Thermoplastic Pipe Market Size by Product Type, Polymer Type, End-User Industry, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

Thermoplastic Pipe Market size was valued at USD 3.51 Bn. in 2023 and the total Thermoplastic Pipe revenue is expected to grow by 4.8 % from 2024 to 2030, reaching nearly USD 4.87 Bn.

Market Overview:

Thermoplastic pipes are plastic pipes manufactured from a polymer substance generated in vast quantities from plants and altered chemically. This type of pipe is gaining favor in oil and gas production since it does not rust and requires less maintenance than metal pipes. Aside from combating corrosion, pipes are an important choice in many piping and plumbing systems due to their numerous benefits. Polyethylene and high-density polyethylene (HDPE), polypropylene (PP), poly (vinyl chloride) (PVC), and polystyrene are some of the most significant thermoplastics. These polymers have a wide range of structural uses, including wire and light-duty utility.

Polyvinyl Chloride (PVC) is a widely used thermoplastic polymer in a variety of sectors. PVC pipe is the favored option of fabricators and custom houses because of its remarkable and constant quality and uniform features. It is very resistant to acids, alkalis, alcohols, and a wide range of other corrosive substances. PVC systems are lightweight, flexible, and durable, with excellent corrosion resistance. Because of these and other features of a high-grade engineered thermoplastic, the savings in the original installation and ongoing maintenance expenses can be significant. PVC pipe is appropriate for corrosive fluid transfer in a variety of applications such as chemical distribution and drainage, water and wastewater treatment, service pipes, irrigation systems, garbage collecting, and many more commercial applications.

The increasing use of thermoplastic composite pipes and reinforced thermoplastic pipes in offshore and onshore production activities, as well as the increasing use of thermoplastic pipes across sectors such as oil and gas, chemical, mining and dredging, and municipal, as well as applications in deep water and ultra-deepwater, are the major factors driving the market's rapid growth. As a result of this, growth in the number of applications for thermoplastic pipes with increased characteristics would give attractive chances for the market to develop rapidly. Higher production costs, as a result of problems in the large-scale manufacture of thermoplastic composite pipes, may affect market growth.

To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

Thermoplastic Pipe Market Dynamics:

Increasing adoption in renewable energy and the oil and gas industry

The increased focus on generating renewable energy resources may increase the global demand for thermoplastic pipes. Its greater adaptability/ flexibility, lightness, and anti-corrosive qualities increase consumer interest in the product. It helps businesses to cut expenses while increasing productivity. Additionally, increased pipe use in the oil and gas industry is expected to boost industry growth. Strohm, for example, secured a contract with the oil and gas industry in Western Australia.

Besides that, its lower maintenance costs and longer lifespan are expected to increase its appeal across a variety of manufacturers. However, the pipe's capacity to tolerate high pressures and temperatures is expected to enhance its acceptance. These reasons would drive the thermoplastic pipe market during the forecast period.

Increased use of thermoplastic composite pipes (TCPs) in industrial operations

Steel is a fundamental material used in the oil and gas sector to manufacture a range of tubes and pipes. Steel is still utilized extensively in the onshore sector for goods like as coiled tubing and flow lines. Thermoplastic composites, on the other hand, as a greater alternative to steel, are predominantly utilized in offshore applications such as chemical injection pipelines and risers. Its features, including wear and corrosion resistance, increased stiffness, and strength in response to temperature variations and stress deformation, make it ideal for underwater applications.

Given the rising importance of deep and ultra-deepwater oil and gas production and exploration operations, offshore drilling and production activities are expected to expand more rapidly than onshore activities during the forecast period. As a result, the use of thermoplastic composites in offshore goods such as flowlines, umbilicals, and risers is expected to strengthen the thermoplastic pipe market in the oil and gas sector.

Reinforced thermoplastic pipes (RTP), on the other hand, are utilized in the oil and gas sector to replace medium-pressure steel pipes. Several major businesses that are approved for international standards develop pipes that can withstand pressures of up to 450 bar or 6527 psi and can be utilized for onshore applications. Additionally, thermoset-based composite elements are used in these entirely plastic pipes, making them perfect for onshore applications.

Expensive high-grade thermoplastic composite pipes restraining the market growth

Thermoplastic pipes generally manufactured from designing and building thermoplastic grades such as polyethylene (PE) and polyvinyl chloride (PVC) have been used extensively because of their affordability and superior chemical high resistance. Higher grades of thermoplastics, such as polyether ether ketone (PEEK), have limited usage in seals and wirelines due to their high cost.

These pipes have substantial raw material and fabrication costs, but they have strong resistance properties, low flammability, and minimal emission of smoke and harmful gases. When compared to steel, composite pipes constructed of PEEK or polyphenylene sulfide (PPS) cost 20-100 times more, making their use in goods such as pipes impracticable, and thus becoming the most prevalent restriction to the thermoplastic pipe industry.

Growing demand for thermoplastics pipes for gas distribution

The adoption of thermoplastic pipeline systems for gas distribution has been a huge success, providing gas engineers with a long-lasting asset that can outlast steel and iron systems. These materials, particularly polyethylene, have become the main option for low-pressure gas systems up to 10 bar, resolving metal systems' corrosion and reliability difficulties.

However, it is unlikely that plastic material research alone could result in a large rise in pressure rating. Future development would most likely focus on multilayer and composite pipe constructions to meet specific application needs and to raise pressure ratings, allowing usage in medium and even high-pressure gas distribution pipes.

Large-scale manufacturing of thermoplastic composite pipes is challenging

Fabricators of thermoplastic composite pipes for the oil and gas sector must typically get raw materials (polymer) directly from manufacturers to meet the operating requirements of oil firms and the quality of material given by suppliers. Thermoplastic composite pipes are customizable goods that must be modified according to end-use circumstances such as pressure, temperature, and corrosion.

As a result, the alterations are often in polymer composition or processing conditions, which can only be carried out with tight cooperation between polymer producers and pipe fabricators. This standardization limitation makes large-scale manufacture of composite pipes challenging, contributing to the overall high cost of thermoplastic pipes.

Thermoplastic Pipe Market Segment Analysis:

By Product Type, the Reinforced thermoplastic pipe (RTP) segment dominated the market with the highest market share in 2023. For high-pressure applications, reinforced thermoplastic pipe (RTP) is widely used as an option for steel pipelines. The material is relatively new to the gas sector, but it has been tested and authorized for oil, gas, and water applications at pressures approaching or surpassing 100 bar throughout the Middle East and Europe (pressure rating depends on fluid, temperature, safety factors, and pipe construction).

Reinforced Thermoplastic Pipe (RTP) is a spoolable high-pressure pipeline system that blends high-performing materials with high-strength reinforcements in a novel structure. This design is ideally suited to a wide range of applications. RTP has been primarily used in the upstream oil and gas industry for a variety of applications including oil collection, gas gathering, water injection, and water disposal. In Canada, RTP has also been deployed in eleven gas distribution applications.

Spoolable reinforced plastic line pipes (RTPs) have been widely used in the onshore oil and gas industry, such as oil and gas gathering and transportation, high-pressure alcohol injection, water injection, sewage treatment, and other fields, due to a variety of advantages such as good flexibility, few joints, long single length, lightweight, easy installation, and so on. However, due to the lack of a clear standard specification of the limit operating properties for RTPs, three common failure modes, namely tensile, flexure, and torsion, frequently occur in terrain changes, construction operations, and subsequent application, which has a significant impact on the use of RTPs.

The use of high-performance glass, carbon, or aramid fibers for reinforcing polymers also increases pipeline-building opportunities. For many years, glass-fiber-reinforced plastic pipes have been utilized in chemical facilities to transport extremely corrosive fluids. When generating natural gas and oil from deep sea areas, reinforced plastic pipes are also employed as flexible risers. In each situation, items are custom designed to fit the application's exact needs. Wrapping procedures create pipes with a huge number of distinct layers.

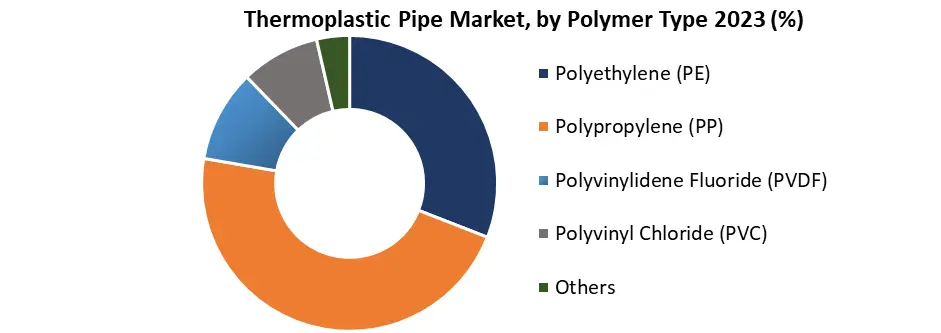

By Polymer Type, the polyethylene (PE) segment held the largest market in 2023 and is expected to grow substantially at a CAGR of about 4.3% during the forecast period. PE has evolved into one of the most frequently used and recognizable thermoplastic materials on the planet. The variety of uses and applications for this one-of-a-kind plastic substance demonstrates its adaptability. PE was first used as a rubber alternative in electrical insulation. PE has now become one of the most frequently used thermoplastics on the planet. Modern PE resins are highly developed for far more demanding applications such as pressure-rated gas and water pipe, landfill membranes, automobile fuel tanks, and other high-strength applications.

With over 90% utilization in North America today, polyethylene gas pipes are the primary natural gas distribution pipeline product. Polyethylene gas pipes are lightweight, non-corrosive, and easy to install using heat fusion or mechanical couplings. PE pipes have shown to be trustworthy and durable for these reasons, and they have been in use. Plumbing supply businesses and different hardware merchants sell PE pipes and fittings throughout the United States and Canada. In general, PE pipe is less costly than metallic pipeline materials. PE is a thermoplastic, which means it is a polymeric material that can be softened and molded into usable shapes using heat and pressure and hardens when cooled. PE belongs to the polyolefins family, which includes polypropylene. Polyolefins, as a class of materials, have low water absorption, moderate to low gas permeability, high toughness and flexibility at low temperatures, and low heat resistance. PE plastics provide flexible yet robust goods with great chemical resistance.

PE is a thermoplastic, which means it is a polymeric material that can be softened and molded into usable shapes using heat and pressure and hardens when cooled. PE belongs to the polyolefins family, which includes polypropylene. Polyolefins, as a class of materials, have low water absorption, moderate to low gas permeability, high toughness and flexibility at low temperatures, and low heat resistance. PE plastics provide flexible yet robust goods with great chemical resistance.

As a pipeline material, PE pipe has various characteristics such as lightweight, flexibility, chemical resistance, overall toughness, and longevity. Because of these advantages, it is a suitable pipe material for a wide range of applications, including potable water service or distribution lines, natural gas distribution, lawn sprinklers, sewers, garbage disposal, and drainage lines. Most common substances are not harmful to PE materials. Polyethylene may be utilized at low temperatures without becoming brittle. As a result, low-temperature heat transfer applications such as radiant floor heating, snow melting, ice rinks, and geothermal ground source heat pump pipes are common uses for specific PE piping formulations. These properties drive the segment growth during the forecast period.

Thermoplastic Pipe Market Regional Insights:

The Asia-Pacific regional market held the largest revenue share and dominated the market in 2023. This area is expected to maintain its dominance at the end of the forecast period, with a CAGR of 4.6%. Growing urbanization and infrastructure development have resulted in the utility industry adopting cost-effective transportation solutions, increasing market demand. Additionally, this has increased the motivation for thermoplastic pipe manufacturers to transition to this pipe.

Countries throughout Asia are stepping up efforts to gain access to drinkable water and sewage infrastructure, creating major prospects for the plastic pipe industry. Plastic pipe has benefits over other pipe materials due to its low cost and simplicity of installation. Additionally, continuing demand for polyvinyl chloride (PVC) in India and rising safety concerns in China are expected to drive regional thermoplastic market growth.

Glass fiber reinforced thermosetting pipes (GRP), anticorrosion plastic alloy composite pipes, steel skeleton reinforced polyethylene composite pipes, and spoolable reinforced plastic pipes are now the most common nonmetallic and composite pipes utilized in China's onshore oilfield systems (RTPs). RTPs are extensively used in oil and gas sectors because of their outstanding flexibility, great impact resistance, few joints, lightweight, cheap transportation cost, rapid and easy installation, and so on.

It has recently become China's fastest-growing non-metallic composite pipe. RTPs are primarily used for collecting and transporting oil and gas, high-pressure alcohol injection, oilfield water injection, sewage treatment, and other applications. RTPs have been tried in gas transportation (mixed oil and gas transportation), downhole water injection, and other sectors since 2011. As a result, the use of RTP products in China is evolving toward serialization and diversity.

The North American market is expected to grow substantially during the forecast period. Plastic pipes and fittings have been used effectively for a wide range of pipeline applications in North America for over 60 years. In specialty pipe, tubing, and fittings applications, thermoplastic and fluoropolymer materials, as well as thermosetting materials, are employed. The major two thermoplastic materials utilized for specific pipe and fittings applications are polyvinyl chloride (PVC) and high-density polyethylene (HDPE), which account for more than 90% of the overall market.

Plastic pipe consumption in North America has increased dramatically during the previous 40 years. PVC pipe is commonly used for potable water pipes, sanitary and storm sewer pipes, drain-waste-and-vent plumbing pipes, and electrical conduits. Polyethylene pipe is widely used in land drainage, gas distribution, telecommunications conduit, ground-coupled heat pump piping, and maritime applications. For hot water pipes and high-temperature industrial applications, many piping products are utilized.

Corrosion and other environmental factors represent a significant concern to North America's buried pipe system. According to a study conducted by the Federal Highway Administration (FHWA), corrosion accounts for more than $36 billion in the yearly loss in water and sewage systems across the United States. Polyvinyl chloride (PVC), a thermoplastic substance, is now the most extensively used material in water and sewage systems in the United States and Canada.

In Europe, the transformation to sustainable power and achieving climate neutrality by 2050 has increased market demand throughout the country. For example, the European Union Green Deal has identified hydrogen as a key technology for achieving climate neutrality in Europe by utilizing green hydrogen and utilizing the existing plastic pipe network to deliver hydrogen fuel to a wide range of industries such as industrial processes, gas for households, transportation fuels, etc.

The considerable growth in investment in the oil and natural gas industry is expected to strengthen markets in Latin America. Latin American countries such as Argentina, Brazil, and Ecuador have significantly increased hydrocarbon output and reserves. This opens up the potential of a new wave of resource in conveying it.

Much of the demand for these pipes in the Middle East and Africa is expected to be driven by the building and construction industry. In GCC nations, thermoplastic pipes are especially popular in sewage applications and have the largest market share. Materials such as PVC and PE are utilized in potable water pipes and are widely available in the area due to the abundant supply and consequent ease of access to high-density polyethylene.

Thermoplastic Pipe Market Scope: Inquire before buying

| Thermoplastic Pipe Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 3.51 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 4.8% | Market Size in 2030: | US $ 4.87 Bn. |

| Segments Covered: | by Product Type | Reinforced Thermoplastic Pipes (RTP) Thermoplastic Composite Pipes (TCP) |

|

| by Polymer Type | Polyethylene (PE) Polypropylene (PP) Polyvinylidene Fluoride (PVDF) Polyvinyl Chloride (PVC) Others |

||

| by End-User Industry | Oil & Gas Water & Wastewater Mining & Dredging Utilities & Renewables |

||

| by Application | Onshore Offshore |

||

Thermoplastic Pipe Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Thermoplastic Pipe Market, Key Players are

1. Advanced Drainage Systems Inc. (US)

2. Chevron Phillips Chemical (US)

3. National Oilwell Varco, L.P. (US)

4. Aetna Plastics Corporation. (US)

5. Baker Hughes (U.S.)

6. Exxon Mobil (U.S.)

7. Polyflow, LLC (U.S.)

8. Aetna Plastics Corp. (U.S.)

9. IPEX Inc. (Canada)

10. Shawcor (Canada)

11. Magma Global (U.K.)

12. Plastichem Limited (U.K.)

13. PES.TEC (Germany)

14. FRANK GmbH (Germany)

15. Prysmian Group (Italy)

16. Saudi Arabian Amiantit (Saudi Arabia)

17. Georg Fischer Piping Systems Ltd. (Switzerland)

18. Uponor Corporation (Finland)

19. KWH Group (Finland)

20. Cosmoplast (UAE)

21. AGRU Kunststofftechnik Gesellschaft M.B.H (Austria)

22. Wienerberger (Austria)

23. Wienerberger (Austria)

24. Finolex Industries Ltd. (India)

25. Sasol (South Africa)

26. Sibur (Russia)

27. Sekisui Industrial Piping Co., Ltd (Taiwan)

FAQs:

1. Which is the potential market for the Thermoplastic Pipe in terms of the region?

Ans. The Asia-Pacific is the potential market for Thermoplastic Pipe in terms of the region

2. What are the opportunities for new market entrants?

Ans. The key opportunity in the market is the Growing demand for thermoplastics pipes for gas distribution.

3. What is expected to drive the growth of the Thermoplastic Pipe market in the forecast period?

Ans. A major driver in the Thermoplastic Pipe market is the Increasing adoption of renewable energy and the oil and gas industry.

4. What is the projected market size & growth rate of the Thermoplastic Pipe Market?

Ans. Thermoplastic Pipe Market size was valued at USD 3.51 Bn. in 2023 and the total Thermoplastic Pipe revenue is expected to grow by 4.8% from 2024 to 2030, reaching nearly USD 4.87 Bn.

5. What segments are covered in the Thermoplastic Pipe Market report?

Ans. The segments covered are Product Type, Polymer Type, End-User Industry, Application, and Region.