Polyvinyl Chloride Market by Product Type, Stabilizer Type, Application,End-User, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

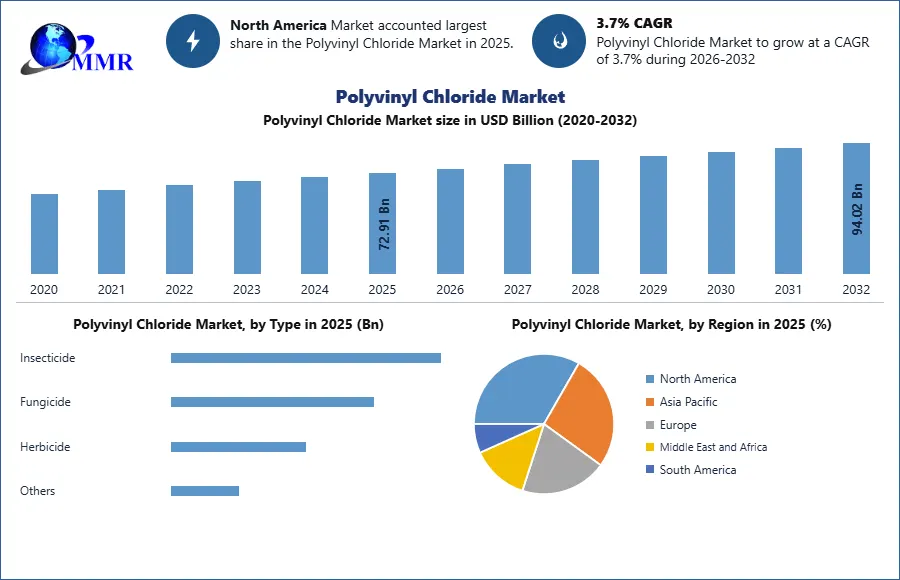

The Polyvinyl Chloride Market size was valued at USD 72.91 Billion in 2025 and the total Polyvinyl Chloride revenue is expected to grow at a CAGR of 3.7% from 2025 to 2032, reaching nearly USD 94.02 Billion by 2032.

Polyvinyl Chloride Market Overview

Polyvinyl Chloride (PVC), also known as Vinyl, stands out as an economical and versatile thermoplastic polymer widely employed in the building and construction sector for crafting door and window profiles. It finds application in drinking and wastewater pipes, wire and cable insulation, medical devices, and others. As the world's third-largest thermoplastic by volume, PVC is favored for its lightweight, durability, low cost, and ease of processability. It has become a popular substitute for traditional materials such as wood, metal, concrete, rubber and ceramics due to its diverse properties. The Polyvinyl Chloride Market has substantial growth driven by the increasing demand within the building and construction sector, particularly in the production of door and window profiles.

To know about the Research Methodology:-Request Free Sample Report

PVC's application lies in its versatility, cost-effectiveness and durability, prompting a shift away from traditional materials such as wood and metal and Polyvinyl Chloride Market growth. Its wide use in manufacturing drinking and wastewater pipes, wire and cable insulation, medical devices and several industrial applications has significantly contributed to industry growth. The lightweight, cost-efficient, and easily processable nature of PVC has facilitated widespread adoption across diverse industries. The industry is poised for growth with emerging opportunities in developing markets, where infrastructure development, construction booms, and urbanization trends create significant avenues for expanding PVC applications. Advancements in PVC technology, including Chlorinated PVC and molecular-oriented PVC (PVC-O), bring enhanced properties and new opportunities for market penetration. Despite challenges related to environmental concerns in PVC production and disposal, the market is well-positioned for growth, driven by its versatile applications, continuous technological innovations, and the increasing demand for cost-effective and sustainable solutions on both regional and global scales.

Polyvinyl Chloride Market trend

Growing emphasis on sustainability and eco-friendly practices

The PVC industry is undergoing a transformative shift with a growing emphasis on sustainability and eco-friendly practices. As environmental concerns take center stage, industries are increasingly recognizing the imperative to adopt more responsible manufacturing processes. The innovations in the PVC sector, push for the development of greener alternatives and the implementation of eco-friendly production methods. Companies are investing in research and development to create PVC products with reduced environmental impact, exploring recycling initiatives and adopting circular economy principles.

Consumer preferences are also evolving, with a heightened awareness of the ecological footprint associated with PVC production. Stakeholders across the Polyvinyl Chloride Market are aligning their strategies to meet this demand for sustainability, and development a positive impact on the industry as well as the environment. As regulations and consumer expectations continue to prioritize eco-friendly practices, the market is composed for a significant transformation towards a more sustainable future.

Polyvinyl Chloride Market Dynamics

Increasing demand within the building and construction sector to Boost Market Growth

PVC has solidified its position as a foundational material in the industry playing an essential role in windows, pipes, flooring, roofing membranes and several construction products. Its widespread use in construction is credited to its unmatched versatility, technical attributes, recyclability and cost-effectiveness. PVC's adaptability spans a broad spectrum of applications, from fundamental elements such as door and window profiles to critical roles in infrastructure development. The ongoing construction boom, particularly in developing economies marked by rapid urbanization and infrastructure expansion helped to boost the Polyvinyl Chloride Market. Significant fact that 70% of PVC production in Europe is dedicated to meeting the demands of the building and construction domain.

The material's inherent strength, lightweight nature, durability and user-friendly characteristics make it indispensable for crafting efficient and sustainable structures. The persistent demand for PVC is boosted by its outstanding properties including water resistance, extended lifespan and minimal maintenance requirements, positioning it as an optimal choice for pipes, roofing, and various construction components. With the global building and construction sector flourishing, the increasing reliance on PVC as an essential and versatile material position. The consistent demand for PVC in construction emphasizes shaping the modern built environment and reaffirms its status as an indispensable component in meeting the dynamic needs of the construction industry on a global scale.

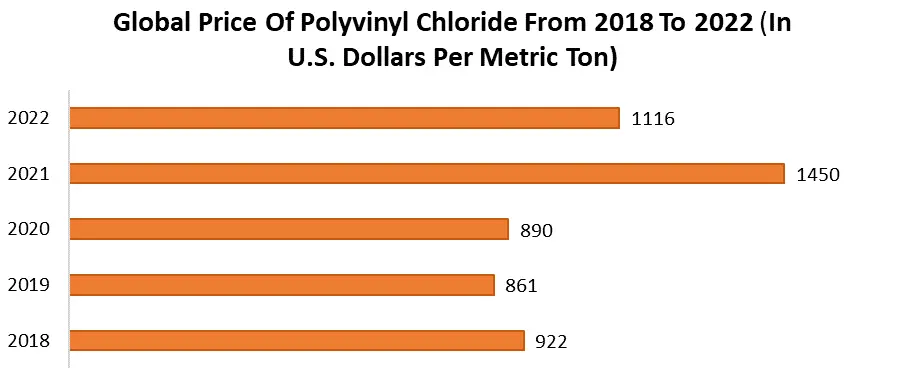

Global Polyvinyl Chloride (PVC) prices experienced a decrease in 2022. The decline coincides with an upswing in demand within the building and construction sector for Polyvinyl Chloride Market growth. The industry anticipates positive momentum due to increasing construction activities and increasing demand for PVC products.

Reliance on fossil fuels for raw materials hampers Market Growth

The dependence on fossil fuels for raw materials is a substantial impediment to the Polyvinyl Chloride Market. Vinyl chloride monomers for PVC synthesis through the chlor-alkali process, predominantly rely on ethylene derived from fossil fuel sources like natural gas or petroleum. This reliance exposes the PVC industry to the volatility in fossil fuel prices, impacting production costs and overall profitability. The extraction, processing, and transportation of fossil fuels contribute to environmental concerns, including carbon emissions. With increasing global efforts to combat climate change, the PVC industry faces heightened pressure to reduce its carbon footprint and embrace more sustainable practices. The reliance on fossil fuels also hinders compliance with evolving regulatory requirements aimed at curbing greenhouse gas emissions and fostering a circular economy. To navigate these challenges, the PVC industry explores alternative, renewable feedstocks, invests in energy-efficient production processes, and adapts to a changing landscape that prioritizes environmental sustainability, steering away from traditional reliance on fossil fuels.

Polyvinyl Chloride Market Segment Analysis

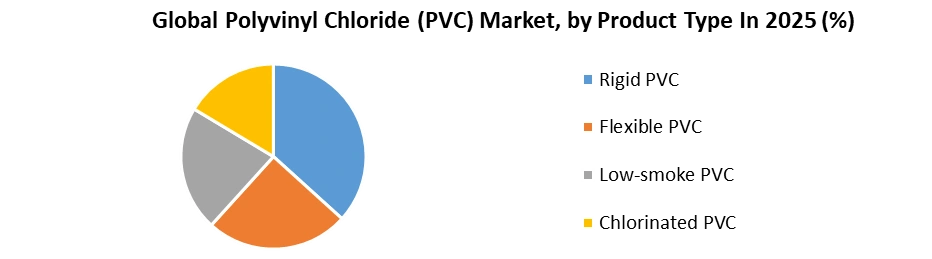

Based on the Product Type, the market is segmented into Rigid PVC, Flexible PVC, Low-smoke PVC and Chlorinated PVC. Rigid PVC held the largest Polyvinyl Chloride Market share in 2025 and is expected to have the highest CAGR during the forecast period. Rigid PVC stands as the powerhouse in the Market, reigning supreme due to its versatility, durability, and widespread applications. Its dominance stems from the remarkable strength and rigidity it imparts to a myriad of products, making it the material of choice in the construction and infrastructure sectors. Rigid PVC's exceptional chemical resistance and low cost have propelled its popularity in the production of pipes, window frames, and a plethora of rigid structures. Beyond its structural prowess, rigid PVC boasts exceptional insulation properties, contributing to its extensive use in electrical applications.

The material's resilience in harsh environmental conditions, coupled with its low maintenance requirements, positions rigid PVC as a go-to solution for industries seeking strong and long-lasting materials. In the blooming Polyvinyl Chloride Market, rigid PVC remains paramount. As global construction and infrastructure expand, rigid PVC proves essential, shaping city skylines, and supporting modern living foundations. Its enduring popularity underscores not only its technical superiority but also its essential role in meeting the evolving needs of diverse industries, establishing rigid PVC as the linchpin in the vibrant tapestry of the Market.

Polyvinyl Chloride Market Regional Insight

Asia Pacific dominated Polyvinyl Chloride Market in 2025 and is expected to continue its dominance over the forecast period. The Asia-Pacific region run by China, has experienced substantial industrial growth and urbanization over the past few decades. PVC is widely used in several industries such as construction and automotive packaging and the demand for these products has increased with the region's economic development.

China, in particular, has been undergoing rapid urbanization and infrastructure development, leading to a substantial demand for PVC in construction applications including pipes, cables, and fittings. Many global companies have established manufacturing facilities in the Asia-Pacific region, particularly in China, due to cost advantages and a strong supply chain. This has contributed to the high consumption of PVC in manufacturing processes. The complete size of the population in the Asia-Pacific region, coupled with rising living standards and consumer demand, has led to increased consumption of PVC-based products in daily life. Significant investments in the chemical industry, including PVC production capacities, have been made in the Asia-Pacific region.

China's ascendance to dominance in the global Polyvinyl Chloride Market, since its accession to the World Trade Organization in 2001, reflects its strategic prowess in shaping industry dynamics. Weathering substantial disruptions during 2020-2022, driven by the COVID-19 pandemic and government interventions, the Chinese PVC market showcased resilience and adaptability, rebounding from supply chain challenges. The growth in construction and manufacturing and China's unwavering demand for PVC solidifies its influential position. As the nation enters a post-pandemic era, China's commitment to sustainable development, technological innovation, and adherence to environmental standards emerges as pivotal factors influencing the future trajectory of the PVC market. The interplay of economic policies, technological advancements and evolving consumer preferences in China has continued to be central to discussions on the current and future state of the PVC market, extending its impact beyond national borders to shape global industry dynamics.

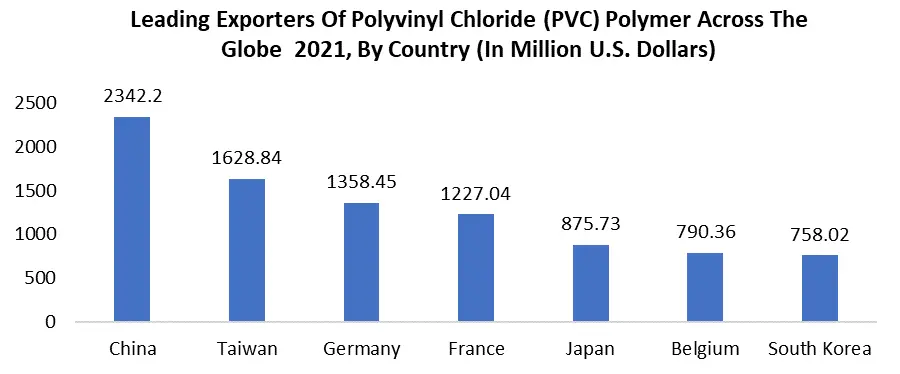

In 2021, China emerged as the dominant exporter of Polyvinyl Chloride (PVC) polymer globally, with exports totaling millions of U.S. dollars. The country's significant role in PVC polymer exports underscores its central position in shaping international trade dynamics for this key industrial material.

Polyvinyl Chloride (PVC) Market Scope: Inquire before buying

| Global Polyvinyl Chloride (PVC) Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 72.91 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 3.7% | Market Size in 2032: | USD 94.02 Bn. |

| Segments Covered: | by Product Type | Rigid PVC Flexible PVC Low-smoke PVC Chlorinated PVC |

|

| by Stabilizer Type | Lead Stabilizers Calcium-Zinc Stabilizers Organotin Stabilizers Others |

||

| by Application | Pipes and fittings Films and sheets Wires and cables Bottles Others |

||

| by End-User | Building and Construction Automotive Electrical and Electronics, Packaging Healthcare Others |

||

| by Application | Building & Construction & Infrastructure

Medical Applications

Insulation & Sheathing

Packaging

Coated Products

Automotive Applications

Leisure & Sports Products

|

||

Polyvinyl Chloride Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Polyvinyl Chloride (PVC) Key Players

Global

1. Formosa Plastics Corporation (Ma On Shan, Hong Kong)

2. Shin-Etsu Chemical Co., Ltd. (Tokyo, Japan)

3. Solvay (Brussels, Belgium)

4. Lotte Chemical Corporation (Seoul, South Korea)

5. Vinnolit GmbH & Co. KG (Burghausen, Germany)

North America

1. Occidental Petroleum Corporation (Houston, Texas)

2. Axiall Corporation (Atlanta, Georgia)

3. Nexeo Plastics (Houston, Texas)

4. Georgia Gulf Polymers & Chemicals LLC (Atlanta, Georgia)

Europe

1. Wacker Chemie AG (Munich, Germany)

2. Huntsman Corporation (The Woodlands, Texas)

3. Georgia Gulf Polymers & Chemicals LLC (Atlanta, Georgia)

4. Polypipe Holding Plc (Manchester, UK)

Europe

1. Solvay (Brussels, Belgium)

2. Kem One (Lyon, France)

3. Elementis plc (Watford, UK)

4. Wacker Chemie AG (Munich, Germany)

Asia Pacific

1. China National Chemical Corporation (ChemChina) (Beijing, China)

2. LG Chem (Seoul, South Korea)

3. Tianjin Bohai Chemical Industry Group Co., Ltd. (Tianjin, China

4. Tosoh Corporation (Shunan, Japan)

5. Hanwha Chemical Corporation (Seoul, South Korea)

Frequently Asked Questions:

1] What is the growth rate of the Global Polyvinyl Chloride Market?

Ans. The Global Polyvinyl Chloride Market is growing at a significant rate of 3.7% during the forecast period.

2] Which region is expected to dominate the Global Polyvinyl Chloride Market?

Ans. Asia Pacific is expected to dominate the Polyvinyl Chloride Market during the forecast period.

3] What is the expected Global Polyvinyl Chloride Market size by 2032?

Ans. The Polyvinyl Chloride Market size is expected to reach USD 94.02 Billion by 2032.

4] Which are the top players in the Global Polyvinyl Chloride Market?

Ans. The major top players in the Global Polyvinyl Chloride Market are Formosa Plastics Corporation (Ma On Shan, Hong Kong), Shin-Etsu Chemical Co., Ltd. (Tokyo, Japan),Solvay (Brussels, Belgium), Lotte Chemical Corporation (Seoul, South Korea), Vinnolit GmbH & Co. KG (Burghausen, Germany) and Others.

5] What are the factors driving the Global Polyvinyl Chloride Market growth?

Ans. Rapid urbanization and population growth and government regulations and standards are expected to drive market growth during the forecast period.