Wind Turbine Blade Market Size by Blade Material, Type, Application, Industry Vertical and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

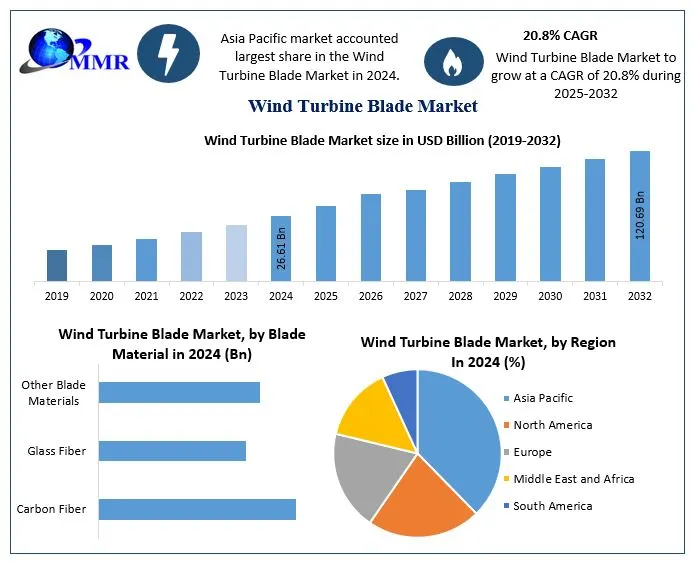

The Wind Turbine Blade Market size was valued at USD 26.61 Billion in 2024 and the total Wind Turbine Blade revenue is expected to grow at a CAGR of 20.8% from 2025 to 2032, reaching nearly USD 120.69 Billion.

Wind Turbine Blade Market Overview:

The wind is a free energy resource until governments charge it, but it is also a very unpredictable and unreliable source of electricity since its intensity and direction are continuously changing. So, to get the most out of the available wind energy, the wind turbine blade design must be of high performance. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Wind turbines must be huge and tall to create significant amounts of electricity, but to function efficiently, they must also be carefully built and manufactured, which makes them expensive. The majority of wind turbines built for energy generation have consisted of a two or three-bladed propeller moving around a horizontal axis. These propeller-like wind turbine blade designs transform wind energy into useful shaft power known as torque.

Wind turbine blades are designed to generate the most electricity from the wind while requiring the least amount of building. However, wind turbine blade makers are always striving to create a more efficient blade design. Constant advancements in wind blade design have resulted in new wind turbine designs that are more compact, quieter, and capable of generating more electricity from less wind. It's thought that by slightly bending the turbine blade, they may catch 5 to 10% more wind energy and function more efficiently in places with lower wind speeds.

Report Scope:

The report's objective is to provide stakeholders in the industry with a complete study of the Wind Turbine Blade market. The report analyses complex data in simple language and present the historical and current state of the industry, as well as anticipated market size and trends. The research examines all areas of the industry, including a detailed examination of important companies such as market leaders, followers, and new entrants.

The report includes a PORTER and PESTEL analysis, as well as the possible influence of market microeconomic aspects. External and internal elements that are expected to affect the organization positively or adversely have been studied, providing decision-makers with a clear future vision of the industry.

The report also helps in the comprehension of the market trends and structure by studying market segments and projecting the market size. The study is an investor's guide because of its clear depiction of competitive analysis of key competitors in the market by product, price, financial situation, product portfolio, growth plans, and geographical presence.

The data provides a thorough analysis of the rapid advances that are currently taking place across all industry sectors. Facts and figures, illustrations, and presentations are used to provide key data analysis for the historical period from 2019 to 2024. The report investigates the Wind Turbine Blade market's drivers, limitations, prospects, and barriers. This MMR report includes investor recommendations based on a thorough examination of the Wind Turbine Blade market's contemporary competitive scenario.

Research Methodology:

To analyze both secondary and primary data, the Bottom-Up Approach is utilized. Secondary data is gathered from nationalized and global data sources, annual and financial reports of significant market participants, press releases, etc. The primary data was gathered through interviews, surveys, expert and trained professional comments, etc. Data on recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, the influence of domestic and major & localized market players, changes in market regulations, and strategic market growth analysis are also included in the report.

Market Dynamics:

The rising concerns about global warming, environmental pollution, and energy security is a key drivers for the Wind Turbine Blade Market.

The Concerns about global warming, pollution, and energy security have increased interest in developing renewable and ecologically friendly energy sources such as wind, solar, hydropower, geothermal, hydrogen, and biomass as substitutes for fossil fuels. Wind energy has the potential to give appropriate answers to global climate change and energy problems. Wind power virtually eliminates emissions of CO 2, SO 2, NO x, and other toxic pollutants, as in typical coal-fuel power plants, or radioactive wastes in nuclear power plants. Wind energy decreases reliance on fossil fuels, which are subject to price and supply volatility, and so strengthens global energy security. Wind power has grown significantly during the last three decades all around the globe. In 2009, global yearly installed wind power capacity hit a new high of 37 GW, increasing total global wind capacity to 158 GW. Wind power, being the most promising renewable, clean, and stable energy source, is expected to play a considerably larger role in power generation during the forecast period.

Increased wind power generation benefits the wind turbine blade market.

Wind energy generation has become deeply established as a major form of power generating. Wind power capacity has expanded significantly around the globe in the recent decade, as wind turbines have gotten more powerful, efficient, and inexpensive to power producers. These factors will boost demand for wind turbine blades, which are a crucial component in wind power developments. Wind energy is a relatively huge single source (approximately 50%) of all global increases in power generation. In addition, Government policies that encourage the use of renewable energy resources to preserve environmental balance are also one of the major drivers for the market. Additionally, the lowering cost of wind energy generation is one of the primary factors responsible for the market's growth. The increase in investments in the supply of clean energy incentive schemes for renewable energy development is expected to be a significant driver driving the wind turbine blade materials market.

Wind Blades getting damaged during the power generations is a key restrain for the Wind Turbine Blade market growth.

Wind blades are key structural parts of wind turbines, yet they, like any other composite component, are susceptible to deterioration. Damage to the blades can cause unexpected structural failure, with considerable repair expenses. As a result, determining the source of damage is critical for preventing problems during the production, transportation, and operating phases. Wind blade damage can occur as a result of manufacturing faults, precipitation and debris, water penetration, fluctuating wind loads, operating mistakes, lightning strikes, and fire. To minimize or reduce injury to expensive wind turbine blades, early detection and mitigation strategies are essential.

Segment Analysis:

By Application, the Onshore Blade Segment held the largest market share of about xx% in 2024 and is expected to maintain its dominance at the end of the forecast period. Wind turbine original equipment manufacturers (OEMs) have reduced onshore wind turbine blade production capacity in industrialized nations during the last five years. Onshore blade production (a labor-intensive process) for markets outside of China is increasingly being established in nations with low labor costs that can supply a regional market or global demand cost-efficiently. This has resulted in a rise in exports from nations such as China, India, Mexico, and Turkey.

In the last five years, there have been significant changes in the onshore market, including declining turbine prices (due largely to the shift to auctions, which typically result in cheaper prices than policies such as feed-in tariff rates) and diversification of demand beyond traditional markets such as the EU. In response to cost challenges, OEMs reduced the number of products they offered, increased modularity (so that similar components could be utilized across numerous products), and moved toward bigger wind turbines and longer blades. These improvements enabled OEMs' onshore blade production to evolve since they were no longer required to create individual products for specific markets and could produce (or source) at higher numbers from a single site to gain economies of scale.

OEMs decreased substantially their onshore blade manufacturing footprint in several industrialized nations, shutting their least competitive factories and production lines, those producing outdated products (e.g., shorter blades), and/or those exclusively focused on supplying low-demand local markets. Between and February , at least a dozen onshore factories or manufacturing lines were shut down in the EU (especially in Denmark, Germany, and Spain), three in the US, and one in Canada. However, the majority of US and European OEMs maintain a manufacturing presence in one or more of these regions.

OEMs are increasingly obtaining blades from low-labor-cost countries, such as China, India, Mexico, and Turkey. Plants in these nations are frequently located near ports and are strategically positioned to service a regional or global market at a low cost. This gives OEMs the freedom to satisfy demand in a variety of regions and to source from several places based on which have the lowest landing costs. Brazil has historically been a key exporter and continues to provide blades across the globe. Sourcing from low-cost locations is done through in-house plants, multinational external suppliers (e.g., TPI Composites in the United States and GE subsidiary LM Wind Power in the United Kingdom), or external suppliers that manufacture primarily in one country (e.g., Chinese suppliers Aeolon and Zhuzhou Times New Material, Brazilian suppliers Aeris and Tecsis).

Wind Turbine Blade Market Regional Insights:

The APAC market held the largest market share of about xx% in 2024 for the Wind Turbine Blade market and is expected to grow significantly during the forecast period. The growing demand for renewable energy sources, the surge in demand for lightweight and high-strength materials used in the manufacture of various sections of wind turbines, and supporting government measures such as favorable regulations and wind power development programs are the major drivers for the Wind Turbine Blade Market during the forecast period. In addition, Factors such as decreased wind energy costs and increased investment in the wind power industry are expected to drive the Asia-Pacific wind turbine blade market during the forecast period.

However, issues such as the related high cost of transportation and the cost competitiveness of other clean energy sources such as solar power, hydropower, and so on, have the potential to restrict market growth throughout the forecast period. Over the forecast period, the global wind turbine blade market is expected to benefit from increased demand from rising economies such as China, India, and Brazil. Because of the increase in economic development and replacement costs associated with old blades, these regions have focused on revitalization through investment in up gradation or modification, resulting in significant investments by end-users across various industries, including the construction sector, and thus contributing to the overall market.

The growing utilization of wind turbines to generate renewable energy drives the global market growth. The rising number of nations such as the United States, Canada, and Germany investing in the installation of massive capacity as well as new projects with Wind turbine blade manufacturers/suppliers for productivity or higher efficiency is the primary driver driving this market. Europe is another important market that is expected to profit the highest during the forecast period. The European market outlook is linked to excellent environmental conditions and growing demand in numerous industries.

However, the wind turbine blade materials market in Europe is expected to rise rapidly as wind installation capacity grows faster than any other kind of power production in Europe. The European market is expected to grow rapidly due to rising demand for wind turbine blades in key European nations such as Germany, France, the United Kingdom, and Russia.

The North American market is also experiencing significant growth in the Wind Turbine Blade market during the forecast period. Growth in the North American area may be linked to increased demand for wind energy as well as an increase in government efforts promoting renewable energy sources such as wind power generation. Additionally, rising private-sector investment is expected to increase the regional market during the forecast period.

However, fluctuating crude oil prices may significantly affect economic growth, negatively impacting the wind turbine blade sector across the Americas area via a cost-price squeeze mechanism. The globally high initial investment required for installation and manufacture adds to the financial strain on end-users, raising the threshold limit of the region's wind turbine blade sector.

Wind Turbine Blade Market Scope: Inquire before buying

| Wind Turbine Blade Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 26.61 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 20.8 % | Market Size in 2032: | USD 120.69 Bn. |

| Segments Covered: | by Blade Material | Carbon Fiber Glass Fiber Other Blade Materials |

|

| by Type | <1.5 MW 1.5 MW 1.5-2.0 MW 2.0 MW 2.0-3.0 MW 3.0 MW 3.0-5.0 MW > 5.0 MW |

||

| by Application | Offshore Wind Blade Onshore Wind Blade |

||

| by Industry Vertical | Energy Plastics Composites Other |

||

Wind Turbine Blade Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest)

South America (Brazil, Argetina and Rest of South America)

Wind Turbine Blade Market Key Players

1. LM Wind Power

2. Vestas Wind Systems A/S

3. Enercon GmbH

4. Tecsis

5. Siemens Gamesa Renewable Energy S.A

6. CARBON ROTEC

7. Acciona

8. Nordex SE

9. Inox Wind

10. Suzlon Energy Limited

11. TPI Composites

12. Zhongfu Lianzhong

13. Avic

14. Sinoma

15. TMT

16. New United

17. United power

18. Mingyang

19. XEMC New Energy

20. DEC

21. Haizhuang

22. Wanyuan

23. SANY

FAQs:

1. Which is the potential market for the Wind Turbine Blade in terms of the region?

Ans. The Asia Pacific is the potential market for the Wind Turbine Blade in terms of the region.

2. What are the opportunities for new market entrants?

Ans. The key opportunity in the market is new initiatives from governments that provide funding for Wind Turbine Blades.

3. What is expected to drive the growth of the Wind Turbine Blade market in the forecast period?

Ans. The rising concerns about global warming, environmental pollution, and energy security is a key drivers for the Wind Turbine Blade Market.

4. What was the Global Wind Turbine Blade Market size in 2024?

Ans: The Global Wind Turbine Blade Market size was USD 26.61 Billion in 2024.

5. What segments are covered in the Wind Turbine Blade Market report?

Ans. The segments covered are Blade Material, Type, Application, Industry Vertical, and Region.