Power-To-Gas Market Size by Technology, Capacity, End User, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

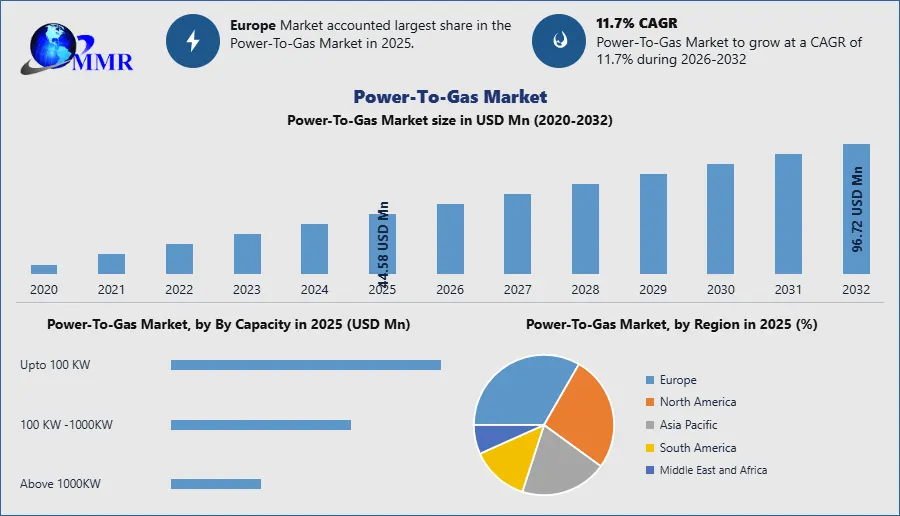

Power-To-Gas Market size was valued at US$ 44.58 Mn. in 2025 and the total revenue is expected to grow at a CAGR of 11.7% through 2025 to 2032, reaching nearly US$ 96.72 Mn.

Power-To-Gas Market Overview:

The power-to-gas delivers a promising approach to transform renewable power into the green hydrogen and methane renewables sector. The Power-to-Gas is very much effective for integrating renewables. It provides a rapid and dynamic response to the grid operator’s variations in renewable generation output.

To know about the Research Methodology :- Request Free Sample Report

Power-To-Gas Market Dynamics:

An increase in demand for renewable hydrogen, which has the potential to decarbonize multiple sectors are expected to drive the market growth. The driver for the growth of the market is the cost reduction of electrolyzer technology. According to the International Energy Agency, the electrolyzer stacks are responsible for 50% and 60% of the capital expenditure, and remaining factors like power electronics, gas-conditioning, and plant components are accounting for the remainder of the expenditure. Currently, The CAPEX requirements for alkaline electrolyzers have a range from $500 to $1,400/kWe. The PEM electrolyzers have a range of $1,100 to $1,800/kWe, and SOEC has an estimated range of $2,800 to $5,600/kWe. The costs for high-temperature electrolysis are expected to plunge 80% by 2021. Furthermore, prominent key players are focusing to build a modular renewable methane production. For instance, The Australian Renewable Energy Agency has granted US $1.1 Mn fund to APA Group to build a renewable methane production demonstration plant.

Despite the high cost, the exponential development cost of the technology and installed capacity are indicating that market implementation of power-to-gas is in underway.

Currently, only small power-to-gas plants (up to 10 MW) are in operation. The production of synthetic gases is currently very high. The Electrolysis manufacturing capacity wants to develop for the up scaling challenges. The production cost of gases is largely determined by capital costs. There will be chances of cost reduction because of up-scaling and learning effects. The framework of regulations, market incentives, tariffs have not taken into account for the opportunity of power-to-gas. With the seasonal storage and other technologies around, there is a need for further development and existing obstacles have to be addressed.

Green mobility - the most encouraging market for power-to-gas

Air quality regulations are increasing the need for hydrogen as a clean fuel for clean transport emissions across the globe. The Energy storage provision has started to become an obligatory requirement in areas like California. The Grid balancing and rapid response demand-side services are offering high proportions integration of renewable energy supply. Also, Auto OEMs are rolling out Fuel Cell Electric Vehicles (FCEVs), which require high purity hydrogen fuel. The Global Hydrogen Refuelling Station infrastructure programmes are underway with remarkable deployment plans. In addition, the price volatility of fossil fuels is driving an industrial substitution to more sustainable chemical processes.

Global energy markets are increasingly recognizing the requirement for the usage of green hydrogen as an energy storage medium and as a transport fuel, chemical fuel, and renewable heat. A number of economies like the Netherlands, Denmark, Germany, Australia, Korea, Japan, China, and the UK have all developed hydrogen roadmaps. In the UK, the Commission for Climate Change (CCC) indicates that there is a requirement of power between 6 and 17GW of electrolysis to achieve its target of net-zero by 2050.

Power-To-Gas Market Segment Analysis:

The Global Power-To-Gas Market is segmented by Technology, Capacity, and End-User.

Based on the Technology, the market is segmented into Electrolysis, and Methanation. Electrolysis segment is expected to hold the largest market shares of xx% by 2029. This is due to its flexible operations and ability to successfully incorporate electricity from intermittent renewable energy sources like wind and solar. These are the key benefit that drives the growth of the Electrolysis segment in the global market during the forecast period.

Based on the Capacity, the market is segmented into Less than 100 kW, 100–999 kW, and 1000 kW and above. 1000 kW and above segment is expected to grow rapidly at a CAGR of xx% during the forecast period. This is due to an increasing commercialization and implementation of several MW level projects of power to gas technologies, as well as demand from utilities and industrial end-users, 1000 KW and above capacity is widely preferred. These are the key factors of 1000 kW and above segment that drives the growth of the global market during the forecast period.

Based on the End-User, the market is segmented into Commercial, Utilities, and Industrial. Utilities segment is expected to grow rapidly at a CAGR of xx% during the forecast period. The utility industry is increasing as power and gas utilities seek to create hydrogen more efficiently by incorporating intermittent renewable power source and maintaining power system flexibility. These are the major factor that drives the growth of the utilities segment in the global market during the forecast period.

Power-To-Gas Market Regional Insights:

Europe dominates the Global Market during the forecast period 2025-2032. Europe is expected to hold the largest market shares of xx% by 2029. The massive development of renewable electricity production is underway in some European countries like Denmark and Germany and is expected to a larger extent in Europe during the forecast period. High capacities of power production which are from intermittent sources are expected to drive low spot prices of electricity. It also offers an opportunity for the development of flexible electro-intensive processes.

In Europe, the technical validation of power-to-gas has witnessed at the pilot scale, due to the series of projects, combined with targets for renewable electricity integration in Europe. The European energy system is undergoing a major transition to reduce carbon emissions. The political RES integration and carbon reduction targets are expected to increase the demand for the power-to-gas technology requirements. The region has put some of the world's highest environmental standards and ambitious climate policies to shape a sustainable future in the power-to-gas market. A climate change and reducing greenhouse gas emissions through efficient renewable energy systems are at the top of the agenda for the maintenance of environment pollution.

Power-To-Gas Market Prominent projects

In 2018, the hydrogen generation and fuel cell firm Hydrogenics and Enbridge Gas Distribution have started their operation of the 2.5-MW Markham Energy Storage Facility in Canada to deliver regulation services to the regional electricity system operator.

In 2018, The HyDeploy project, which was funded by Ofgem and led by Cadent and Northern Gas Networks have performed trial to establish the potential for blending up to 20% hydrogen into the normal gas supply to reduce carbon dioxide emissions. It will run a live trial of blended gas on part of the University of Keele gas network to determine the level of hydrogen.

Power-To-Gas Market Ambitious Future

The German transmission grid operator Amprion GmbH and European pipeline owner Open Grid Europe has announced a 100-MW electrolysis plant along with dedicated hydrogen. The companies are expected the projected cost of around €150 million and they want to successfully implement this technology for the German economy on an industrial scale. If the project receives necessary approvals, it could begin operations by 2025.

The industrial hydrogen producer H2V has contracted GE Power’s Grid Solutions business for the turnkey supply of two 225 kV/30 kV substations to feed the first 100-MW H2V Industry production units In Europe. The two projects are expected to feature 26 electrolyzers supplied by HydrogenPro and produce an average of 14,000 tonnes of hydrogen per year.

Many major players operated in the power-to-gas market includes Hydrogenics, ITM Power, and Electrochaea GmbH are focusing on signing contracts and agreements with end-users and installation of power-to-gas projects to reduce carbon emissions For instance, in 2025, ITM Power installed a 100MW power-to-gas energy storage project that helped the organization to use the hydrogen as a fuel and makes a significant contribution towards decarbonisation of the electricity and gas networks across Europe.

The objective of the report is to present a comprehensive analysis of the Global Power-To-Gas Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also helps in understanding the Global Power-To-Gas Market dynamic, structure by analyzing the market segments and project the Global Power-To-Gas Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Global Power-To-Gas Market make the report investor’s guide.

Recent Development:

October 2025: As part of Europe’s ongoing P2G and hydrogen infrastructure expansion, a major milestone was reached when Gascade Gastransport GmbH began the **initial filling and conversion of approximately 400 kilometers of existing natural gas pipelines for hydrogen transport under its “Flow – making hydrogen happen” program. This marks a significant step toward establishing a core hydrogen network in Germany that will link industrial centers across the country and support large-scale P2G integration and green hydrogen distribution by the end of 2025.

June 2024: Siemens Energy secured a USD 1.5 billion long-term service agreement for two gas-fired power plants in Saudi Arabia. The 25-year contract covers maintenance and advanced power plant technologies for the Taiba 2 and Qassim 2 facilities, which are expected to generate nearly 4 GW of electricity, strengthening the country’s power infrastructure and supporting energy transition initiatives.

May 2024: Nel ASA, through its subsidiary Nel Hydrogen Electrolyser AS, entered into a technology licensing agreement with Reliance Industries Limited. The agreement grants Reliance exclusive rights to deploy Nel’s alkaline electrolyzer technology in India, along with global manufacturing rights for internal use, accelerating green hydrogen production capacity.

Power-To-Gas Market Scope: Inquire before buying

| Power-To-Gas Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 44.58 USD Mn |

| Forecast Period 2026-2032 CAGR: | 11.7% | Market Size in 2032: | 96.72 USD Mn |

| Segments Covered: | By Technology | Electrolysis Methanation |

|

| By Feedstock | Water Biomass Carbon Dioxide Natural Gas |

||

| By Capacity | Upto 100 KW 100 KW -1000KW Above 1000KW |

||

| By End-User | Utility Commercial Industrial |

||

Power-To-Gas Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Player / Competitors Profile Covered in Power-To-Gas Market Report in Strategic Perspective:

1. Hydrogenics

2. ITM Power

3. McPhy Energy

4. Siemens

5. MAN Energy Solutions

6. Uniper

7. Micropyros

8. Carbotech

9. Power-to-gas Hungary

10. Aquahydrex

11. Fuelcell Energy

12. Nel Hydrogen

13. ThyssenKrupp

14. Electrochaea

15. Exytron

16. GreenHydrogen

17. Hitachi Zosen Inova Etogas

18. Ineratec

19. Socalgas