Global Ethylene Oxide Market by Applications, End Use, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

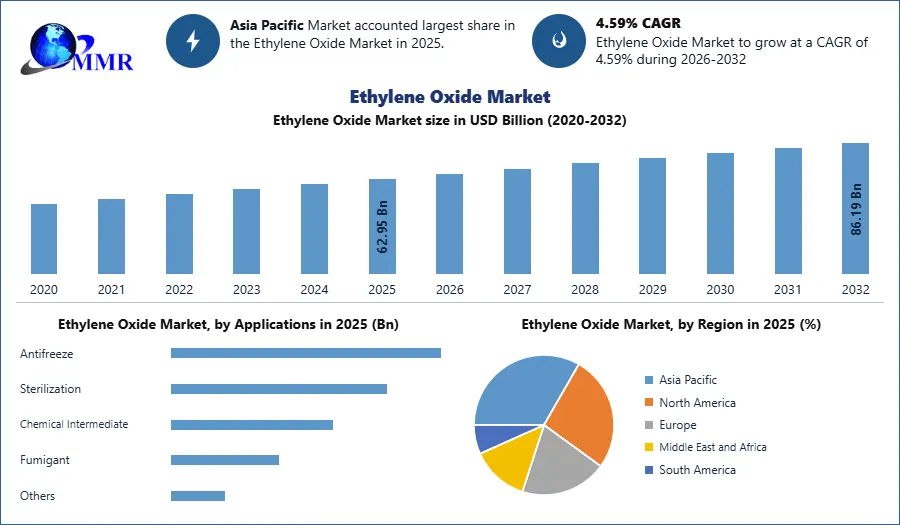

The Ethylene Oxide Market size was valued at USD 62.95 Billion in 2025 and the total Ethylene Oxide revenue is expected to grow at a CAGR of 4.59% from 2026 to 2032, reaching nearly USD 86.19 Billion.

Global Ethylene Oxide Market Overview:

The global ethylene oxide market is witnessing steady growth, driven by its critical role as an intermediate chemical in the production of ethylene glycol, ethoxylates, ethanolamines, glycol ethers, and polyethylene glycol, which are widely used across automotive, packaging, textiles, personal care, detergents, and pharmaceutical industries. Ethylene oxide is primarily consumed in the manufacture of ethylene glycol, a key raw material for polyester fibers, polyethylene terephthalate (PET) resins, antifreeze formulations, and industrial coolants, making it indispensable to several downstream industries. In addition to its chemical applications, ethylene oxide remains an essential sterilizing agent for heat- and moisture-sensitive medical devices, supporting demand from the global healthcare sector.

Market growth is further supported by increasing demand for polyester textiles, expanding automotive production, rising consumption of PET packaging, and growing investments in industrial manufacturing across emerging economies. The healthcare industry's increasing reliance on sterile medical equipment, coupled with the expansion of pharmaceutical manufacturing and healthcare infrastructure, is also contributing to market expansion. Technological advancements in ethylene oxide production, including process optimization, catalyst innovations, and energy-efficient manufacturing technologies, are improving operational efficiency while reducing production costs. Furthermore, manufacturers are increasingly investing in bio-based feedstocks, emission reduction technologies, and sustainable production processes to comply with stringent environmental regulations and achieve decarbonization goals.

Despite its strong growth outlook, the market faces challenges related to stringent environmental and occupational safety regulations due to the hazardous and carcinogenic nature of ethylene oxide. Manufacturers are therefore focusing on enhancing plant safety, reducing emissions, and adopting advanced monitoring systems while expanding production capacities to meet the growing demand from downstream industries. With increasing industrialization, rising demand for specialty chemicals, and continued expansion of packaging, automotive, and healthcare sectors, the global ethylene oxide market is expected to maintain stable growth over the coming years.

To know about the Research Methodology:-Request Free Sample Report

Global Ethylene Oxide Market Dynamics:

Rising demand for ethylene glycol from packaging and textile industries is driving the market

The increasing demand for ethylene glycol, the largest application of ethylene oxide, is a major factor driving market growth. Ethylene glycol is extensively used in the production of polyethylene terephthalate (PET) resins, polyester fibers, antifreeze, and industrial coolants. Rising consumption of PET bottles for food and beverage packaging, coupled with growing demand for polyester-based textiles, is significantly increasing the need for ethylene oxide. Additionally, rapid urbanization, industrialization, and expanding automotive production are supporting the demand for coolants and lightweight polyester materials, further strengthening the market. Increasing investments in downstream chemical manufacturing across emerging economies are also contributing to sustained market growth.

Growing demand for medical device sterilization and sustainable production technologies is creating market opportunities

The expansion of the healthcare industry is creating significant opportunities for the ethylene oxide market due to the increasing use of ethylene oxide for sterilizing heat- and moisture-sensitive medical devices, surgical instruments, and pharmaceutical packaging. Rising healthcare expenditure, aging populations, and growing demand for disposable medical products continue to support this application. Furthermore, manufacturers are investing in energy-efficient production technologies, advanced catalysts, carbon emission reduction initiatives, and bio-based feedstocks to improve sustainability and comply with evolving environmental regulations. These innovations are expected to unlock new growth opportunities while supporting the transition toward greener chemical manufacturing.

Stringent environmental regulations governing ethylene oxide handling are restraining market growth

Strict environmental and occupational safety regulations related to the production, transportation, storage, and use of ethylene oxide continue to restrain market expansion. Since ethylene oxide is classified as a hazardous and carcinogenic substance, manufacturers must comply with stringent emission standards, workplace exposure limits, and environmental monitoring requirements imposed by regulatory authorities. These compliance obligations increase operational costs, require continuous investments in safety infrastructure, and can delay capacity expansion projects, particularly in developed regions with rigorous environmental regulations.

Fluctuating ethylene feedstock prices and high production costs remain key market challenges

Volatility in ethylene prices, driven by fluctuations in crude oil and natural gas markets, geopolitical uncertainties, and supply chain disruptions, remains a major challenge for ethylene oxide manufacturers. Rising feedstock costs directly affect production expenses and profit margins, making long-term pricing strategies more difficult. In addition, ethylene oxide production requires significant capital investment in specialized processing equipment, emission control systems, and safety infrastructure to meet strict regulatory requirements. Balancing production efficiency, cost competitiveness, and sustainability objectives continues to be a critical challenge for industry participants.

Key Trends in the Global Ethylene Oxide Market

- Growing demand for bio-based and low-carbon ethylene oxide production: Manufacturers are increasingly investing in sustainable production technologies, renewable feedstocks, and energy-efficient manufacturing processes to reduce carbon emissions and comply with stringent environmental regulations. The transition toward low-carbon chemical production is becoming a key competitive strategy across the industry.

- Increasing consumption of ethylene oxide in medical device sterilization: The expanding healthcare sector and rising demand for single-use medical devices are driving the adoption of ethylene oxide sterilization. Hospitals, pharmaceutical companies, and medical device manufacturers continue to rely on ethylene oxide for sterilizing heat- and moisture-sensitive equipment, supporting steady market growth.

- Rising demand for PET packaging and polyester fibers: The growing use of polyethylene terephthalate (PET) bottles, food packaging materials, and polyester textiles is significantly increasing the demand for ethylene glycol, the largest derivative of ethylene oxide. Expanding e-commerce, packaged food consumption, and the global textile industry continue to strengthen this trend.

- Expansion of downstream specialty chemical production: Increasing investments in the production of ethoxylates, ethanolamines, glycol ethers, and polyethylene glycol (PEG) are driving ethylene oxide consumption across industries such as personal care, agrochemicals, detergents, paints and coatings, and pharmaceuticals. Manufacturers are expanding downstream integration to enhance value creation and improve supply chain efficiency.

Segment Analysis – Global Ethylene Oxide Market

By Derivatives,

The Ethylene Glycol segment dominated the global ethylene oxide market in 2025, accounting for the largest market share due to its extensive use in the production of polyester fibers, polyethylene terephthalate (PET) resins, antifreeze formulations, and industrial coolants. The growing demand for PET packaging in the food and beverage industry, coupled with increasing consumption of polyester textiles and rising automotive production, continues to drive the demand for ethylene glycol. Additionally, expanding infrastructure development and industrial manufacturing activities across emerging economies are further supporting segment growth.

The Ethoxylates segment is expected to witness significant growth during the forecast period owing to their increasing use in household detergents, industrial cleaners, personal care products, agrochemicals, and oilfield chemicals. Ethanolamines are also experiencing steady demand due to their applications in gas treatment, cement production, surfactants, and personal care formulations. Meanwhile, Glycol Ethers continue to gain traction in paints, coatings, inks, and cleaning products because of their excellent solvent properties. The Polyethylene Glycol (PEG) segment is expanding with rising demand from pharmaceutical, cosmetic, and biomedical applications, while the Others segment continues to support market growth through niche specialty chemical applications.

By Application,

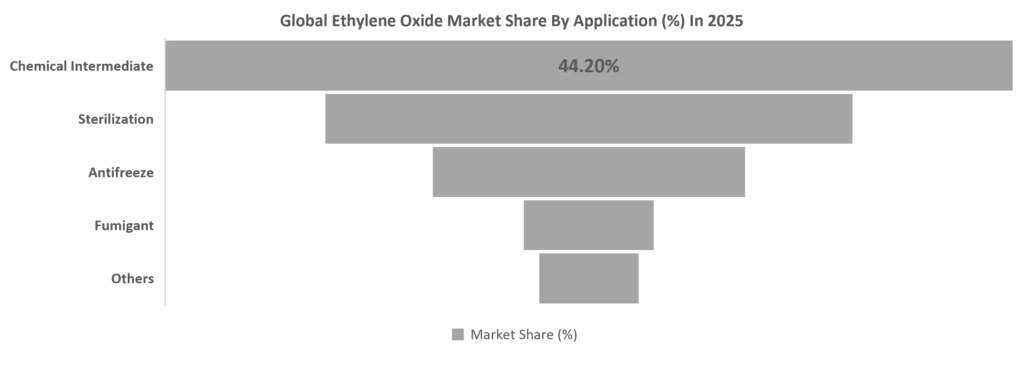

The Chemical Intermediate segment held the largest share of the global ethylene oxide market in 2025, driven by the extensive use of ethylene oxide as a key intermediate in the production of ethylene glycol, ethanolamines, ethoxylates, glycol ethers, and polyethylene glycol. The increasing demand for these downstream chemicals across the packaging, automotive, textile, construction, and consumer goods industries continues to fuel segment growth. Growing investments in chemical manufacturing facilities and expanding industrial production are further strengthening demand for ethylene oxide as an essential feedstock.

The Sterilization segment is projected to register substantial growth during the forecast period due to the increasing use of ethylene oxide for sterilizing heat- and moisture-sensitive medical devices, surgical instruments, and pharmaceutical packaging. Rising healthcare expenditure, expanding hospital infrastructure, and growing demand for single-use medical devices are supporting this segment's expansion. The Antifreeze segment continues to witness stable growth with increasing automotive production and industrial cooling applications. The Fumigant segment maintains moderate demand for specialized agricultural and industrial sterilization applications, while the Others segment, including specialty chemical synthesis and research applications, contributes steadily to the overall market growth.

| Company | Key Strategies |

| Dow Inc. | Expansion of integrated ethylene oxide and ethylene glycol production, operational efficiency improvements, and sustainability initiatives. |

| BASF SE | Capacity expansion, investment in low-carbon chemical manufacturing, and development of high-performance ethylene oxide derivatives. |

| Shell plc | Integrated petrochemical production, process optimization, and strategic investments in downstream ethylene oxide applications. |

| SABIC | Expansion of petrochemical manufacturing capacity, advanced production technologies, and focus on sustainable chemical solutions. |

| LyondellBasell Industries N.V. | Technology innovation, operational excellence, and expansion of ethylene oxide derivative production. |

| INEOS Group | Production capacity optimization, strategic investments in petrochemical infrastructure, and supply chain integration. |

| Nippon Shokubai Co., Ltd. | Specialty ethylene oxide derivatives, advanced catalyst technologies, and expansion in Asian markets. |

| Reliance Industries Limited | Integrated petrochemical operations, downstream chemical expansion, and capacity enhancement in India. |

| Huntsman Corporation | Development of specialty ethylene oxide derivatives, sustainable manufacturing, and product portfolio diversification. |

| India Glycols Limited | Bio-based chemical production, expansion of ethylene oxide derivative portfolio, and focus on specialty chemicals. |

Recent Developments – Global Ethylene Oxide Market

- December 2025: BASF SE continued the ramp-up of its integrated Zhanjiang Verbund project in China, strengthening regional production capabilities for petrochemicals, including downstream ethylene oxide value chains.

- August 2025: Prismane Consulting highlighted ongoing investments by major producers, including Dow, BASF, Shell, SABIC, INEOS, and Reliance Industries, in expanding ethylene oxide capacity and downstream derivative production to meet rising global demand.

- March 2025: Industry reports indicated that manufacturers increased investments in low-carbon and energy-efficient ethylene oxide production technologies to improve operational efficiency and comply with stricter environmental regulations.

- 2025: Nippon Shokubai Co., Ltd. continued expanding its portfolio of high-value ethylene oxide derivatives for pharmaceutical, personal care, and industrial applications, strengthening its position in specialty chemicals.

- 2025: Major global producers accelerated investments in advanced process safety systems, digital plant monitoring, and emission reduction technologies to improve manufacturing reliability and support sustainable ethylene oxide production.

Ethylene Oxide Market Scope: Inquire before buying

| Ethylene Oxide Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 62.95 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.59% | Market Size in 2032: | 86.19 USD Billion |

| Segments Covered: | By Derivatives | Ethylene Glycol Ethanolamine Ethoxylates Glycol Ethers Polyethylene Glycol (PEG) Others |

|

| By Applications | Antifreeze Sterilization Chemical Intermediate Fumigant Others |

||

| By End User | Automotive Agriculture Food & Beverages Personal Care Pharmaceuticals Textile Detergents Others |

||

Ethylene Oxide Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Ethylene Oxide Market, Key Players

1. Clariant AG

2. Dow Inc.

3. BASF SE

4. Shell plc

5. Sinopec

6. INEOS Group

7. LyondellBasell

8. Reliance Industries

9. Nouryon

10. Nippon Shokubai

11. Mitsubishi Chemical

12. ExxonMobil

13. Indorama Ventures Public Company Limited

14. LOTTE Chemical Corporation

15. India Glycols Limited

16. PTT Global Chemical Public Company Limited

17. SABIC

18. Formosa Plastics

Frequently Asked Questions:

1. Which region has the largest share in Global Ethylene Oxide Market?

Ans: Asia-Pacific region held the highest share in 2025.

2. What was the Global Ethylene Oxide Market size in 2025?

Ans: The Global Ethylene Oxide Market size was USD 62.95 Billion in 2025.

3. Who are the key players in Global market?

Ans: The important key players in the Global Market are – SABIC, India Glycols Limited, DowDuPont Inc., Indorama, Ventures Public Company Limited, BASF SE, Formosa Plastics Corporation, Indian Oil Corporation Ltd., Royal Dutch, Shell Plc., Huntsman International LLC., LOTTE Chemical CORPORATION, Akzo Nobel N.V., Chemicals Incorporated, Clariant Corporation, Environmental Tectonics Corp., Restek Corporation, The Dow Chemical Company, Advanced Air Technologies, and Inc.

4. What is the study period of this market?

Ans: The Global Market is studied from 2020 to 2032.