Poultry Feed Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

The Global Poultry Feed Market is not merely an agricultural input market—it is the economic backbone of the global poultry protein industry. Feed determines production cost, bird health, mortality rate, feed conversion ratio (FCR), regulatory compliance, and ultimately profit margins for integrators and farmers.

According to Maximize Market Research (MMR), the global poultry feed market was valued at USD 244.02 Bn in 2025 and is projected to reach USD 339.07 Bn by 2032, growing at a CAGR of 4.8% (2025–2032). This growth is not purely demand-led. Instead, it is driven by a multi-layered interaction of protein consumption growth, feed conversion efficiency economics, regulatory pressure on antibiotic usage, raw material price volatility, and rapid industrialization of poultry farming in emerging markets. What differentiates this market is not “growth”, but who captures value, who absorbs risk, and where margins are migrating.

This report is designed for feed manufacturers, additive suppliers, poultry integrators, and investors seeking to understand where value is shifting in global poultry protein economics.

Volume Economics & Consumption Reality: The Core Engine of the Market

To know about the Research Methodology :- Request Free Sample Report

Globally, poultry feed consumption exceeds 600–650 million metric tons per year, making it the largest segment within compound animal feed, ahead of cattle and swine feed.

Why Volume Is Structurally Locked In

• Poultry is the fastest-growing animal protein due to:

o Lowest feed-to-protein conversion

o Short production cycle

o Cultural and religious acceptability

• Feed constitutes 60–70% of total poultry production cost

• Every 1% improvement in feed conversion ratio (FCR) directly impacts farm EBITDA

• Poultry meat consumption continues to rise due to:

o Urbanization

o Price sensitivity vs red meat

o Protein affordability

Consumption Intensity with Volume Logic

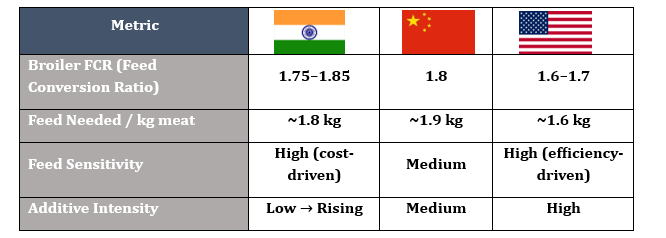

• Broilers: ~3.0–3.6 kg feed per kg live weight

• Layers: ~110–120 g feed/bird/day (~40–44 kg/bird/year)

• Turkeys: Higher protein density → higher feed cost per ton

A single commercial broiler consumes ~3.8 kg of feed over a 42-day cycle. At global production exceeding 75 billion birds annually, poultry feed demand structurally exceeds 285–300 million metric tons per year.

This makes feed demand inelastic: even during disease outbreaks or price spikes, baseline feed consumption does not collapse—it recalibrates.

Segment Intelligence: Where the Real Profit Pools Exist

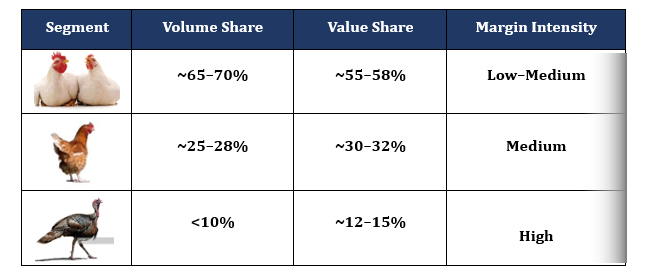

By Poultry Type • Broilers dominate volume but suffer margin compression due to price sensitivity.

• Broilers dominate volume but suffer margin compression due to price sensitivity.

• Layers offer stable recurring demand, predictable intake cycles, and better pricing power.

• Turkey feed, though niche, delivers high additive intensity and premium pricing.

By Feed Form & Ingredient (Value Migration)

• Pellets & Crumbles dominate due to superior digestibility and lower wastage

• Additives (enzymes, amino acids, probiotics) are the fastest-growing value segment (7–9% CAGR)

• Antibiotic growth promoters are structurally replaced by enzymes, organic acids, and phytogenics

Key Economic Shift:

Value is migrating from bulk feed tonnage to formulation intelligence.

DROCT Framework: Strategic Market Drivers

| Dimension | Market Impact |

| Drivers | Rising protein demand, urbanization, integrator farming |

| Restraints | Raw material price volatility, disease outbreaks |

| Opportunities | Additives, insect protein, precision nutrition |

| Challenges | Regulatory pressure, margin squeeze |

| Trends | Antibiotic-free feed, digital formulation, sustainability |

Market Structure: Who Controls Value vs Who Carries Risk

Supply Side Reality

• Feed milling is fragmented

• Raw material sourcing and additives are highly concentrated

• Additive suppliers often capture disproportionate margins

Demand Side Reality

• Thousands of farms, but buying power increasingly shifts to large integrators

• Small farmers remain price-takers

• Integrated poultry companies increasingly:

o Backward integrate into feed

o Lock long-term supply contracts

This creates a “margin squeeze funnel”:

Raw material volatility + regulatory pressure → margins compress downstream → innovation shifts upstream.

Table Suggestion:

Value chain margin distribution: raw materials → additives → feed mills → poultry integrators

Cost Pressure & Feedstock Economics (Real Industry Pain)

Raw Material Volatility

• Corn, soybean meal, wheat = 70–75% of feed formulation cost

• Price swings driven by:

o Climate volatility

o Trade restrictions

o Currency depreciation (Asia, Africa)

Impact on Feed Economics

• Every 10% increase in soybean meal price can:

o Increase feed cost by 4–6%

o Reduce farmer margins by 8–12% if not passed on

This is why:

• Amino acids substitute crude protein

• Enzymes reduce nutrient wastage

• Alternative grains gain traction

Regulatory Pressure Is Reshaping the Market

Contrary to common belief, regulation is not suppressing poultry feed growth—it is redistributing value.

Key Regulatory Forces

• Antibiotic Growth Promoter (AGP) bans

• Feed hygiene & traceability norms

• Carbon and sustainability reporting

Resulting Market Shift

• Higher additive intensity per ton of feed

• Premium pricing for compliant formulations

• Exit of small, non-compliant mills

• Consolidation around technology-ready players

The market is moving from “cheapest feed” to “lowest cost per kg of meat.”

Regional Power Dynamics: Where Volume vs Value Plays Out

Asia Pacific – Volume Anchor

• ~32–35% global feed volume

• China & India dominate poultry population

• Rapid shift from backyard to integrated farms

• Largest poultry feed consuming region

• Feed demand growth driven by:

o Population

o Urban protein demand

o Government-backed poultry expansion

North America – Efficiency Play

• High adoption of precision nutrition

• Strong regulation-driven additive penetration

• Captive feed mills dominate economics

Europe – Regulation-Driven Innovation

• Antibiotic bans accelerate enzyme & probiotic demand

• Higher feed cost, but premium meat economics

Competition: Why This Is Not a Commodity Market Anymore

The poultry feed market looks fragmented, but competitive advantage is concentrated.

| Player Type | Strategic Advantage |

| Integrated Poultry Giants | Cost control, captive feed |

| Multinational Feed Majors | R&D, additives, scale |

| Regional / Local Mills | Flexibility, proximity |

| Additive Specialists | Margin leadership |

Winning Capabilities

• Scale in raw material sourcing

• Proprietary formulations

• Regulatory readiness

• Advisory & on-farm technical support

• Digital feed optimization tools

Competitive Structure

• Integrated giants: CP Group, Cargill, New Hope

• Additive powerhouses: DSM, Evonik, BASF

• Regional champions: De Heus, ForFarmers

Fig: Competitive Positioning Matrix: scale × formulation capability × compliance readiness

Recent Developments & Industry Impact

• Expansion of enzyme portfolios (DSM–Novonesis, Evonik)

• Rapid feed mill capacity addition in India & Southeast Asia

• Regulatory tightening on antimicrobial resistance

• Rising investment in insect protein and synthetic amino acids

These developments structurally increase entry barriers, accelerating market consolidation.

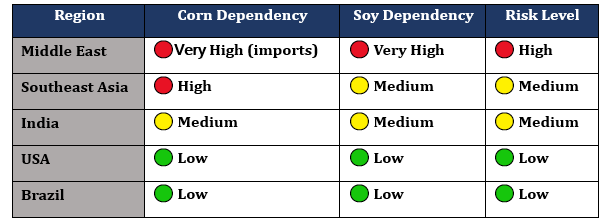

Import Dependence & Raw Material Risk Innovation & White Spaces

Innovation & White Spaces

Despite rapid innovation in enzymes, precision nutrition, and alternative proteins, the poultry feed market continues to exhibit structural white spaces. Adoption remains concentrated among large integrators, while mid-sized farms, smallholders, and emerging markets face cost, scalability, and integration barriers—creating untapped opportunities in climate-specific feeds, antibiotic-free formulations, digital feed-advisory bundling, and private-label manufacturing models.

Strategic Takeaway

• Volume is structurally guaranteed

• Margins migrate toward technology and compliance

• Feed economics decide poultry profitability

• Additives outperform base feed growth

• Consolidation favors serious players

Poultry feed is no longer about feeding birds—it is about controlling protein economics.

Poultry Feed Market, by Region

North America (United States, Canada and Mexico) Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Poultry Feed Market Scope: Inquiry Before Buying

| Poultry Feed Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 233.02 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.8% | Market Size in 2032: | USD 339.07 Bn. |

| Segments Covered: | by Poultry Type | Layer Feed Broiler Feed Turkey Feed Others |

|

| by Form | Pellets Crumbles Mashed Others |

||

| by Ingredient Type | Cereals Oilseed Meal Molasses Fish Oil Fish Meal Additives |

||

| by Feed Type | Complete Feed Concentrates Premix Others |

||

| by Nature | Conventional Organic |

||

| by Additive | Antibiotics Vitamins Antioxidants Amino Acid Feed Enzymes Feed Acidifiers Others |

||

| by Distribution Channel | Online Offline |

||

| by End-User Type | Independent Feed Mills Integrated Poultry Companies Contract Farmers (Integrator-backed) Cooperatives On-farm Mixers (declining share) |

||

Company Profile: Key Players – Global Poultry Feed Market

Global Integrated & Multinational Leaders

1. Cargill Inc. – Global scale, vertically integrated nutrition & grains

2. Archer Daniels Midland (ADM) – Feedstock sourcing + formulation leadership

3. Land O’Lakes, Inc. – Cooperative-led nutrition & premix expertise

4. Charoen Pokphand Group (CP Group) – Captive feed + poultry integration (Asia)

5. Tyson Foods, Inc. – Integrated poultry operations with in-house feed

6. Associated British Foods plc (AB Agri) – Europe-focused compound feed strength

7. Nutreco N.V. (SHV Holdings) – Animal nutrition & sustainability-driven feed

8. ForFarmers B.V. – Europe’s largest compound feed producer

9. De Heus Animal Nutrition (De Heus Voeders B.V.) – Rapidly expanding global footprint

10. New Hope Liuhe Group – China’s largest feed & poultry integrator

Additives, Nutrition & Technology Specialists

11. DSM-Firmenich (Royal DSM N.V.) – Enzymes, vitamins, precision nutrition

12. Evonik Industries AG – Amino acids (methionine), additive margin leadership

13. Alltech Inc. – Probiotics, enzymes, antibiotic-free solutions

14. Kemin Industries, Inc. – Feed additives, preservatives, nutrition science

15. Novus International Inc. – Methionine & specialty poultry nutrition

16. BASF SE – Feed enzymes, vitamins, and functional additives

17. Chr. Hansen Holding A/S – Probiotics & microbial solutions for poultry feed

Regional & Domestic Feed Powerhouses

18. Wen’s Food Group – China-focused integrated poultry & feed player

19. Kent Nutrition Group, Inc. – US-based regional feed strength

20. Hi-Pro Feeds, Inc. – North American livestock & poultry feed

21. Southern States Cooperative – Cooperative-based feed distribution (US)

22. Weston Milling Animal Nutrition – Australia & Oceania regional leader

23. EWOS Group – Specialized nutrition (now under Cargill, legacy relevance)

24. Balance Agri-Nutrients Ltd. – India-based regional poultry feed supplier

25. DeKalb Feeds, Inc. – Localized feed mill operator (US)

26. Godrej Agrovet Ltd. – India’s integrated feed & poultry platform

27. Japfa Ltd. – Southeast Asia-focused poultry & feed integrator

28. BRF S.A. – Brazil-based integrated poultry & feed player

29. Perdue Farms Inc. – US integrated poultry producer with captive feed

30. Suguna Foods Pvt. Ltd. – India’s largest contract poultry integrator

FAQs

Q1. Why is poultry feed considered a volume-driven market?

Because consumption is tied directly to bird population and biological feed requirements, not discretionary demand.

Q2. What is the biggest cost driver in poultry feed?

Corn and soybean meal, accounting for ~70% of formulation cost.

Q3. Why are additives growing faster than total feed volume?

They improve FCR, replace antibiotics, and help manage cost volatility.

Q4. Which region offers maximum long-term growth?

Asia Pacific, due to population, protein demand, and industrial farming adoption.

Q5. Is poultry feed becoming more profitable?

Profitability is shifting upstream to formulation, additives, and integrated models.

Lead Analyst Profile (EXCLUDED FROM WORD COUNT)

Lead Analyst – Global Feedstock & Animal Nutrition Markets

This research is authored by analysts with deep experience in poultry feed economics, feedstock volatility modeling, animal nutrition science, and agri-value-chain strategy, advising feed manufacturers, integrators, ingredient suppliers, and institutional investors across Asia, Europe, and the Americas.