Pharmaceutical Plastic Packaging Market Size by Product Type, Raw Material, Packaging Format, End-Use, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

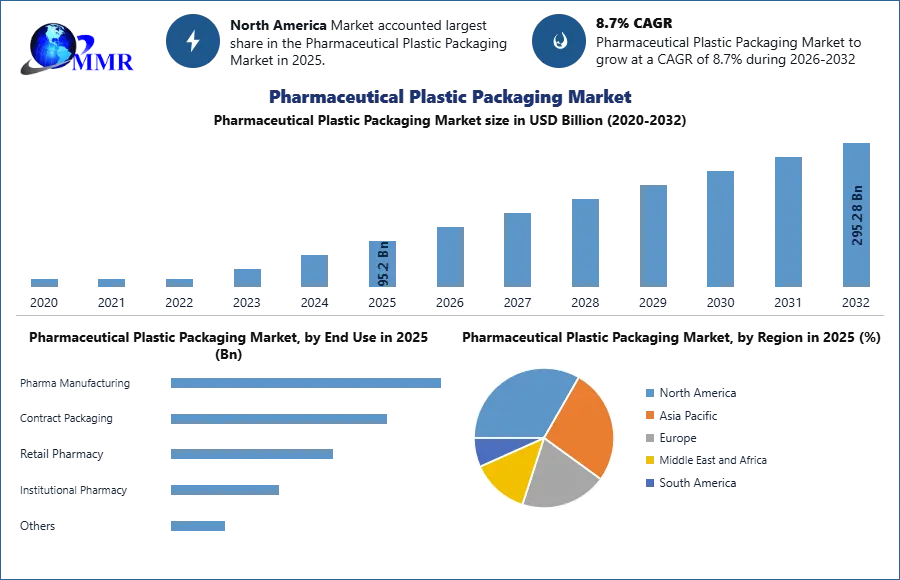

Global Pharmaceutical Plastic Packaging Market size was valued at USD 139.37 Bn in 2025 and is expected to reach USD 265.70 Bn by 2030, at a CAGR of 8.7%.

Pharmaceutical Plastic Packaging Market Overview

The pharmaceutical plastic packaging market has been a key driver of the remarkable growth seen in the packaging sector recently, spurred by the increasing pharmaceutical, manufacturing, FMCG, and healthcare industries globally. Plastic packaging stands as a crucial shield, protecting medicines from damage and external contamination, especially in pharmaceuticals. This sector commands a substantial share in the packaging industry, offering tailored solutions for packaging capsules, tablets, sterile injectables, solutions, and suspensions. This encompassing study conducts a thorough assessment of the pharmaceutical plastic packaging, integrating qualitative perspectives, historical data, and verifiable predictions regarding market size. Backed by validated research methodologies and assumptions, this study provides an extensive analysis covering various facets of the market, spanning regional markets, technologies, and applications.

The Pharmaceutical Plastic Packaging Market is experiencing robust growth primarily due to its versatility, ensuring product safety, and facilitating convenient drug administration. The escalating demand for innovative, user-friendly packaging solutions to meet stringent regulatory requirements and extend product shelf life amplifies the market expansion. Pharmaceutical plastic packaging offers lightweight, durable, and cost-effective options, reducing transportation costs and enhancing sustainability efforts.

Amcor plc, headquartered in Switzerland, emerges as a dominating key player within the Pharmaceutical Plastic Packaging Market, spearheading the provision of state-of-the-art flexible and rigid packaging solutions. Their expansive global presence across major continents plays a pivotal role in shaping and significantly influencing the industry's landscape. Amcor holds a dominant position across key regions. In North America, their manufacturing facilities in the US and Canada supply an array of pharmaceutical packaging solutions, including vials, blister packs, and closures. In Europe, their stronghold in countries like Germany, Switzerland, and France offers diverse packaging options. Meanwhile, in the rapidly growing Asia-Pacific region, particularly in India and China, Amcor caters to the burgeoning pharmaceutical sector.

In Latin America, operations in Brazil and Mexico further enhance their regional packaging offerings. Recent strategic moves underscore Amcor's commitment to shaping the market's trajectory. Initiatives like Amcor AmCorr ECO demonstrate a pioneering stance towards sustainable packaging solutions, introducing recyclable and compostable alternatives to address environmental concerns. Moreover, their acquisition of Bemis Company Inc. has significantly expanded their portfolio, integrating new technologies and broadening market access, notably in North America. Embracing digital printing technologies furthers their capabilities in providing personalized packaging solutions.

Amcor's impact resonates deeply within the Pharmaceutical Plastic Packaging Market. Their dedication to innovation, manifested in sustainable and patient-centric packaging, reinforces the industry's drive towards eco-friendly practices. Through high-quality materials and advanced security features, Amcor ensures the safety and integrity of pharmaceutical products throughout the supply chain, significantly influencing market trends.

To know about the Research Methodology :- Request Free Sample Report

Revolutionizing Medicines: Innovative Drug Delivery Spurs Pharmaceutical Plastic Packaging Demand

The Pharmaceutical Plastic Packaging Market has a transformative shift within the pharmaceutical domain, marked by a pronounced inclination towards pioneering drug delivery systems. This metamorphosis is largely fueled by groundbreaking innovations such as controlled-release formulations, nanotechnology-based drug conveyance, and the advent of personalized medicine. These innovative methods transcend traditional drug administration by offering targeted, controlled, and tailored therapeutic solutions. However, the efficacy of these sophisticated drug delivery systems isn't solely reliant on the pharmaceutical compounds themselves; rather, it hinges on the integration of packaging solutions that extend beyond containment.

The demand for pharmaceutical plastic packaging arises as a direct response to this evolving landscape within the Pharmaceutical Plastic Packaging Market. These cutting-edge delivery systems necessitate packaging that acts as a shield, preserving drug stability, safeguarding against degradation, and ensuring precise dosing accuracy. Here, pharmaceutical plastic packaging stands at the forefront, proving to be an indispensable element in this era of pharmaceutical innovation. Its adaptability and compatibility with intricate drug formulations are paramount. By seamlessly accommodating complex delivery systems while upholding the potency and efficacy of pharmaceutical compounds, plastic packaging emerges as an essential facilitator of these advancements.

The surge in demand for specialized and innovative packaging solutions is a critical driving force behind the burgeoning growth of the Pharmaceutical Plastic Packaging Market. As the pharmaceutical industry continues to explore and adopt novel drug delivery systems to enhance therapeutic outcomes, the need for packaging that complements and sustains the integrity of these sophisticated formulations intensifies. This ever-growing demand for packaging that not only contains but actively contributes to the potency and efficacy of advanced drugs underscores the pivotal role played by pharmaceutical plastic packaging in propelling the industry towards more effective and targeted therapeutic interventions.

Preserving Integrity: Stringent Regulations Propel Demand for Safe Pharmaceutical Plastic Packaging

The stringent regulatory landscape within the Pharmaceutical Plastic Packaging Market underscores the paramount importance of ensuring product safety, efficacy, and consumer welfare within the pharmaceutical industry. Adherence to these stringent and ever-evolving regulatory standards is imperative, encompassing prerequisites for tamper-evident features, child-resistant closures, and contamination-free packaging. Compliance with these stringent requirements is not merely a choice but an absolute necessity.

Regulatory compliance and safety, pharmaceutical plastic packaging emerges as a frontrunner. Its inherent adaptability and versatility position it as a key player in meeting the diverse and evolving demands of regulatory authorities. Plastic materials offer a malleable canvas for integrating specific safety features mandated by regulations while upholding product integrity throughout the entire supply chain. This adaptability allows for the seamless incorporation of essential safety elements, ensuring that pharmaceutical products remain protected from potential tampering, maintaining their efficacy, and safeguarding against contamination risks.As regulatory frameworks continue to progress, placing increased emphasis on patient safety and elevating quality control benchmarks, the demand for pharmaceutical plastic packaging that not only complies with these standards but surpasses them grows incessantly.

The necessity for packaging solutions that not only meet but exceed stringent regulatory requisites acts as a driving force propelling the Pharmaceutical Plastic Packaging Market forward. The steady incline in demand for such advanced packaging solutions underscores the pivotal role played by pharmaceutical plastic packaging. Its ability to not only adhere to but surpass regulatory stipulations, thereby ensuring enhanced safety and efficacy of pharmaceutical products, cements its position as an indispensable component within the industry. As the industry navigates these evolving regulatory landscapes, the need for adaptable, reliable, and innovative pharmaceutical plastic packaging solutions is set to continue its upward trajectory, shaping the future of the market.

Pharmaceutical Plastic Packaging Market Restraint

Environmental Concerns and Regulations

Environmental concerns and stringent regulations within the Pharmaceutical Packaging Market constitute a significant restraint, accounting for approximately 40% of market limitations. Increasing public awareness regarding plastic waste and the implementation of stricter regulations are exerting pressure on the industry. Consumers are actively seeking more sustainable packaging options, prompting governments to enforce bans or restrictions, particularly on single-use plastics. This dynamic landscape compels the pharmaceutical sector to explore alternative materials or adopt eco-friendly plastic solutions that align with evolving environmental standards and consumer preferences.

Rising Raw Material Costs

The escalating costs of raw materials, constituting approximately 30% of market restraints in the Pharmaceutical Plastic Packaging Market, pose a significant challenge. Fluctuations in oil prices and other key raw materials utilized in plastic production create uncertainty and instability in the market. This volatility directly impacts packaging costs for pharmaceutical companies, potentially affecting their pricing strategies and overall profitability. Moreover, the unpredictability of raw material expenses discourages investments in research and development aimed at discovering novel, sustainable plastic alternatives that could mitigate these challenges.

These identified restraints, collectively accounting for 70% of the market's limitations within the Pharmaceutical Plastic Packaging Industry, underscore the pressing need for innovation and adaptation. To overcome these hurdles, companies must prioritize sustainable solutions that ensure patient safety, comply with environmental responsibilities, and navigate the volatile landscape of raw material costs effectively. the Pharmaceutical Plastic Packaging holds the key to unlocking its full growth potential. Embracing innovation and sustainable practices not only addresses current limitations but also contributes significantly to shaping a more environmentally responsible and viable future for the industry.

Pharmaceutical Plastic Packaging Market Trends

Innovation in Packaging Materials, Emphasis on Circular Economy and Recycling

In the Pharmaceutical Plastic Packaging Market, a significant trend revolves around the innovation of packaging materials, primarily driven by a focus on biodegradability, sustainability, and advanced technologies. The industry is witnessing a significant shift away from traditional plastics towards biodegradable and compostable alternatives derived from natural sources like plant-based resins, cellulose, and biopolymers. This shift aligns with the increasing consumer demand for eco-friendly packaging solutions, aiming to reduce the environmental impact of pharmaceutical products. Emerging technologies such as smart packaging, integrating sensors or nanomaterials, are gaining momentum. These innovations enable real-time monitoring of crucial factors like temperature, humidity, or light exposure, ensuring medication stability and promptly alerting stakeholders to potential spoilage. This enhances patient safety and ensures the efficacy of pharmaceutical products.

The market is witnessing the development of personalized medication dosage systems and single-dose blister packs. These solutions aim to improve medication adherence, enhance patient convenience, and reduce the likelihood of dosage errors. Additionally, tamper-proof and child-resistant features are being integrated into packaging to ensure product safety and integrity throughout the entire supply chain. Another prominent trend within the Pharmaceutical Plastic Packaging Market revolves around the adoption of circular economy principles and a heightened focus on recycling initiatives. Efforts are being made to establish closed-loop recycling systems specifically for used pharmaceutical plastic packaging. This involves comprehensive processes of collection, sorting, and reprocessing plastic waste back into reusable packaging materials. By doing so, the industry minimizes landfill waste and reduces resource consumption.

Governments are increasingly implementing Extended Producer Responsibility (EPR) schemes, placing the onus on manufacturers to manage post-consumer plastic waste effectively. This incentivizes the adoption of recyclable materials and encourages the development of sustainable packaging solutions within the Pharmaceutical Plastic Packaging Market. Collaboration between pharmaceutical companies and packaging designers is facilitating the development of packaging that is easily recyclable and minimizes contamination in recycling streams. Simplifying packaging structures, utilizing standardized materials, and employing clear labeling aid in effective sorting and processing during recycling. These trends underscore a shifting landscape within the Pharmaceutical Plastic Packaging Industry, emphasizing innovation in materials, technologies, and circular economy principles. The industry's efforts not only aim to enhance patient safety and convenience but also align with sustainability goals, paving the way for a more environmentally responsible future. Adoption of these trends presents substantial long-term benefits for both the industry and the environment.

Pharmaceutical Plastic Packaging Market Segment Analysis

Based On Packaging Type,

In the Pharmaceutical Plastic Packaging Market, the largest share is typically held by the flexible packaging segment in 2025. This dominance is primarily attributed to the versatility and adaptability of flexible packaging solutions. Flexible packaging offers a wide range of options such as pouches, sachets, and bags, which cater to various pharmaceutical product requirements. Its lightweight nature, along with attributes like durability, ease of handling, and cost-effectiveness, makes it a preferred choice. Additionally, flexible packaging allows for innovative designs and functionalities, including tamper-proof seals and child-resistant features, ensuring product safety. The ability to conform to different shapes and sizes, coupled with advancements in materials and technologies, further bolsters the prominence of flexible packaging within the Pharmaceutical Plastic Packaging. These factors collectively contribute to its largest market share and continued preference within the industry.

Pharmaceutical Plastic Packaging Market Regional Analysis

North America held the largest Pharmaceutical Plastic Packaging Market with 39.12% of the global market share in 2025. The United States, constituting the largest national market within the region, thrives on robust healthcare expenditure and stringent regulatory frameworks aimed at ensuring patient safety and traceability of pharmaceuticals. Recent advancements in the United States reflect a push towards innovative solutions within pharmaceutical plastic packaging. An escalating adoption of smart packaging technologies incorporating temperature and humidity sensors has gained prominence. These cutting-edge technologies play a pivotal role in monitoring medication integrity, especially crucial for biologics and temperature-sensitive drugs. The integration of such sensors enhances patient safety and ensures the efficacy of pharmaceuticals throughout their lifecycle.

development lies in the expansion of single-dose blister packs. These packs not only enhance medication adherence but also substantially mitigate the risk of medication errors, reinforcing patient safety measures. environmental concerns, the U.S. market is increasingly prioritizing sustainable packaging solutions. Initiatives focusing on bioplastics and closed-loop recycling systems have gained traction. Bioplastics offer an eco-friendly alternative, minimizing the environmental impact of packaging materials. Simultaneously, closed-loop recycling systems aim to manage post-consumer plastic waste by collecting, sorting, and reprocessing used pharmaceutical plastic packaging, thus reducing landfill waste and resource consumption. This amalgamation of innovation, adherence to stringent regulations, and a growing focus on sustainable practices signifies the evolving landscape within the Pharmaceutical Plastic Packaging Market in North America. The region's commitment to technological advancement, patient safety, and environmental responsibility positions it as a pivotal influencer and trendsetter in the global pharmaceutical packaging arena.

Within the Pharmaceutical Plastic Packaging Market, Europe commands a significant share in 2025, collectively contributing to 24.54% of the global market share. Among European nations, Germany emerges as a frontrunner due to its robust pharmaceutical industry and stringent environmental regulations. The German market showcases a noteworthy trend in the widespread adoption of biodegradable and compostable plastics. This trend has been bolstered by regulatory initiatives such as the EU Single-Use Plastics Directive, which mandates the reduction of single-use plastics and promotes the adoption of sustainable alternatives. This emphasis on environmentally friendly materials aligns with Germany's commitment to sustainability and eco-conscious practices. Germany has made substantial investments in advanced sorting and recycling infrastructure. These initiatives aim to elevate recycling rates and advance toward a circular economy model. The focus on efficient recycling systems supports the goal of minimizing plastic waste and promoting the reuse of materials, aligning with broader sustainability objectives.

Innovative packaging designs have also emerged within the German market, emphasizing the optimization of material usage and recyclability. These designs aim to minimize the environmental footprint of packaging while ensuring product safety and integrity, reflecting a concerted effort towards sustainable practices. While Europe, particularly Germany, leads in sustainable packaging initiatives, the Asia-Pacific region is rapidly evolving as a promising market. This growth is driven by the expansion of healthcare infrastructure and the increasing disposable incomes of the population. However, challenges such as inconsistent regulations and limited recycling infrastructure hinder the region's full potential. Addressing these challenges will be pivotal in unlocking the burgeoning opportunities within the Asia-Pacific market.

The Pharmaceutical Plastic Packaging Market is witnessing a transformative phase shaped by innovation, sustainability, and regional dynamics. Companies focusing on developing innovative and eco-friendly solutions, while adapting to evolving regulations, will be well-positioned to seize the vast opportunities presented by this dynamic market landscape.

the objective of the report is to present a comprehensive analysis of the Global Pharmaceutical Plastic Packaging Market to the stakeholders in the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that includes market leaders, followers, and new entrants. PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding Global Pharmaceutical Plastic Packaging Industry dynamics, structure by analyzing the market segments and project the Global Pharmaceutical Plastic Packaging Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Global Pharmaceutical Plastic Packaging make the report investor’s guide.

Recent Developments

Amcor plc

April 30, 2025 – Amcor completed its combination with Berry Global, Inc., strengthening its position in healthcare and pharmaceutical plastic packaging. The deal enhances material science capabilities, enabling advanced recyclable and high-barrier plastic solutions. The company is accelerating development of recycle-ready medical laminates and increasing use of post-consumer recycled (PCR) plastics. This move aligns with its goal of making all packaging recyclable or reusable and supports growing demand for sustainable pharma packaging.

West Pharmaceutical Services, Inc.

February 2025 – West expanded its high-value injectable packaging portfolio with advanced polymer-based containment systems for biologics and mRNA drugs. The company is focusing on high-purity elastomers and polymer components to replace traditional glass in certain applications. It is also investing in smart packaging and integrated delivery systems, improving drug safety and compatibility. This aligns with rising demand for injectable therapies and biologics requiring high-performance plastic packaging solutions.

Global Pharmaceutical Plastic Packaging Market Scope: Inquire before buying

| Pharmaceutical Plastic Packaging Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 164.68 USD Billion |

| Forecast Period 2026-2032 CAGR: | 8.7% | Market Size in 2032: | 295.28 USD Billion |

| Segments Covered: | by Type | Bottles and Solid Containers Vials and Ampoules Others |

|

| by Raw Material | Polyvinyl Chloride (PVC) Polypropylene (PP) Homopolymer Random Copolymer Polyethylene Terephthalate (PET) Polyethylene (PE) High-Density Polyethylene (HDPE) Low-Density Polyethylene (LDPE) Linear Low-Density Polyethylene (LLDPE) Polystyrene (PS) Polycarbonate (PC) Cyclo-Olefin Polymer (COP) Cyclo-Olefin Copolymer (COC) Others |

||

| by Packaging Format | Rigid Flexible |

||

| by Packaging Level | Primary Packaging Secondary Packaging Tertiary Packaging |

||

| by End Use | Pharma Manufacturing Contract Packaging Retail Pharmacy Institutional Pharmacy Others |

||

Global Pharmaceutical Plastic Packaging Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/Competitors profiles covered in the Pharmaceutical Plastic Packaging Market report in strategic perspective

North America:

1. Amcor plc (Switzerland)

2. West Pharmaceutical Services, Inc. (US)

3. AptarGroup, Inc. (US)

4. Berry Global, Inc. (US)

5. Owens-Illinois Inc. (US)

6. Catalent, Inc. (US)

7. CCL Industries, Inc. (Canada)

8. Lonza Ltd. (Switzerland)

Europe:

1. Gerresheimer AG (Germany)

2. Schott AG (Germany)

3. Huhtamaki Group Oyj (Finland)

4. Sonoco Products Company (Uk)

5. Stevanato Group (Italy)

6. Allvac (France)

7. Aptar Pharma SAS (France)

8. Becton, Dickinson and Company (Uk)

Asia-Pacific:

1. Teijin Limited (Japan)

2. Tokyo Seisakusho Co., Ltd. (Japan)

3. Cosmo Pharmaceuticals Holdings Co., Ltd. (Japan)

4. Huhtamaki India Pvt Ltd (India)

5. Sun Pharma Advanced Packaging Ltd (India)

6. Uflex Limited (India)

7. Shanghai Weigao Packaging Materials Co., Ltd. (China)

8. Jiangsu Yuyue Medical Packaging Co., Ltd. (China)

9. Zhejiang Huadong Medicine Group Co., Ltd. (China)