Automotive Lightweight Materials Market Material Type, Application, Vehicle Type, Manufacturing Process, End Industry and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

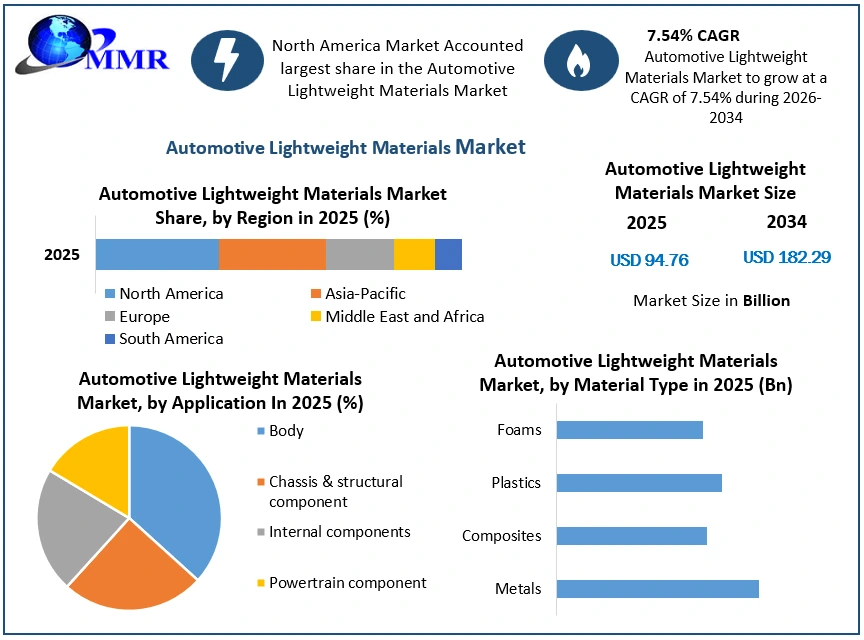

The Automotive Lightweight Materials Market size was valued at USD 94.76 Billion in 2025 and the total Automotive Lightweight Materials revenue is expected to grow at a CAGR of 7.54% from 2026 to 2034, reaching nearly USD 182.29 Billion.

Automotive Lightweight Materials Market Overview

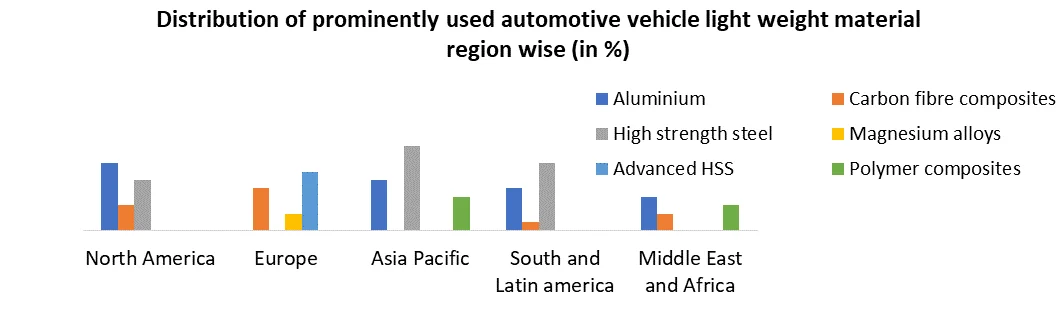

The demand for Automotive Lightweight Materials Market has been driven by the increasing emphasis on fuel efficiency, emission reduction, and compliance with stringent regulatory standards. The rising demand for lightweight materials in the automotive sector is due to the desire to enhance fuel economy and environmental sustainability. These materials allow automakers to reduce vehicle weight, resulting in improved fuel efficiency and lower emissions. Aluminium is a dominant player in the market, widely utilized in the automotive industry due to its lightweight nature and strength. It finds extensive application in vehicle bodies, engine components, and structural parts. The demand for aluminium is expected to persist due to factors such as availability, recyclability, and cost-effectiveness. Carbon fibre reinforced polymer (CFRP) composites offer exceptional strength-to-weight ratios and are increasingly adopted in high-performance and luxury vehicles. However, their high cost and production complexities have limited their widespread use in mainstream vehicles. Ongoing efforts focus on reducing costs and expanding production capacities to enhance CFRP accessibility.

Advanced high-strength steel (AHSS) has gained prominence as a cost-effective lightweighting solution. It provides improved strength and formability compared to traditional steel, enabling weight reduction while maintaining structural integrity. AHSS is prominently employed in safety-critical areas and is anticipated to maintain its strong presence in the market. Magnesium and lightweight plastics, including composites, are also used to reduce vehicle weight. However, their adoption remains limited due to factors such as cost, corrosion resistance, and manufacturing challenges. Continued research and development aim to overcome these limitations and unlock their full potential. The regulatory environment plays a crucial role in driving the adoption of lightweight materials. Stringent emissions and fuel efficiency standards compel automakers to explore lightweight solutions. Compliance with these regulations is a key motivator for integrating lightweight materials across various vehicle segments. Advancements in manufacturing technologies, including innovative joining techniques and hybrid material solutions, have facilitated the integration of lightweight materials into vehicle designs. Improvements in production processes aim to reduce costs and enhance the scalability of lightweight materials.

The Automotive Vehicle Lightweight Material Industry is characterized by intense competition among material suppliers, automakers, and research institutions. It is essential to note that market dynamics can change rapidly due to evolving regulations, technological advancements, and Automotive Lightweight Materials Market forces.

To know about the Research Methodology :- Request Free Sample Report

Automotive Lightweight Materials Market Report Scope

This market research report focuses on providing a comprehensive analysis of the automotive lightweight materials industry. The report covers segments such as aluminium, carbon fibre composites, high-strength steel, magnesium, and lightweight plastics. It aims to offer precise insights into Automotive Lightweight Materials Market trends, key players, emerging technologies, and regulatory landscapes, facilitating informed decision-making for businesses operating in the automotive sector. The collected data underwent rigorous statistical and qualitative analysis to identify and evaluate market trends, drivers, challenges, and opportunities specific to lightweight materials. The analysis encompassed market sizing, growth rates, and forecasts for the automotive lightweight materials industry and its various segments. Advanced data analysis and visualization tools were utilized to ensure accurate interpretation and presentation of the findings. To improve the accuracy and reliability of the research, advanced tools were used throughout the process. These tools facilitated data analysis, visualization, and interpretation, enabling a comprehensive understanding of the market landscape for lightweight materials in the automotive industry.

Automotive Lightweight Materials Market Dynamics

Automotive Lightweight Materials Market Drivers

One primary driver is the urgent need to enhance fuel efficiency and reduce emissions. By reducing the overall weight of vehicles, lightweight materials play a crucial role in achieving improved fuel economy and lower carbon emissions, thus addressing environmental concerns. Stringent government regulations and standards aimed at improving fuel efficiency and curbing greenhouse gas emissions exert pressure on automakers to incorporate lightweight materials. Another key driver is the expanding market for electric and hybrid vehicles. These vehicles require lighter components to counterbalance the weight of batteries and maximize their driving range. Lightweight materials are vital in striking the right balance between vehicle weight, battery capacity, and overall performance, making them indispensable in the development of electric and hybrid vehicles.

The quest for enhanced performance and safety contributes to the growing demand for lightweight materials. These materials offer exceptional strength-to-weight ratios, leading to improved acceleration, handling, braking performance, as well as bolstered crashworthiness and occupant protection when applied strategically in critical structural areas. The advancement of manufacturing technologies has revolutionized the production of lightweight materials, making it more feasible and cost-effective for automakers. Streamlined production processes and an expanded range of lightweight components have facilitated their integration into vehicle designs. Consumer demand for fuel-efficient and eco-friendly vehicles further fuels the adoption of lightweight materials. With a heightened awareness of environmental issues, consumers seek vehicles with better fuel economy and reduced carbon footprints. Lightweight materials, which are associated with improved efficiency and sustainability, align with these consumer preferences.

Automotive Lightweight Materials Market challenges

The Automotive Lightweight Materials Market encounters significant challenges that impede its widespread adoption and growth. These challenges include cost considerations, manufacturing complexities, material availability, compatibility with existing infrastructure, durability and longevity concerns, safety standards and regulations, and consumer perception and acceptance. The cost of lightweight materials is a prominent challenge, as their production costs are generally higher compared to traditional materials. Thishinder their economic viability, particularly for mass-market vehicles. The manufacturing processes involved in working with lightweight materials can be complex, often requiring specialized techniques and equipment. As a result, production cycles may become lengthier.

The limited availability of specific lightweight materials and the need for a stable supply chain further compound the challenges. Ensuring a consistent and reliable supply of these materials can be demanding, potentially affecting the industry's ability to meet growing demands. Moreover, integrating lightweight materials into existing infrastructure poses compatibility issues, requiring modifications and adjustments to manufacturing facilities and equipment. Durability and longevity are also concerns with lightweight materials. They must meet stringent standards to ensure they withstand demanding operating conditions and maintain their performance over time. Additionally, adherence to safety regulations is crucial, ensuring that lightweight materials provide adequate protection to occupants in the event of accidents. Consumer perception and acceptance present another obstacle. Some individuals may associate lighter vehicles with compromised safety or durability, requiring efforts to educate and change perceptions.

Automotive Lightweight Materials Market opportunities

The Automotive Lightweight Materials Market holds significant opportunities for growth and advancement. One notable opportunity is the rising demand for fuel efficiency and emission reduction. Lightweight materials have the potential to greatly enhance fuel efficiency, enabling automakers to meet stringent fuel economy standards and reduce carbon emissions. Another opportunity lies in the expanding market for electric and hybrid vehicles, where lightweight components are essential to offset battery weight and improve overall performance. Technological advancements play a pivotal role in unlocking opportunities in the lightweight material market. Innovations in materials science, manufacturing techniques, and design capabilities have paved the way for high-performance lightweight components, such as advanced composites, nanomaterials, and lightweight alloys.

Cost reduction and scalability are critical factors in driving the adoption of lightweight materials. By optimizing production processes, exploring alternative materials, and improving manufacturing efficiency, lightweight materials become more cost-effective and viable for a wider range of vehicles. Sustainability is a growing concern, and lightweight materials offer environmental benefits. Their improved fuel efficiency and reduced emissions contribute to a more sustainable transportation sector. Moreover, their recyclability aligns with the principles of a circular economy, presenting opportunities to meet consumer preferences and regulatory requirements. Collaboration and partnerships among automakers, material suppliers, research institutions, and technology companies foster innovation in the lightweight material market. Joint research projects and strategic partnerships drive advancements in material development, manufacturing processes, and application techniques.

Automotive Lightweight Materials Market trends

One prominent trend is the increasing demand for lightweight materials driven by the need to enhance fuel efficiency, reduce emissions, and improve overall vehicle performance. Lightweight materials enable automakers to achieve these objectives by reducing vehicle weight without compromising safety or structural integrity. Another noteworthy trend in the Automotive Lightweight Materials Market is the adoption of advanced composite materials, such as carbon fibre-reinforced polymers (CFRP). These materials offer exceptional strength-to-weight ratios, making them ideal for producing lightweight yet strong components. Automakers are increasingly incorporating composites into their vehicle designs to achieve weight reduction and improve fuel efficiency.

In addition to composites, lightweight metals like aluminium, magnesium, and high-strength steel alloys are gaining prominence in automotive manufacturing. These metals strike a balance between weight reduction and structural integrity, and they are used in various vehicle components such as body panels, chassis, and powertrain to reduce overall weight and enhance fuel efficiency. Sustainability is another significant trend driving the development of lightweight materials. The industry is focusing on the use of sustainable materials, including bio-based composites and recycled polymers, which offer reduced environmental impact throughout their lifecycle. These materials align with the automotive industry's sustainability goals and contribute to a greener and more eco-friendly future.

The rise of electric vehicles (EVs) is also influencing the Automotive Lightweight Materials Market. Lightweight materials are essential in EVs to maximize energy efficiency and optimize performance. They are integrated into components such as battery enclosures, frames, and interiors to reduce vehicle weight, extend driving range, and improve battery efficiency. Advancements in manufacturing technologies are further shaping the market. Additive manufacturing (3D printing) and advanced joining techniques enable the production of complex lightweight components with precision and customization. These technologies also contribute to reduced material waste and faster production cycles, making the adoption of lightweight materials more feasible and cost-effective.

Collaboration and partnerships among automotive manufacturers, material suppliers, research institutions, and technology companies are prevalent in the lightweight material market. These collaborations drive innovation, accelerate material development, and enhance manufacturing processes. Through joint research projects and partnerships, expertise, resources, and technological advancements are shared, pushing the boundaries of lightweight material applications in the automotive industry.

Automotive Lightweight Materials Market Regional Analysis

North America stands as a prominent market for automotive lightweight materials. Stringent fuel efficiency regulations, increasing consumer demand for fuel-efficient vehicles, and the presence of major automotive manufacturers contribute to its significance. The region has witnessed notable investments in research and development in the Automotive Lightweight Materials Market, leading to the widespread adoption of advanced lightweight materials in vehicle manufacturing. Europe, known for its emphasis on sustainability and emission reduction, represents another important Automotive Lightweight Materials Market. Stringent emission regulations and the preference for eco-friendly vehicles drive the demand for lightweight materials in the region. European automakers were early users of lightweight technologies, using sophisticated composites and lightweight metals to reduce fuel consumption and environmental effect.

China, Japan, and South Korea's rising vehicle manufacturing drives Asia Pacific's automotive lightweight materials market. A rapidly growing middle class, disposable earnings, and increased urbanisation drive regional car demand. Asia Pacific automakers use lightweight materials to improve fuel efficiency, emissions, and performance. South America and the Middle East & Africa regions experience steady growth in the automotive lightweight material market. Improving economic conditions, increasing urbanization, and rising awareness of fuel efficiency and environmental impact drive the adoption of lightweight materials in these regions. South America and the Middle East & Africa are developing markets for lightweight, cost-effective solutions.

Challenges and opportunities vary by region. North America struggles with lightweight material costs, whereas Europe prioritises environmental production. Asia Pacific offers an opportunity to cater to the growing demand for lightweight materials in the expanding automotive manufacturing sector. Government regulations, economic conditions, consumer preferences, and the presence of key automotive manufacturers play crucial roles in shaping the regional dynamics of the Automotive Lightweight Materials Market. Understanding these regional variations is essential for market participants to tailor their strategies, investments, and product offerings accordingly.

Automotive Lightweight Materials Market Recent Industry Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 29 June 2026 | AD Ports Group & Emirates Global Aluminium (EGA) | The companies signed an agreement to advance logistics, shipping, and raw material handling solutions tailored for large-scale premium aluminium distribution. | This initiative optimizes the supply chain infrastructure required to distribute structural lightweight aluminum sheets to global automotive export markets. |

| 24 June 2026 | Emirates Global Aluminium (EGA) | The company officially inaugurated the UAE's largest industrial aluminium recycling plant to process premium scrap metal. | The facility boosts the availability of low-carbon, secondary aluminum alloys required by global car manufacturers to lower the embedded lifecycle emissions of lightweight vehicle architectures. |

| 29 April 2026 | Century Aluminum Company | The company completed its primary expansion phase and poured first hot metal at its Mt. Holly facility in South Carolina, increasing total U.S. primary aluminum production capacity by 10%. | The ramp-up strengthens the domestic supply chain stability of high-purity metal needed for automotive casting, structural components, and extrusion programs. |

| 10 February 2026 | Emirates Global Aluminium (EGA) & Century Aluminum | The joint-venture alliance appointed engineering firm Bechtel to lead preparatory engineering and design work for a multi-billion dollar greenfield primary aluminum smelter in Oklahoma. | The massive project targets a long-term supply volume of 750,000 tonnes of primary metal specifically to fulfill severe structural material shortages across North American automotive manufacturing grids. |

| 26 January 2026 | Century Aluminum Company & Emirates Global Aluminium (EGA) | The companies finalized a formal joint development agreement to build the first domestic primary aluminum smelter in the United States in nearly 50 years. | This milestone doubles total U.S. domestic supply capacities, insulating automotive OEMs from volatile tariff penalties and logistics bottlenecks for lightweight chassis and body-in-white structures. |

| 06 March 2025 | McLaren Automotive | The automaker commercialized an aerospace-derived Automated Rapid Tape (ART) production process to manufacture high-volume carbon fiber structural parts. | The process scales production efficiency, minimizes material scrap waste, and optimizes the strength-to-weight ratio of high-performance composite components. |

Automotive Lightweight Materials Market Segment Analysis

The Automotive Lightweight Materials Market is analysed through segment analysis, which provides insights into the specific areas where these materials are extensively used. Within the body structure segment, the implementation of lightweight materials is of utmost importance in achieving a reduction in overall vehicle weight, while simultaneously ensuring the preservation of structural integrity and safety standards. Aluminium, high-strength steel, and carbon fibre composites are commonly utilised materials that aid in weight reduction and fuel efficiency enhancement.

Lightweight materials are utilised within the interior segment to improve comfort, aesthetics, and functionality. Polymer composites, such as glass fibre-reinforced plastics (GRP), are frequently incorporated into interior trim panels, dashboard components, and seat structures. These materials offer weight reduction, design flexibility, and improved passenger experience. In the chassis and suspension segment, lightweight materials are essential for providing stability and handling. Aluminium and high-strength steel alloys are commonly employed to reduce weight while maintaining structural integrity, ensuring optimal handling and ride quality.

The electrical and electronics segment relies on lightweight materials for various components. Polymer composites and aluminium are used in electrical and electronic enclosures, wiring harnesses, and connectors, enabling weight reduction and efficient performance of these systems. Doors, hoods, fenders, and other exterior components are examples of segments where lightweight materials are utilised. These materials contribute to vehicle weight reduction, enhanced fuel economy, and enhanced overall performance.

Automotive Lightweight Materials Market competitive landscape

The automotive vehicle lightweight material industry is experiencing intense competition due to the increasing need for lightweight solutions that enhances fuel efficiency, reduce emissions, and improve overall vehicle performance. The market's leading contenders are consistently endeavouring to enhance their competitive advantage by providing inventive products and solutions. One significant factor influencing the competition is the regulatory environment. Stringent emission regulations and fuel efficiency standards imposed by governments worldwide have pushed automotive manufacturers to adopt lightweight materials in their vehicle designs. This has created a strong demand for lightweight materials and intensified competition among suppliers to meet these requirements effectively.

Another aspect of the competitive environment is the focus on sustainability. As the automotive industry places a greater emphasis on environmental consciousness, lightweight materials that contribute to reduced energy consumption and lower carbon emissions are highly sought after. Companies that can provide sustainable lightweight solutions have a competitive advantage in the market. Moreover, the industry's competitive landscape is influenced by advancements in material science and manufacturing technologies. Companies investing in research and development to develop new lightweight materials and manufacturing processes gain a competitive edge. This includes exploring alternative materials such as carbon fibre composites, high-strength steels, aluminium alloys, and polymer composites.

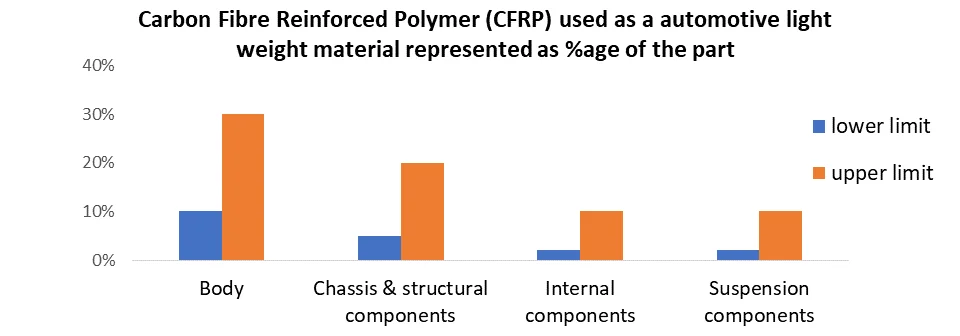

Collaborations and partnerships between lightweight material suppliers and automotive manufacturers also play a crucial role in the competitive landscape. The strategic partnerships between companies enable the creation of personalised and efficient lightweight solutions that cater to the unique needs of various vehicle models. This provides a competitive edge to the collaborating firms. Competitiveness depends on cost-effectiveness. Lightweight materials may cost more in the current market. Therefore, organisations that offer affordable alternatives while retaining quality and performance have a competitive advantage. One of the most unique automotive vehicle lightweight materials used is carbon fibre reinforced polymer (CFRP). CFRP is an advanced composite material that combines carbon fibres and a polymer matrix. It offers an exceptional strength-to-weight ratio, making it significantly lighter than traditional materials while maintaining high structural integrity.

One of the most unique automotive vehicle lightweight materials used is carbon fibre reinforced polymer (CFRP). CFRP is an advanced composite material that combines carbon fibres and a polymer matrix. It offers an exceptional strength-to-weight ratio, making it significantly lighter than traditional materials while maintaining high structural integrity.

Automotive Lightweight Materials Market Scope: Inquire before buying

| Automotive Lightweight Materials Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 94.76 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 7.54% | Market Size in 2034: | USD 182.29 Bn. |

| Segments Covered: | by Material Type | Metals Composites Plastics Foams |

|

| by Application | Body Chassis & structural component Internal components Powertrain component |

||

| by Vehicle Type | Passenger Commercial |

||

| by Manufacturing Process | Casting Extrusion Injection moulding Compression moulding Pultrusion Resin transfer moulding (RTM) Filament winding |

||

| by End Industry | Commuter mobility Corporate mobility Freight mobility |

||

Automotive Lightweight Materials Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Company Profile: Automotive vehicle lightweight material Key players

North America:

1. Alcoa Corporation (United States)

2. Novelis Inc. (United States)

3. Owens Corning (United States)

4. Toray Industries, Inc. (United States)

5. 3M Company (United States)

6.DuPont de Nemours, Inc. (United States)

7. General Motors Company (United States)

8. Ford Motor Company (United States)

9. Magna International Inc. (Canada)

10. Arconic Inc. (United States)

Europe:

1. ArcelorMittal S.A. (Luxembourg)

2. BASF SE (Germany)

3. Covestro AG (Germany)

4. Thyssenkrupp AG (Germany)

5. Solvay S.A. (Belgium)

6. SGL Carbon SE (Germany)

7. Evonik Industries AG (Germany)

8. Tata Steel Europe Ltd. (United Kingdom)

9. Saint-Gobain SA (France)

10. BMW Group (Germany)

Asia Pacific:

1. Mitsubishi Chemical Holdings Corporation (Japan)

2. Toyota Motor Corporation (Japan)

3. Hyundai Motor Company (South Korea)

4. Nippon Steel Corporation (Japan)

5. Sumitomo Chemical Co., Ltd. (Japan)

6. Honda Motor Co., Ltd. (Japan)

7. LG Chem Ltd. (South Korea)

8. POSCO (South Korea)

9. Geely Automobile Holdings Limited (China)

10. Tata Motors Limited (India)

Middle East & Africa:

1.Saudi Basic Industries Corporation (Saudi Arabia)

2.Emirates Global Aluminium (United Arab Emirates)

3.TATA Steel Middle East FZE (United Arab Emirates)

4.Ezz Steel (Egypt)

5.Rigidal Industries LLC (United Arab Emirates)

6.Safal Group (South Africa)

7.SABIC (Saudi Arabia)

8.ElvalHalcor Hellenic Copper and Aluminium Industry S.A. (Greece)

South America:

1.Gerdau S.A. (Brazil)

2.Usiminas (Brazil)

3.Embraer S.A. (Brazil)

4.Ternium S.A. (Argentina)

5.Aluar Aluminio Argentino S.A.I.C. (Argentina)

6.Novelis do Brasil Ltda. (Brazil)

7.Tenaris (Argentina)

8.Votorantim S.A. (Brazil)

FAQs

Q1: What is the size of the global Automotive Lightweight Materials Market?

A: The Automotive Lightweight Materials Market size was valued at USD 94.76 Billion in 2025 and the total Automotive Lightweight Materials revenue is expected to grow at a CAGR of 7.54% from 2026 to 2034, reaching nearly USD 182.29 Billion.

Q2: What are the key factors driving the growth of the Automotive Lightweight Materials Market?

A: The growth of the Automotive Lightweight Materials Market is primarily driven by increasing demand for fuel-efficient vehicles, stringent emission regulations, the shift towards electric and hybrid vehicles, and the need to improve overall vehicle performance.

Q3: Which lightweight materials are expected to dominate the market?

A: Aluminium, carbon fibre reinforced polymer (CFRP), and advanced high-strength steel (AHSS) are expected to dominate the Automotive Lightweight Materials Market due to their excellent strength-to-weight ratio, cost-effectiveness, and widespread availability.

Q4: Which regions are witnessing significant growth in the Automotive Lightweight Materials Market?

A: North America and Europe are currently leading the Automotive Lightweight Materials Market due to the presence of established automotive industries, stringent emission standards, and a focus on sustainability. However, the Asia Pacific region is also witnessing significant growth due to the rapid expansion of the automotive sector in emerging economies such as China and India.

Q5: Who are the major players in the Automotive Lightweight Materials Market?

A: Major players in the Automotive Lightweight Materials Market include companies such as Alcoa Corporation, Novelis Inc., Toray Industries, Inc., BASF SE, ArcelorMittal S.A., and Mitsubishi Chemical Holdings Corporation. These companies are actively involved in research and development activities to innovate lightweight materials and cater to the evolving needs of the automotive industry.