Sack Kraft Paper Market - Industry Structure Evaluation, Demand Drivers Analysis, Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2032

Overview

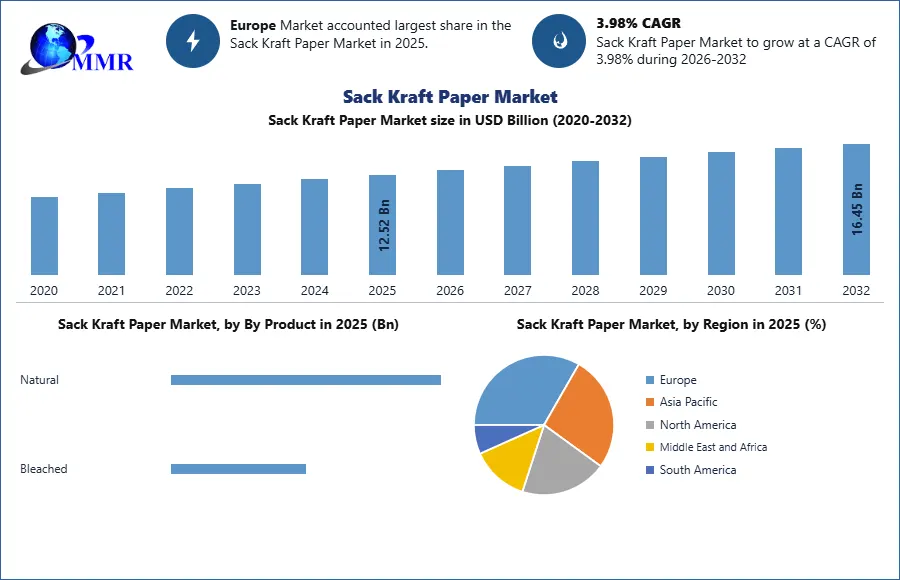

Global Sack Kraft Paper Market size was valued at USD 12.52 Bn. in 2025 and the total Sack Kraft Paper revenue is expected to grow by 3.98 % from 2026 to 2032, reaching nearly USD 16.45 Bn. by 2032.

Sack Kraft Paper Market Overview

Sack kraft paper is a porous kraft paper with high elasticity and high tear resistance, designed for packaging products with high demands for strength and durability. The global Sack Kraft Paper market is experiencing steady growth owing to the increasing demand for sustainable and eco-friendly packaging solutions across diverse industries. With a focus on reducing plastic waste and adopting recyclable materials, sack Kraft paper has emerged as an attractive alternative for packaging applications. The rise in e-commerce activities and the growing popularity of ready-to-eat meals have further boosted the demand for sack Kraft paper, as it ensures safe and hygienic packaging of products. The sack Kraft paper market includes a wide range of industries, including construction, agriculture, chemical, food, and others. It includes various paper grades, such as brown and bleached, as well as different weight categories, catering to the specific needs of end-users.

Rising environmental awareness and stringent regulations on plastic usage are driving the shift towards sustainable packaging solutions, promoting the adoption of sack Kraft paper. Market leaders doing advancements in product development, for instance, Mondi invests USD 439.14 million in a new kraft paper machine at Štětí mill, meeting the demand for eco-friendly packaging. This investment bolsters Mondi's Paper Bags business growth and is part of a USD 1.10 billion expansionary capital investment program to accelerate sustainable packaging growth.

Sack Kraft Paper Market Scope and Research Methodology

The Sack Kraft Paper Market report offers a thorough market evaluation for the forecast period. It examines patterns and factors shaping the market, including drivers, constraints, opportunities, and challenges. The report also provides expected revenue growth for the Sack Kraft Paper Market during the forecast period. The Sack Kraft Paper Market research analyses major applications, business strategies, and influencing factors. The report examines market trends, volume, cost, share, supply and demand, and utilises methods like SWOT and PESTLE analysis. Primary research resources include databases and surveys. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Sack Kraft Paper Market Dynamics:

Sack Kraft Paper Market Drivers

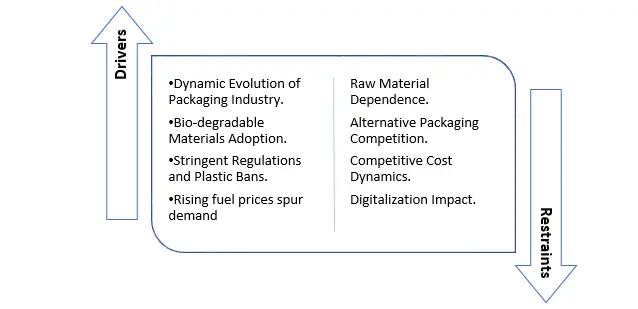

Packaging Evolution and Green Initiatives Energize Sack Kraft Paper Growth

The significant expansion happening in the building and construction sector stands out as a primary driver driving the growth of the sack kraft paper market. This increase is complemented by the enforcement of stringent regulations and bans on plastics across developed nations, coupled with the dynamic evolution of the packaging industry and the continual advancements in packaging and wrapping applications. These factors, among others, contribute to the growing demand for sack kraft paper.

The rising E-commerce and retail sectors, along with the trend toward product premiumization, usher in new opportunities for the sack kraft paper market in the foreseeable future. Several countries are actively promoting the adoption of bio-degradable materials for the storage and transportation of goods. Laminated and three-ply sack kraft paper bags have become the preferred choice for storing frozen and wet food products. The demand for environmentally-friendly packaging of industrial materials such as gypsum and cement further drive the sack kraft paper market in the packaging domain.

Sack kraft paper plays a key role in the storage of heavy building materials like cement, with each sack boasting a weight-bearing capacity of approximately 50 kilograms. These sacks are not only robust but also amenable to customization through brand or product-specific printing, adding an extra layer of appeal. The biodegradability of sack kraft paper sacks and bags positions them as eco-friendly alternatives, progressively supplanting their plastic counterparts.

The mounting concern over non-compostable solid waste and land pollution originating from polyethene and plastic bags acts as a catalyst for the growing adoption of sack kraft paper in packaging and carrying commodities. The versatility of sack kraft paper becomes evident as it easily accommodates diverse contents, from cement to sugar and wheat grains. To address the packaging of wet or liquid materials such as fruit juice, an inner coating of polyethene (PE) or polypropylene (PP) is applied to the bags.

Sack Kraft Paper Market Restraint

Raw Material Supply and Cost Dynamics Impacting Sack Kraft Paper Market

The sack kraft paper market encounters several significant restraints that impact its growth. The production of sack kraft paper heavily relies on softwood, a crucial raw material derived from trees like pines, Douglas fir, and juniper. In response to the pressing concerns of global warming and deforestation, various governments have implemented measures to curtail forest depletion. This has led to amendments that limit the felling of softwood trees, creating a challenge in ensuring a sustainable supply chain. Forest development, required to yield the necessary raw material, demands a protracted timeline to achieve equilibrium, thereby exacerbating the shortage of this pivotal resource and impeding market expansion.

The sack kraft paper market contends with a cost disparity compared to plastic-based alternatives, potentially restraining its uptake in price-sensitive markets. In scenarios necessitating moisture resistance or extended shelf life, sack kraft paper faces stiff competition from alternative packaging materials that offer superior attributes. This competitive landscape in specialized applications limits the market's growth potential. The ongoing digitalization trend, coupled with reduced reliance on traditional paper, poses a significant challenge to the sack kraft paper market. As certain sectors increasingly transition to digital documentation and communication, the demand for traditional paper diminishes, which could have cascading effects on the market's demand dynamics.

Sack Kraft Paper Market Opportunities

Innovative Sack Kraft Paper Solutions Offers Growth Opportunity

The sack kraft paper market is offering promising opportunities, with a range of factors that help market expansion and product innovation. The advent of aftermarket products crafted from sack kraft paper, including shipping sacks and shopping bags, is unlocking a realm of potential for small-scale industries. Market players are seizing the moment by introducing ingenious sack paper strings, which can be conveniently punched or glued onto open-mouth bags, enhancing the ease of transport. Domestic enterprises are channelling their efforts into infusing these sacks and bags with innovative designs and captivating prints, effectively capturing the attention of the packaging industry and carving a distinctive niche for themselves.

The increasing spread of the internet is positioned to serve as a catalyst for the widespread uptake of sack kraft paper in numerous countries. The pandemic period has significantly boosted businesses towards digital platforms, with manufacturers capitalizing on this shift by showcasing their processing units, end-products, and comprehensive product specifications, encompassing attributes such as colour, strength, and lamination, on their websites. As internet usage continues to rise, its role becomes pivotal in bridging the gap between large-scale enterprises and their smaller counterparts, fostering an environment of accessibility and collaboration.

The evolution of advanced sack kraft paper, fortified with enhanced properties like heightened tear resistance and superior moisture barriers, ushers in a fresh avenue of growth across diverse end-use industries. As consumer awareness about sustainable packaging gains traction, particularly in emerging economies, the sack kraft paper market stands poised to expand its presence and seize lucrative prospects. This growing consciousness opens doors for conscientious manufacturers to provide personalized and visually appealing packaging solutions, thereby not only gaining a competitive edge but also unearthing novel avenues for growth within the market.

Sack Kraft Paper Market Segment Analysis:

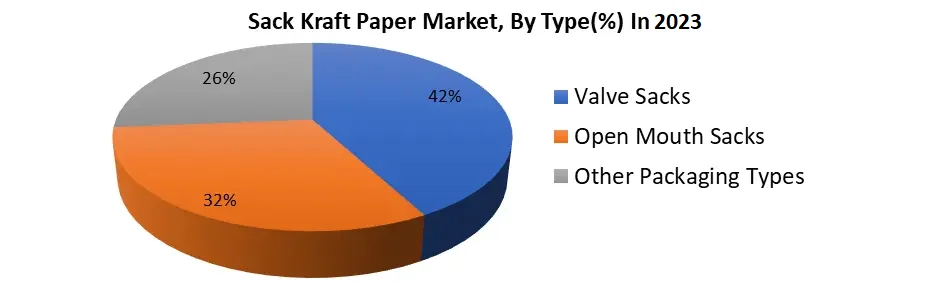

Based on Packaging Type, Valve Sacks dominated the Sack Kraft Paper Market in 2025 with 46% market share and is expected to continue its dominance during the forecast period. These are widely adopted in industries like cement, chemicals, and food. The self-closing valve offers convenience and efficient filling, making them suitable for fine and powdered materials. While Open Mouth Sacks is a fast-growing segment in market Commonly used in agriculture for products like seeds, fertilizers, and animal feed packaging. Their easy-fill design and robust structure ensure safe transportation and storage. Several other packaging types also emerging in the Sack Kraft Paper industry such as pinch bottom sacks, sewn open-mouth sacks, and more. These types of packaging find applications in sectors like pet food, building materials, and industrial chemicals. Based on End-Users, Building Materials and Cement dominated this segment in 2025 with a 38% Sack Kraft Paper Market share. In the construction sector, it ensures the safe packaging, storage, and transportation of cement, concrete, and construction materials. While the chemical industry is rapidly incorporating the use of sack kraft paper in packaging as it benefits from its moisture-resistant properties, safeguarding product integrity during chemical packaging. Likewise, in the agrochemical domain, Sack Kraft Paper is the preferred choice for packaging fertilizers, pesticides, and seeds, shielding them from external elements. Its application extends to animal feed and pet food packaging, maintaining hygiene and extending shelf life. In the food and beverage industry, the use of sack kraft paper in packaging is increased as it offers suitability for packaging dry goods, flour, and grains, and its eco-friendly nature aligns with sustainability trends. Department stores and supermarkets use kraft paper bags, capitalizing on their versatility.

Based on End-Users, Building Materials and Cement dominated this segment in 2025 with a 38% Sack Kraft Paper Market share. In the construction sector, it ensures the safe packaging, storage, and transportation of cement, concrete, and construction materials. While the chemical industry is rapidly incorporating the use of sack kraft paper in packaging as it benefits from its moisture-resistant properties, safeguarding product integrity during chemical packaging. Likewise, in the agrochemical domain, Sack Kraft Paper is the preferred choice for packaging fertilizers, pesticides, and seeds, shielding them from external elements. Its application extends to animal feed and pet food packaging, maintaining hygiene and extending shelf life. In the food and beverage industry, the use of sack kraft paper in packaging is increased as it offers suitability for packaging dry goods, flour, and grains, and its eco-friendly nature aligns with sustainability trends. Department stores and supermarkets use kraft paper bags, capitalizing on their versatility.

Sack Kraft Paper Market Regional Insights:

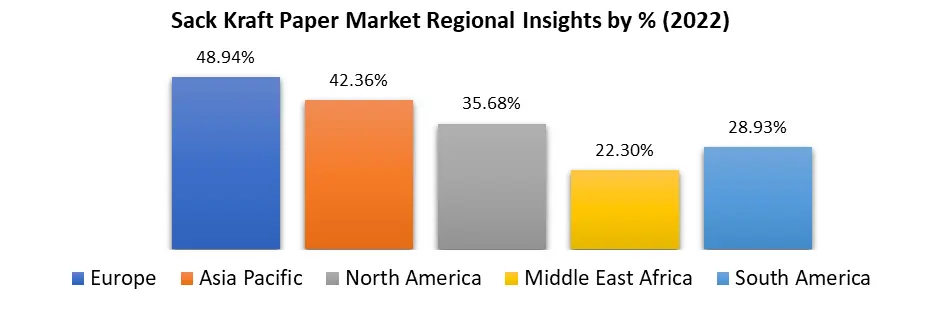

Europe dominated the Sack Kraft Paper Market in 2025 and is expected to continue its dominance during the forecast period. Europe has stringent regulations promoting recyclability and a shift towards biodegradable packaging materials boosts the market's expansion. The UK's strong paper industry, comprising 47 mills, contributes 4 million tons of paper, with noteworthy exports, fueled by a substantial consumption volume.

The Asia-Pacific region, characterized by rapid urbanization and increasing consumerism, witnesses escalating demand for Sack Kraft Paper in the packaging of various goods, particularly in emerging economies like India and China. South America experiences steady growth due to rising industrial activities and a heightened focus on sustainable packaging alternatives. In North America, a growing e-commerce sector and sustainable packaging initiatives drive demand for eco-friendly and robust packaging solutions, boosting the Sack Kraft Paper market.

Sack Kraft Paper Market Competitive Landscape

The competitive landscape of the Sack Kraft Paper market is marked by a dynamic interplay between industry leaders and innovative newcomers vying for market dominance. Market players like Mondi Group, Smurfit Kappa Group, and WestRock Company have established their supremacy through extensive product portfolios, global distribution networks, and sustainable solutions investments, effectively solidifying their market foothold. These industry leaders actively partake in strategic partnerships, mergers, and acquisitions to amplify their technological prowess and extend their market outreach. Concurrently, nimble entrants like Horizon Pulp & Paper Ltd. and Nordic Paper infuse the landscape with dynamism, concentrating on specialized segments and pioneering production techniques that foster a culture of ingenuity.

Sack Kraft Paper Market Recent Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 19 February 2026 | Mondi plc | The company reported a 5% increase in paper bag sales volume for the full year 2025 despite a cyclical market downturn. | This performance reinforces its global leadership in kraft paper production and highlights the resilience of the flexible packaging segment. |

| 30 January 2026 | Billerud AB | Billerud announced the planned installation of a new headbox at PM6 at the Gruvön mill to elevate its fluting and sack paper quality. | The upgrade will launch the next generation of Billerud Flute® in H2 2026, targeting superior strength and runnability for industrial customers. |

| 01 January 2026 | Stora Enso Oyj | Stora Enso officially discontinued its standalone Wood Products segment to integrate assets into consumer and industrial packaging divisions. | This reorganization aims to streamline the supply chain for renewable packaging and accelerate circular bioeconomy initiatives. |

| 15 May 2025 | Billerud AB | The company successfully commercialized a fully compostable, digitally printed sack kraft paper specifically for the Swedish market. | This innovation enables brands to achieve high-fidelity graphics while meeting strict biodegradability standards for consumer packaging. |

| 08 May 2025 | Mondi plc | Mondi announced a significant expansion of its sack kraft paper capacity at its Austrian facilities by adding a new production line. | The expansion directly addresses the surging demand from the European construction and food service packaging sectors. |

| 15 January 2025 | Segezha Group PJSC | The group launched a new high-barrier variety of sack kraft paper designed for industrial chemicals and powdered food products. | The material provides critical moisture and grease resistance while remaining 100% recyclable, replacing traditional plastic-lined bags. |

Sack Kraft Paper Market Scope: Inquiry Before Buying

| Sack Kraft Paper Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 12.52 USD Billion |

| Forecast Period 2026-2032 CAGR: | 3.98% | Market Size in 2032: | 16.45 USD Billion |

| Segments Covered: | By Product | Natural Bleached |

|

| By Grade | Standard Semi-Extensible Fully-Extensible |

||

| By Packaging Type | Valve Sacks Open Mouth Sacks Pinch-Bottom Sacks Form-Fill-Seal Sacks Others |

||

| By Ply / Layer Count | 1-Ply 2-Ply 3-Ply More than 3-Ply |

||

| By End-Use Industry | Building Materials and Cement Food and Beverage Ingredients Chemicals and Fertilizers Agriculture and Animal Feed Minerals and Pigments Others |

||

Sack Kraft Paper Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Sack Kraft Paper Market Key Players

- Mondi plc

- Smurfit Westrock plc

- Billerud AB

- Segezha Group PJSC

- Stora Enso Oyj

- Gascogne Groupe SA

- Nordic Paper AS

- Natron-Hayat d.o.o.

- Horizon Pulp & Paper Ltd.

- Klabin S.A.

- COPAMEX

- SCG Packaging Public Company Limited

- Oji Holdings Corporation

- Nine Dragons Paper Holdings Ltd.

- Heinzel Holding GmbH

- Georgia-Pacific LLC

- Rengo Co., Ltd.

- Daio Paper Corporation

- Sappi Limited

- International Paper Company

- Canfor Corporation

- Canadian Kraft Paper Ltd.

- Tokushu Tokai Paper Co., Ltd.

- Fujian Qingshan Paper Co., Ltd.

- Empresas CMPC S.A.

- Canadian Forest Products Ltd.

- Foresco (Forest Companies Ltd.)

- Venkraft Paper Mills Pvt. Ltd.

- Shree Rudra Lamkraft Pvt. Ltd.

- Saras Paper Products Pvt. Ltd.

Others