Pea Protein Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

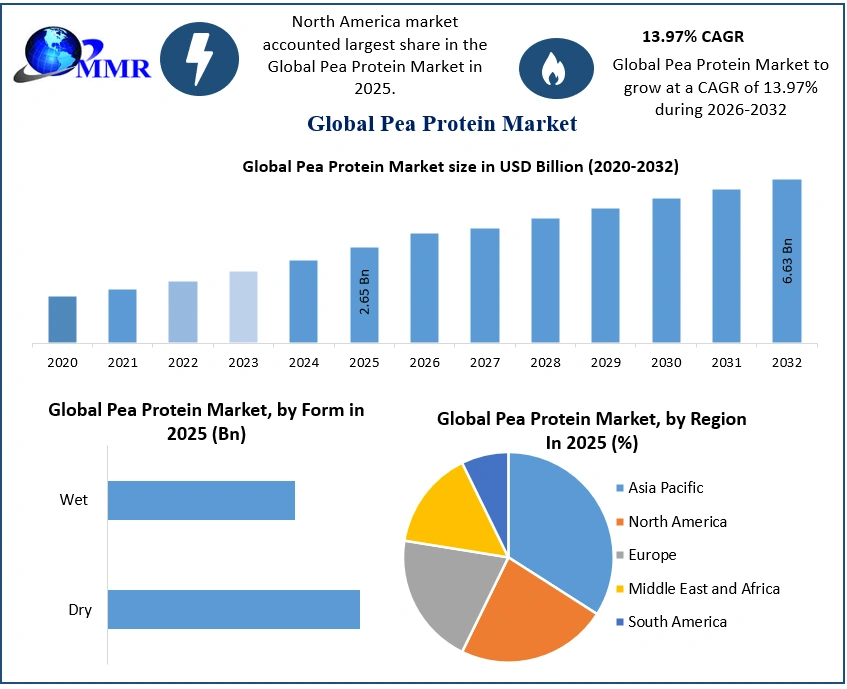

The Pea Protein Market size was valued at USD 2.65 Billion in 2025 and the total Pea Protein revenue is expected to grow at a CAGR of 13.97% from 2026 to 2032, reaching nearly USD 6.63 Billion by 2032.

Pea Protein Market Overview:

Pea protein, sourced from yellow split peas, is widely utilized as both a dietary supplement and a functional ingredient in diverse food products. It serves as a plant-based, dairy-free, and frequently gluten-free alternative to traditional animal proteins. Known for its high protein concentration, well-balanced amino acid profile, and easy digestibility, pea protein has become a popular choice among consumers seeking nutritious, allergen-friendly, and sustainable protein options. The pea protein is a plant-based, sustainable, and allergen-free versions of protein that attract consumers. The pea proteins are derived from yellow peas and it is a digestible and ALS-rich type of protein comparable to protein from eggs. Pea protein is gaining traction in human food and beverage products, dietary supplements, and animal feed.

Pea protein usage is accelerated due to the vegan/flexitarian dietary trends are becoming mainstream, and as more consumers become lactase intolerant (lactose), and/or soy-and-dairy allergic. Pea protein is growing faster as meat substitutes, dairy-free, and sports nutrition subcategories. The addition of pea protein in these segments is propelled in increase in sustainability-focused practices and products, and the desire for clean-label products. Pea protein has a better resource designation than animal-based protein. Innovators are launching better extraction processes, and new product categories are emerging, which are stimulating consumer interest. The growth coherence-driving factor is the growth of e-commerce, which is complemented by expanded retail access to health-based foods in the Pea Protein Market.

To know about the Research Methodology :- Request Free Sample Report

Pea Protein Market Dynamics:

Rising Demand for Plant-Based Protein and Functional Ingredients to Propel Market Growth

The growing global shift toward plant-based diets, combined with increasing consumer demand for clean-label, allergen-free protein sources, is a significant catalyst for the expansion of the pea protein market. For example, Ingredion’s recent launch of VITESSENCE® Pea 100 HD in July 2024 highlights how innovation is addressing consumer needs for texture, softness, and nutrition in cold-pressed bars. This reflects the wider market trend of incorporating pea protein into snacks, bakery items, sports nutrition, dairy alternatives, and plant-based meat products. Health and sustainability concerns further fuel demand, as pea protein is dairy-free, gluten-free, and non-GMO, appealing to consumers with dietary restrictions or ethical considerations. Additionally, partnerships and product innovation by major players like Roquette, Cargill, and Beyond Meat demonstrate how the industry is scaling up production and applications of pea protein to meet rising global demand. With governments promoting sustainable agriculture and protein diversification, and growing awareness of the environmental benefits of plant-based protein over animal-based protein, the pea protein market is poised for rapid growth.

Cost, Taste, and Functional Limitations Hamper Market Growth

The relatively higher cost of production compared to conventional proteins such as soy or whey often restricts mass adoption, particularly in price-sensitive markets. Taste and texture remain persistent hurdles, with many formulations struggling to overcome the characteristic chalky or gritty mouthfeel and pulse flavor. While innovations like Ingredion’s VITESSENCE Pea 100 HD address these issues, widespread improvements are needed across product categories. Infrastructure gaps in processing and supply chains also limit growth. For instance, North America currently dominates the market due to established processing facilities, while Asia-Pacific, though fast-growing, faces challenges in scaling up high-quality pea protein production. Additionally, the lack of uniform global standards for labelling and protein claims creates inconsistency across markets, making it difficult for manufacturers to maintain quality and compliance internationally. The reliance on limited raw material sources, primarily yellow split peas, raises concerns about supply stability. These factors collectively restrain the market’s potential, underscoring the need for innovation, cost optimization, and harmonized regulations to fully realize the pea protein market growth opportunities.

Rising Demand for Clean-Label Proteins Fuels Pea Protein Market Growth

The pea protein market is positioned for significant opportunities as global demand for plant-based nutrition continues to grow. The rising popularity of veganism, flexitarian diets, and clean-label products is creating new pathways for pea protein adoption across food, beverages, and nutraceuticals. Pea protein’s allergen-free, non-GMO, and sustainable profile positions it as a strong alternative to soy and whey, especially among consumers with dietary restrictions. The biggest opportunities lie in the plant-based meat industry, where textured pea protein is used to replicate the fibrous, meat-like texture consumers expect. With global investments in alternative protein startups and partnerships between major players such as Beyond Meat and Nestlé, demand is set to accelerate. Similarly, sports nutrition, protein bars, and dairy alternatives represent high-growth segments where pea protein can deliver functionality and high protein density. Emerging markets in Asia-Pacific and South America provide growth potential, rising disposable incomes, changing diets, and expanding urban populations. The advancements in processing technology, such as flavor masking and protein enrichment, grow applications and consumer acceptance. These opportunities ensure pea protein will remain a cornerstone of the global shift toward sustainable, functional, and health-focused protein solutions.

Pea Protein Market Segmentation:

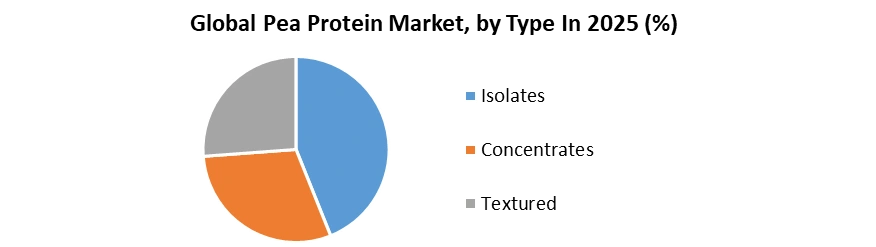

Based on type, the Pea Protein market is segmented into Isolates, Concentrates, and Textured. Among these, pea protein isolates dominate the global market share in 2025 and are expected to maintain their leading position throughout the forecast period. Pea protein isolates are highly refined, containing more than 80–85% protein content on a dry basis, making them a preferred choice for manufacturers seeking high nutritional value and superior functional properties. Their clean taste profile, excellent solubility, and digestibility make them particularly popular in sports nutrition, dietary supplements, and beverages. Isolates meet the rising demand for clean-label, allergen-free, and vegan protein sources, further fueling their adoption in plant-based dairy products, protein powders, and ready-to-drink nutritional beverages. Pea protein concentrates, while lower in protein content (typically 55–65%), retain more starch and fiber. They are widely used in snack foods, baked goods, and nutritional bars, where texture and bulk matter more than protein density. This makes concentrates a cost-effective option for food manufacturers but keeps them behind isolates in market dominance. Textured pea protein, on the other hand, is mainly used as a meat extender or substitute. With its fibrous, meat-like structure, it plays a crucial role in the booming plant-based meat industry, but its Pea Protein Market share remains smaller compared to isolates and concentrates due to its narrower application base.

By Form, the dry pea protein held the largest Pea Protein Market share in 2025, due to its versatility and storage benefits, and is expected to grow at the highest CAGR during 2026-2032. The dry form of pea protein dominates the global market, primarily because of its practical benefits and versatility across industries. Its popularity stems from several advantages: it is easier to transport and store, offers a much longer shelf life compared to the wet form, and provides consistent functionality in a variety of formulations. Dry pea protein is typically available as a powder, making it convenient for manufacturers to handle and integrate into different production processes. This format reduces logistical challenges, lowers storage costs, and ensures reliable performance in end-use applications. Manufacturers prefer the dry form because it allows for precise blending in processed foods, beverages, and nutritional supplements. The powder form ensures accurate dosing and uniform texture, which is essential in large-scale food production. Moreover, dry pea protein delivers high protein concentration, clean-label advantages, and functional properties like solubility and emulsification, which improve product quality. It is widely used in protein bars, bakery items, sports nutrition products, dairy alternatives, and plant-based meats.

Pea Protein Market Regional Insights:

North America dominated the global pea protein market in 2025. The regional market is rising demand for gluten-free products, rising concerns about cardiovascular diseases (CVDs) caused by red meat consumption, and robust growth of the sports nutrition industry in North America. Additionally, the existence of large meat product producers in the United States, such as JBF, Tyson, National Foods, and Cargill, is expected to raise demand for the product as a texturizing agent in meat manufacturing. The rising grain use for bio-based chemicals, such as canola and soy, is expected to reduce their availability as protein components. Therefore, pea protein is expected to become a necessary component.

Asia-Pacific is expected to be the fastest-growing regional pea protein market from 2025-2032. This growth is attributed to the growing consumption of nutrient-fortified functional food products. The rising demand for meat replacements and allergen-friendly sports and fitness supplements. In India and China, favourable regulatory dispositions geared towards the development of the agricultural industry have resulted in adequate raw material supply for manufacturers. The food & beverage industry's strong manufacturing base in China, because of improved raw material access and rising domestic consumption, is expected to drive regional pea protein market growth. Moreover, the expanding hotel and restaurant business, as well as the growing number of retail chains, in supermarkets, are projected to play an important role in boosting the food & beverage industry's growth and, as a result, increasing product demand.

Pea Protein Industry Ecosystem:

Pea Protein Market Competitive Landscape

Biotech giant DuPont (now part of IFF, United States) and Roquette Frères (France) are the two major players in the global pea protein market, representing North America and Europe, respectively.

Using its biotechnology origin and global supply chain, DuPont is able to produce innovative, highly functional pea protein ingredients for niche products such as clinical nutrition, sports nutrition, and plant-based dairy. DuPont's formulating abilities are the real competitive advantage, along with long-standing relationships with food industry stalwarts.

Roquette Frères leads the European pea protein scene and boasts a global footprint as well, including a vertically integrated supply chain and major processing facilities including its new pea protein plant in Canada, and multiple products sold through its NUTRALYS® brand. Roquette is more focused on R&D investment and sustainability to take advantage of food ingredient clean-label trends and provide sustainable solutions and value underneath multiple product categories including beverage applications and meat analogues. DuPont and Roquette are in direct competition on the basis of global footprint, innovation, and capacity to meet/foresee customer demands for high-quality plant-based nutritional ingredients.

Pea Protein Market Key Trends

• Premiumization & Branding

Brands are taking pea protein to the next level with premium, clean-label positioning. For example, Beyond Meat and Nestlé are emphasizing the sustainable aspects, while MyProtein is working on specific blends with added probiotics. Luxury brands are using traceable pea protein and offering QR codes for farm-to-table" transparency.

• Functional Innovations

Better processes also improve taste, and the ways to provide specific textures have improved. Startups like NuCicer are making neutral-tasting, non-GMO pea protein isolates, and Roquette has been making fibrous, meat-like textures. Recent developments in microencapsulation boost stability in beverages and baked goods.

• E-Commerce & DTC Growth

Online B2B platforms like Alibaba continue to impact bulk sales, and DTC options of pea protein are growing as well. Brands like Ghost and KOS are using DTC subscription methods with pea protein sales, and single-serve pea protein sticks in a no-brainer way of selling and growing.

• Work towards a new market

Asia is leading the charge with plant-based snacks and pea proteins for bubble teas. the Middle East is adopting halal-approved protein options, and Latin America is starting to see a surge in simple and inexpensive meat alternatives.

• Sustainability

Upcycled versions of pea protein reduce food waste problems post-harvest; meanwhile, "carbon-neutral" production using Pea protein is gaining momentum in the food industry, and regenerative farming practices are helping modernize eco-friendly sourcing.

Pea Protein Market Key Developments

In June 2025, Roquette Frères (France/Global) launched its NUTRALYS® PRO premium pea protein isolate, which has 90% protein content and a neutral flavour profile designed for high-performance sports nutrition and clean-label meat alternatives. The new ingredient has improved solubility and is planned to launch first in North America, with a global rollout scheduled for 2026.

On July 15, 2024, Ingredion launched VITESSENCE Pea 100 HD, a North American-grown pea protein designed to improve cold-pressed bars’ texture and shelf life. The ingredient delivers softness, smooth texture, and reduced chalky or gritty mouthfeel compared to soy, whey, and other plant proteins. With 84% protein content (dry basis), it supports “good” or “excellent” protein claims while ensuring balanced taste and clean labeling. Tested in sensory and shelf-life studies, VITESSENCE Pea 100 HD outperformed competitors and gained consumer preference. Ingredion’s innovation targets rising demand for nutritious, plant-based protein bars that maintain superior eating experiences across their shelf life.

Pea Protein Market Scope: Inquire before buying

| Pea Protein Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 2.65 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 13.97% | Market Size in 2032: | USD 6.63 Bn. |

| Segments Covered: | by Type | Isolates Concentrates Textured |

|

| by Form | Dry Wet |

||

| by Source | Split yellow peas Lentils Chickpeas Others |

||

| by Application | Animal Feed Bakery Goods Beverages Dietary Supplements Infant Nutrition Meat Substitutes Personal Cosmetics Others |

||

| by Distribution Channel | Online Channels Pharmacies Specialty Stores Supermarkets / Hypermarkets Others |

||

Pea Protein Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Pea Protein Market, Key players:

Major Pea Protein Providers in North America:

1. DuPont (United States)

2. Ingredion (United States)

3. Puris (United States)

4. The Scoular Company (United States)

5. Burcon (Canada)

6. AGT Food and Ingredients (Canada)

8. Axiom Foods, Inc. (United States)

Leading Pea Protein Manufacturers in Europe:

1. Roquette Frères (France)

2. Cosucra Groupe Warcoing SA (Belgium)

5. Emsland Group (Germany)

6. Glanbia PLC (Ireland)

7. Kerry (Ireland)

Key Players of Pea Protein Market in APAC:

1. Yantai Shuangta Foods Co., Ltd (China)

2. Shandong Jianyuan Group (China)

3. ET-Chem (China)

4. Shandong Xiangchi Jianyuan Bio-Tech Co., Ltd. (China)

6. Shandong Huatai Food (China)

7. Shuangta Food (China)

8. Shandong Oriental Herbest Bio-Tech Co., Ltd. (China)

FAQs:

1. What are the growth drivers for the Pea Protein market?

Ans. Growing Demand for Plant-Based Proteins, Rising Vegan and Vegetarian Population factors are expected to be the major drivers for the market.

2. What is the major restraint for the Pea Protein market growth?

Ans. Competition from Other Plant Proteins is expected to be the major restraining factor for the market growth.

3. Which region is expected to lead the global Pea Protein market during the forecast period?

Ans. North America is expected to lead the global market during the forecast period.

4. What is the projected market size & and growth rate of the Pea Protein Market?

Ans. The Pea Protein Market size was valued at USD 2.65 Billion in 2025 and the total Pea Protein revenue is expected to grow at a CAGR of 13.97% from 2026 to 2032, reaching nearly USD 6.63 Billion by 2032.

5. What segments are covered in the Pea Protein Market report?

Ans. The segments covered in the Pea Protein market report are type, form, source, application, distribution channel, and region.