Elevators Market Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

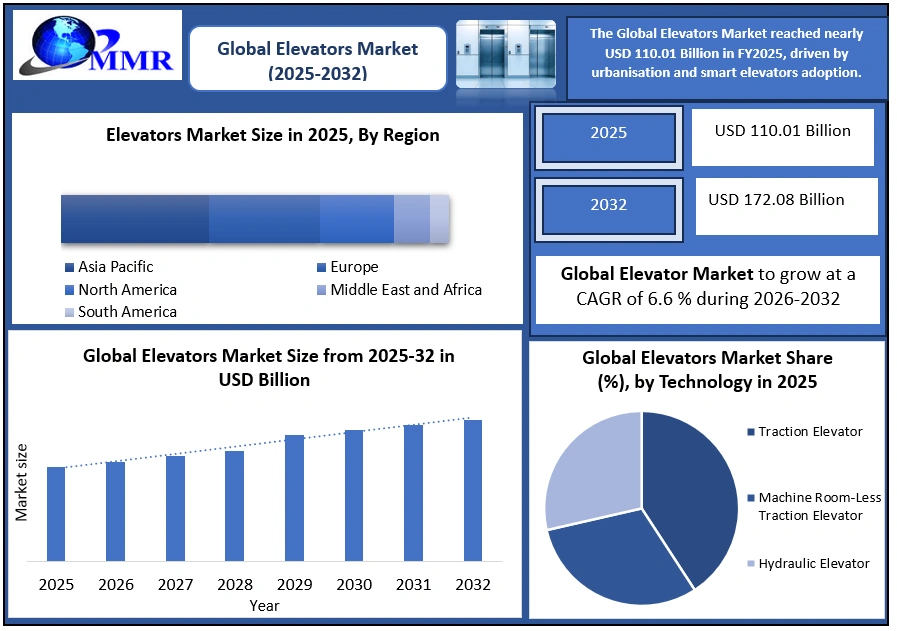

Elevators Market was valued at USD 110.01 Bn. in 2025 and is expected to reach USD 172.08 Bn. by 2032, at a CAGR of 6.6 % during the forecast period mainly due to growing service market, improving economic indicators, rapid urbanization and boom in high rise construction projects.

Global Elevators Market Overview

Elevators form a critical component of modern urban infrastructure, enabling vertical mobility across residential buildings, commercial complexes, hospitals, airports, metros, and mixed-use developments. Rapid urban density, limited horizontal expansion in cities, and rising building heights are structurally increasing reliance on Elevators systems worldwide.

A key trend in the Elevators industry analysis is the growing importance of the Elevators installation and maintenance market. The Elevators maintenance services segment was valued at approximately USD xx Billion in 2025 and is projected to grow at a CAGR of 6.6%, faster than new installations. Despite starting from a lower base, Modernization segment will develop the fastest. For global OEMs such as Otis, KONE, Schindler, and TK Elevators, services account for 40–60% of total revenues, driven by long-term contracts, digital monitoring, and predictive maintenance solutions.

Technological advancement is reshaping the market, with rising adoption of smart Elevators and IoT integration, destination control systems, Intelligent Elevators Dispatch, AI-based traffic optimisation, AI-Powered Predictive Elevators Maintenance and energy-efficient drives aligned with green building standards.

To know about the Research Methodology :- Request Free Sample Report

Key Highlights (2025)

• Elevators Market Growth: The global Elevators market forecast indicates sustained expansion supported by urbanisation, infrastructure spending, and aging installed base

• Service-Led Revenue Model: Maintenance and modernisation contributed 40–60% of OEM revenues, providing recurring cash flows.

• Passenger Elevators Market Dominance: Passenger Elevatorss accounted 65.8% of global revenue, reflecting residential and commercial building demand.

• Traction Elevators Market Leadership: Traction technology held xx % market share due to energy efficiency and suitability for mid- and high-rise buildings.

• Labour Constraints: Technician shortages are estimated to reduce potential growth by 2.5% in emerging markets.

Global Elevators Market Segment Analysis:

By Product Type Analysis

The Product Type segmentation of the Global Elevators Market is primarily driven by building usage intensity, passenger flow requirements, and vertical transport efficiency. Among all product categories, Passenger Elevatorss dominated the global Elevators market, accounting for approximately xx % of total market revenue in 2025.

Globally, over 1.1 million Elevators units are installed annually, of which more than 70% are passenger Elevatorss. Asia-Pacific leads passenger Elevators installations with over 66% volume share, driven by China followed by India with a double-digit CAGR of xx%. In mature markets such as Europe and North America, passenger Elevators demand is increasingly replacement-driven, as over 50.2% of installed Elevators exceed 15-18 years of operational life.

Freight Elevatorss accounted for xx% of global revenue, supported by industrial manufacturing facilities, logistics warehouses, hospitals, and large retail infrastructure. Dumbwaiters and other specialized Elevators systems collectively represent 10–14% of the market, with steady demand from hotels, healthcare facilities, and food service environments.

By Technology Analysis

The Technology segmentation highlights a decisive shift toward energy-efficient, high-performance systems. The Traction Elevators Market dominates the global landscape, accounting for approximately 71–72% of total installations. Traction Elevatorss are preferred for mid-rise to high-rise buildings due to their 35–40% lower energy consumption compared to hydraulic systems and superior speed capabilities.

Hydraulic Elevators, though declining in relative share, still account for 22–23% of global installations, especially in low-rise residential and institutional buildings across North America and parts of Europe. However, regulatory pressure on energy efficiency and space optimization continues to shift demand toward traction systems. As a result, traction technology remains central to Elevators market growth, smart Elevatorss and IoT integration, and long-term global Elevators market forecast.

Global Elevators Market – Regional Analysis

The Asia-Pacific region led the global Elevators market in 2025 driven by rapid urbanisation and high-rise construction. China dominated with over 650,000 new installations annually, contributing 70% of APAC demand, while India is the fastest-growing market with a CAGR of xx %, supported by metro rail and smart city projects. Europe held xx % share in 2025, characterised by a mature installed base of over x.8 million Elevators, nearly xx.5 % of which are over 20 years old, driving modernization demand. North America accounted for xx % in 2025, supported by smart buildings & maintenance in light of the developed installed base in the region, while Middle East & Africa benefits from mega-projects.

Pricing, Trade, and Market Structure

Elevators pricing varies significantly by technology, capacity, speed, and regional cost structures. In emerging markets, standard residential Elevators systems are typically priced between USD 7500 and USD 17,500 per unit, while premium and customised Elevatorss range from USD 18,000 to USD 35,000. In commercial and high-rise applications, machine-room-less (MRL) Elevatorss for mid-rise buildings are generally priced between USD xx and USD xx per unit, while high-speed Elevators for skyscrapers frequently exceed USD 450,000 per unit.

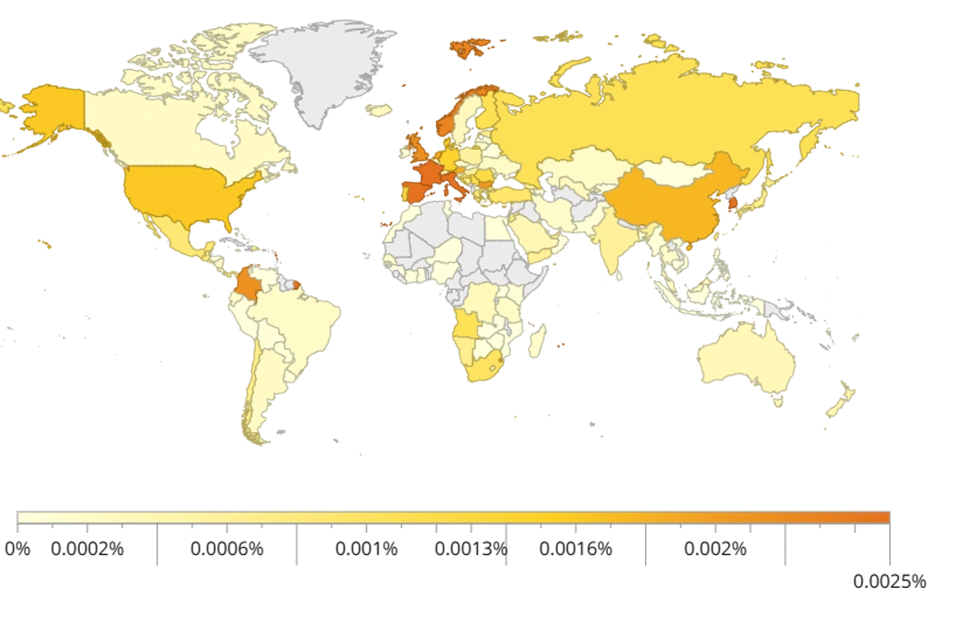

From a global trade standpoint, Elevators import export analysis highlights China as the largest exporter, with annual exports exceeding USD xx Billion, followed by Spain (USD xx Million) and Italy (USD xx Million). On the import side, the United States, United Kingdom, and Germany each import approximately USD xx Million worth of Elevators systems annually, reflecting strong demand for advanced and high-specification equipment.

Liquid Elevators Exports divided by a Country's Total Exports (2025)

Recent Developments

Otis World

• In 2024, Otis projected annual net sales of USD xx billion, with the service segment up 3.5% year-over-year and new equipment sales declining in some regions due to construction slowdowns in North America and China.

• In late 2025, Otis reported 25.5% growth in modernization orders and an xx % rise in service net sales, demonstrating resilience in aftermarket demand.

• Innovation Highlights — Introduction of Gen3 Comfort, Skyrise Mod, and Link Mod, along with an upgraded smart cab, the Otis AI inspection robot, and the Otis AI agent. Subscription revenue from connected units rose by 35% in 2025, while Otis One connected units reached nearly 1.1 million worldwide.

Schindler Group

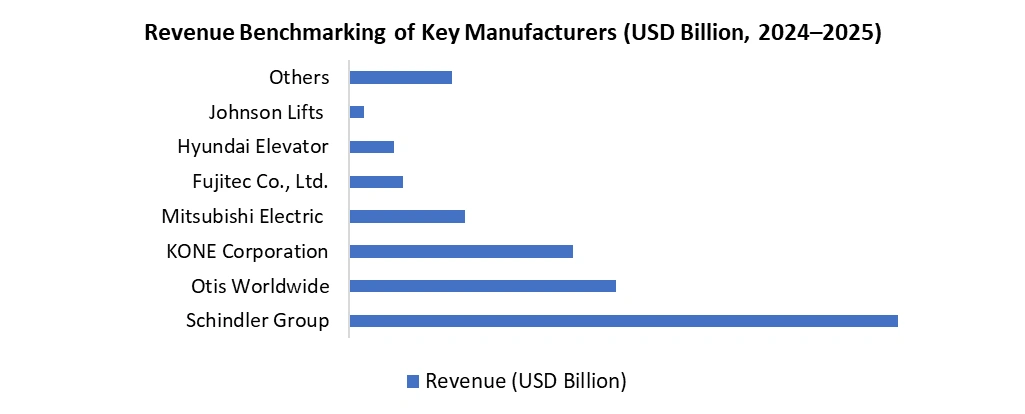

• In 2024, Schindler generated USD 12.2 billion in revenue, with margins improving through pricing and digital initiatives.

• In 2025, Schindler raised its operating profit margin forecast to 11.5%, even as new orders in China and other regions softened.

• In 2025, Schindler launched the Schindler X8, an Elevators solution designed to overcome longstanding architectural and into the Swiss and Italian markets.

Competitive Landscape:

The global Elevators market is largely dominated by six major multinational companies — Otis, Kone, Schindler, TKE, and Mitsubishi.

Elevators Market Scope: Inquiry Before Buying

| Global Elevators Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 110.01 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.6% | Market Size in 2032: | USD 172.08 Bn. |

| Segments Covered: | by Product Type | Passenger Elevatorss Freight Elevatorss Dumbwaiter Others |

|

| by Technology | Traction Elevators Machine Room-Less Traction Elevators Hydraulic Elevators |

||

| by Machine Type | Geared Machine Gearless Machine |

||

| by Deck Type | Single deck Double deck |

||

| by Door Type | Automatic Manual / Swing Doors |

||

| by Destination Control | Conventional Smart |

||

| by Business Type | New Equipment Maintenance & Repair Modernization |

||

| by Speed | Up to 1.0 m/s 1.1 – 2.5 m/s 2.6 – 4.0 m/s Above 4.0 m/s |

||

| by Capacity | 450 – 1150 kg 1151 – 1500 kg 1501 – 2000 kg 2001 – 3000 kg Above 3000 kg |

||

| by End User | Residential Commercial Industrial Others |

||

Elevators Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Global Elevators Market, Key Players

1. Kone Corporation

2. Johnson Lifts Private Limited

3. Schindler.

4. Otis World

5. Tk Elevators

6. Mitsubishi Electric

7. Fujitec Co., Ltd.

8. Hitachi Elevators.

9. Blue Star Elevatorss Ltd.

10. Beacon Elevators Co. Pvt. Ltd.

11. City Lift India Ltd.

12. Avt Beckett

13. Escon Elevatorss Pvt. Ltd.

14. Orona Group

15. Delfar Elevators

16. Sepl India Ltd.

17. Toshiba Corporation

18. Ningbo Hosting Elevators Co., Ltd. .

19. Stannah

20. Dazen

21. Hyundai Elevators Co., Ltd.

22. Kleemann

23. Canny Elevators Co., Ltd.

24. Others

Frequently asked Questions:

1. What are elevators?

Ans: Elevators, also known as lifts in some regions, are vertical transportation devices used to move people or goods between different floors or levels within a building or structure. They consist of a car (or platform) that travels along vertical rails or shafts, usually enclosed within a shaft or hoistway.

2. How is the elevator industry evolving?

Ans: The elevator industry is transforming with the integration of advanced technologies such as IoT (Internet of Things), AI (Artificial Intelligence), and smart sensors. These innovations aim to improve efficiency, safety, and user experience, leading to enhanced elevator systems and services.

3. What are the key drivers of the elevators market?

Ans: High-rise construction, technological advancements, energy efficiency, safety regulations, urban mobility solutions, and market expansion in emerging economies are among the key drivers of the elevators market. These factors contribute to the growing demand for elevators in various residential, commercial, and industrial sectors worldwide.

4. What are the challenges faced by the elevators market?

Ans: High initial costs, long development cycles, technical challenges, economic uncertainty, and regulatory compliance are some of the challenges faced by the elevators market. These factors impact the growth and profitability of elevator manufacturers and developers, requiring them to navigate complex market dynamics effectively.

5. How is the elevators market segmented?

Ans: The elevators market is segmented based on type (residential, freight, passenger), deck type (single deck, double deck), and geography (region-wise). Each segment represents distinct market opportunities and dynamics within the elevator industry, catering to different customer needs and preferences across various applications and regions.