Medical Non-Woven Disposable Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2029

Overview

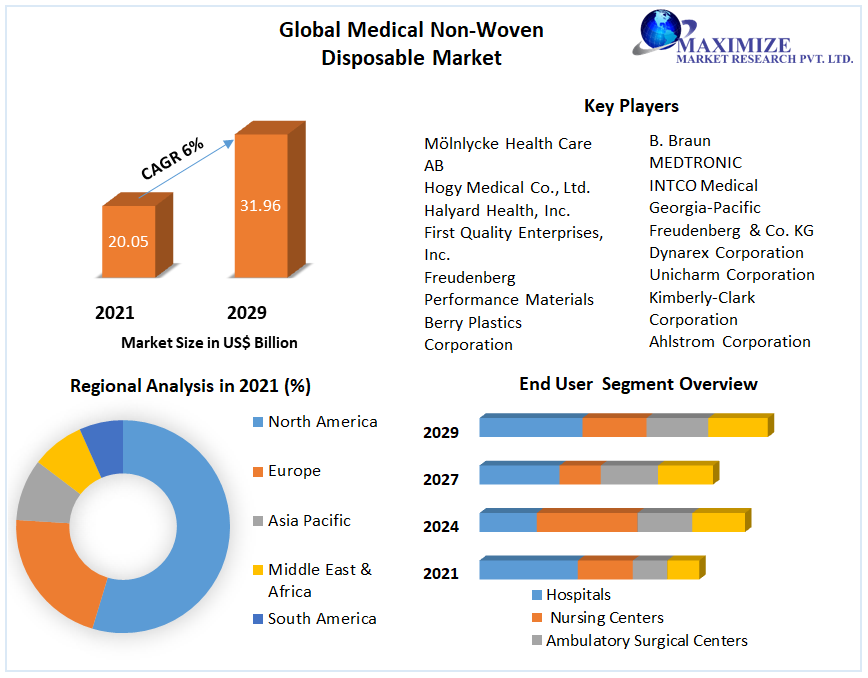

Medical Non-Woven Disposable Market size is expected to grow at a CAGR of 6% during the forecast period and the market size is expected to reach nearly US$ 31.96 Bn. by 2029.

The Global Medical Non-Woven Disposable Market growth rate is driven by the factors including the rising elderly population and increasing cases of incontinence. Furthermore, changing lifestyle, unhealthy diet and excessive alcohol consumption and tobacco smoking lead the people towards chronic conditions such as diabetes, obesity, and chronic cough. These chronic conditions will lead to onset of incontinence due to stressed urinary sphincter. Thus, drive the market through the forecast period. To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

The report study has analyzed revenue impact of COVID -19 pandemic on the sales revenue of market leaders, market followers and market disrupters in the report and same is reflected in our analysis.

Moreover, rising cases of hospital-acquired infections also expected to drive the market. It is expected that nearly 5 million women in the UK are suffering from incontinency in the year 2017. Factors including technological advancements such as disposable incontinence underwear, biodegradable incontinence are expected to drive the Global Medical Non-Woven Disposable Market through the forecast period.

In 2017, North America held the highest market share. The Global Medical Non-Woven Disposable Market growth is coupled with increasing count of the aging population, improved healthcare infrastructure, rising per capita spending on healthcare, improving hygiene habits and favorable government regulations. Other factors including the high consumption rate of advanced medical products and a comparatively higher level of consciousness for hygiene also expected to drive the Global Medical Non-Woven Disposable Market through the forecast period.

Asia-Pacific is expected to have a higher growth rate in the forecast period coupled with developing economies such as China and India. These countries provide an increase in healthcare infrastructure, rising disposable income and thus, drive the market. In addition, the ongoing improvement of the health care infection prevention standards would further drive the growth of Global Medical Non-Woven Disposable Market.

Incontinence products held the highest market share in 2017. The Global Medical Non-Woven Disposable Market growth is driven by the rising cases of incontinence and the introduction of innovative products, such as thinner and rustle-free diapers. The market is also expected to grow in the future period due to an aging population, particularly in U.S., U.K., and China. Rising demand for surgical nonwoven products such as nonwoven gowns, drapes, masks, caps, sheets, and gauze for preventing cross-infection in healthcare facilities also expected to drive the Global Medical Non-Woven Disposable Market.

The objective of the report is to present comprehensive Lobal Medical Non-Woven Disposable Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with analysis of complicated data in simple language. The report covers all the aspects of industry with dedicated study of key players that includes market leaders, followers and new entrants by region. PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors by region on the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give clear futuristic view of the industry to the decision makers.

The report also helps in understanding Lobal Medical Non-Woven Disposable Market North America for Asia Pacific dynamics, structure by analyzing the market segments, and project the Lobal Medical Non-Woven Disposable Market North America for Asia Pacific size. Clear representation of competitive analysis of key players by type, price, financial position, product portfolio, growth strategies, and regional presence in the Lobal Medical Non-Woven Disposable Market North America for Asia Pacific make the report investor’s guide.

Scope of the Global Medical Non-Woven Disposable Market: Inquire before buying

| Global Medical Non-Woven Disposable Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2021 | Forecast Period: | 2022-2029 |

| Historical Data: | 2017 to 2021 | Market Size in 2021: | US $ 20.05 Bn. |

| Forecast Period 2022 to 2029 CAGR: | 6% | Market Size in 2029: | US $ 31.96 Bn. |

| Segments Covered: | by Product | •Incontinence Products Disposable underwear Cotton pads Panty Shields Disposable diapers• Ultra-absorbent• Super-absorbent• Biodegradable o Surgical nonwoven products Surgical Masks Surgical Drapes Shoe covers Surgical caps Surgical gowns Sterile nonwoven swabs Others |

|

| by Material | •Polypropylene o Polyethylene o Acetate o Rayon o Polyamides & Polyester o Acrylic o Others |

||

| by End User | o Hospitals o Nursing Centers o Ambulatory Surgical Centers o Clinics |

||

Medical Non-Woven Disposable Market, by Region:

• North America

o U.S.

o Canada

• Europe

o Germany

o UK

o France

o Spain

o Italy

• Asia Pacific

o China

o India

o Japan

o Australia

• Latin America

o Argentina

o Brazil

o Mexico

• Middle East and Africa

o South Africa

o Saudi Arabia

Medical Non-Woven Disposable Market Key Players are:

•Mölnlycke Health Care AB

•Hogy Medical Co., Ltd.

•Halyard Health, Inc.

•First Quality Enterprises, Inc.

•Freudenberg Performance Materials

•Berry Plastics Corporation

•Asahi Kasei Corporation

•Precision Fabrics Group, Inc.

•Paul Hartmann Ag

•Svenska Cellulosa Aktiebolaget

•Domtar Corporation

•Swedish Cellulosa Aktiebolaget SCA

•Cardinal Health

•B. Braun

•MEDTRONIC

•INTCO Medical

•Georgia-Pacific

•Freudenberg & Co. KG

•Dynarex Corporation

•Unicharm Corporation

•Kimberly-Clark Corporation

•Ahlstrom Corporation

•Medline Industries

•First Quality Enterprises

Frequently Asked questions

1. What is the market size of the Global Medical Non-Woven Disposable Market in 2021?

Ans. The market size Global Medical Non-Woven Disposable Market in 2021 was US$ 20.05 Billion.

2. What are the different segments of the Global Medical Non-Woven Disposable Market?

Ans. The Global Medical Non-Woven Disposable Market is divided into Product, Material and End User .

3. What is the study period of this market?

Ans. The Global Medical Non-Woven Disposable Market will be studied from 2021 to 2029.

4. Which region is expected to hold the highest Global Medical Non-Woven Disposable Market share?

Ans. The Asia Pacific dominates the market share in the market.

5. What is the Forecast Period of Global Medical Non-Woven Disposable Market?

Ans. The Forecast Period of the market is 2022-2029 in the market.