Liquid Cooling System Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

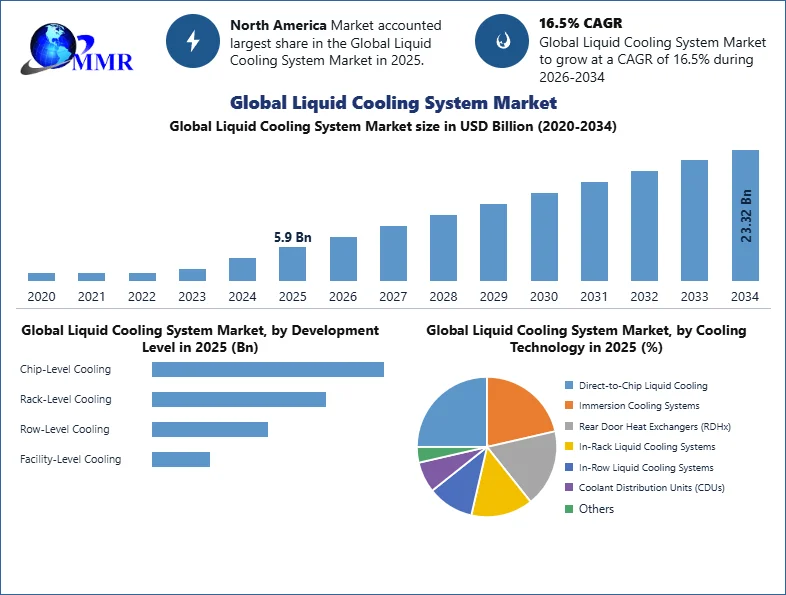

Liquid Cooling System Market size was valued at US$ 5.9 Bn. in 2025 and the total revenue is expected to grow at a CAGR of 16.5% through 2026 to 2034, reaching nearly US$ 23.32 Bn.

Liquid Cooling System Market Overview:

Liquid cooling is a form of active thermal management system that removes thermal energy from electronic applications using a pumped liquid. A liquid cooling system has a higher thermal transfer efficiency than traditional cooling systems because to its high-power modules. Furthermore, the liquid cooling technology provides an effective cooling solution while also helping to reduce noise generated by higher processor units. To circulate the chilled liquid across electronic applications, you will need a circulating pump and connect hoses.

To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

Liquid Cooling System Market Dynamics:

The rising demand for liquid cooling systems from the gaming and IT industries is expected to drive market growth during the forecast period 2026-2034. Besides, the global market is being driven by the requirement for increased liquid cooling system-based data centres as a result of the large number of data being generated.

Due to an increase in demand for liquid cooling systems from Smartphone manufacturers throughout the world, the Liquid Cooling System Market is expected to grow significantly during the forecast period. Furthermore, technological advancements in the IT sector are expected to provide lucrative chances for the Liquid Cooling System Market to grow.

The significant maintenance costs associated with liquid cooling systems, on the other hand, are limiting market growth. During the forecast period, however, the development of portable liquid cooling systems for in-build server rooms and sectors with mild temperatures is expected to provide a lucrative potential for the Liquid Cooling System Market to grow.

Liquid Cooling System Market Segment Analysis:

By deployment level, the liquid cooling system market is segmented into chip-level cooling, rack-level cooling, row-level cooling, and facility-level cooling. In 2025, chip-level cooling held the largest market share, driven by rising use of high-density CPUs, GPUs, and AI accelerators that require heat removal directly at the processor level. Rack-level cooling also gained strong adoption as operators deployed coolant distribution units, rear-door heat exchangers, and liquid-ready racks to support AI and HPC workloads. Row-level and facility-level cooling remained important for broader thermal management, particularly in retrofitted data centers, commercial HVAC, and industrial cooling environments. Direct-to-chip cooling is gaining preference because it removes heat at the source and supports higher rack densities in AI and HPC infrastructure.

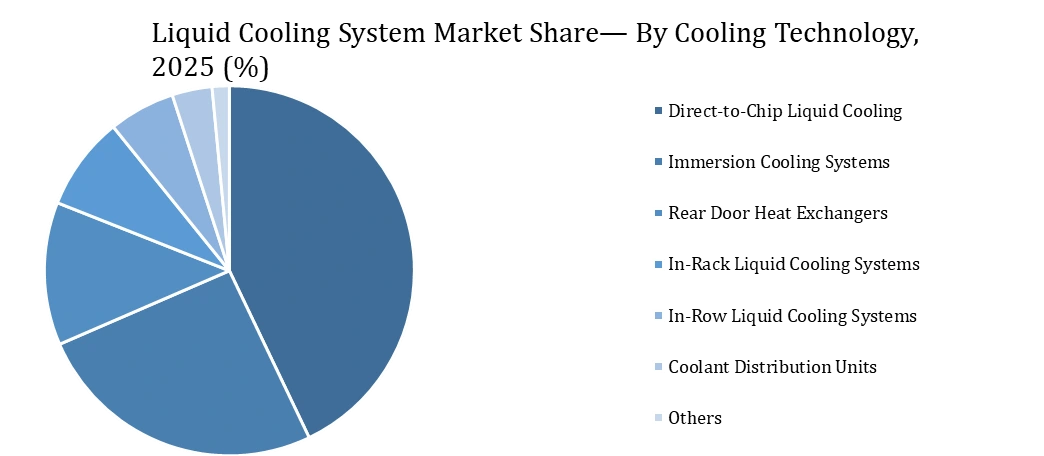

By cooling technology, the market is segmented into direct-to-chip liquid cooling, immersion cooling systems, rear door heat exchangers, in-rack liquid cooling systems, in-row liquid cooling systems, coolant distribution units, and others. Direct-to-chip liquid cooling led the market in 2025 because it is commercially mature, scalable, and highly suitable for AI servers, hyperscale data centers, and high-performance computing systems. Immersion cooling is expanding quickly because it can support extreme heat loads by submerging servers or components in dielectric fluids. Rear-door heat exchangers, in-rack, and in-row liquid cooling systems are increasingly used in retrofit environments where operators need liquid cooling without fully redesigning the data hall. Secondary data reports direct-to-chip at 42.85% share in 2025, while immersion cooling is highlighted as one of the fastest-growing technologies.

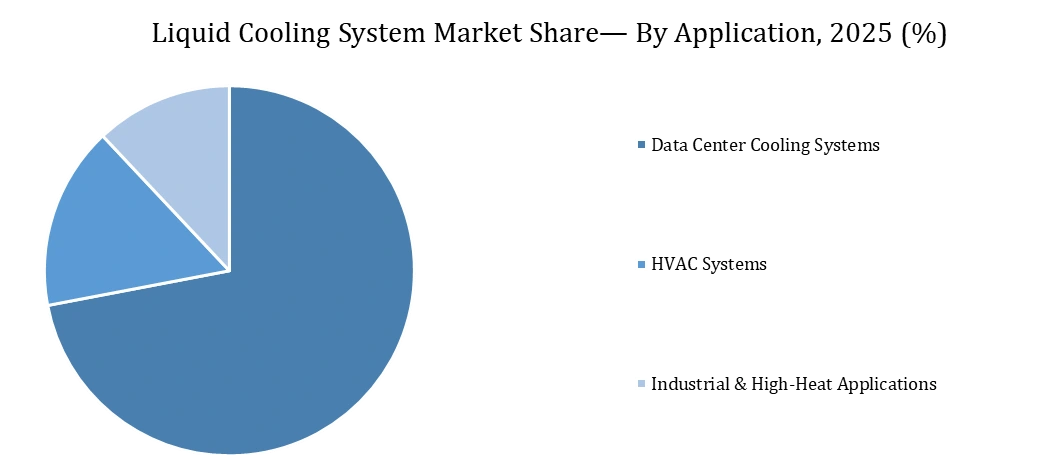

By application, the liquid cooling system market is segmented into data center cooling systems, HVAC systems, and industrial & high-heat applications. Data center cooling systems accounted for the largest share in 2025, supported by rapid growth in hyperscale data centers, colocation facilities, AI/HPC clusters, and enterprise data centers. Rising rack power density has made conventional air cooling less effective, pushing operators toward direct liquid cooling, immersion cooling, and hybrid liquid-air architectures. HVAC systems represented a meaningful share due to adoption in commercial, industrial, district cooling, and green building applications, while industrial and high-heat applications gained demand from semiconductor manufacturing, electronics cooling, EV battery testing, industrial process cooling, and high-performance laboratories. The data center liquid cooling market was valued at USD 6.7 billion in 2025, supported by AI, machine learning, and high-performance computing workloads.

By end user, the market is segmented into data center operators, MEP & engineering ecosystem, and industrial & institutional users. Data center operators held the dominant share in 2025, led by hyperscalers, colocation providers, and enterprise facilities deploying liquid cooling to manage AI workloads, GPU clusters, and high-density compute environments. The MEP and engineering ecosystem, including MEP contractors, EPC companies, design consultants, system integrators, and facility management companies, formed the second-largest group because liquid cooling projects require specialized design, installation, commissioning, and lifecycle maintenance. Industrial and institutional users, including manufacturing facilities, research labs, government facilities, healthcare facilities, and advanced electronics sites, adopted liquid cooling where high heat loads, equipment reliability, and energy efficiency are critical. Secondary sources show strong growth in data center cooling and liquid cooling due to cloud computing, AI, edge computing, and energy-efficient thermal management demand.

Liquid Cooling System Market Regional Insights:

North America is expected to dominate the Liquid Cooling System Market during the forecast period 2026-2034. North America is expected hold the largest market share of xx% by 2034. This is due to the presence of leading market players, as well as an increase in artificial intelligence-based applications across key industries in the North America region. These are the major factors that drive the growth of this region in the Liquid Cooling System Market during the forecast period 2026-2034.

Asia Pacific is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. This is due to increased industrialization and urbanization in the Asia-Pacific region.

The objective of the report is to present a comprehensive analysis of the Global Liquid Cooling System Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Global Liquid Cooling System Market dynamic, structure by analyzing the market segments and project the Global Liquid Cooling System Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Global Liquid Cooling System Market make the report investor’s guide.

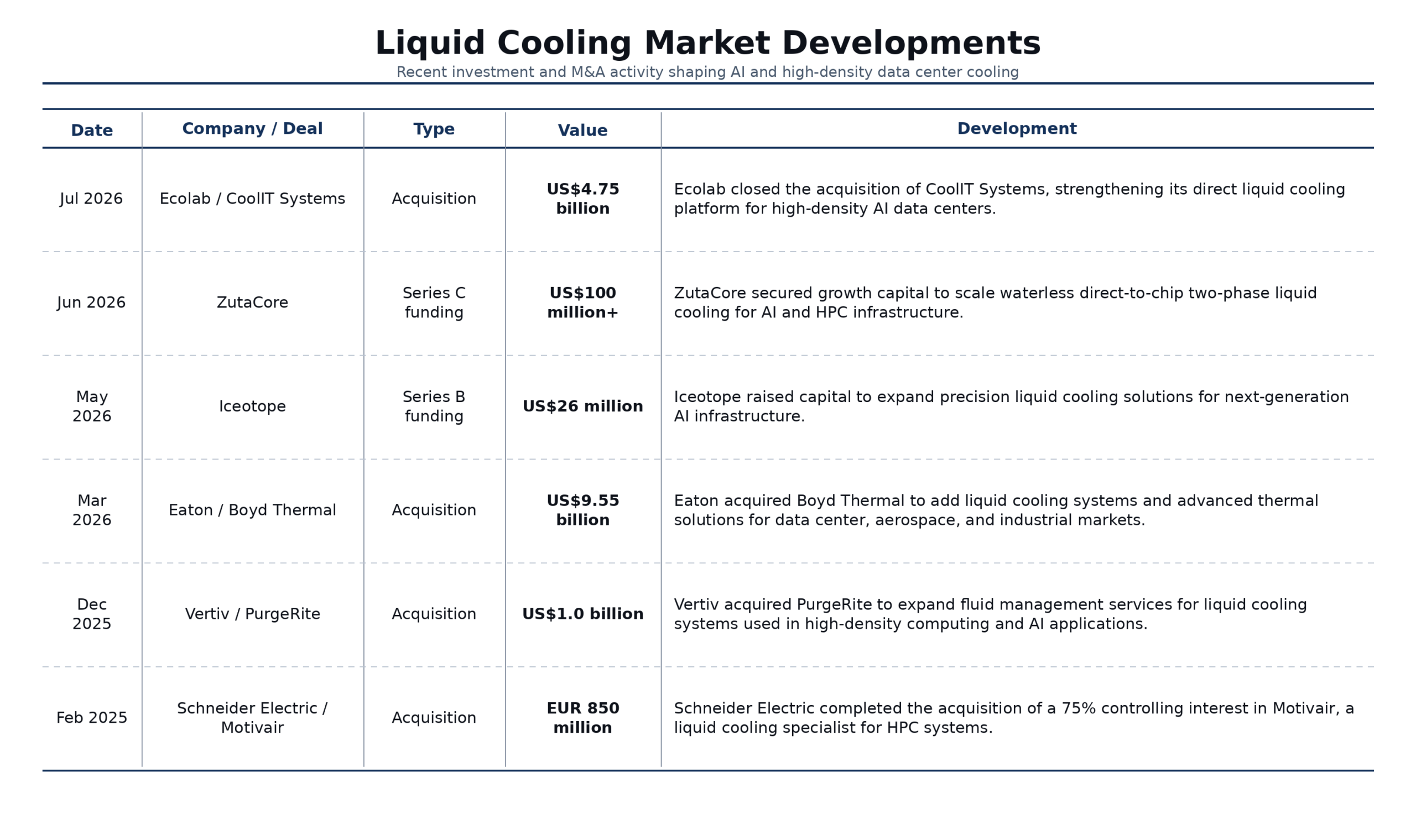

Recent Development:

Liquid Cooling System Market Scope: Inquire before buying

| Liquid Cooling System Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 5.9 USD Billion |

| Forecast Period 2026-2034 CAGR: | 16.5% | Market Size in 2034: | 23.32 USD Billion |

| Segments Covered: | by Cooling technology | Direct-to-Chip Liquid Cooling Immersion Cooling Systems Rear Door Heat Exchangers (RDHx) In-Rack Liquid Cooling Systems In-Row Liquid Cooling Systems Coolant Distribution Units (CDUs) Others |

|

| by Application | Data Center Cooling Systems Hyperscale Data Centers Colocation Data Centers Enterprise Data Centers Edge Data Centers AI / HPC Data Centers HVAC Systems Commercial HVAC Systems Industrial HVAC Systems District Cooling Systems Green & Energy-Efficient Buildings Industrial & High-Heat Applications Semiconductor & Electronics Cooling EV & Battery Testing Facilities Industrial Process Cooling Systems High-Performance Computing Labs |

||

| by End User | Data Center Operators (Hyperscalers, Colocation, Enterprise) MEP & Engineering Ecosystem MEP Contractors EPC Companies Design & Engineering Consultants System Integrators Facility Management Companies Industrial & Institutional Users Manufacturing Facilities Research & Government Labs Healthcare & Advanced Facilities |

||

| by Development Level | Chip-Level Cooling Rack-Level Cooling Row-Level Cooling Facility-Level Cooling |

||

Liquid Cooling System Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Liquid Cooling System Market Key Players

- Boyd Corporation

- CoolIT Systems Inc.

- Submer Technologies

- Schneider Electric SE

- Vertiv Group Corp.

- AMETEK, Inc.

- Rittal GmbH & Co. KG

- ALFA LAVAL

- Green Revolution Cooling (GRC)

- Midas Green Technologies LLC

- Chilldyne Inc.

- LiquidStack Holding B.V.

- Iceotope Technologies Ltd.

- Asperitas

- LiquidCool Solutions Inc.

- Motivair Corporation

- Laird Thermal Systems

- Parker Hannifin Corporation

- Mikros Technologies

- Delta Electronics, Inc.

- Fujitsu Limited

- Lenovo Group Limited

- Dell Technologies Inc.

- Supermicro

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Intel Corporation

- ZutaCore Ltd.

- Bitfury Group

Others

Frequently Asked Questions:

1. Which region has the largest share in Global Liquid Cooling System Market?

Ans: North America region held the highest share in 2025.

2. What is the growth rate of Global Liquid Cooling System Market?

Ans: The Global Liquid Cooling System Market is growing at a CAGR of 16.5% during forecasting period 2026-2034.

3. What is scope of the Global Liquid Cooling System Market report?

Ans: Global Liquid Cooling System Market report helps with the PESTEL, PORTER, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Liquid Cooling System Market?

Ans: The important key players in the Global Liquid Cooling System Market are – Allied Control Ltd., Asetek, Inc., Boyd Corporation, CooIIT Systems, Inc., Emerson Electric Co., Green Revolution Cooling Inc., Laird Thermal Systems, Midas Green Technologies LLC, Rittal GmbH & Co. KG, Schneider Electric SE, Lytron, Koolance, Millerwelds, Parker NA, Watteredge

5. What is the study period of this Market?

Ans: The Global Liquid Cooling System Market is studied from 2025 to 2034.