Insulation Market by Insulation Type, Material Type, End User and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

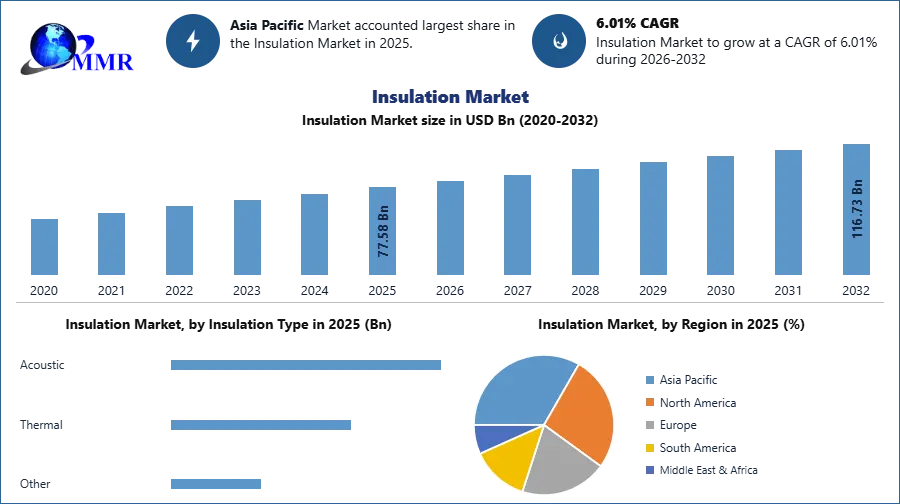

The Insulation Market size was valued at USD 77.58 Billion in 2025 and the total Insulation revenue is expected to grow at a CAGR of 6.01% from 2026 to 2032, reaching nearly USD 116.74 Billion.

Insulation Market Overview

Insulation is a crucial aspect of optimizing home comfort and energy efficiency. By resisting heat flow through conduction, convection, and radiation, insulation reduces heating and cooling costs. The R-value, measuring thermal resistance, guides insulation effectiveness—higher values indicate better insulation. Climate-specific recommendations ensure tailored solutions. Insulation types vary, including fibers, foams, and reflective materials. Proper installation is key, considering factors like continuous insulation and exterior siding. Insulation materials are used in commercial, industrial, and residential use to prevent heat, electricity, or sound from passing into or out of electronic devices and building materials.

Insulating materials come in a variety of forms including plastic foams, mineral wool, and fiberglass wool. The National Insulation Association estimates that implementing a comprehensive mechanical insulation maintenance and upgrade program in the commercial and industrial sectors will result in Energy savings of $4.8 billion per year and CO2 reductions of 43 million metric tonnes per year. Leading players in the global insulation market are focused on developing efficient solutions owing to the increased construction activity globally. Furthermore, Consumers throughout the world are becoming more conscious of the need for energy saving, which is driving demand for a variety of insulating materials during the forecast period.

The insulation market is experiencing transformative advancements, driven by a critical revaluation of environmental impacts. Traditional insulating materials, while reducing operational carbon, often pose environmental hazards. Emerging technologies aim to mitigate these concerns. Aerogels, known for their exceptional thermal insulation properties, are being developed with a focus on bio-based alternatives. Manufacturers are exploring hollow silica particles combined with cellulose fibers as a robust and scalable thermal composite. Surprisingly, even household items like popcorn are being transformed into insulation boards with fire-resistance and water-repellent properties. Additionally, a novel composite of wool, sulfur, and discarded cooking oil is demonstrating promising thermal insulation and biodegradability. These innovations signal a promising shift towards sustainable and eco-friendly insulation solutions in the construction industry.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Insulation Market Dynamics

Green Building Revolution to Drive the Insulation Market

The increasing global focus on sustainability and energy efficiency emerges as a primary growth driver for the insulation market. One of the most significant trends in green roofing insulation is the use of sustainable insulation materials. Traditional insulation materials, such as fiberglass and foam, are known for their adverse environmental impacts. However, newer alternatives like recycled denim, cellulose, and natural fibers are gaining popularity. These materials not only have a smaller environmental footprint but also offer comparable or even superior insulation performance. With governments enforcing stringent environmental regulations, the demand for eco-friendly insulation materials rises. This trend is bolstered by the growing awareness among consumers and industries alike about the long-term benefits of energy-efficient structures, driving the adoption of advanced insulation solutions.

The surge in green building practices in the U.S., influenced by the Biden administration's $1.9 trillion American Rescue Plan, reflects a paradigm shift in construction. Structures like Austin's Central Library exemplify this shift, showcasing features like natural light and rainwater harvesting. Climate change concerns, coupled with various incentives and the marketing appeal of sustainable features, have accelerated the adoption of green construction. Challenges, such as initial costs and the need for skilled labor, are being addressed by decreasing green material costs and governmental support. Businesses are urged to explore green certifications, reassess processes, scrutinize suppliers, and leverage tools such as PlanRadar to actively contribute to the green building revolution, aligning with a sustainable construction future.

Sustainability has become a central concern for industries across the globe, with a growing emphasis on minimizing carbon footprints and reducing environmental impact. Industrial buildings, which often have large footprints and energy-intensive operations, are no exception to this trend. As a result, such factors are expected to drive the Insulation Market growth.

Technological Advancements in the Insulation Sector to Drive the Market Growth

In recent years, various most common thermal and heat insulation materials used such as fiberglass insulation, mineral wool, cellulose, polyurethane foam, polystyrene, and other common insulation materials. Innovations such as smart insulation materials, aerogels, and advanced foams enhance thermal performance and contribute to reduced energy consumption. These cutting-edge solutions not only cater to the demand for superior insulation but also open avenues for novel applications, spurring market growth. The top thermal insulation materials, which are cost-effective fiberglass and eco-friendly cellulose to fire-resistant polyurethane foam and waterproof polystyrene, each material's attributes are analyzed based on factors such as R-value, environmental impact, and flammability.

Recently, materials like aerogel (used by NASA for the construction of heat-resistant tiles, capable of withstanding heat up to approximately 2000 degrees Fahrenheit with little or no heat transfer), have become affordable and available. One in particular is Pyrogel XT. Pyrogel is one of the most efficient industrial insulations in the world. Its required thicknesses are 50% – 80% less than other insulation materials. Such advanced materials are expected to create a global opportunity for the Insulation Market.

Also, The EU-funded GELCLAD project aims to revolutionize building energy efficiency with its innovative eco-panels. Around 40% of EU energy consumption and 36% of CO2 emissions originate from buildings, and the GELCLAD project addresses this challenge by developing cost-effective, easy-to-install eco-panels for external building use. These smart modular cladding panels incorporate advanced nano-insulation materials, recycled polymers, plastic foams, and wood biopolymer composites. The panels, lasting over 30 years, feature aerogel material for superior insulation performance. The project successfully conducted pilots in the UK, Slovenia, and Germany, showcasing its potential to penetrate the exterior insulation facade systems market and contribute to greening the future.

Energy Retrofitting Projects to Create Lucrative Opportunity for Market Growth

The increasing focus on energy efficiency and retrofitting existing structures creates a promising opportunity. Renovation and retrofitting projects, aimed at enhancing energy performance in older buildings, require effective insulation solutions. Companies specializing in retrofit-friendly insulation materials and services can tap into this Insulation Market segment, offering solutions that align with energy conservation goals and sustainability initiatives. Renovation, retrofit, and refurbishment of existing buildings represent an opportunity to upgrade the energy performance of commercial building assets for their ongoing life.

Fluctuating Raw Material Prices to Restrain the Market Growth

The insulation market is susceptible to fluctuations in raw material prices, particularly petrochemical-based components. Volatility in these prices can impact production costs and, consequently, the overall pricing of insulation products. Manufacturers may face challenges in maintaining stable profit margins and competitiveness amid unpredictable raw material costs.

In some developing regions, there is a lack of awareness regarding the benefits of proper insulation. Limited knowledge about energy efficiency, thermal comfort, and long-term cost savings through insulation may hinder market growth. Education and awareness campaigns are crucial to overcoming this restraint and fostering greater adoption of insulation solutions in these untapped markets.

Insulation Market Segment Analysis

Based on material type, the Expanded Polystyrene (EPS) accounted the largest Insulation Market share in 2025. This insulation is a lightweight, rigid, closed-cell insulation. EPS is available in several compressive strengths to withstand load and back-fill forces. This closed-cell structure provides minimal water absorption and low vapor permanence. Also, the glass wool product segment stands out with its thermal and acoustic insulation properties, derived from sand. Notably, it boasts attributes like low weight and high tensile strength. Additionally, the production of removable blankets, a byproduct of glass wool, adds versatility, making them ideal covers for various industrial equipment such as turbines, pumps, heat exchangers, tanks, expansion joints, valves, flanges, and other irregular surfaces prone to heat generation. Meanwhile, stone wool, a natural byproduct of volcanic eruptions, distinguishes itself with resistance to heat transfer, combining the thermal insulation characteristics of wool with the robustness of stone.

Based on the end user, Building & Construction segment dominated the largest market share in 2025, in that the wires and cables sub-segment dominates the global insulation market. A common cable wire and cable insulation product includes an insulated wire conductor and a jacket that encloses the insulated wire. Insulation is used on conducting materials to provide electrical isolation between the conductor and the ground. An insulated wire that is commonly used in equipment such as fire alarms, heating devices, automobiles, and others needs safety at high working temperatures. The insulation of a wire determines its safety and effectiveness.

This type of insulated wire is often formed by a conductor that has been coated with a heat-resistant organic resin, such as fluoro resin. Factors such as rising urbanization and increased investment in infrastructure development projects throughout the world are driving the growth of the insulated wire and cable segment in the insulation Industry.

Insulation Market Regional insight

Asia Pacific held the largest Insulation Market share in 2025. The regional market growth is influenced by oil and gas production, energy consumption and urbanization and construction boom. The region's insulation market is propelled by the escalating levels of oil production in key economies such as China and India. The increasing emphasis on energy conservation and a growing awareness of significant energy wastage contributes to the demand for insulation materials. Industries in the Asia Pacific region are increasingly adopting insulation solutions to enhance energy efficiency and reduce environmental impact. The leadership is attributed to the escalating oil production levels in China and India, coupled with growing concerns about substantial energy wastage. The demand for insulation materials in refurbishing and renovation activities further drive this regional market ascendancy.

In North America, the insulation market is significantly influenced by diverse industry demands, including oil and gas, manufacturing, metal and mining, and power sectors, where high operating temperatures prevail. The region's emphasis on insulation is underscored by the imperative need to address temperature-related challenges in these industries. Companies in North America are actively engaged in minimizing losses and enhancing operational efficiency through regular maintenance inspections. This strategic approach reflects a concerted effort to optimize performance and reduce energy-related inefficiencies in the region.

North America is a key regional market for insulation, with the United States holding a major market share due to the relatively active construction industry, and higher investments into urbanization projects in the country. Some of the primary factors include an increasing focus on green building projects and the resultant demand for thermal insulation in the industrial sector. According to the United Nations Environment Program, the residential and commercial buildings in the U.S. account for 43.5% of overall energy consumption annually which are supporting the demand for insulation materials in this region.

Insulation Market Scope: Inquire before buying

| Insulation Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 77.58 USD Bn |

| Forecast Period 2026-2032 CAGR: | 6.01% | Market Size in 2032: | 116.73 USD Bn |

| Segments Covered: | by Insulation Type | Acoustic Thermal Other |

|

| by Material Type | Mineral Wool Fiberglass Stone wool Polyurethane Foam (PUF) Expanded Polystyrene (EPS) Flexible Elastomeric Foam (FEF) Other Insulations |

||

| by Form Type | Rigid Insulation Flexible Insulation Spray Foam Insulation Loose-Fill Insulation Reflective Insulation Board Insulation |

||

| by Installation Method | Pre-Installed Insulation Retrofit Insulation Spray Applied Insulation Blown-in Insulation Batt & Roll Insulation |

||

| by End User | Building & Construction Industrial Transportation Automotive Other (Aerospace, oil & gas etc.) |

||

Global Insulation Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Insulation Key Players by Region:

North America

1. Huntsman Corporation (USA)

2. Atlas Roofing Corporation (USA)

3. GAF Materials Corporation (USA)

4. The Dow Chemical Company (USA)

5. Owens Corning (USA)

6. E. I. du Pont de Nemours (USA)

7. Aspen Aerogels (USA)

Europe:

1. BASF SE (Germany)

2. Bayer AG (Germany)

3. Saint-Gobain S.A (France)

4. Rockwool International (Denmark)

5. Evonik Industries AG (Germany)

6. Kingspan Group PLC (Ireland)

7. Morgan Thermal Ceramics (United Kingdom)

8. Knauf Insulation (Germany)

9. Armacell (Germany)

10. Knauf Insulation (Germany)

11. Saint-Gobain S.A (France)

Asia Pacific:

1. Atticcleanfl (India)

2. Bridgestone (Japan)

3. Ibiden Co. Ltd. (Japan)

4. Asahi Kasei Corporation (Japan)

5. Asahi Kasei Corporation (Japan)

6. Ibiden Co. Ltd. (Japan)

7. Others