Container Fleet Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

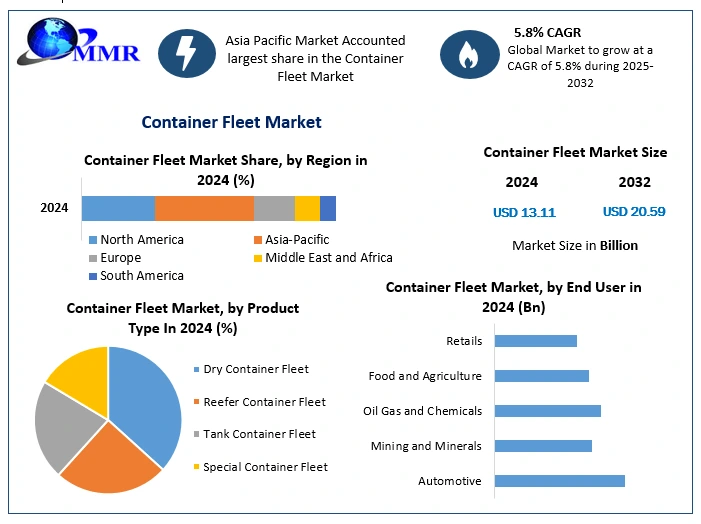

The Container Fleet Market size was valued at USD 13.11 Billion in 2024 and the total Container Fleet revenue is expected to grow at a CAGR of 5.8% from 2025 to 2032, reaching nearly USD 20.59 Billion.

Container Fleet Market Overview

The container fleet market is of paramount importance to global commerce, facilitating the seamless transportation of goods across vast distances. Containerization has revolutionized the logistics industry by offering a standardized, efficient method for cargo transport, significantly reducing costs and improving efficiency. This streamlined approach to shipping has become indispensable for businesses worldwide, driving the market forward as companies seek to capitalize on its benefits to remain competitive in the global marketplace.

Increasing globalization of trade, which has led to rising demand for efficient transportation solutions and it is driving the growth of container fleet industry. As businesses expand their reach to new markets and consumers, the need for reliable and cost-effective shipping services becomes ever more crucial. Additionally, the growth of e-commerce has further fueled demand for containerized shipping, as online retailers rely on timely delivery of goods to meet customer expectations. These factors, combined with advancements in technology and infrastructure, are growing the container fleet market forward, driving revenue growth and market share expansion. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Trends in the container fleet market reflect the industry's ongoing evolution to meet the changing needs of global trade. Key trends include the adoption of digitalization and automation technologies to enhance operational efficiency and transparency. Smart containers equipped with sensors and tracking systems are increasingly being utilized to monitor cargo conditions and optimize shipping routes. Also, there is a growing emphasis on environmental sustainability, with efforts to reduce emissions and minimize the ecological impact of container shipping operations.

End users of container fleet services span a wide range of industries, including manufacturing, retail, agriculture, and consumer goods. These industries rely on containerized shipping to transport raw materials, components, and finished products to markets around the world. As such, the container fleet market serves as a critical enabler of global supply chains, supporting economic growth and trade expansion across diverse sectors.

Key players in the container fleet market include major shipping lines such as Maersk Line, Mediterranean Shipping Company (MSC), and COSCO Shipping Lines, among others. These companies dominate market share through their extensive fleets, global network coverage, and comprehensive service offerings. As leaders in the industry, they drive innovation, set industry standards, and shape the direction of the container fleet market. Additionally, container leasing companies and terminal operators play vital roles in the market ecosystem, providing essential services and infrastructure to support containerized shipping operations.

Container Fleet Market Dynamics

"Dynamic Trends in Container Freight Rates: Insights from 2022 and Prospects for Stabilization in 2023"

The container freight market experienced significant fluctuations throughout 2022, following record-high rates at the end of 2021. Early 2022 witnessed a continuation of this upward trend, but by the third quarter, spot rates on major trade lanes notably decreased, indicating a shift from the extreme levels observed previously. By the close of 2022, container rates approached pre-pandemic levels, subsequently stabilizing in the early months of 2023. Factors contributing to this stabilization include the rebalancing of supply and demand dynamics and a reduction in port congestion.

Global containerized trade saw a slight decline in 2022, but container ship carrying capacity expanded by 3.9%, posing a supply-demand imbalance. This surplus raises concerns about supply overcapacity, with projections suggesting a further capacity influx between 2023 and 2025. Spot container freight rates eased in 2023.

Constraints and Trials in the Container Fleet Industry

The container fleet market faces significant challenges, primarily stemming from oversupply and pricing pressures. Low freight rates, driven by an oversupply of vessels and low bunker prices, pose a major obstacle. The imbalance between supply and demand in the tanker sector exacerbates pricing issues, making it difficult to predict demand accurately. With buyers initiating pricing due to low demand, shipping companies are forced to reduce prices based on cost per ton or tanker. Consequently, the reduction in freight prices results in operating costs surpassing earnings, leading to financial strain within the industry. Heavy debts further compound the financial crisis, creating a challenging environment for container fleet operators to navigate. Overall, the industry grapples with the ramifications of oversupply, fluctuating demand, and pricing pressures, which collectively hinder profitability and sustainability.

Strategic Initiatives Driving Growth in the Container Fleet Market

The container fleet market is ripe with opportunities driven by strategic maneuvers aimed at maximizing profitability. Companies are increasingly focusing on enhancing supply chain efficiency and operational productivity to gain a competitive edge. The breaking down of geographical barriers and heightened interdependency among industry verticals necessitate streamlined supply chain processes. Implementing efficient intermodal freight transportation solutions emerges as a critical strategy in this regard. Moreover, there is a growing emphasis on boosting operational efficiency amid shrinking profit margins. Leveraging fleet capacity to its fullest potential stands out as a key tactic to augment profit margins. Additionally, a shift in business strategies towards optimizing inventory and warehouse planning further underscores the potential for market expansion. These strategic moves not only present avenues for revenue growth but also underscore the evolving landscape of the container fleet industry, offering promising prospects for companies to capitalize on.

Container Fleet Market Segment Analysis

Based on Product type, dry containers hold the highest share and it is expected to grow in forecast period. The market analysis report meticulously dissects the container fleet industry, delineating its various segments with precision. Among these segments, including dry container, reefer container, tank container, and special container, the dry container emerges as the frontrunner. Its dominance is attributed to its unparalleled versatility and extensive utility. Dry containers serve as the workhorse of global trade, facilitating the transportation of a diverse range of dry cargo, from electronics to textiles and manufactured goods. Renowned for their cost-effectiveness and ability to shield cargo from external elements, these containers remain indispensable in the logistics ecosystem. As the largest segment, dry containers not only symbolize the backbone of modern trade but also underscore their indispensability across myriad industries, perpetuating their steadfast reign in the container fleet market.

Reefer containers stand as indispensable assets in the transportation realm, specifically tailored for the delicate task of conveying temperature-sensitive cargo. With a primary focus on perishable foods and pharmaceuticals, these containers boast meticulously engineered systems to uphold precise temperature and humidity levels throughout the journey. This meticulous control safeguards the integrity and safety of goods, guaranteeing their quality upon arrival.

Meanwhile, tank containers emerge as veritable workhorses in the transport landscape, specially crafted for the conveyance of liquids and gases. Their significance reverberates across industries like chemical, petrochemical, and food, where the secure transportation of liquids is paramount. Renowned for their robust safety features, tank containers offer a shielded conduit for the transit of hazardous materials, ensuring both the safety of the cargo and the peace of mind of stakeholders.

1. On 14th March 2024, according to the International Tank Container Organisation (ITCO) 2023 Global Tank Container Fleet Survey, the global tank container fleet had 801,800 units on January 1, 2023, up from 737,935 on January 1, 2022, representing an 8.6% increase. 66% of these tanks are managed by more than 235 active operators.

2. The ITCO Survey of the Global Tank Container Market for this year indicates that 67,865 new tank containers were created in 2022 as opposed to 53,285 new units the year before, a rise of around 14,580 units.

3. As of January 1, 2023, there were 801,800 tank containers in the world, compared to 737,935 on the same date in 2022.

4. The leading manufacturers of tank containers, the CIMC, NT Tank, JJAP, Welfit Oddy, Singamas, and Dalian CRRC, are listed in order of quantity produced. The top six account for 97% of all manufacturing worldwide.

Container Fleet Market Regional Insights

The Asia-Pacific region contributes the highest market share during the forecast period. With a high demand for intermodal transportation and an increasing global reliance on reefer cargo shipping, Asia-Pacific stands at the forefront of this dynamic market. Market experts attribute this dominance to the rapid industrialization and production surge observed in developing countries within the region. These nations are transitioning into significant exporters, amplifying the need for robust cargo shipping capabilities. Asia-Pacific boasts a plethora of developing countries across various key business sectors, further solidifying its position as the largest market for the cargo shipping trade. Among these, China takes center stage as a major manufacturer of container fleets within the region. The country's relentless pursuit of technological innovation, particularly in ship capacity and infrastructure development, underpins its pivotal role in driving revenue and market growth within Asia-Pacific's container fleet industry.

North America emerges as a formidable force in the container fleet market, propelled largely by the economic powerhouses of the United States and Canada. The region's robust industrial framework, underscored by thriving sectors such as automotive and oil and gas, underscores a heavy reliance on containerized transportation for facilitating seamless domestic and international trade. This reliance not only underscores the pivotal role of container fleets in sustaining North America's economic vibrancy but also highlights the region's enduring significance as a key player in the global logistics landscape.

Container Fleet Market Competitive Landscapes

Several major firms are fighting for market share in the competitive Container Fleet industry. Archer Daniels Midland (ADM), Cargill, Bunge Limited, Wilmar International, and Louis Dreyfus Company are a few of the significant businesses involved in the Container Fleet industry. These corporations have a robust market presence and frequently employ tactics like partnerships, product launches, and mergers and acquisitions to sustain their competitive advantage. New competitors entering the market are also delivering cutting-edge items and targeting specialized markets. The competitive nature of the Container Fleet market is primarily determined by many variables, including the quality of the product, pricing, distribution networks, and ways of marketing.

1. In 2022, the combined number of tank containers produced by all of the world’s manufacturers totalled over 67,865 new units.

2. In January 2022, Evergreen Marine Corp. declared a new initiative to construct 20 carbon- neutral vessels, with the goal of meeting the International Maritime Organization's ambitious carbon reduction targets by 2050. This strategic decision underscores the shipping giant's ongoing dedication to sustainability and environmental responsibility.

3. ZIM Integrated Shipping Services garnered media attention in April 2022 when it revealed plans to purchase ten additional ultra-large cargo ships. These additions will effectively expand ZIM's operating capacity, enabling the company to cater to the growing demand in the market.

4. In early 2023, Seaspan Corporation, a leading independent charter owner, reported a significant increase in revenue, attributing the growth to escalating leasing rates and robust demand.

5. In January 2022, Evergreen Marine Corp. declared a new initiative to construct 20 carbon- neutral vessels, with the goal of meeting the International Maritime Organization's ambitious carbon reduction targets by 2050. This strategic decision underscores the shipping giant's ongoing dedication to sustainability and environmental responsibility.

Container Fleet Market Scope:Inquire before buying

| Container Fleet Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 13.11 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.8% | Market Size in 2032: | USD 20.59 Bn. |

| Segments Covered: | by Product Type | Dry Container Fleet Reefer Container Fleet Tank Container Fleet Special Container Fleet |

|

| by End User | Automotive Mining and Minerals Oil Gas and Chemicals Food and Agriculture Retails |

||

Container Fleet Market, by Region:

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Container Fleet Market Key Players

North America:

1. Maersk Line (Denmark)

2. Hapag Lloyd (Germany)

3. Matson (USA)

Europe:

1. Westfal-Larsen Shipping A/S (Norway)

2. CMA CGM (France)

3. Mediterranean Shipping Corporation S.A. (Switzerland)

4. Hapag-Lloyd AG (Germany)

5. Westfal-Larsen (Norway)

6. CMA CGM Group (France)

7. Arkas Container Transport S.A. (Turkey)

8. Unifeeder A/S (Denmark)

Asia Pacific:

1. Kawasaki Kisen Kaisha Ltd.(Japan)

2. Evergreen Marine Corporation (Taiwan) Ltd. (Taiwan)

3. China Ocean Shipping (Group) Company (China)

4. Mitsui O.S.K. Lines, Ltd (Japan)

5. Hyundai Merchant Marine Co. Ltd. (South Korea)

6. Mitsui O.S.K. Lines (Japan)

7. NYK Line (Japan)

8. Orient Overseas Container Line Limited (OOCL) (Hong Kong)

9. Yang Ming Marine Transport Corporation (Taiwan)

10. Pacific International Lines Pte Ltd (Singapore)

11. NileDutch (Netherlands)

12. Ocean Network Express Pte. Ltd. (Singapore)

13. Wan Hai Lines Ltd. (Taiwan)

14. ZIM Integrated Shipping Services Ltd (Israel)

FAQs:

1. What are the growth drivers for the Container Fleet Market?

Ans. Dynamic Trends in Container Freight Rates: Insights from 2023 and Prospects for Stabilization in 2024 is the driver of the Global Container Fleet Market.

2. Which region is expected to lead the global Container Fleet Market during the forecast period?

Ans. Asia pacific region is expected to lead the global Container Fleet Market during the forecast period.

3. What was the Global Container Fleet Market size in 2024?

Ans: The Global Container Fleet Market size was USD 13.11 Billion in 2024.

4. What segments are covered in the Container Fleet Market report?

Ans. The segments covered in the Container Fleet Market report are Product type, End User and region.