Molded Fiber Bowls Market Size Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

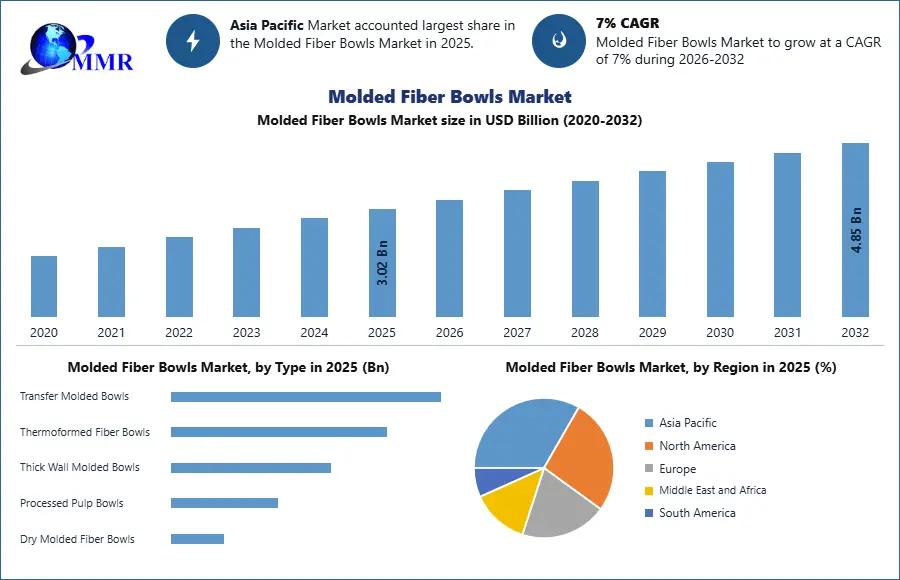

The Molded Fiber Bowls Market was valued at USD 3.02 Billion in 2025 and is estimated to grow at a CAGR of 7.0% over the forecast period, reaching USD 4.85 Billion by 2032.

The global Molded Fiber Bowls market report is a comprehensive analysis of the industry, market, and key players. The report has covered the market by demand and supply-side by segments. The global Molded Fiber Bowls report also provides trends by market segments, technology, and investment with a competitive landscape.

To know about the Research Methodology :- Request Free Sample Report

Molded Fiber Bowls Market Overview

The Molded Fiber Bowls Market refers to rigid and semi-rigid bowl formats manufactured from recycled paper pulp, virgin wood fiber, bagasse, bamboo pulp, wheat straw, and other plant-based fibers through transfer molded, thermoformed, or advanced dry molded processes. These bowls are primarily used in foodservice, takeaway, meal delivery, institutional catering, retail-ready packaged foods, and event-based disposable dining. Their commercial relevance has increased because they combine compostability or recyclability potential with heat resistance, stackability, grease tolerance, and compatibility with sustainability-led procurement standards. In functional terms, molded fiber bowls have evolved from a low-cost disposable serving format into a strategic product class within sustainable foodservice packaging, eco friendly food packaging, biodegradable bowls, and compostable tableware.

The growth trajectory of the Molded Fiber Bowls Market is strongly linked to structural pressure on single-use plastic packaging. The European Commission states that the Single-Use Plastics Directive aims to reduce the impact of plastic products on the environment while promoting innovative and sustainable alternatives, and official EU guidance explicitly recognizes paper-based products without plastic lining or coating as more sustainable alternatives in relevant applications. In parallel, the EPA continues to highlight single-use foodservice plastics as a major contributor to plastic pollution streams. This regulatory and environmental alignment has accelerated buyer migration toward fiber-based bowls in restaurants, catering chains, educational institutions, and convenience-led packaged food channels.

Technology development has also materially improved market readiness. The category is no longer limited to basic thick-wall pulp formats. Newer thermoformed fiber, precision-molded pulp, and dry molded fiber systems are improving rim finish, stiffness, moisture tolerance, nesting efficiency, and branding flexibility. These process improvements are particularly important because bowls face tougher performance requirements than flat plates in hot, wet, oily, and delivery-oriented applications. As a result, the Molded Fiber Bowls Market forecast has become more favorable, especially in premium takeaway, institutional catering, prepared meals, and supermarket deli packaging, where functionality used to be a barrier to fiber adoption.

Demand visibility remains strong because foodservice volume is large and recurring. The USDA notes that the National School Lunch Program serves students in more than 95,000 schools, while public procurement and food-away-from-home channels continue to favor lower-waste serving formats. This means molded fiber bowls are supported not only by consumer preference but also by repeat institutional purchasing, which is critical for long-term market growth.

Molded Fiber Bowls Market Growth Catalysts

Single-Use Plastic Regulation Accelerated Fiber Substitution

The most powerful catalyst for the Molded Fiber Bowls Market was the tightening of regulation around single-use plastic packaging. The European Commission’s SUP framework was designed to reduce the environmental impact of problematic plastic items while encouraging sustainable alternatives, and the policy direction has strengthened purchasing confidence for fiber-based serving formats across Europe. Beyond Europe, public-sector and institutional buyers increasingly treat molded fiber bowls as a practical compliance-led replacement rather than a niche sustainability option. This regulatory pull has been particularly important for bowls because they are heavily used in takeaway meals, salad serving, hot food applications, and prepared food counters, which are all segments under scrutiny for packaging waste reduction.

Foodservice and Institutional Demand Increased Volume Stability

The Molded Fiber Bowls Market also expanded because foodservice demand remained structurally resilient. Schools, hospitals, quick-service restaurants, workplace cafeterias, and organized catering programs require high-volume disposable serveware with predictable performance. USDA-linked meal infrastructure demonstrates how large institutional channels continuously consume foodservice packaging, and this recurring demand profile supports bowl adoption more than many other molded fiber formats. Bowls are especially favored in soups, grain meals, curries, noodles, frozen desserts, and deli-ready applications, making them more versatile than single-use trays in many serving environments. That versatility improved reorder rates and strengthened manufacturing scale economics.

Manufacturing Innovation Improved Product Performance

The Molded Fiber Bowls Market gained traction because performance gaps narrowed. New production systems are improving shape consistency, wall uniformity, barrier compatibility, and premium finish, while large-scale investments in thermoforming and dry fiber technology are increasing industrial throughput. This matters because bowl buyers do not only need compostability claims; they need stackability, leak resistance, acceptable lid fit, and brand-quality presentation. Investments by manufacturers and equipment providers indicate that the category is moving beyond commodity pulp ware toward engineered foodservice packaging suitable for mainstream retail and restaurant use.

Molded Fiber Bowls Market Limitations

Cost Competitiveness Remained Uneven Against Low-Cost Plastics

A major limitation in the Molded Fiber Bowls Market was price sensitivity. Despite stronger sustainability demand, molded fiber bowls often remained more expensive than legacy plastic or foam alternatives in price-driven channels, particularly where waste disposal regulation is weak or composting infrastructure is underdeveloped. This restricted penetration in small independent foodservice outlets and in developing markets where buyers continue to prioritize unit economics over lifecycle packaging performance.

Coating and End-of-Life Complexity Slowed Full Circularity Claims

Another limitation was the tension between product performance and true circularity. Bowls used for oily, wet, or hot foods may require coatings or additives to improve grease and moisture resistance. When these layers are not carefully selected, compostability, recyclability, or consumer sorting clarity can become more complex. That has created hesitation among some institutional buyers who want unambiguous end-of-life performance rather than marketing-led sustainability claims.

Molded Fiber Bowls Market Future Growth Potential

Meal Delivery and Ready-to-Eat Packaging Created a Premium Growth Pocket

One of the strongest emerging opportunities in the Molded Fiber Bowls Market lies in premium takeaway, food delivery, and chilled or hot ready-meal formats. Bowls are increasingly preferred for single-portion meals, salad kits, grain bowls, frozen desserts, and heat-and-eat servings because they offer both branding surface and product protection. As food retail and convenience dining continue to converge, molded fiber bowls are likely to gain share in higher-value packaged meal formats that previously depended on plastic tubs or laminated containers.

Asia Pacific Offered the Broadest Untapped Volume Upside

The most attractive geographic opportunity in the Molded Fiber Bowls Market remains Asia Pacific, where broader molded fiber packaging already has the largest regional share and where food delivery, urban foodservice, and regulatory interest in packaging sustainability continue to expand. The region benefits from large food consumption volumes, growing organized retail, and strong fiber raw-material access in several markets. This creates favorable conditions for both low-cost production and domestic consumption growth.

Molded Fiber Bowls Market Operational and Strategic Barriers

Market Fragmentation Reduced Brand Standardization

The Molded Fiber Bowls Market remained fragmented across global packaging groups, regional foodservice suppliers, specialist compostable brands, and contract manufacturers. This fragmentation limited standardization in quality, lid compatibility, coating chemistry, and certification messaging. As a result, large buyers often faced inconsistent product performance across vendors, which slowed category consolidation.

Scaling Specialized Bowl Formats Required Capital and Process Discipline

Bowls are not the easiest molded fiber format to scale because they need deeper draw, better rim precision, more robust nesting behavior, and stronger wet-food performance than many trays or flat serviceware items. That meant industrial scaling required investment in forming, trimming, automation, and quality assurance. The recent wave of plant expansion and equipment partnerships shows that the industry is addressing this issue, but the barrier remains meaningful.

Molded Fiber Bowls Market Current and Future Market Trends

Dry Molded Fiber and Precision Thermoforming Became Commercially Important

A major industry trend in the Molded Fiber Bowls Market is the shift toward higher-precision molded fiber manufacturing. Dry fiber and advanced wet-forming platforms are enabling better aesthetics, lighter weight, improved productivity, and higher-function food-contact formats. This is strategically important because the market is moving from basic eco-substitution to performance-led adoption.

Regenerative and Alternative Fiber Inputs Strengthened Product Positioning

The important market growth trend is the use of bagasse, perennial grasses, and other renewable non-wood fibers to differentiate molded bowl products. Better Earth’s 2025 retail launch built its story around regenerative farm-sourced fibers, illustrating how raw-material narrative is becoming part of product positioning. This trend matters because buyers increasingly want both sustainable performance and traceable material storytelling.

Molded Fiber Bowls Market Segments Analysis

Molded Fiber Bowls Market Segmentation, by Type

Type

- Transfer Molded Bowls

- Thermoformed Fiber Bowls

- Thick Wall Molded Bowls

- Processed Pulp Bowls

- Dry Molded Fiber Bowls

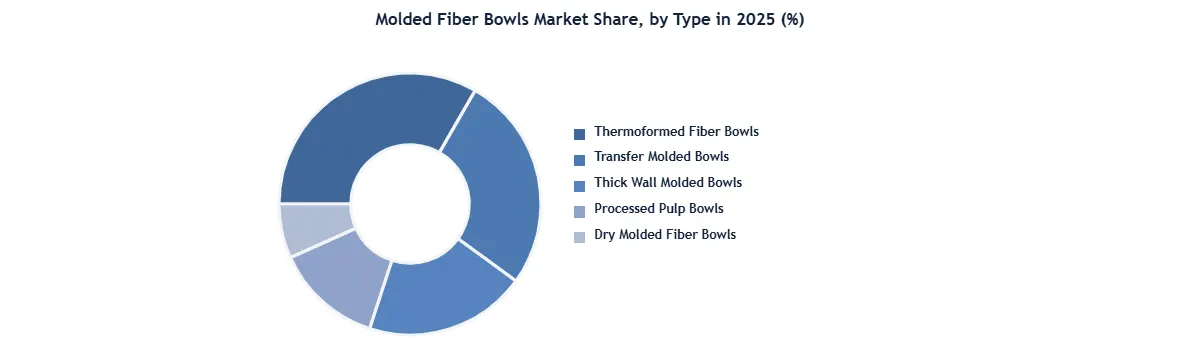

In 2025, the Thermoformed Fiber Bowls segment was the largest in the Molded Fiber Bowls Market because it offered the best balance between functional performance, commercial scalability, and premium foodservice presentation. Thermoformed bowls were increasingly adopted in takeaway meals, institutional catering, deli foods, and ready-to-eat packaging because they provided smoother surfaces, more precise dimensions, stronger rim structure, and improved stackability compared with traditional lower-finish pulp formats. The segment also benefited from rising demand for bowls that could handle oily, moist, and hot food applications without losing structural integrity. Adoption was particularly strong among organized foodservice buyers, retail food brands, and contract caterers that required consistent appearance and operational efficiency across high-volume packaging lines. In addition, thermoformed products fit better with premium compostable packaging positioning, which helped them capture demand in markets where sustainability and presentation increasingly moved together. This dominance in 2025 was therefore not only a function of volume, but also of application breadth, usability, and compatibility with modern foodservice requirements.

Molded Fiber Bowls Market Segmentation, by Material

- Bagasse

- Recycled Paper Pulp

- Virgin Wood Pulp

- Bamboo Fiber

- Wheat Straw Fiber

- Blended Natural Fibers

In 2025, Bagasse was the largest material segment in the Molded Fiber Bowls Market because it aligned most effectively with foodservice economics, compostability expectations, and global supply visibility. Bagasse offered a commercially proven route to sturdy disposable bowls with good heat tolerance and acceptable grease resistance, making it suitable for high-turnover restaurant and catering applications. It also benefited from its positioning as an agricultural byproduct-based material, which appealed to sustainability-focused buyers seeking reduced virgin plastic and lower-fossil packaging narratives. Demand was especially strong in Asian markets and export-oriented supply chains, where sugarcane-based molded tableware already had scale advantages. As a result, bagasse led not just on raw material availability, but on buyer familiarity, performance credibility, and manufacturing readiness.

Molded Fiber Bowls Market Segmentation, by End Use

- Quick Service Restaurants

- Full Service Restaurants

- Cafeterias and Institutional Catering

- Retail Food Packaging

- Food Delivery and Takeaway

- Events and Outdoor Catering

- Household Use

In 2025, Food Delivery and Takeaway was the largest end-use segment in the Molded Fiber Bowls Market because bowls are inherently suited to portable, single-portion meals. The segment dominated due to strong demand for soups, noodles, rice meals, salads, and dessert servings that require a deep, liddable, rigid container rather than a flat plate. Delivery-led food formats also created greater need for leak resistance, stackability, and sustainable packaging visibility, which supported rapid adoption of molded fiber bowls. As meal delivery ecosystems expanded, buyers increasingly selected bowls that reinforced both operational convenience and eco-friendly brand perception. That combination of functionality and sustainability made delivery and takeaway the most commercially important application area in 2025.

Molded Fiber Bowls Market Regional Analysis

In 2025, Asia Pacific was the leading region in the Molded Fiber Bowls Market because it combined large-scale foodservice demand, strong manufacturing capacity, favorable raw-material availability, and increasingly supportive policy direction on sustainable packaging. The region had already established leadership in the broader molded fiber packaging and molded fiber tableware industries, which gave bowl manufacturers an existing supply base, labor ecosystem, and converting infrastructure. Asia Pacific also benefited from dense urban populations, fast-growing takeaway and convenience food channels, and expanding organized retail, all of which supported high-volume use of bowl-based food packaging. From a policy standpoint, the region continued to respond to plastic waste pressure through tighter sustainability expectations and procurement shifts, even though the pace varied by country. Its technology position improved as local and multinational manufacturers invested in better thermoforming, automation, and fiber-conversion capacity. Infrastructure strength, including food processing, packaging conversion, export logistics, and raw-material access, further reinforced regional dominance. For these reasons, Asia Pacific remained the most commercially attractive and operationally advantaged region in 2025.

Recent Developments

February 2025: Better Earth launched its Farmer’s Fiber Retail Collection, a new U.S.-made line of BPI-certified compostable molded fiber plates and bowls built around regenerative farm-sourced fibers. From a market perspective, this development was important because it pushed the molded fiber bowl category further into branded retail and consumer-facing channels rather than leaving it confined to back-of-house foodservice procurement. The launch also signaled a shift in category competition: molded fiber products are no longer being sold only on biodegradability and plastic substitution, but increasingly on material story, domestic sourcing, climate positioning, and premium shelf appeal. The product line included bowl formats manufactured in Tennessee and positioned as alternatives to petroleum-based plastics and virgin wood fiber tableware. For the Molded Fiber Bowls Market, the strategic importance lies in its proof that molded bowls can command differentiated positioning through regenerative agriculture messaging, not just functional packaging performance. That strengthens category value perception and expands the addressable market into higher-margin retail sustainable dining segments.

July 2025: Genera announced the completion of its $340+ million expansion in Vonore, Tennessee, describing the facility as a state-of-the-art American manufacturing site for sustainable molded fiber packaging. The company stated that the expanded site would support annual capacity of more than 30,000 tons, equivalent to over 2 billion molded fiber pieces, while also creating over 200 jobs. This was a major signal for the Molded Fiber Bowls Market because bowl economics depend heavily on large-scale throughput, automation, and reliable fiber supply. Expansions of this magnitude reduce a key industry barrier: limited industrial capacity for high-volume foodservice conversion. Beyond volume, the project also indicated rising confidence from investors and manufacturers that molded fiber packaging demand will remain durable over the long term. Strategically, this kind of capacity buildout supports better unit-cost competitiveness, shorter lead times, and stronger ability to serve national foodservice and retail programs, all of which are critical for broader molded bowl penetration.

September 2025: Fiberdom and Kiefel entered a strategic partnership to accelerate fiber-based packaging innovation using advanced dry forming technology. The collaboration combined Fiberdom’s material platform with Kiefel’s processing and machinery expertise to expand scalable, cost-effective fiber applications for packaging manufacturers and converters. For the Molded Fiber Bowls Market, this development matters because future category leadership will depend not only on sustainable materials but also on machine-enabled precision, throughput, and product consistency. Dry forming technology has the potential to improve surface finish, reduce material usage, and expand the range of high-function fiber food-contact products that can compete with plastic on both performance and economics. The partnership therefore represented more than a technology announcement; it showed that the ecosystem is moving toward industrial-grade platform building. That is strategically significant for bowls, where rim quality, structural performance, and manufacturing repeatability directly influence commercial adoption in takeaway, retail meal packaging, and institutional foodservice.

Global Molded Fiber Bowls Market Scope: Inquire before buying

| Molded Fiber Bowls Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 3.02 Billion |

| Forecast Period 2026-2032 CAGR: | 7% | Market Size in 2032: | USD 4.85 Billion |

| Segments Covered: | by Type | Thermoformed Fiber Bowls Transfer Molded Bowls Thick Wall Molded Bowls Processed Pulp Bowls Dry Molded Fiber Bowls |

|

| by Material | Bagasse Recycled Paper Pulp Virgin Wood Pulp Bamboo Fiber Wheat Straw Fiber Blended Natural Fibers |

||

| by End Use | Food Delivery and Takeaway Quick Service Restaurants Full Service Restaurants Cafeterias and Institutional Catering Retail Food Packaging Events and Outdoor Catering Household Use |

||

| by Distribution Channel | Direct Sales Distributors and Wholesalers Retail Stores E-Commerce Platforms Foodservice Procurement Contracts |

||

Key Players/Competitors Profiles Covered in the Molded Fiber Bowls Market Report in Strategic Perspective

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- Genpak LLC

- Sabert Corporation

- Eco-Products, Inc.

- Dart Container Corporation

- Novolex Holdings, LLC

- Georgia-Pacific LLC

- International Paper Company

- Stora Enso Oyj

- Cascades Inc.

- CKF Inc.

- Duni Group

- BioPak Pty Ltd

- Vegware Ltd

- PulPac AB

- TekniPlex Consumer Products

- Genera Inc.

- Better Earth

- Graphic Packaging International, LLC

- Pakka Limited

- Seda International Packaging Group

- Guangdong Shaoneng Group Co., Ltd.

- PulpWorks, Inc.

- WinCup, Inc.