Global HVAC Equipment Market by Type, End User, Business Type, System Type, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

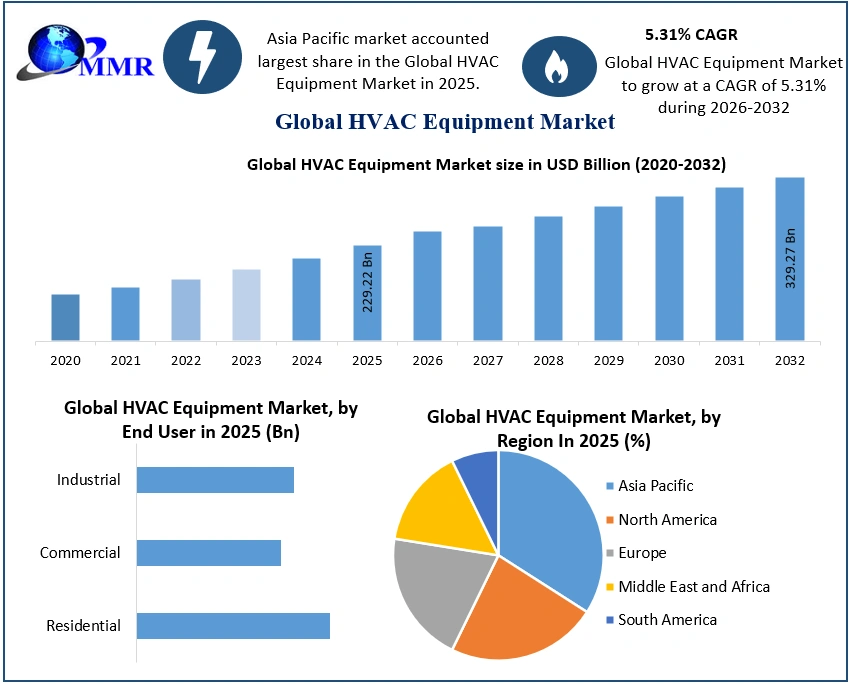

The HVAC Equipment Market size was valued at USD 229.22 Billion in 2025 and the total HVAC Equipment revenue is expected to grow at a CAGR of 5.31% from 2026 to 2032, reaching nearly USD 329.27 Billion by 2032.

HVAC Equipment Market Overview:

The booming construction business in individual emerging economies and the increasing end-user markets, like the data center market, are significant factors driving the growth of the HVAC equipment market over the forecast period. Some of the benefits of adopting HVAC equipment include energy efficient, improved results, and lifespan, among others.

To know about the Research Methodology :- Request Free Sample Report

Benefits of Installing HVAC Systems:

• Energy Efficiency - One of the massive trends in the home technology sector is the improvement of energy efficiency to reduce power bills. Latest thermostats and comfort-monitoring systems allow for automated scheduling based on when you are most likely to be home.

• Improved Results - The use of fans and air filters may improve the air quality of homes and commercial buildings while creating a more universal temperature throughout.

• Lifespan - Since the technology utilized to manufacture HVAC systems has improved coupled with better construction materials, these systems are expected to last longer than they did in the past. Essential routine maintenance implies fewer repairs and less need for replacements in the future.

• Changes in industrialization, urbanization, and migration are some of the critical factors influencing the growth of the market studied; this has increased the number of factories, manufacturing units, commercial buildings that use HVAC equipment.

• According to the Population Reference Bureau, in the degree of urbanization worldwide was approximately 54%. According to the source, North America, with 82% of the population living in cities, was the most urbanized continent worldwide. An AHR Expo and ASHRAE Journal survey found that nearly 88% of respondents in the HVAC industry are witnessing a "good" or "excellent" business year in. 43% of those respondents anticipate 5-10% growth for their business, and 23.5% expect growth at exceeds 10%.

• Moreover, reducing IoT sensor costs are also expected to result in OEMs offering products for a more competitive and lower price, which could indirectly impact the HVAC equipment market. Green HVAC systems are being developed to bring down costs and improve energy efficiency.

HVAC Equipment Market Dynamics:

Several regulations have changed the way manufacturers engineer commercial rooftop air conditioners, heat pumps, and warm-air for low-rise buildings, like retail stores, educational facilities, and mid-level hospitals, to improve RTU efficiency and cut energy usage and waste. To cater to these needs of the customers and to comply with the green technology requirements, several manufacturers have been developing equipment phasing out CFC (chlorofluorocarbon) and HCFC (Hydro chlorofluorocarbons), thereby, increasing the need for services for the replacement of old models, thus, driving the usage HVAC equipment.

Growing government support, in the form of higher budget allocations, designed to increase sustainable community development may contribute to the continually growing commercial and industrial construction sector. Besides, increased construction activities, rapid urbanization, and infrastructural reforms result in an upsurge in HVAC unit replacements, thus, driving the HVAC equipment market.

Furthermore, the companies' rebates and warranties have also been driving the HVAC replacement in the studied market. For instance, major companies, such as Honeywell and Siemens, provide one-year replacement warranties and five-year assistance assurances for HVAC systems. It is estimated that approximately 50% of the United States' growth will be generated from the replacement demand for these systems.

Furthermore, the geothermal federal tax credit which was reinstated in the United States (February ) could be retroactively applied to installations placed in service on January 1, or later. HVAC equipment that meets ENERGY STAR requirements at the time of installation is eligible for the tax credit. Covered expenditures include labor for assembly, onsite preparation, or original system installation and piping or wiring to connect a home system. This incentivization is further anticipated to boost the demand of the studied market in the long-term forecast. Central air conditioners, packaged units, heat pumps, and ductless mini-split systems qualified for a credit of up to USD 300. Geothermal heat pumps qualified for a credit of 30% of the cost, with no upper limit.

High initial cost is restraining the HVAC equipment market. Installing an HVAC system includes determining whether the unit is going to be a split system or roof mounted. Roof-mounted HVAC systems have the heating and cooling systems in one cabinet. Split systems are more efficient because the heat exchanger can be put in a shadier or cooler location. The choice between various HVAC equipment is primarily influenced by the convenience, environmental friendliness, availability, and price of fuels, as well as the initial costs, operating costs, and efficiency of the equipment.

With the growing awareness about installation charges, consumers are choosing products that include installation costs and provide a warranty for a longer period. Furthermore, the energy start certification is also playing a significant role in the selection of HVAC systems in both commercial and residential complexes. For instance, for a 1,000 square foot space, the cost of an HVAC system is USD 6,000-USD 12,000, including a new furnace, air conditioning unit, and ductwork. The cost of either fixing, replacing, or installing an HVAC system is about USD 2.61 per square foot or roughly USD 13,000 for a 5,000-squarefoot space.

HVAC Equipment Market Segment Analysis:

On the basis of type, HVAC equipment market is segmented into heating, air conditioning, ventilation and others. The introduction of new government regulations, like in the United States, is expected to result in increased energy efficiency of HVAC equipment. This has opened a gateway to the smart HVAC control systems for most advanced heating units in buildings. Packaged re-heat air conditioners, packaged re-heat gas/electric models, and packaged heat pump models are some of the products that cater to the segmental market. AHUs are most often connected to central plants, such as chillers and boilers, to provide the heating and cooling.

Starting from 2025, all new residential central air-source heat pump systems sold in the United States are expected to meet new minimum energy efficiency regulations and standards. The latest minimum energy efficiency standards for these equipment types went into effect in. The new regulations require an increase in the heating efficiency of all air-source heat pumps.

According to the Aeroseal Report, variable speed heat pumps can trim monthly homeowners' costs by up to 40%. Proper insulation for a building or home, on its own, can improve HVAC efficiencies by up to 30%.

Air conditioning equipment is expected to hold a prominent share of the HVAC equipment market, owing to the trend of an increasing number of residential and commercial users, combined with government regulations for energy efficiency and eco-friendly equipment. Since 1990, the energy demand for space cooling has more than tripled, making it the fastest-growing end-use equipment in buildings.

For instance, according to the International Energy Agency (IEA), space cooling was responsible for the emission of about 1 GT of CO2 and nearly 8.5% of the total final electricity consumption in . Moreover, roughly 2 Billion AC units are now in operation worldwide, making space cooling the leading driver of electricity demand in buildings, with a capacity to meet the peak power demand. Residential units account for 68% of the total air conditioners. Such instances depict that there is a significant demand for air conditioning equipment, and thus, the market is likely to grow at a significant rate over the forecast period.

On the basis of Sub-Type, HVAC Equipment market is segmented into Air Handling Units (AHU), Rooftop units and others. Rooftop units is leading the market with highest market share in . Rooftop units (RTUs for short), as the name suggests, are located on the roof of small commercial buildings and shops to provide air conditioning to pre-defined areas by connecting to ductwork, which provides a defined route for the conditioned air to travel along. These are considered as packaged air conditioning units and are so popular, as they are simple, compact, self-contained, and all-in-one HVAC units. RTUs are also a type of air handlers. RTU units are very much similar to AHUs, except that they are usually more compact and are always installed on the roof. In such regard, they need to be more robust and weatherproof to deal with external conditions, such as sun, rain, snow, and wind. In addition, AHUs are most often connected to central plants, such as chillers and boilers, to provide the heating and cooling, whereas RTUs are self-contained and contain everything that is required.

An air handling unit (AHU) is a unit used to re-condition and circulate air as part of a HVAC system. A typical function of these units includes taking in outside air, re-conditioning it, and supplying it to a building, as fresh air. In order to reduce the operating costs of the AHU, companies, such as VTS Group Ventilation Systems, are offering advanced control solutions, which allow the performance adjustment of the units to the actual conditions inside the building, consequently ensuring low operating costs.

On the basis of end user, HVAC Equipment market is segmented into commercial, industrial and Institutional. Commercial segment is leading the market with highest market share in . Cooling capacities of commercially available unitary products range from 3 metric ton to 25 metric ton. Some of the popular products include packaged air conditioners, packaged re-heat air conditioners, packaged gas/electric models, packaged re-heat gas/electric models, packaged heat pump models, split air conditioners, and split heat pump models.

HVAC unitary equipment manufacturers catering to the commercial sector in particular are expected to meet more demanding mandatory efficiency regulations around the world. For instance, AHRI 340/360 (Commercial & Industrial Unitary Air-Conditioning and Heat Pump Equipment) and AHRI 365 & 366 (Commercial and Industrial Unitary Air-Conditioning Condensing Units) are ISO 17025 accredited HVAC/R performance standards proposed by UL LLC, a global safety certification company. Such standards provide the framework for delivering value-enhancing growth. Furthermore, upgrades in these systems are helping combat the COVID-19 pandemic in commercial buildings. With more occupants expected to return to their offices in the next 1-2 quarters, commercial building owners can allay health and safety concerns, with simple changes to their indoor air quality (IAQ) strategies.

The growth in the construction industry and the increase in the disposable income in developing countries increased the requirement for HVAC equipment for a broader consumer base. According to the Bureau of Labor Statistics, the construction industry's business in the United States is expected to amount to almost USD 1.58 trillion by . However, not all industrial AHUs are manufactured the same way. Depending on the size, type, and other factors of the facility, the deployment of different or additional components can be noticed.

However, the COVID-19 pandemic created an economic turmoil for small-, medium-, and large-scale industries alike, across the world. Adding to the woes, the country-wise lockdown inflicted by various governments around the world to minimize the spread of the virus further resulted in industries taking a hit. Under these constrained circumstances, industries’ facilities across the world have witnessed a vast decline in revenue and profits, leading to significant cut down of employees and workers. Thus, this resulted in an overall loss to industrial production activities.

HVAC Equipment Market Regional Insights:

The demand for HVAC equipment in the region was witnessing significant growth opportunities over the past few years. China is one of the significant markets for data center cooling, due to the exponential growth in the number of data centers and the government’s policies to support more energy-efficient infrastructure in the country. China is also the fastest-expanding data center market in the world. With finch growth and digital transformation in the country, this expansion offers a massive opportunity for the vendors in the market studied.

According to the measure of data center space per user, internet data centers in China may expand to at least 22 times compare to the United States, or at least ten times the current area of Japan. Such expansion may generate demand for the deployment of the cooling equipment.

Besides, the increase in commercial buildings is estimated to directly affect national energy consumption, due to which the Chinese government has taken energy management into serious consideration. Two laws, Energy Saving Law and Renewable Energy Law, provide the main guidelines for building energy systems and HVAC and R industries.

HVAC systems are finding widespread adoption across the North American region, due to the multiple advantages offered by these systems, most notably, the power-saving techniques.

The United States and Canada rank among the world's top 10 energy-consuming countries, with the United States taking the second place, only behind China. The increased activity within the industrial sector, comprising manufacturing facilities (specifically the food industry), hospitals, data centers, and other institutional and industrial facilities, has been driving the market demand for HVAC equipment.

The objective of the report is to present a comprehensive analysis of the global HVAC Equipment market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the global HVAC Equipment market dynamics, structure by analyzing the market segments and project the global HVAC Equipment market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the global HVAC Equipment market make the report investor’s guide.

HVAC Equipment Market Scope: Inquiry Before Buying

| Global HVAC Equipment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 229.22 USD Bn |

| Forecast Period 2026-2032 CAGR: | 5.31% | Market Size in 2032: | 329.26 USD Bn |

| Segments Covered: | By Product Type | Heating Heat Pump Furnace Unitary Heaters Boilers Electric Baseboards Heating Cables Others Ventilation Air Purifier Dehumidifier Air Handling Units Ventilation Fans Others Cooling Air Conditioning Chillers Cooling Towers Others |

|

| By System Type | Central Decentralized |

||

| By Installation Type | New construction Replacement/Retrofit |

||

| By Distribution Channel | Online Retail Stores Wholesale Stores Others |

||

| By End User | Residential Commercial Industrials |

||

HVAC Equipment Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

HVAC Equipment Market, Key Players

- Daikin

- Carrier

- Mitsubishi Electric

- Trane

- Johnson Controls

- Lennox

- LG

- Samsung

- Midea

- Rheem

- Haier HVAC Solutions

- Bosch Thermotechnology Corp.

- Honeywell

- Fujitsu General

- Blue Star

- Voltas Ltd.

- Panasonic Corporation

- Hitachi Ltd.

- Danfoss Group

- Alfa Laval

- Systemair

- Zehnder Group AG

- Clivet S.p.A.

- AAON Inc.

- Nortek Global HVAC

- Greenheck Fan Corporation

- SPX Technologies

- Emerson Electric