Crop Harvesting Robots Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

Crop Harvesting Robots Market was valued at US$ 18.93 Bn. in 2025. The Global Crop Harvesting Robots Market size is estimated to grow at a CAGR of 33.48 % over the forecast period.

Crop Harvesting Robots Market Overview:

Crop harvesting robots are agricultural robots that define the location of the plant, or estimated locations, as well as the size of the fruit and vegetable. Robots employ computer vision algorithms to detect and locate fruits and grains. The report explores the market segments (Type, Application, and Region). Data has been provided by market participants, and regions (North America, Asia Pacific, Europe, Middle East & Africa, and South America). This market report provides a thorough analysis of the rapid advances that are currently taking place across all industry sectors. Facts and figures, illustrations, and presentations are used to provide key data analysis for the historical period from 2017 to 2020. The report investigates the market drivers, limitations, prospects, and barriers. This MMR report includes investor recommendations based on a thorough examination of the market contemporary competitive scenario.

To know about the Research Methodology:-Request Free Sample Report

Crop Harvesting Robots Market Dynamics:

Driver: Increasing the awareness and understanding of smart agriculture

The harvesting robot market is gaining traction due to reasons such as rising demand for food security and a growing awareness of smart agriculture. Also, smart farming is a new concept that refers to managing farms utilizing contemporary information and communication technology to boost Type quantity and quality while minimizing the amount of human labor required. As a result of the growing awareness of smart agriculture, the demand for harvesting robots is increasing around the world.

Increased population and labor shortages encourage automation

The agriculture industry is under strain due to the rising global population and the need to increase output from current farmland. The agriculture industry is now being impacted by factors such as changing demographics and urbanization. With an aging farmer population significantly limiting the supply of physical labor, the labor shortage has become a global issue. As a result, current farmers have been laboring in the field for longer periods of time. Robotic automation can not only replace the employment that is no longer needed, but it can also draw qualified employees to non-repetitive duties. Robots can automate duties such as cleaning and feeding on dairy farms, allowing farmers to concentrate more on decision-making. Large farming firms are investing in agricultural robotic solutions startups to help them get started.

The market is Propelled Forward by Consistent Government Support

The global agricultural robotics market is growing due to rising urbanization and rising food consumption around the world. Also, governments around the world have declared different helpful policies in the form of subsidies or aid for greater type, as well as campaigns to raise knowledge about agricultural robots among farmers.

Restraint: Orchard setting that is largely disorganized

Harvesting robot systems have had limited success in the past because to the highly unstructured orchard environment and changing outside circumstances. There has been no commercial viability, and every apple destined for the fresh market is still chosen. Because agricultural workspaces like apple orchards and grape vineyards are biologically driven environments, this is the case. Also, in agricultural robots, the lack of broad design limit criteria has caused variance in design approaches.

Opportunity: Improved dexterity to deal with crops

In the agricultural industry, rising labor costs are driving automation. Also, AI-enabled harvesting Robots are a growing opportunity in the Global Harvesting Robot Market, their increased dexterity in handling crops of varied shapes and sizes is forecasted to be an opportunity for the future.

Field applications of real-time multimodal robot systems

Multimodal or heterogeneous platforms, which integrate ground-based and airborne vehicles, provide for targeted support, intelligence, and mission planning. Large-scale agriculture and dairy operations benefit from collaborative and cooperative behavior between robots because activities can be completed simultaneously, resulting in superior economies of scale. In a systematic approach, different types of robots and autonomous systems can now be brought together. Players in the agricultural robotics market are likely to employ multimodal robot systems extensively during the forecast period, owing to their capacity to run swarms of robots on farms to conduct numerous agricultural applications such as spraying and weeding simultaneously. Investing in multimodal systems is projected to increase revenue streams for agricultural robot manufacturers.

Challenge: Data privacy concerns and regulations

Data ownership raises ethical concerns, particularly with the advent of software applications for agricultural use. A situation similar to other technology fields can evolve where a small number of corporations control the majority of client data. Data collected by ground robots may differ significantly from that collected by drones. Third parties, such as banks, frequently purchase this data in order to make loans depending on the farmer's productivity. As a result, data security must be considered. Governments around the world must also address other ethical issues of agricultural robotics, such as liability frameworks and the re-use of robot-collected data for research or study. The absence of technological standards also makes system integration more difficult, as most equipment manufacturers utilize proprietary communication protocols. In many circumstances, the creation of extra gateways is required for data translation and transfer across different manufacturers' equipment.

Crop Harvesting Robots Market Trends:

The labor market's decreasing tendency is turning into increased labor wages. According to the Farm Labor Survey (NASS FLS) of the National Agriculture Statistical Service, the agriculture industry suffered a 7% decrease in hired farm labor and a 5% increase in labor wages. Farm automation solutions can assist alleviate the effects of the farm labor shortage. Agtech can help agricultural systems become more efficient and increase overall productivity without driving up expenses. As a result of the labor deficit, stakeholders are considering how to modernize the country's farms. According to the American Farm Bureau Federation (AFBF), 56% of US farms have started utilizing agritech, with more than half citing labor shortages as a reason. Wireless sensors, robotics, a predictive forecasting model, and data analytics are examples of new agro-technology. As a result, rising labor shortages and wages are propelling the market forward.

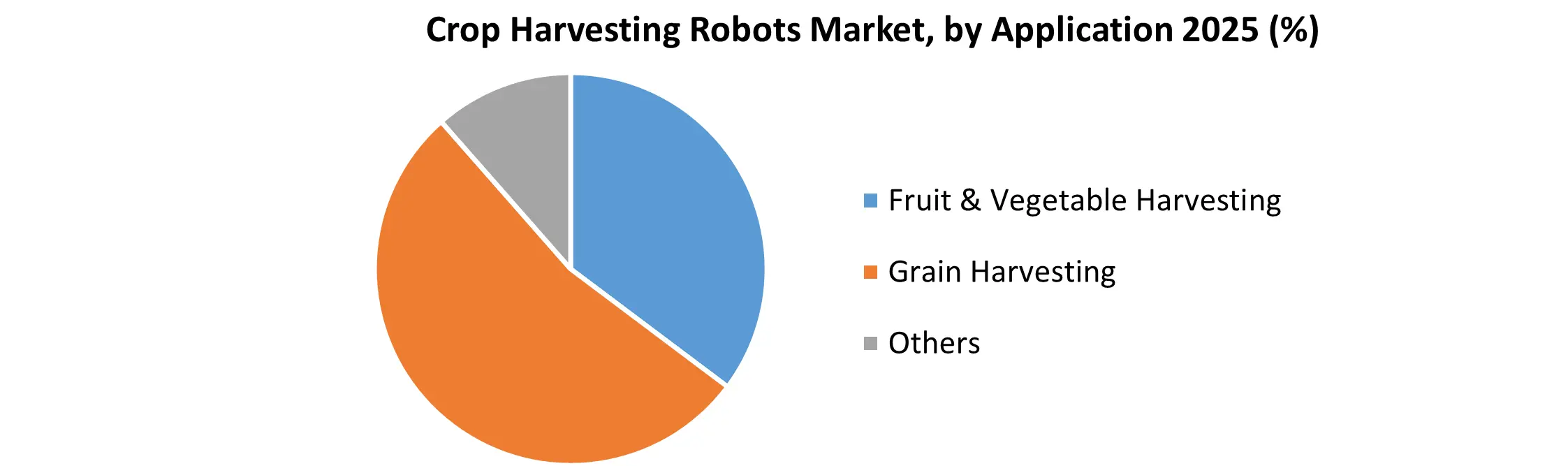

Crop Harvesting Robots Market Segment Analysis:

Based on Application, the Crop Harvesting Robots Market is segmented into Fruit & Vegetable Harvesting and Grain Harvesting. Fruit harvesting robots are predicted to develop at the fastest rate of 20.9 % due to rising demand for fruits for industries such as seed of juices and jealous, among others. Harvesting robots for fruits and vegetables have the biggest market share since they can only collect fruits and veggies that are ready to eat. Farmers' interest in fruit and vegetable harvesting robots is fueled by the possibility of such selective harvesting.

Based on Robot Type, the Crop Harvesting Robots Market is segmented into Semi-Autonomous Robots and Fully-Autonomous Robots Based on robot type, the global crop harvesting robots market is divided into two categories: semi-autonomous robots and completely autonomous robots. The market for semi-autonomous robots is the larger of the two. It is growing in poorer economies where agriculture is the dominant industry, although fully autonomous robots are also forecasted to rise.

Regional Insights:

The North American region held the largest market share accounting for 38.2% in 2025. North American region is expected to witness significant growth at a CAGR of 12.6% through the forecast period. The North American region is expected to be the leading market for crop harvesting robots market due to the high adoption of automation technologies in various industries such as agriculture. Automation technologies help reduce labor costs associated with crop harvesting as well as increase production capacity, resulting in better quality produce fetching higher revenue generation by farmers. Due to the increasing demand for automation in various industries such as agriculture, South America is predicted to be the fastest-growing market for Crop Harvesting Robots Market. This is accelerating investments by key players towards creating crop harvesting robots.

The objective of the report is to present a comprehensive analysis of the global Crop Harvesting Robots Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Crop Harvesting Robots Market dynamic, and structure by analyzing the market segments and projecting the Crop Harvesting Robots Market size. Clear representation of competitive analysis of key players by Design, price, financial position, Type portfolio, growth strategies, and regional presence in the Crop Harvesting Robots Market make the report investor’s guide.

Crop Harvesting Robots Market Competitive Landscape:

Key advancements in the crop harvesting robots industry, as well as organic and inorganic growth methods, are covered in the report. Product launches, product approvals, and other organic growth tactics such as patents and events are being prioritized by a number of companies. Acquisitions and partnerships & collaborations were two inorganic growth tactics seen in the sector. These initiatives have paved the road for market players to expand their business and client base. With the increased demand for crop harvesting robots, market players in the crop harvesting robots market are expected to benefit from lucrative growth prospects in the future. A list of a few firms involved in the agriculture harvesting robots market is provided below. Some of the major key players in the crop harvesting robots market are Agrobot, Cerescon BV, Robotics Inc., Dogtooth Technologies Ltd., Energid Technologies Corp., FFRobotics, Green Robot Machinery Pvt. Ltd., Harvest Automation, Harvest CROO Robotics

Crop Harvesting Robots Market Scope: Inquire before buying

| Crop Harvesting Robots Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 18.93 USD Billion |

| Forecast Period 2026-2032 CAGR: | 33.48% | Market Size in 2032: | 142.91 USD Billion |

| Segments Covered: | by Type | Grains & Cereals Fruits & Vegetables Others |

|

| by Component | Hardware Software Services |

||

| by Robot Type | Unmanned Ground Vehicles (UGVs) Unmanned Aerial Vehicles (UAVs) |

||

| by Autonomy Level | Semi-Autonomous Fully Autonomous |

||

| by Farm Size | Small & Medium Farms Large Farms |

||

| by Farming Environment | Outdoor Farming Flat Terrain Farming Hilly / Sloped Terrain Farming (Hillside Equipment) Indoor / Greenhouse Farming |

||

| by Business Model | OEM (Direct Sales) Robotics-as-a-Service (RaaS) / Aftermarket |

||

| by Application | Fruit & Vegetable Harvesting Grain Harvesting Others |

||

by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Crop Harvesting Robots Market Key Players:

1. Deere & Company

2. AGCO Corporation

3. Kubota Corporation

0. Yanmar Holdings Co., Ltd.

5. FFRobotics

6. Harvest CROO Robotics

7. Agrobot

8. Dogtooth Technologies Ltd.

9. Tortuga Agricultural Technologies Inc.

10.Advanced Farm Technologies Inc.

11.MetoMotion

12.Octinion

13.Ripe Robotics

14.Shibuya Seiki

15.Clearpath Robotics Inc.

16.SwarmFarm Robotics

17.AgXeed BV

18.Antobot Ltd.

19.Small Robot Company

20.Saga Robotics

21.Autonomous Solutions, Inc.

22.Trimble Inc.

23.Blue River Technology

24.AgEagle Aerial Systems Inc.

25.EcoRobotix

26.Naïo Technologies

27.Cerescon BV

28.Muddy Machines Ltd.

29.Four Growers

30.Tevel Aerobotics Technologies

31.Green Robot Machinery Pvt. Ltd.

32.SPUDNIK Equipment Company LLC

33.Harvest Automation, Inc.

34.Energid Technologies Corporation

35.AVL Motion BV

36.Fendt

Frequently Asked Questions:

1] What is the forecasted market size and growth rate of the Crop harvesting robots market?

Ans. Forecasted market size US$ 142.91 Bn. till 2032, with a CAGR of 33.48 %.

2] What are the restraining factors of the growth of the Crop harvesting robots market?

Ans. Orchard setting that is largely disorganized is the restraining factors in the Crop harvesting robots market.

3] Which region is expected to hold the highest share in the Crop harvesting robots Market?

Ans. The North American region is expected to hold the highest share in the Crop harvesting robots Market in 2025.

4] Which are the leading key players in the Crop harvesting robots market?

Ans. Agrobot, Cerescon BV, Clearpath Robotics Inc., Dogtooth Technologies Ltd., Energid Technologies Corp., FFRobotics, Green Robot Machinery Pvt. Ltd. are some of the leading key players of crop harvesting robots market.

Harvest Automation

5] What segments are covered in Crop harvesting robots?

Ans. The Crop harvesting robots market is segmented into Type, application, and Region.