Automotive Hypervisor Market Size by Type, Vehicle Type, Bus System, End-User, Level Of Autonomous Driving and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

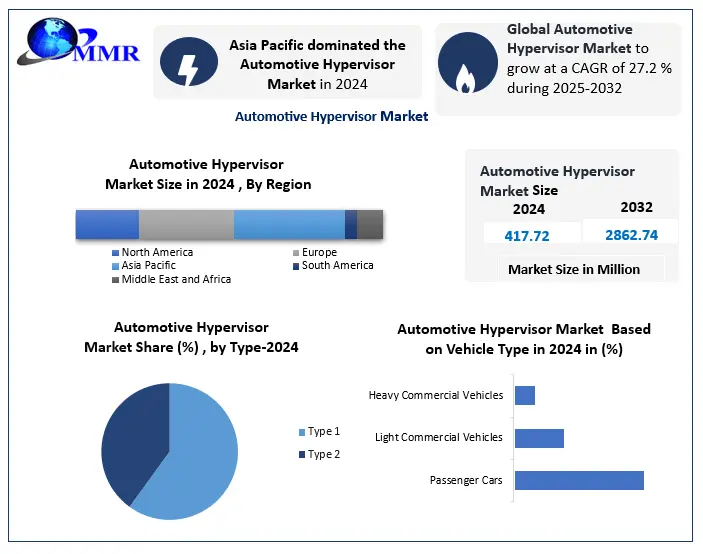

Automotive Hypervisor Market size was valued at 417.72 million USD in 2024, and the total Automotive Hypervisor Market is expected to grow at 27.2% from 2025 to 2032, reaching nearly 2862.74 million USD.

Automotive Hypervisor Market Overview

An automotive hypervisor is a software platform that allows a number of automotive applications and operating systems to run on a single hardware platform. The automotive hypervisor is a system that is responsible for managing the distribution of resources and isolating applications for the highest level of safety, security, and reliability in vehicle electronic and software systems.

The Automotive Hypervisor Market has been witnessing rapid growth, because of the increasing complexity of vehicle electronic systems and the growing demand for advanced driver assistance systems (ADAS), infotainment, and connectivity solutions. Automotive hypervisors, which were initially developed as basic virtualization tools to enable multiple operating systems on a single hardware platform, have evolved significantly, offering real-time performance, enhanced security, and scalability. These advancements have made them vital for connected and autonomous vehicles, supported by innovations in hardware-assisted virtualization, secure boot mechanisms, and adaptive partitioning.

Global adoption has accelerated, with ADAS now integrated into over 90% of newly manufactured premium vehicles and in-vehicle infotainment systems becoming standard in more than 75% of passenger cars. The rise of electric mobility has further boost Automotive Hypervisor Market growth, as global electric vehicle (EV) sales have surpassed 14 million units in 2024, and autonomous driving pilot programs have expanded to over 30 countries. This surge in technology integration was created strong demand for hypervisors to optimize resource utilization, improve safety, and support complex software ecosystems.

The rapid EV adoption in China, India and increasing government safety regulations, and investments in intelligent transportation systems helps to drive the Automotive Hypervisor Industry. Key players such as BlackBerry QNX, Siemens (Mentor Graphics), Wind River, Green Hills Software, and VMware have been competing on performance, security compliance (ISO 26262, ISO 21434), and strategic OEM partnerships. Their innovations in real-time virtualization and secure system architectures have positioned automotive hypervisors as a core enabler of next-generation software-defined vehicles. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Automotive Hypervisor Market Dynamics

Growing adoption of advanced driver-assistance systems (ADAS) to drive the Automotive Hypervisor Market

The rising implementation of Advanced Driver-Assistance Systems (ADAS) is a key driver for the automotive hypervisor market. Modern vehicles integrate multiple complex electronic systems such as ADAS, infotainment, and advanced connectivity which require efficient resource allocation, real-time processing, and isolation of critical functions. Hypervisor solutions enable these capabilities by allowing multiple operating systems to run securely on a single hardware platform, ensuring safety and performance.

The shift towards electric vehicles (EVs) has further accelerated this trend. For instance, Tesla’s EV platforms utilize hypervisors to optimize resource utilization, improve scalability, and support continuous software updates. Similarly, the advancement of autonomous driving demands robust computing environments capable of running diverse software stacks. Companies such as Waymo leverage hypervisors to manage the highly complex software ecosystem required for self-driving operations.

Compliance with stringent safety standards such as ISO 26262 also promotes hypervisor adoption, ensuring functional safety in critical vehicle systems. Additionally, the growth of software-defined vehicle architectures and demand for cost optimization are pushing automakers to adopt centralized computing platforms supported by hypervisors.

Collaborations in the industry further enhance market growth. For example, NVIDIA and Continental have partnered to develop hypervisor-enabled automotive solutions that integrate safety, infotainment, and ADAS functions efficiently. The rise of Mobility-as-a-Service (MaaS) models such as Uber’s fleet management also benefits from hypervisors, enabling reliable and scalable vehicle operations. The convergence of safety regulations, autonomous driving advancements, EV adoption, and connected vehicle trends positions hypervisor technology as a critical enabler in next-generation automotive architectures.

High Implementation Costs to restrain the Automotive Hypervisor Market Growth

The High implementation costs and integration complexity remain primary challenges, as deploying hypervisor solutions often requires advanced hardware upgrades, extensive software customization, and specialized technical expertise.

Specialized hardware requirements, as hypervisors demand advanced System-on-Chips (SoCs), increased RAM, enhanced security modules, and robust Electronic Control Units (ECUs). Upgrading existing vehicle architectures especially in older or budget models entails significant costs. Software development and integration also pose barriers, requiring heavy investment in research and development, rigorous system integration, and extensive testing to ensure compatibility across diverse hardware platforms and operating systems. Maintenance and upgrade requirements add complexity, as hypervisor systems need continuous updates, security patches, and adherence to evolving industry standards such as ISO 26262 and UNECE WP.29. Each software update or introduction of a new vehicle feature can trigger substantial additional costs. For mainstream OEMs, the complexity and risk of retrofitting existing models or designing new platforms specifically for hypervisors can be prohibitive. This often limits adoption to luxury carmakers or high-end models where the investment can be justified by premium pricing.

Regulatory compliance further amplifies the challenge, as meeting stringent safety and cybersecurity requirements demands extensive certification, audits, and additional engineering efforts. Smaller or cost-sensitive automakers struggle to bear these expenses, particularly in competitive markets where cost efficiency is critical. These combined factors ranging from costly hardware upgrades to ongoing regulatory and technical burdens create significant barriers to scaling hypervisor adoption across all vehicle segments, potentially slowing the market’s growth despite strong demand for advanced in-vehicle computing and virtualization solutions.

Electric Vehicle Growth creates lucrative growth opportunities to the Automotive Hypervisor Market

The growth of the electric vehicle (EV) market presents a significant opportunity for the Automotive Hypervisor Market. EVs demand advanced software integration for battery management, power distribution, real-time safety systems, infotainment, and connectivity. Hypervisors enable these diverse applications to run securely and efficiently on shared hardware, facilitating system consolidation and reducing the number of Electronic Control Units (ECUs). This not only saves space and costs but also optimizes energy use critical for EV efficiency.

With EV adoption surging over 4 million units sold globally in Q1 2025 alone automakers are increasingly integrating autonomous and connected features, making hypervisors essential for isolating safety-critical tasks from non-critical ones. This ensures functional safety, supports over-the-air updates, and meets stringent regulatory standards in markets such as North America and Europe.

Leading EV manufacturers such as Tesla, BMW, Mercedes-Benz, and Volkswagen are already deploying hypervisor platforms (e.g., BlackBerry QNX, Green Hills Software) to integrate ADAS, battery monitoring, and infotainment within unified architectures. Regional policies, such as Brazil’s $3.8 billion green mobility incentives, are accelerating adoption by funding advanced vehicle platforms. As the EV market grows toward 245 million units globally by 2030, hypervisor adoption rise in parallel, positioning the technology as a cornerstone of next-generation electric mobility.

Automotive Hypervisor Market Segment Analysis:

Based on Type, the autonomous hypervisor market is segmented by type Type 1, and Type 2. In 2024, Type 1 hypervisors dominated the Automotive Hypervisor Market, driven by their ability to operate directly on hardware, delivering superior efficiency, low latency, and enhanced security. By granting direct access to system resources, they are ideal for mission-critical automotive functions such as advanced driver assistance systems (ADAS), autonomous driving platforms, and high-reliability infotainment systems. Their robust performance and isolation capabilities make them the preferred choice for safety-critical applications, where seamless operation and stringent cybersecurity are essential.

In contrast, Type 2 hypervisors run on top of an operating system, introducing additional latency and slightly reduced security. However, they offer simpler installation, lower deployment costs, and easier maintenance, making them suitable for less demanding automotive applications, including prototype testing, secondary infotainment systems, and non-critical connectivity solutions. Automakers often select Type 1 hypervisors for electric and premium vehicles, where maximum performance and safety are priorities, while Type 2 solutions cater to use cases prioritizing flexibility and faster integration. This performance-security balance paved Type 1’s position as the market leader

Based on Vehicle Type, the autonomous hypervisor market Segment by vehicle type into passenger cars, light commercial vehicles (LCV), and heavy commercial vehicles (HCV) segments. In 2024, the passenger car segment held the largest share of the Automotive Hypervisor Market. the strong demand for advanced features, rapid urbanization, and cutting-edge technology integration. Passenger cars increasingly adopt hypervisor technology to power infotainment, ADAS, connectivity, and autonomous driving systems securely on shared hardware. Rising living standards and personal transportation needs boosted sales, with Asia Pacific capturing over 39.8% of the market. Automakers such as Tesla, BMW, and Mercedes-Benz prioritized passenger cars for innovations, leveraging hypervisors to enhance safety, performance, and user experience. The shift toward connected, electric, and semi-autonomous vehicles is most prominent in this segment, supported by regulatory and sustainability goals. Hypervisors enable efficient system consolidation, reducing costs while improving functionality. Notable examples include Tesla’s Model S/X and BMW’s i Series, which showcased hypervisor-driven ADAS and connectivity. This made passenger cars the dominant and fastest-growing segment for automotive hypervisor solutions.

Automotive Hypervisor Market Regional Insights:

Asia Pacific Dominated the Automotive Hypervisor Market

The Asia Pacific dominated the Automotive Hypervisor Market in 2024. The demand for luxury segment vehicles in countries such as India and Thailand is boosting the adoption of automotive hypervisors. The increasing uptake of advanced features such as ADAS, in-vehicle infotainment, and navigation systems in next-generation vehicles is boosting the overall demand for hypervisors in the region. Asia Pacific boasts a robust ecosystem for the development of self-driving cars, with the presence of tech giants, automotive OEMs, and tier 1 suppliers. Collaborations among these stakeholders, coupled with support from government agencies, further augur well for the growth of the automotive hypervisor market in the region during the forecast period.

The Asia Pacific region was dominated the global automotive hypervisor market in 2024. The vast automotive production base, rapid technology adoption, and accelerating electric vehicle (EV) growth. The region accounts for over 60% of global vehicle production, with China, Japan, South Korea, and India leading manufacturing output. This scale creates a strong foundation for embedding hypervisor technology in new models.

Advanced vehicle features such as ADAS, infotainment, connected services, and autonomous driving are gaining traction across the region, all of which rely on hypervisors for secure and efficient system integration. EV adoption is a major growth engine China alone registered 8.1 million new electric cars in 2023, a 35% year-on-year rise while India, Japan, and South Korea also see rapid growth driven by government initiatives like China’s “Made in China 2025” and India’s FAME II.

Leading OEMs such as BYD, Toyota, Hyundai, and Tata Motors, alongside technology firms like Panasonic, Renesas Electronics, and NXP Semiconductors, are investing heavily in hypervisor-enabled platforms. The deployments range from BYD’s integrated ADAS and infotainment systems in China to Hyundai’s hypervisor-supported EV safety features in South Korea. Collaborative ecosystems involving automakers, tech suppliers, and governments further accelerate adoption, solidifying Asia Pacific’s position as the global hub for automotive hypervisor innovation.

Automotive Hypervisor Market Competitive Landscape

The automotive hypervisor market is highly competitive, driven by collaborations, technological innovations, and expanding applications in software-defined vehicles. Key players include BlackBerry Limited, Panasonic Holdings Corporation, Green Hills Software, Sasken Technologies, Visteon Corporation, Siemens AG, Wind River Systems, Renesas Electronics, Continental, Harman, Hangsheng Technology, and IBM. BlackBerry’s QNX Type 1 hypervisor is widely adopted for secure, multi-OS integration, with partnerships like ETAS GmbH and Marelli enhancing safety-critical and eCockpit solutions. Panasonic Automotive Systems leads in virtualization security and high-performance computing innovations, including the Neuron HPC platform and vSkipGen virtual cockpit. NXP Semiconductors’ S32G Vehicle Integration Platform accelerates software-defined vehicle development. Industry collaborations, such as LDRA with OpenSynergy, strengthen cybersecurity strategies for embedded automotive systems. These companies focus on integrating ADAS, infotainment, and connectivity while ensuring compliance with safety standards like ISO 26262, leveraging hypervisors to enable system consolidation, security, and OTA capabilities positioning themselves to capture growth in the rapidly evolving EV and autonomous vehicle landscape.

Automotive Hypervisor Market Key Developments

• June 2021: LDRA, a provider of automated software verification, testing tools, and analysis services, partnered with automotive embedded software specialist OpenSynergy to promote a defense-in-depth strategy for embedded automotive functions and applications using hypervisor technology.

• February 2022: NXP Semiconductors launched the S32G Vehicle Integration Platform, designed to accelerate the development of software-defined vehicles (SDVs) using S32G vehicle network processors. The platform supports processor evaluation, software development, rapid prototyping, and real-time performance monitoring.

• January 2023: Panasonic Automotive Systems Co., Ltd. introduced VERZEUSE for Virtualization Extensions, an advanced virtualization security solution aimed at protecting next-generation vehicle cockpit systems from cyber-attacks by consolidating multiple ECUs into a single ECU via a hypervisor platform.

• November 2023 : Panasonic Automotive Systems released Virtual SkipGen (vSkipGen) on AWS Marketplace, enabling early-stage automotive development without physical hardware. vSkipGen is a virtual replica of Panasonic’s 3rd generation SkipGen Digital Cockpit, developed in collaboration with Amazon.

• January 2024: Panasonic Automotive Systems unveiled Neuron™ HPC, a high-performance computing platform that supports both software and hardware upgrades across a vehicle’s lifecycle, addressing evolving SDV requirements.

• April 2024: BlackBerry Limited partnered with ETAS GmbH to co-develop and market software solutions that enhance safety-critical functions in next-generation SDVs.

Automotive Hypervisor Market Key Trends

1. Rising Adoption of Hypervisors to Support Advanced Vehicle Functionalities

Across regions, there is a clear shift toward vehicles with advanced driver assistance systems (ADAS), connected features, and autonomous capabilities. Markets such as the U.S., Europe, and Asia Pacific are witnessing strong demand for hypervisors as they efficiently manage multiple ECUs and enable seamless integration of complex electronic systems. This trend is fueled by luxury and premium vehicle growth in the U.S. and India, regulatory-driven safety feature adoption in Europe, and consumer preference for connected vehicles in Asia Pacific.

2. Regulatory and Technological Push Accelerating Hypervisor Integration

Global automotive markets are experiencing a dual push from stringent safety, emissions, and cybersecurity regulations, alongside rapid technological innovation. Governments in regions like the UK, Germany, and Latin America are promoting EVs, autonomous driving, and secure vehicle architectures. This is compelling OEMs and technology providers to deploy hypervisors to meet compliance requirements, enhance vehicle performance, and safeguard data, making regulatory-driven technology adoption a central growth driver worldwide.

Automotive Hypervisor Market Scope: Inquire before buying

| Automotive Hypervisor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 417.72 Mn. |

| Forecast Period 2025 to 2032 CAGR: | 27.2% | Market Size in 2032: | USD 2862.74 Mn. |

| Segments Covered: | by Type | Type 1 Type 2 |

|

| by Vehicle Type | Passenger Cars Light Commercial Vehicles Heavy Commercial Vehicles |

||

| by Bus System | CAN LIN Ethernet Flexray |

||

| by End-User | Economy vehicles Mid-priced vehicle Luxury vehicle |

||

| by Level Of Autonomous Driving | Semi-autonomous Vehicle Autonomous Vehicle |

||

Automotive Hypervisor Market, by Region

North America (United States, Canada, Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Philippines, Thailand, Vietnam, Rest of Asia Pacific)

Middle East and Africa (MEA) (South Africa, GCC, Nigeria, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Rest of South America)

Automotive Hypervisor Market, Key Players

North America

1. BlackBerry –Canada

2. Green Hills Software – USA

3. Harman International – USA

4. Qualcomm Technologies – USA

5. Texas Instruments – USA

6. Lynx Software Technologies – USA

7. VMware – USA

Europe

1. NXP Semiconductors – Netherlands

2. Siemens – Germany

3. Elektrobit – Germany

4. SYSGO – Germany

5. OpenSynergy – Germany

6. Luxoft – Switzerland

7. QT Company – Finland

8. ETAS – Germany

9. Infineon Technologies – Germany

Asia-Pacific

1. Panasonic – Japan

2. Renesas Electronics – Japan

3. Visteon Corporation – USA

4. Sasken Technologies – India

5. KPIT Technologies – India

6. Tata Elxsi – India

7. Hangsheng Technology – China

Frequently Asked Questions:

1] What Major Key players in the Global Automotive Hypervisor Market report?

Ans. The Major Key players covered in the Automotive Hypervisor Market report are BlackBerry QNX, Green Hills Software, Wind River Systems, Mentor (a Siemens Business), Wind River Systems Red Hat (part of IBM).

2] Which region is expected to hold the highest share in the Global Automotive Hypervisor Market?

Ans. Asia Pacific region is expected to hold the highest share in the Automotive Hypervisor Market.

3] What is the market size of the Global Automotive Hypervisor Market by 2030?

Ans. The market size of the Automotive Hypervisor Market by 2032 is expected to reach US$ 2862.74 Million.

4] What is the forecast period for the Global Automotive Hypervisor Market?

Ans. The forecast period for the Automotive Hypervisor Market is 2025-2032.

5] What was the market size of the Global Automotive Hypervisor Market in 2024?

Ans. The market size of the Automotive Hypervisor Market in 2024 was valued at US$ 417.72 Million.