acceptance of the zero trust model. A report by the National Institute of Standards and Technology (NIST) in March 2023 underscores the potential negative impact of overly strict authentication on user experience. The report recommends a risk-based approach to authentication, emphasizing the importance of striking a balance between robust security measures and positive user satisfaction.

Cloud Migration Opens New Avenues for Zero Trust Security

The ongoing trend of organizations migrating their infrastructure and applications to the cloud presents a promising opportunity for the zero trust security market. Traditional security measures based on perimeter defense become less effective in the cloud environment, necessitating a paradigm shift towards zero trust principles. Zero trust security seamlessly integrates with cloud migration strategies by providing granular access controls, continuous monitoring, and robust authentication mechanisms tailored for cloud resources. This ensures that only authenticated and authorized users can access cloud assets, effectively reducing the risk of unauthorized access and data breaches.

Beyond secure access controls, zero trust security solutions offer visibility and monitoring capabilities, addressing the distinct security challenges inherent in cloud environments. The increasing adoption of cloud-based services across industries creates substantial market potential for zero trust security solutions, allowing organizations to confidently embrace cloud migration while maintaining a strong security posture. This strategic alignment positions zero trust security as a key enabler for organizations seeking to secure their cloud environments and expand their market share in the evolving landscape of cybersecurity solutions.

Zero Trust Security Market Segment Analysis

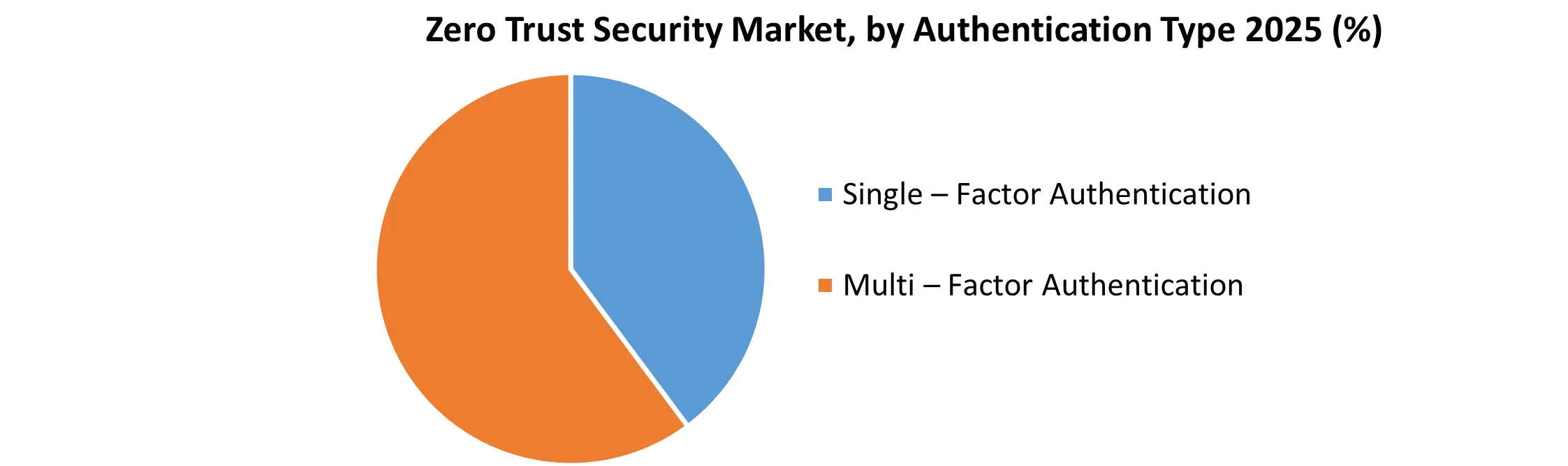

Authentication Type:

The Zero Trust Security market is characterized by its diverse nature, influenced by key segmentation factors, including authentication types, deployment models, solution types, and industry verticals. A thorough segment analysis offers a comprehensive view of the crucial dimensions within the Zero Trust Security market, providing insights into market share, regional segment growth, and detailed segment analysis. This method involves a single layer of user verification, typically through a username and password. While providing a fundamental level of security, it may prove insufficient for robust protection in the evolving threat landscape.

The market share for single-factor authentication is notable, especially in industries where a basic security layer suffices. MFA introduces an additional layer of security by requiring users to provide multiple forms of identification. This can include something the user knows (password), something the user has (security token), or something the user is (biometric data). MFA enhances security by reducing the risk of unauthorized access, addressing the need for heightened authentication. The market potential for MFA is growing as organizations prioritize enhanced security measures.

Deployment Model:

On-premises deployment involves implementing Zero Trust Security solutions within the organization's physical infrastructure. This model provides organizations with direct control over their security infrastructure but may require higher upfront investments in hardware and maintenance. Market share analysis indicates a significant presence of on-premises solutions, especially in industries with stringent data control requirements. Cloud-based deployment involves hosting Zero Trust Security solutions on cloud platforms.

This model offers flexibility, scalability, and accessibility from anywhere. As organizations increasingly adopt cloud services, cloud-based deployment becomes a strategic choice for Zero Trust Security solutions, aligning with modern IT trends. The market penetration of cloud-based solutions is expanding rapidly, driven by the advantages of scalability and accessibility.

Solution Type:

This solution focuses on securing the organization's network infrastructure, preventing unauthorized access, and ensuring the integrity of data in transit. Market segment analysis reveals a consistent demand for robust network security solutions. Involving measures to protect sensitive data, both at rest and in transit, to prevent data breaches and unauthorized disclosure. The market potential for data security solutions is significant, given the increasing concerns about data breaches. Concentrating on securing individual devices (endpoints) connected to the corporate network, such as computers, smartphones, and other devices. Endpoint security solutions hold a substantial market share, considering the proliferation of connected devices. This solution combines orchestration and automation to streamline security processes and improve incident response efficiency. SOAR solutions are gaining traction, with organizations recognizing the need for efficient incident response. Addressing the security of Application Programming Interfaces (APIs), ensuring secure communication and data exchange between software components.

The market share for API security solutions is growing as organizations increasingly rely on APIs for seamless software integration. Involves the use of advanced analytics to detect and respond to security threats by analyzing patterns and anomalies in data. Security analytics solutions play a crucial role in proactive threat detection and response. Encompasses the creation, enforcement, and management of security policies across the organization. Security policy management solutions are integral to maintaining a consistent and enforceable security posture. Includes additional specialized solutions that contribute to the overall Zero Trust Security framework, offering a comprehensive suite of security measures. The market for specialized solutions is evolving as organizations seek tailored approaches to unique security challenges.

Zero Trust Security Market Regional Analysis

The Zero Trust Security market unfolds diverse dynamics across North America, Europe, and Asia Pacific, influenced by regulatory frameworks, technological advancements, and the overall maturity of the IT landscape. A detailed analysis provides insights into the unique trends and opportunities specific to each region. In North America, the Zero Trust Security market undergoes robust growth propelled by a sophisticated IT infrastructure, stringent cybersecurity regulations, and a proactive stance in adopting advanced security measures. The United States takes center stage, contributing significantly to the market with substantial investments in cybersecurity.

The regional analysis indicates a mature market characterized by a high adoption rate, particularly evident among large enterprises in finance, technology, and healthcare. North America, especially the U.S., boasts well-defined and strictly enforced cybersecurity regulations, compelling organizations to invest in advanced security solutions like Zero Trust Security. This regulatory environment fosters a culture of compliance and security readiness. The region's proactive IT landscape, combined with a heightened awareness of cybersecurity threats, drives the adoption of cutting-edge security measures. Organizations exhibit a proactive approach to stay ahead of evolving threats. The prevalence of numerous large enterprises across diverse sectors contributes to the adoption of comprehensive Zero Trust Security solutions. Large enterprises, particularly in finance and technology, play a crucial role in driving market maturity.

The Zero Trust Security market in the United States experiences substantial regional growth, given the country's significant contributions to the overall market. With a sophisticated IT infrastructure and a proactive cybersecurity approach, the U.S. serves as a key driver in shaping the regional landscape. The market's expansion in the U.S. is further fueled by large enterprises, particularly in finance and technology, emphasizing the importance of stringent security measures. The U.S. holds a considerable share in the Zero Trust Security market, reflecting its dominance in cybersecurity investments and technology adoption. As organizations prioritize robust security measures to combat evolving cyber threats, the market share in the U.S. continues to grow. Large enterprises, in particular, contribute significantly to this share, recognizing the need for comprehensive Zero Trust Security solutions.

North America, encompassing the U.S. and other regions, presents immense potential for the Zero Trust Security market. The region's mature market, coupled with a proactive IT landscape and stringent cybersecurity regulations, creates a fertile ground for the widespread adoption of advanced security measures. The potential for market growth in North America is driven by the continuous emphasis on data protection, compliance, and the ever-evolving cybersecurity landscape.

Europe presents a robust presence in the Zero Trust Security market, emphasizing the strengthening of cybersecurity frameworks and addressing emerging threats. The European Union's stringent data protection regulations, such as GDPR, significantly influence the adoption of Zero Trust Security practices. The regional analysis showcases a diverse market landscape with a growing focus on securing critical infrastructure and sensitive data. The GDPR mandates stringent data protection measures, compelling organizations to implement Zero Trust Security solutions for compliance and safeguarding sensitive information. GDPR compliance is a key driver for the adoption of advanced security measures.

European nations prioritize the security of critical infrastructure, including utilities and transportation, contributing to the adoption of Zero Trust Security in these sectors. This emphasis aligns with the need for comprehensive security in vital areas. Cross-border collaborations and initiatives on cybersecurity enhance the overall cybersecurity posture in Europe. Such collaborative efforts foster the adoption of advanced security measures across national and organizational boundaries.

Zero Trust Security Market Competitive Landscape

Google LLC, announced its first commercial product based on the zero trust approach – BeyondCorp Remote Access. This product was aimed to help the employees’ access internal web applications from most of the devices, and from any location, without any Virtual Private Network. Blackberry Ltd., announced its new platform – Spark, with a new Unified End point Security (UES) layer, which can work with Blackberry Unified Endpoint Management (UEM), in order to deliver zero trust security. Palo Alto Networks, a cyber – security leader, announced its acquisition of PureSec – leader in server less security. This acquisition was done for extending the company’s Prisma cloud security strategic, and was expected to help the company to strengthen their ability to secure server less applications and hence deliver greater protections across multiple cloud environments.

In recent updates, Cisco, a prominent global player in networking technology, is steadfastly reinforcing its commitment to fortify partner marketing practices. The company is achieving this through a significant expansion of its Marketing Velocity brand, recognizing the central role of digital marketing in the B2B landscape. Cisco's strategic move involves consolidating its resources under the Marketing Velocity umbrella, presenting partners with a comprehensive program. With a vast network of over 62,000 partners worldwide, Cisco aims to empower partners in effectively reaching customers through transformative marketing activities.

The expanded initiative covers a spectrum of capabilities, ranging from elevating marketing practices to providing essential resources such as marketing funds and enablement tools for field activation. This comprehensive approach not only consolidates partner marketing resources but also integrates and enhances marketing practices, showcasing Cisco's unwavering dedication to accelerating its partners' marketing expertise and fostering success in the digital era.

In recent announcements, Akamai, a significant market share holder in cloud services, has introduced substantial enhancements to its Partner Program, aiming to drive growth for channel partners. These updates strategically focus on providing predictable income and simplifying the overall partner experience. One notable improvement includes offering additional pricing discounts for upfront deals, aligning financial incentives with the objectives of field sales professionals. The on boarding process for new channel partners has been streamlined and simplified, ensuring a quicker and more efficient integration into the Akamai Partner Program.

Akamai is also actively enhancing the overall partner experience through continuous improvements to the partner portal. Upcoming enhancements include facilitating easier registration and management of new opportunities, streamlining business planning processes, and increasing transparency of key metrics for more efficient quarterly business reviews. These developments are geared towards making the partner program more rewarding, predictable, and accessible for channel partners associated with Akamai.

Scope of Global Zero Trust Security Market: Inquire before buying

| Global Zero Trust Security Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 41.32 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 16.4% | Market Size in 2032: | US $ 119.64 Bn. |

| Segments Covered: | by Authentication Type | Single – Factor Authentication Multi – Factor Authentication |

|

| by Deployment Model | On Premises Cloud Based |

||

| by Solution Type | Network Security Data Security Endpoint Security Security Orchestration Automation & Response API Security Security Analytics Security Policy Management Others |

||

| by Industry Vertical | IT & ITES Financial & Insurance Retail & Trade Utilities Manufacturing Healthcare & Social Assistance Others |

||

Zero Trust Security Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Zero Trust Security Market Key Players:

North America:

1. Cisco Systems Inc.

2. Akamai Technologies

3. Palo Alto Networks

4. Okta Inc.

5. Check Point Software Technologies

6. Trend Micro Inc.

7. Symantec Corporation

8. FireEye Inc.

9. McAfee Corporation

10. Forcepoint

11. RSA Security

12. Centrify

13. Cyxtera Technologies

14. Sophos Group PLC

15. QNext Corporation

16. Google LLC

17. Microsoft Corporation

18. VMWare Inc.

19. Fortinet

20. Cloudflare Inc.

21. SonicWall

22. Varonis Systems

23. Pulse Secure

24. CrowdStrike Inc.

25. Proofpoint Inc.

26. Rapid7

27. F5 Networks Inc.

28. Zscaler Inc.

Europe:

1. Palo Alto Networks

2. Trend Micro Inc.

3. Symantec Corporation

4. Forcepoint

5. RSA Security

6. Sophos Group PLC

7. Centrify

8. Varonis Systems

9. Kaspersky Lab

10. ESET

11. Checkmarx

12. Darktrace

13. Mimecast

14. Bitdefender

Asia Pacific:

1. Trend Micro Inc.

2. Sophos Group PLC

3. QNext Corporation

4. Google LLC

5. Microsoft Corporation

6. VMWare Inc.

7. Fortinet

8. Cloudflare Inc.

9. SonicWall

10. Varonis Systems

11. Kaspersky Lab

12. ESET

13. NTT Security

14. Trend Micro Inc.

15. AhnLab

16. Kingsoft Corporation

Middle East:

1. Symantec Corporation

2. Forcepoint

3. RSA Security

4. Centrify

5. Sophos Group PLC

6. Varonis Systems

7. Kaspersky Lab

8. Darktrace

9. Mimecast

10. Bitdefender

11. F5 Networks Inc.

12. Zscaler Inc.

13. Fortinet

FAQs:

1. What is the Zero Trust Security market?

Ans: The Zero Trust Security market refers to the industry focused on cybersecurity solutions that assume no inherent trust, requiring strict verification for every user and device accessing networks and data.

2. What factors are driving the growth of the Zero Trust Security market?

Ans: The market is propelled by rising concerns for data security, increased remote workforce, and the need to address evolving cyber threats and multi-vector attacks.

3. How does Zero Trust Security mitigate the risks associated with remote work?

Ans: Zero Trust Security ensures that every user and device, regardless of location, undergoes strict authentication and authorization, reducing the risk of unauthorized access and data breaches in remote work scenarios.

4. What challenges does the Zero Trust Security market face?

Ans: The integration of new solutions, particularly during the market's early stages, faces challenges due to budgetary constraints, especially among small and medium-sized enterprises.

5. How does Zero Trust Security cater to different industry verticals?

Ans: Zero Trust Security offers tailored solutions for various industry verticals, including IT, finance, retail, utilities, manufacturing, healthcare, and others, addressing specific security needs and challenges in each sector.