1. Health Care Interoperability Solutions Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Global Health Care Interoperability Solutions Market: Competitive Landscape

2.1. MMR Competition Matrix

2.2. Competitive Landscape

2.3. Key Players Benchmarking

2.3.1. Company Name

2.3.2. Business Segment

2.3.3. End-user Segment

2.3.4. Revenue (2025)

2.3.5. Company Locations

2.4. Leading Health Care Interoperability Solutions Market Companies, by market capitalization

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Health Care Interoperability Solutions Market: Dynamics

3.1. Health Care Interoperability Solutions Market Trends by Region

3.1.1. North America Health Care Interoperability Solutions Market Trends

3.1.2. Europe Health Care Interoperability Solutions Market Trends

3.1.3. Asia Pacific Health Care Interoperability Solutions Market Trends

3.1.4. Middle East and Africa Health Care Interoperability Solutions Market Trends

3.1.5. South America Health Care Interoperability Solutions Market Trends

3.2. Health Care Interoperability Solutions Market Dynamics by Region

3.2.1. North America

3.2.1.1. North America Health Care Interoperability Solutions Market Drivers

3.2.1.2. North America Health Care Interoperability Solutions Market Restraints

3.2.1.3. North America Health Care Interoperability Solutions Market Opportunities

3.2.1.4. North America Health Care Interoperability Solutions Market Challenges

3.2.2. Europe

3.2.2.1. Europe Health Care Interoperability Solutions Market Drivers

3.2.2.2. Europe Health Care Interoperability Solutions Market Restraints

3.2.2.3. Europe Health Care Interoperability Solutions Market Opportunities

3.2.2.4. Europe Health Care Interoperability Solutions Market Challenges

3.2.3. Asia Pacific

3.2.3.1. Asia Pacific Health Care Interoperability Solutions Market Drivers

3.2.3.2. Asia Pacific Health Care Interoperability Solutions Market Restraints

3.2.3.3. Asia Pacific Health Care Interoperability Solutions Market Opportunities

3.2.3.4. Asia Pacific Health Care Interoperability Solutions Market Challenges

3.2.4. Middle East and Africa

3.2.4.1. Middle East and Africa Health Care Interoperability Solutions Market Drivers

3.2.4.2. Middle East and Africa Health Care Interoperability Solutions Market Restraints

3.2.4.3. Middle East and Africa Health Care Interoperability Solutions Market Opportunities

3.2.4.4. Middle East and Africa Health Care Interoperability Solutions Market Challenges

3.2.5. South America

3.2.5.1. South America Health Care Interoperability Solutions Market Drivers

3.2.5.2. South America Health Care Interoperability Solutions Market Restraints

3.2.5.3. South America Health Care Interoperability Solutions Market Opportunities

3.2.5.4. South America Health Care Interoperability Solutions Market Challenges

3.3. PORTER's Five Forces Analysis

3.4. PESTLE Analysis

3.5. Technology Roadmap

3.6. Regulatory Landscape by Region

3.6.1. North America

3.6.2. Europe

3.6.3. Asia Pacific

3.6.4. Middle East and Africa

3.6.5. South America

3.7. Key Opinion Leader Analysis For Health Care Interoperability Solutions Industry

3.8. Analysis of Government Schemes and Initiatives For Health Care Interoperability Solutions Industry

3.9. Health Care Interoperability Solutions Market Trade Analysis

3.10. The Global Pandemic Impact on Health Care Interoperability Solutions Market

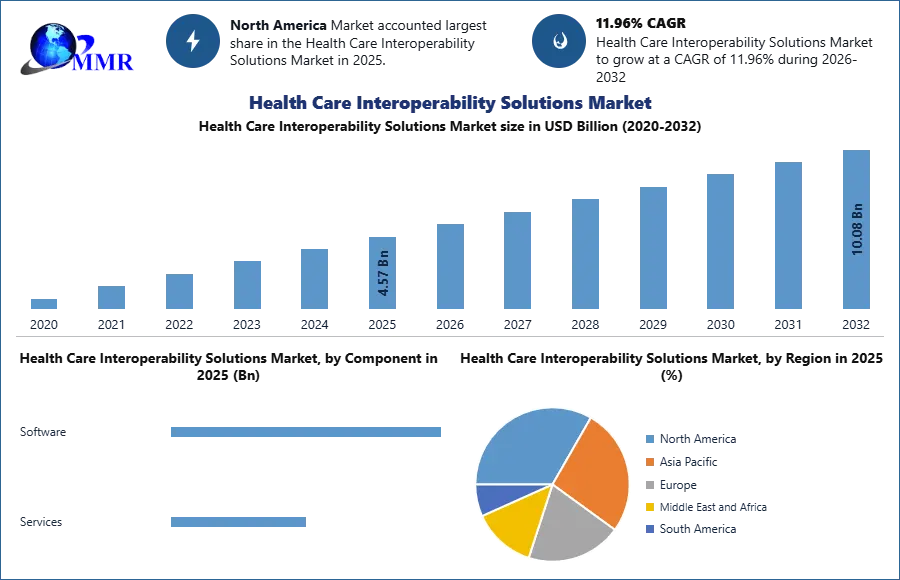

4. Health Care Interoperability Solutions Market: Global Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

4.1. Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

4.1.1. Software

4.1.2. Services

4.2. Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

4.2.1. Foundational

4.2.2. Structural

4.2.3. Semantic

4.3. Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

4.3.1. Cloud-based

4.3.2. On-premises

4.3.3. Hybrid

4.4. Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

4.4.1. Healthcare Providers

4.4.2. Healthcare Payers

4.4.3. Others

4.5. Health Care Interoperability Solutions Market Size and Forecast, by Region (2025-2032)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

5. North America Health Care Interoperability Solutions Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

5.1. North America Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

5.1.1. Software

5.1.2. Services

5.2. North America Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

5.2.1. Foundational

5.2.2. Structural

5.2.3. Semantic

5.3. North America Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

5.3.1. Cloud-based

5.3.2. On-premises

5.3.3. Hybrid

5.4. North America Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

5.4.1. Healthcare Providers

5.4.2. Healthcare Payers

5.4.3. Others

5.5. North America Health Care Interoperability Solutions Market Size and Forecast, by Country (2025-2032)

5.5.1. United States

5.5.1.1. United States Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

5.5.1.1.1. Software

5.5.1.1.2. Services

5.5.1.2. United States Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

5.5.1.2.1. Foundational

5.5.1.2.2. Structural

5.5.1.2.3. Semantic

5.5.1.3. United States Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

5.5.1.3.1. Cloud-based

5.5.1.3.2. On-premises

5.5.1.3.3. Hybrid

5.5.1.4. United States Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

5.5.1.4.1. Healthcare Providers

5.5.1.4.2. Healthcare Payers

5.5.1.4.3. Others

5.5.2. Canada

5.5.2.1. Canada Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

5.5.2.1.1. Software

5.5.2.1.2. Services

5.5.2.2. Canada Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

5.5.2.2.1. Foundational

5.5.2.2.2. Structural

5.5.2.2.3. Semantic

5.5.2.3. Canada Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

5.5.2.3.1. Cloud-based

5.5.2.3.2. On-premises

5.5.2.3.3. Hybrid

5.5.2.4. Canada Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

5.5.2.4.1. Healthcare Providers

5.5.2.4.2. Healthcare Payers

5.5.2.4.3. Others

5.5.3. Mexico

5.5.3.1. Mexico Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

5.5.3.1.1. Software

5.5.3.1.2. Services

5.5.3.2. Mexico Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

5.5.3.2.1. Foundational

5.5.3.2.2. Structural

5.5.3.2.3. Semantic

5.5.3.3. Mexico Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

5.5.3.3.1. Cloud-based

5.5.3.3.2. On-premises

5.5.3.3.3. Hybrid

5.5.3.4. Mexico Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

5.5.3.4.1. Healthcare Providers

5.5.3.4.2. Healthcare Payers

5.5.3.4.3. Others

6. Europe Health Care Interoperability Solutions Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

6.1. Europe Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.2. Europe Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.3. Europe Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.4. Europe Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5. Europe Health Care Interoperability Solutions Market Size and Forecast, by Country (2025-2032)

6.5.1. United Kingdom

6.5.1.1. United Kingdom Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.1.2. United Kingdom Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.1.3. United Kingdom Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.1.4. United Kingdom Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5.2. France

6.5.2.1. France Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.2.2. France Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.2.3. France Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.2.4. France Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5.3. Germany

6.5.3.1. Germany Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.3.2. Germany Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.3.3. Germany Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.3.4. Germany Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5.4. Italy

6.5.4.1. Italy Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.4.2. Italy Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.4.3. Italy Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.4.4. Italy Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5.5. Spain

6.5.5.1. Spain Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.5.2. Spain Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.5.3. Spain Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.5.4. Spain Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5.6. Sweden

6.5.6.1. Sweden Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.6.2. Sweden Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.6.3. Sweden Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.6.4. Sweden Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5.7. Austria

6.5.7.1. Austria Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.7.2. Austria Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.7.3. Austria Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.7.4. Austria Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

6.5.8. Rest of Europe

6.5.8.1. Rest of Europe Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

6.5.8.2. Rest of Europe Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

6.5.8.3. Rest of Europe Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

6.5.8.4. Rest of Europe Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7. Asia Pacific Health Care Interoperability Solutions Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

7.1. Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.2. Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.3. Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.4. Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5. Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by Country (2025-2032)

7.5.1. China

7.5.1.1. China Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.1.2. China Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.1.3. China Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.1.4. China Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.2. S Korea

7.5.2.1. S Korea Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.2.2. S Korea Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.2.3. S Korea Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.2.4. S Korea Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.3. Japan

7.5.3.1. Japan Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.3.2. Japan Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.3.3. Japan Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.3.4. Japan Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.4. India

7.5.4.1. India Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.4.2. India Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.4.3. India Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.4.4. India Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.5. Australia

7.5.5.1. Australia Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.5.2. Australia Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.5.3. Australia Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.5.4. Australia Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.6. Indonesia

7.5.6.1. Indonesia Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.6.2. Indonesia Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.6.3. Indonesia Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.6.4. Indonesia Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.7. Malaysia

7.5.7.1. Malaysia Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.7.2. Malaysia Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.7.3. Malaysia Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.7.4. Malaysia Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.8. Vietnam

7.5.8.1. Vietnam Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.8.2. Vietnam Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.8.3. Vietnam Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.8.4. Vietnam Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.9. Taiwan

7.5.9.1. Taiwan Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.9.2. Taiwan Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.9.3. Taiwan Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.9.4. Taiwan Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

7.5.10. Rest of Asia Pacific

7.5.10.1. Rest of Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

7.5.10.2. Rest of Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

7.5.10.3. Rest of Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

7.5.10.4. Rest of Asia Pacific Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

8. Middle East and Africa Health Care Interoperability Solutions Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

8.1. Middle East and Africa Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

8.2. Middle East and Africa Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

8.3. Middle East and Africa Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

8.4. Middle East and Africa Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

8.5. Middle East and Africa Health Care Interoperability Solutions Market Size and Forecast, by Country (2025-2032)

8.5.1. South Africa

8.5.1.1. South Africa Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

8.5.1.2. South Africa Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

8.5.1.3. South Africa Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

8.5.1.4. South Africa Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

8.5.2. GCC

8.5.2.1. GCC Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

8.5.2.2. GCC Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

8.5.2.3. GCC Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

8.5.2.4. GCC Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

8.5.3. Nigeria

8.5.3.1. Nigeria Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

8.5.3.2. Nigeria Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

8.5.3.3. Nigeria Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

8.5.3.4. Nigeria Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

8.5.4. Rest of ME&A

8.5.4.1. Rest of ME&A Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

8.5.4.2. Rest of ME&A Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

8.5.4.3. Rest of ME&A Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

8.5.4.4. Rest of ME&A Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

9. South America Health Care Interoperability Solutions Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

9.1. South America Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

9.2. South America Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

9.3. South America Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

9.4. South America Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

9.5. South America Health Care Interoperability Solutions Market Size and Forecast, by Country (2025-2032)

9.5.1. Brazil

9.5.1.1. Brazil Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

9.5.1.2. Brazil Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

9.5.1.3. Brazil Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

9.5.1.4. Brazil Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

9.5.2. Argentina

9.5.2.1. Argentina Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

9.5.2.2. Argentina Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

9.5.2.3. Argentina Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

9.5.2.4. Argentina Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

9.5.3. Rest Of South America

9.5.3.1. Rest Of South America Health Care Interoperability Solutions Market Size and Forecast, by Component (2025-2032)

9.5.3.2. Rest Of South America Health Care Interoperability Solutions Market Size and Forecast, by Interoperability Level (2025-2032)

9.5.3.3. Rest Of South America Health Care Interoperability Solutions Market Size and Forecast, by Deployment Model (2025-2032)

9.5.3.4. Rest Of South America Health Care Interoperability Solutions Market Size and Forecast, by End User (2025-2032)

10. Company Profile: Key Players

10.1. Cerner Corporation (Oracle Health)

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Scale of Operation (small, medium, and large)

10.1.7. Details on Partnership

10.1.8. Regulatory Accreditations and Certifications Received by Them

10.1.9. Awards Received by the Firm

10.1.10. Recent Developments

10.2. Epic Systems Corporation

10.3. Koninklijke Philips N.V.

10.4. InterSystems Corporation

10.5. Allscripts Healthcare Solutions Inc. (Veradigm)

10.6. NextGen Healthcare Inc.

10.7. Infor Inc. (Koch Software Investments)

10.8. Medical Information Technology Inc. (MEDITECH)

10.9. Orion Health Group Limited

10.10. IBM Corporation

10.11. GE HealthCare

10.12. Siemens Healthineers AG

10.13. Cognizant

10.14. Change Healthcare

10.15. Jitterbit Inc.

10.16. Virtusa Corporation

10.17. Lyniate

10.18. Onyx Health

10.19. Edifecs Inc.

10.20. Health Catalyst Inc.

10.21. Redox Inc.

10.22. ViSolve Inc.

10.23. iNTERFACEWARE Inc.

10.24. Quality Systems Inc.

10.25. Enovacom

11. Key Findings

12. Industry Recommendations

13. Health Care Interoperability Solutions Market: Research Methodology

14. Terms and Glossary

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report