Ferroalloys Market Size by Type, End-Use Industry, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

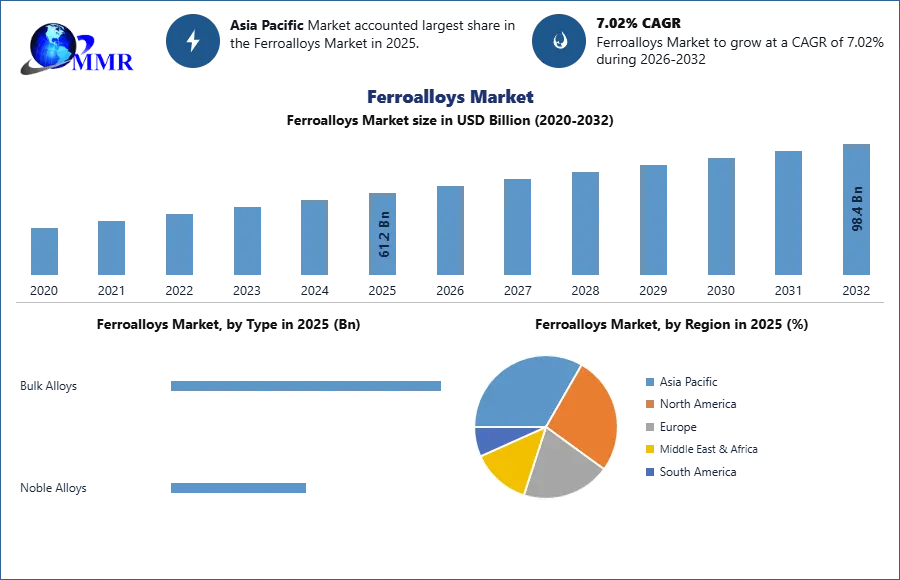

The Ferroalloys Market was valued at USD 61.2 Bn in 2025 and is estimated to reach at an evaluation of USD 98.4 Bn by the end of 2032, growing at a CAGR of 7.02% during the forecast 2026 and 2032.

Ferroalloys Market Definition:

Ferroalloys are iron metal alloy composed of aluminum, silicon, or magnesium primarily used in the production of steel & to enhance the properties of metal such as durability, the tensile strength with magnetic properties which makes them useful in the construction of electrical appliances & large motor. Ferrous metals are also find useful in automobiles, housing construction, railways & roadways transportation etc. The report study has analyzed revenue impact of covid-19 pandemic on the sales revenue of market leaders, market followers and disrupters in the report and same is reflected in our analysis.

To know about the Research Methodology :- Request Free Sample Report

Ferroalloys Market Dynamics:

The report covers worldwide Ferroalloys Market size in value and volume with market dynamics by region. All the segments and their detailed evaluation of the trends and factors affecting the market analyzed in the report. Market affecting factors cover drivers, restraints, opportunities, and challenges, consolidation, investment in the industry with focus on key market players by region.

Some of the key factors driving the growth of ferroalloys market are growing demand for steels in shipbuilding, construction, automotive and other industries in manufacturing. Emerging countries such as India and China have become center hub for Ferroalloys with high steel production. The Global crude steel production was valued to be 1.8 Bn tons in 2025 and is expected to grow with a CAGR of 7.02%. Furthermore, growing population with improving standard of living and initiatives in R&D by government are anticipated to benefit the market’s growth in the upcoming forecast.

The development of high-strength steel grades and lightweight provide opportunities to promote the development especially in emerging countries and is another factor driving the global ferroalloys market.

However, stringent regulations in concern to environmental hazard with high operating costs are major factor constricting the growth and hindering the market. Thanks to strict regulation the market opportunities are shifted towards eastern countries, which is amazed in the report by countries.

Ferroalloys Market Segmentation:

The report covers competitive analysis of the Ferroalloys Market in each of the geographical segments thereby providing insight into a market share of the countries.

In terms of Application, steel held largest market share in 2025 and its development is forecasted to have a significant growth over next seven year, 2026- 2032. The growth is attributed to growing production nearly 80% of ferroalloy are utilized in the production of steel because of low price, good characteristic & widespread application of steel in automotive, construction, shipbuilding sector. Moreover, upsurge demand for different types steel grade in emerging countries especially in, China & India region is one of the driving factors of ferroalloy market growth. For instance, Asia pacific in 2025, valued a market growth of 2.4 Mn tons in crude steel production compared to 2018. Furthermore, initiatives by government in recent development for smart cities promotes opportunities for steel and hinder the growth for ferroalloy market.

Based on type, bulk ferroalloys generates the largest revenue in 2025 and is estimated to grow in the coming forecast almost 80 % of ferroalloys are used to product bulk ferroalloys to improve properties of steel. Ferromanganese is anticipated to show the fastest growth during the forecast, due to its extensive usage in steel production. Ferromanganese is widely used as a desulfurizing agent to produce steel and plays a major part in steel production, as it reduces the production of undesired iron oxide and removes nitrogen bubbles.

Noble ferroalloys show steady growth an accounts for 30% of the global market share as they are expensive to produce in comparison to bulk ferroalloys and are made from rare earth minerals such as, tungsten, chromium, nickel, boron, cobalt and phosphorus.

Ferroalloys Market Regional Analysis:

Asia Pacific is the dominant market with market share of 35% in 2025. China is considered as center glut for steel production with 51.3% in 2018, and as per world steel association, In June 2025 China is registered as the largest steel producer, with an upsurge of 6.6 percent from~860 MT around ~900 Mn tones (MT) of steel. Moreover, rapid industrialization and large investments by government of India and large companies in development and making smart India is expected to boost demand for Ferroalloys in market.

Europe, is projected to have a healthy growth over the forecast due to widespread utilization of Ferro alloy in automotive industries and increasing used of matrix alloy to lessen metal toxicity drive the market.

North America is projected to register a considerable CAGR during the forecast due to the Existence of major players and presence of well-established industries such as, metallurgical, aerospace, construction etc., positively impact the regional market.

Competitive Analysis: Global Ferroalloys Market:

The report of Global Ferroalloys Market analysis includes information of detailed analysis leading manufacturer’s, prominent vendors and upcoming trends & challenges that will influence market growth. Further, the adoption of variant strategic business activities such as acquisitions, mergers, collaboration, etc. are estimated to create productive opportunities for the global market over the forecast period. As per report, some major prominent players in Ferroalloys Market are BASF Corporation, Tata Steel, and ArcelorMittal etc.

Recent Industry Developments (2025–2026):

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 13 February 2026 | Glencore plc | Restarted ferrochrome production at a key South African plant following a strategic agreement on temporary electricity tariffs. | The restart helps stabilize global ferrochrome supply after significant output plunges reported in the 2025 fiscal year. |

| 01 January 2026 | Ferroglobe PLC | Activated a new 10-year energy agreement for its French operations to provide long-term cost stability and operational flexibility. | This agreement improves earnings capacity and protects the company from the energy price volatility that impacted silicon-based alloy margins in 2025. |

The objective of the report is to present a comprehensive analysis of the Global Ferroalloys Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that includes market leaders, followers, and new entrants. PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding Global Ferroalloys Market dynamics, structure by analyzing the market segments and projects the Global Ferroalloys Market size. Clear representation of competitive analysis of key players By Pathogen Type, price, financial position, Product portfolio, growth strategies, and regional presence in the Global Ferroalloys Market make the report investor’s guide

Ferroalloys Market Scope : Inquire before buying

| Ferroalloys Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 61.2 USD Billion |

| Forecast Period 2026-2032 CAGR: | 7.02% | Market Size in 2032: | 98.4 USD Billion |

| Segments Covered: | by Type | Bulk Alloys Noble Alloys |

|

| by Bulk Alloys | Ferrosilicon Ferromanganese Ferrochromium Others |

||

| by Noble Alloys | Ferromolybdenum Ferronickel Ferrotungsten Ferrovanadium Ferrotitanium Others |

||

| by End User | Steel Superalloys and Alloys Wire Production Welding Electrodes Others |

||

Ferroalloys Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina and Rest of South America)

Ferroalloys Market Key Players are:

1. ArcelorMittal

2. Tata Steel

3. Sakura Ferroalloys

4. BAFA Bahrain

5. OM Holdings LTD

6. Pertama Ferroalloys

7. NikoPol Ferroalloy Plant

8. Brahm Group

9. Ferroalloy Corporation Limited

10. China Minmetals Corporation

11. Gulf Ferroalloys Company

12. Shanghai Shenjia Ferroalloys Co. Ltd.

13. Vale S.A.

14. MORTEX GroupGeorgian American Alloys

15. SAIL

16. OFZ S.A.

17. Eurasian Natural Resources Corporation

18. S.C. Ferl S.R.L.

19. Jindal Group

20. Glencore

21. Samancore Chrome

22. Ferro Alloys Corporation Limited.