PET Foam Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

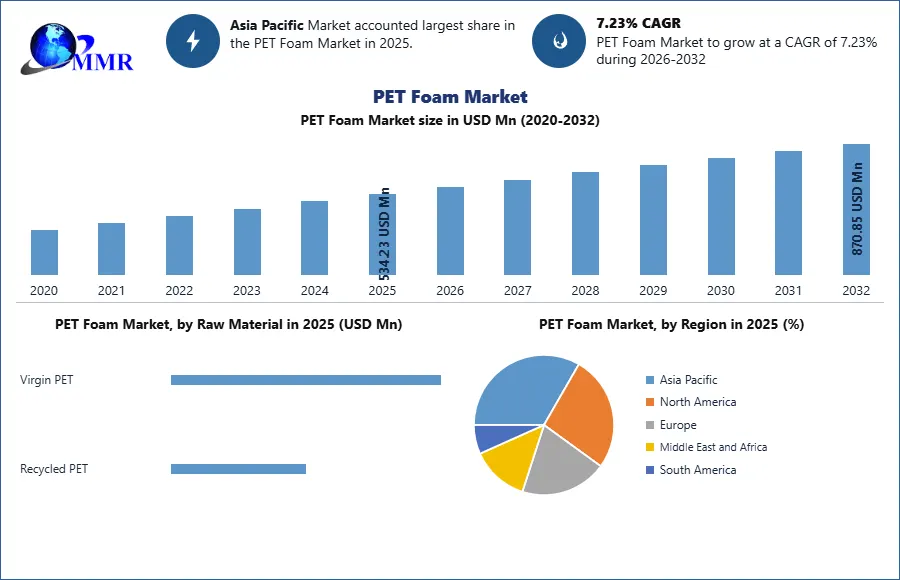

PET Foam Market was valued at USD 534.23 Million in 2025, and it is expected to reach USD 870.85 Million by 2032, exhibiting a CAGR of 7.23 % during the forecast period (2026-2032)

PET (Polyethylene Terephthalate) is a thermoplastic that yields a low-cost but structurally robust core product. PET cores, which is heated and moulded to precise forms, are becoming increasingly popular as more manufacturers recognise their consistent qualities and benefits. Wind and other renewable energy sources are quickly becoming a greater part of the overall power supply, and Composites One offers the materials and technical assistance to help businesses succeed. Wind turbine blade designs have grown in size and efficiency in order to maximise energy generation capacity.

Another problem is to increase the functional lifespan of wind turbines in order to recoup their initial cost. PET foam and other thermoplastic materials provide strength, stiffness, durability, and design freedom, which can assist extend blade life. Hence, the demand from wind energy industry has been driving the PET Foam Market.

Diab Group (Diab), a major player in sandwich composite solutions, has chosen SABIC's new LNP COLORCOMP compound, which employs nanotechnology to reduce weight and improve mechanical properties of sandwich structures made of polyethylene terephthalate (PET) foams and will be used as the core material of wind turbine blades. The PET Foam Market report has covered the detailed analysis of each country and each market segment with the drivers and restraints in the market. Microanalysis of industry and external as well internal factors affecting the PET Foam Market will give deep insight in the industry. To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

PET Foam Market Dynamics

Increasing Construction Activities in the Asia-Pacific Region to drive the PET Foam Market

Thanks to fast growing middle class population, particularly in developing economies such as China and India, and ASEAN countries, need for housing is clearly increasing at a rapid pace. This is causing an increase in residential building all through the region, which is likely to boost the market for PET foam used in architectural applications and other application sectors.

PET foam-based constructions are well recognized for their simplicity of installation, improved energy efficiency, lower maintenance and repair costs, and so give more efficient solutions to the building industry. Furthermore, the particular features of PET foam and its unique eco-balance enable building industry directions for ecologically responsible and resource-friendly building design, construction, operation, and maintenance throughout its full life cycle.

The Asia-Pacific construction industry is expected to become the world's largest and fastest-growing industry, both in the residential and commercial sectors, with the region accounting for around 45% of global construction spending. The Indian government is focusing on infrastructure development in order to stimulate economic growth.

China is in the midst of a massive development boom. The country is the world's largest construction market, accounting for 20% of total worldwide construction investment. By 2030, the country is estimated to spend over USD 13 trillion on construction. In 2020, the Chinese government set an annual maximum of CNY 3 trillion for a new infrastructure bond. Therefore, from the factors mentioned above, the demand for PET foam from the building and construction industry is expected to increase during the forecast period.

Increasing Usage in the Automotive Industry to drive the PET Foam Market

The need for light weight polymers and composite materials has increased in recent years as a result of rising customer demand for fuel-efficient and lightweight cars. PET foam has several advantages, including superior thermal stability, minimal water absorption, good electrical characteristics, and great surface qualities. PET foams are utilised in the production of external body components, as well as the casing and housing of numerous automobile parts such as wiper arms and gear housings, engine covers, interior trim, connector housings, headlight retainers, and many more. Substituting foam for heavier materials results in an overall weight reduction of roughly 10%, resulting in a 3% to 7% gain in fuel economy.

Availability of Substitutes for Pet Foam: A restraint to overcome for PET Foam Manufacturers

PET is inexpensive and lightweight, has strong mechanical and thermal insulating qualities, is more resistant to heat, is safer and less poisonous, is more easily recycled, and has a reduced carbon footprint. However, the reproducible creation of stable, homogenous PET foams can be difficult and discouraging to producers.

To begin, foaming PET necessitates the insertion of additives into the polymer, such as chain extenders. Furthermore, because the melting point of PET is roughly 250°C, the equipment utilised must be prepared for high temperatures. As a result, there are several core foams on the market, including Polyvinyl Chloride (PVC), Styrene Acrylonitrile (SAN), Polymethacrylimide (PMI), and Polyetherimide (PEI). These foams are simple to produce and shape, and they have a high strength-to-weight ratio.

As a result, they are employed in the wind energy, aerospace and defence, maritime, and transportation industries. These foams might be used as a replacement for PET foam. As a result, the presence of a high number of replacements is seen as a major impediment to market expansion. In compared to general-purpose polystyrene resin, Styrene Acrylonitrile (SAN) has greater mechanical qualities, chemical resistance, and heat resistance. SAN outperforms conventional foams in terms of surface gloss, dimensional stability, mechanical strength, and electrical characteristics.

It can be treated more readily than acrylic resins. Furthermore, as compared to other foams of comparable density, PVC foams are closed-cell, moisture resistant, and have superior physical qualities. It burns itself out and will not decay. Other inherent properties are excellent fatigue life and good bond strength with common adhesives and resins. However, the presence of substitutes is likely to restrain the PET foam market during the forecast period.

PET Foam Market Segment Analysis

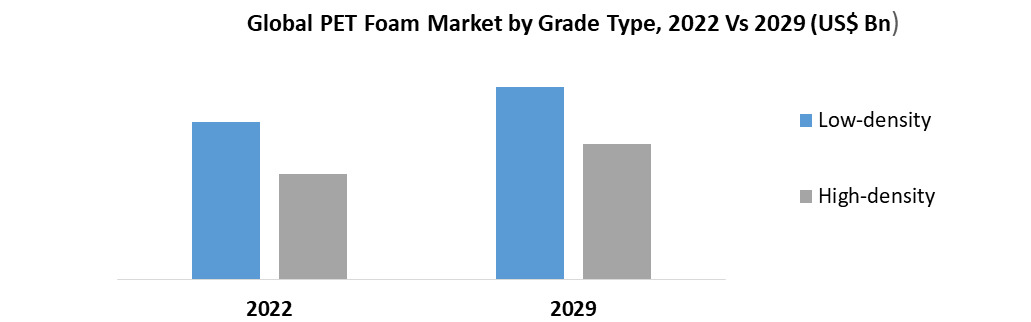

Based on Grade Type, the density of the foam has a considerable impact on its performance. While low density foams are softer and more flexible than high density foams, they cannot tolerate extreme pressure or weight. Because of its greater appropriate performance in many applications, low-density PET foams have a bigger market share than high-density PET foams. PET foam is favoured at low density, particularly for applications such as commercial container applications, since low-density foam performs better at low temperatures and provides the essential rigidity for deeply formed containers.

Because of its lightweight and good chemical and electrical resistance, low-density PET foam is regarded a perfect choice for a variety of end-use sectors, including transportation, building and construction, and packaging. Low-density PET foams are being driven by the rapid growth of the packaging, building, and construction sectors, as well as the widespread use of low-density PET foam and its better attributes compared to alternative core materials in these industries. Overall, demand for low-density PET foam is predicted to expand moderately to slowly during the forecast period.

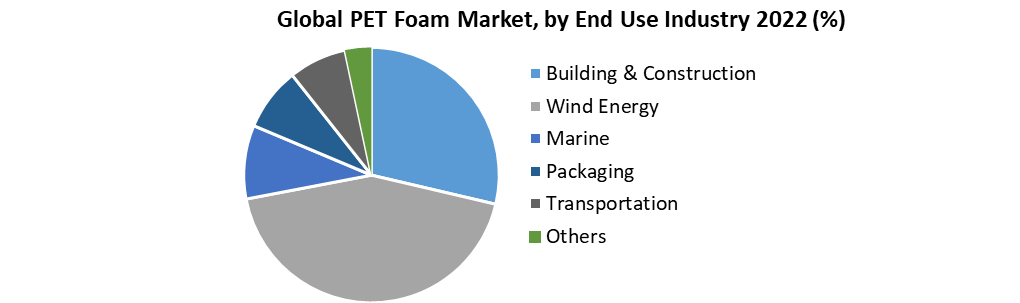

PET Foam Market Based on End-Use Industry, one of the largest and fastest growing applications of the PET foam industry is wind energy. Polyethylene terephthalate (PET) foam is utilised in wind energy applications such as wind turbine blades and nacelles. Wind energy consumption has been growing at an unprecedented rate in recent times due to the rapid desire for cleaner and more efficient energy methods. In general, global electricity demand is expected to rise by 75% by 2030.

PET Foam Market Regional Insights

Asia Pacific region dominated the PET Foam market in 2025 and is expected to grow at a CAGR of 8.12% during the forecast period. One of the most thorough endeavours to join the highest tiers of aerospace development and production is China's aerospace strategy. Over the next 20 years, China is expected to be the world's largest single nation market for civil aircraft sales. According to the 'Made in China 2025' strategy, China is expected to provide more than 10% of domestic commercial aircraft to the domestic market . During the forecast period, this is likely to drive demand for PET foams in the aerospace industry.

China has the world's second-largest packaging industry. The country is expected to develop steadily during the forecast period, owing to the emergence of customised packaging in the food segment, such as microwave food, snack foods, and frozen foods, as well as increased exports. PET foams are predicted to be used more in packaging in the future. Furthermore, China serves as a hub for a variety of manufacturing operations. As a result, it is involved in the bulk export of various items, whether little or large, to many foreign locations. As a result, this situation is expected to raise the country's demand for PET foams.

PET Foam Market Recent Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 16 March 2026 | Armacell International SA | Announced that its ArmaFlex Ultima technical foam received NK Type Approval from Nippon Kaiji Kyokai for use in marine and offshore structures. | The certification confirms compliance with international marine safety standards, streamlining ship inspections and promoting ultra-low smoke insulation solutions. |

| 02 March 2026 | Gurit Holding | Reported 2025 net sales of CHF 319.6 million, highlighting a landmark long-term supply agreement for core kits utilizing OptiCore technology. | The agreement with a leading Western wind OEM reinforces Gurit's global leadership in sustainable wind energy and sets a positive growth trajectory for 2026. |

| 08 October 2025 | DIAB Group | Won the IBEX 2025 Innovation Award in the Boatbuilding Methods & Materials category for its Advanced Kits composite solutions. | The award recognizes Diab's ability to deliver lighter, lower-impact solutions that optimize efficiency for commercial and leisure boatbuilders worldwide. |

| 13 January 2025 | Armacell International SA | Showcased the ArmaPET Eco50 and ArmaPET Struct GRX recycled PET foam cores at the BAU 2025 exhibition in Munich. | These products highlight the industry's shift toward recycled-content structural foams, offering high-strength alternatives for green building and energy-efficient construction. |

PET Foam Market Scope: Inquire before buying

| PET Foam Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 534.23 USD Mn |

| Forecast Period 2026-2032 CAGR: | 7.23% | Market Size in 2032: | 870.85 USD Mn |

| Segments Covered: | by Raw Material | Virgin PET Recycled PET |

|

| by Grade Type | Low-Density PET Foam High-Density PET Foam |

||

| by End-Use Industry | Building & Construction Wind Energy Marine Packaging Transportation Others |

||

PET Foam Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

PET Foam Market, Key Players are

- Carbon-Core Corp.

- CoreLite

- 3M

- Huntsman International

- Sealed Air

- Wisconsin Foam Products

- Protac Inc.

- Pregis LLC

- Acrylic Depot

- Changzhou Tiansheng New Materials Co. Ltd.

- Sekisui Plastics

- Nitto Denko Corporation

- TORAY INDUSTRIES INC.

- INOAC CORPORATION

- Furukawa Electric Co. Ltd.

- Armacell International SA

- 3A Composites

- Gurit Holding

- Synthos S.A.

- DIAB Group

- H. Ziegler GmbH

- Schweiter Technologies

- BASF SE

- Zotefoams Plc

- Palziv Inc.

- Airex AG

- Composites One

- Feininger (Nanjing) Energy Saving Technology Co. Ltd.

- Gneuss Kunststofftechnik GmbH

- USEON Technology Limited

Others