Software Defined Infrastructure Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

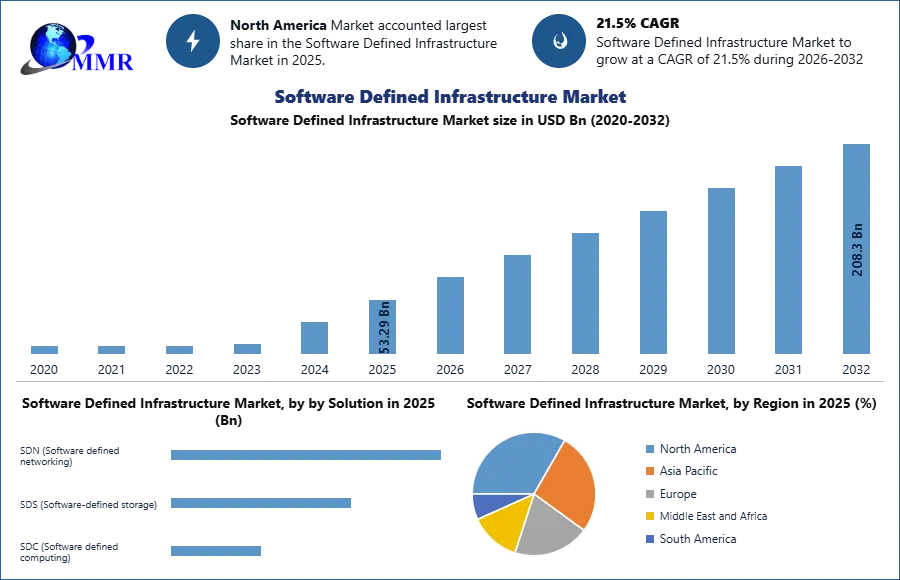

Global Software Defined Infrastructure Market was valued at USD 53.29 Bn in 2025 and is expected to reach USD208.3 Bn by 2032, growing at a CAGR of 21.5% during the forecast period.

Software-defined infrastructure (SDI) refers to managing IT infrastructure through software, essentially treating computing, storage, and networking resources like the software itself.

Example: Leading cloud providers like Amazon Web Services, Microsoft Azure, and Google Cloud Platform support the Software Defined Infrastructure Market.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The Software Defined Infrastructure Market Research Report 2025 Presents an Extensive Analysis of Market Dynamics, Competitive Landscape and Emerging Trends, By Regional Outlook and Forecast, 2025 - 2032. Our latest research report aims to provide valuable insights encompassing critical elements such as market size, market share, CAGR status, PESTEL & SWOT analysis, Porter’s 5 Forces, historical assessment, growth prospects, industry drivers and constraints, opportunities, and challenges, market revenue, and segmentation.

The demand for advanced IT infrastructure, and efficient data center management drives the Software Defined Infrastructure Market by automating tasks and freeing up IT staff for strategic initiatives. The top import-export software sources globally are the United States, Vietnam, and Germany.

Major companies in the Software Defined Infrastructure Market include Cisco Systems Inc., IBM Corporation, Hitachi Ltd., Huawei, Microsoft Corporation, and NEC Corporation among others. In the software-defined infrastructure market concentration highlights the prominence of key players and the competitive landscape driving innovation and development.

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 02 March 2026 | Broadcom Inc. | Broadcom unveiled the VMware Telco Cloud Platform 9, a unified AI-native private cloud platform designed for sovereign-ready telco infrastructure. | The update drives 40% cumulative TCO savings and introduces GPU-as-a-Service, enabling telecom operators to scale AI workloads with high hardware efficiency. |

| 24 February 2026 | Hewlett Packard Enterprise (HPE) | HPE launched Cloud Ops Software, a unified operational foundation to modernize private clouds and reduce reliance on expensive legacy hypervisors. | This solution consolidates virtualization and container management, helping service providers lower risk and accelerate the rollout of AI-driven managed services. |

| 11 February 2026 | Cisco Systems, Inc. | Cisco introduced AgenticOps innovations across its networking and observability portfolio to automate lifecycle governance for AI infrastructure. | The integration allows IT teams to manage distributed AI fabrics more efficiently, reducing complexity in gigawatt-scale data center deployments. |

| 02 December 2025 | ING / Broadcom Inc. | ING selected VMware Cloud Foundation (VCF) 9.0 as its strategic platform for private cloud modernization across its global financial operations. | This deployment enables global workload mobility and strengthens sovereign infrastructure compliance for multinational digital banking. |

| 17 November 2025 | Dell Technologies | Dell expanded its AI Factory portfolio, announcing that PowerScale storage would be available as an independent software license for PowerEdge servers. | The software-defined storage shift offers cloud providers greater flexibility and automated response capabilities for high-density AI training clusters. |

| 26 August 2025 | NVIDIA / Broadcom | Broadcom and NVIDIA partnered to integrate NVIDIA AI technology directly into the VMware Cloud Foundation stack. | The collaboration empowers enterprises to scale next-generation AI models on cutting-edge servers while maintaining private cloud security and control. |

Asia Pacific is the fastest-growing region in the Software Defined Infrastructure Market with a large market share of about 20.7 % in 2023 and is expected to grow at a CAGR of 21.4 % during the forecast period and maintain its dominance by 2030. The region is the fastest growing because With the rising internet usage, more users and businesses are coming online, creating a demand for efficient data management solutions. Significant economic growth is occurring in countries like China and India, which is driving up expenses in IT infrastructure.

Software Defined Infrastructure Market Dynamics:

Growing Demand for Cloud-Based Services and Mobility

The software-defined infrastructure market is growing because of the increasing demand for flexibility, scalability, and efficiency in modern IT environments. Businesses increasingly depend on cloud-based applications and services for data storage, program execution, and collaboration. This modification requires a flexible and scalable IT infrastructure, which SDI delivers effectively.

The growing demand for cloud-based services and mobility is redesigning the landscape of modern IT infrastructure. Businesses are adopting cloud solutions to improve their agility, scalability, and cost-effectiveness while meeting the growing need for remote access and mobility. Cloud-based services offer flexible deployment options that enable organizations to scale resources effortlessly, access data from any location, and support distributed workforces. The development represents a change toward an IT environment that is more dynamic and adaptive, where cloud technologies enable companies to compete, create, and work together in a constantly changing digital world. Data integration platforms streamline repetitive processes like provisioning, setup, and enhancement, reducing manual involvement and decreasing human mistakes. The development of the software-defined infrastructure industry is boosted by increasing network complexity, fluctuating traffic patterns, and server virtualization.

Software Defined Infrastructure Market Restraints:

Implementing Software Defined Infrastructure solutions often involves integrating various technologies and components, which is complex and time-consuming. Organizations face challenges in transitioning from old infrastructure to security, mostly because they lack the required knowledge or assets.

Security concerns are a major challenge in the Software Defined Infrastructure market because of the centralized control that is inherent in SDN architectures. Centralizing control functions leads to a single point of failure, making networks susceptible to targeted attacks or system failures. It is essential to protect the control plane against unauthorized access and cruel activities, which lead to unauthorized manipulation of network resources. It is essential to implement strong authentication methods, encryption protocols, and ongoing monitoring to safeguard the integrity, confidentiality, and accessibility of data in the SDN framework.

Software Defined Infrastructure Market Segment Analysis:

Based on the Solution, the SDN segment holds the largest market share of about 42.4% in the Software Defined Infrastructure Market in 2025. According to the MMR analysis, the segment is expected to grow at a CAGR of 21.4 % during the forecast period and maintain its dominance till 2032. The SDN (software-defined networking) segment is dominating because of earlier adoption and established presence in data centers. This technology separates the control plane (network intelligence) from the data plane (physical network devices) allowing for programmable and centralized network management.

Based on the End users, Retail Enterprises hold the largest market share in the Software Defined Infrastructure Market in 2025 and are expected to maintain their dominance till 2032. Retail enterprises need efficient and scalable solutions to manage huge massive data volumes, so the Software-defined infrastructure helps faster application distribution and IT infrastructure adaptation to changing business needs. Infrastructure costs become decreased by the efficient use of resources through software-defined infrastructure. The Telecom & IT service providers are experiencing significant growth because of cloud adoption as well as Network virtualization. Telecom companies influence Software-defined infrastructure for network function virtualization (NFV) and software-defined wide-area networks (SD-WAN).

| Software Defined Infrastructure Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 53.29 USD Bn |

| Forecast Period 2026-2032 CAGR: | 21.5% | Market Size in 2032: | 208.3 USD Bn |

| Segments Covered: | by Solution | SDN (Software defined networking) SDS (Software-defined storage) SDC (Software defined computing) |

|

| by Service | Managed Service Consulting Service Integration Deployment service |

||

| by Deployment Mode | On-Premises Cloud Hybrid |

||

| by Enterprise Size | Small & Medium Enterprises (SMEs) Large Enterprises |

||

| by End Users | Retail Telecom & IT Manufacturing Healthcare Others |

||

Software Defined Infrastructure Market of Regional Analysis:

North America dominates the Software Defined Infrastructure Market, which holds the largest market share accounting for 34.5% in 2025, the region is expected to grow during the forecast period and maintain its dominance by 2032. North America is a dominating region thanks to the early adoption of advanced technologies, because of their advanced IT infrastructures, countries like the US and Canada are more inclined towards implementing innovative technologies like SDI. North America is the leading region owing to the presence of top key players like Microsoft, IBM, Dell Technologies, and Cisco are headquartered in North America. So, a large base of technology companies as well as a matured IT market is available. The proximity of belonging creates a strong environment for SDI solution research, development, and implementation. North America leads the software-defined market as the top-selling region, offering a wide range of innovative solutions and services.

Some companies in North America are actively working on digital transformation projects. SDI's ability to provide agility, flexibility, and scalability in IT environments aligns with these goals. Significant investments in research and development have boosted North America to the lead of the software-defined infrastructure market. The software-defined market in the region is heavily influenced by market concentration, which is displayed by the strong infrastructure and technological advancements.

These regions including Latin America, the Middle East, and Africa, are expected to show promising growth potential owing to increasing IT adoption and government investments in infrastructure development.

Competitive Landscape for the Software Defined Infrastructure Market:

A key Company's strategy is its constant commitment to research and development (R&D) to maintain a leading position in technological development. The competitive landscape of the Software Defined Infrastructure Market includes a mix of established companies focusing on research and development to enhance efficiency and performance. Product launches have been an important strategic step for the major players in theMarket to remain competitive in the global market. The leading companies are adopting strategies such as acquisition, agreement, growth, partnership, contracts, and product launches to strengthen their market position.

To improve their products and strengthen their market position, key players in the global market focus on introducing improved solutions and services.

1. In November 2022, HPE and VMware announced a partnership to provide an integrated hybrid cloud experience. This collaboration combines HPE Green Lake and VMware Cloud to deliver a fully integrated solution with a simple pay-as-you-go hybrid cloud consumption model.

2. In August 2022, Arista Networks acquired Pluribus Networks, a unified cloud network company that develops unified cloud networking technology.

3. In March 2022, Nokia was chosen to work with Vodafone on the evolution of the software-defined network manager and controller (SDN-M&C) services for the company's multi-access fixed network technology.

4. In August 2023, VMware and AWS teamed up to bring VMware's enterprise-class software-defined data center software to the AWS Cloud's dedicated, elastic, bare-metal infrastructure, delivered as an on-demand service.

5. In February 2023, BICS deployed Nokia's SDN (software-defined networking) controller to automate optimal traffic routing on the network, which the company said would improve overall network performance.

Software Defined Infrastructure Market Scope: Inquiry Before Buying

Software Defined Infrastructure Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players /Competitor Profiles Covered in the Global Software Defined Infrastructure Market

Report from a Strategic Perspective.

- Cisco Systems

- VMware

- Microsoft

- IBM

- Hewlett Packard Enterprise

- Dell Technologies

- Oracle

- Amazon Web Services

- Google Cloud

- Huawei Technologies

- Nutaniх

- Red Hat

- Citrix Systems

- NetApp

- Fujitsu

- Hitachi Vantara

- Lenovo

- Arista Networks

- Juniper Networks

- Extreme Networks

- NEC Corporation

- Intel

- Ciena

- Broadcom

- Scale Computing