COVID-19 Diagnostics Market Size by Test Type, Product Type, Technology, Sample Type and Distribution Channel

Overview

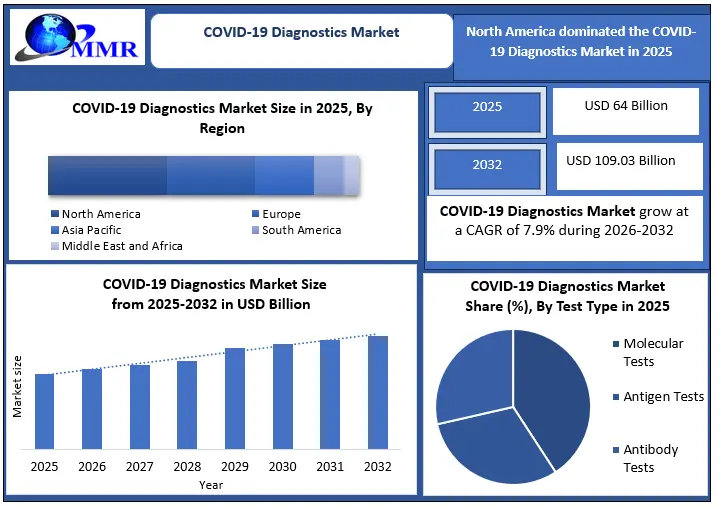

Global COVID-19 Diagnostics Market Size Was USD 64 Billion in 2025 and is Expected to Reach USD 109.03 Billion by 2032, Growing at a CAGR of 7.9% During 2026–2032. Even as COVID-19 transitions from a global emergency to an endemic public health challenge, diagnostics continue to remain at the center of healthcare preparedness strategies worldwide. Hospitals, airports, diagnostic laboratories, and government surveillance agencies are increasingly shifting from emergency-driven mass testing toward targeted respiratory screening, variant monitoring, and multiplex infectious disease diagnostics. Against this backdrop, the Global COVID-19 Diagnostics Market was valued at USD 64 billion in 2025 and is projected to reach USD 109.03 billion by 2032, expanding at a CAGR of 7.9% during the forecast period from 2026 to 2032.

COVID-19 Diagnostics Market Overview

The COVID-19 Diagnostics remained relevant beyond the pandemic peak as testing shifted from mass screening to targeted confirmatory testing, multiplex respiratory panel integration, and surveillance-led preparedness programs. PCR/NAAT diagnostics continued to dominate the COVID-19 Diagnostics Market as the clinical gold standard due to high sensitivity and regulatory preference, while rapid antigen tests supported decentralized, point-of-care, and at-home COVID-19 testing. However, performance gaps persisted, with antigen tests showing 47% sensitivity compared to RT-PCR and ~80% sensitivity versus viral culture, capturing many infectious cases but missing low viral-load infections.

Technological innovation sustained utilization across hospitals and diagnostic laboratories within the COVID-19 Diagnostics Market through multiplex molecular diagnostics. In June 2024, Roche’s cobas liat SARS-CoV-2, Influenza A/B & RSV received FDA Emergency Use Authorization (EUA), enabling automated, high-throughput multiplex RT-PCR testing in acute-care settings. Similarly, Thermo Fisher Scientific’s TaqPath COVID-19, Flu A, Flu B, RSV Select Panel received FDA 510(k) clearance, reinforcing the shift toward single-test, multi-pathogen respiratory diagnostics. These advancements improved laboratory efficiency, turnaround time, and clinical differentiation, supporting the long-term demand outlook for the global COVID-19 Diagnostics Market.

To know about the Research Methodology :- Request Free Sample Report

Global COVID-19 Diagnostics Market Key Highlights

COVID-19 Diagnostics Market Growth Analysis: COVID-19 Diagnostics Industry growth is driven by continued demand for PCR-based confirmatory testing, rapid antigen tests, and integrated respiratory panels, alongside investments in diagnostic preparedness and surveillance systems.

• >85% of hospitals continue to use PCR as the primary confirmatory test for symptomatic patients.

• PCR sensitivity ranges between 95–99%, compared to 70–85% for antigen tests.

• Multi-target PCR assays detect >99% of known variants, ensuring long-term relevance.

• High-throughput PCR systems process 1,000–4,000 samples/day per lab, supporting surveillance-scale testing.

• Shift Toward Point-of-Care & At-Home Testing: Decentralized testing solutions gained traction, improving accessibility, turnaround times, and compliance across healthcare and community settings.

• Molecular Diagnostics Dominance: PCR and other nucleic acid amplification tests remained the gold standard, accounting for the largest share due to high sensitivity and accuracy.

• Public Health Surveillance Expansion: Governments increasingly relied on diagnostics for variant tracking, population screening, and outbreak management, sustaining long-term demand.

Industry Adoption in COVID-19 Diagnostics Market

Healthcare & Hospitals

The 85% of hospitals globally continued to rely on molecular and antigen-based COVID-19 diagnostics in 2025 for patient triage, infection control, and clinical confirmation. Diagnostic laboratories expanded automated PCR platforms to support high-throughput testing and respiratory panel integration.

Public Health & Government Agencies

Governments accounted for a significant share of diagnostic demand through mass testing programs, surveillance initiatives, and emergency response frameworks. National public health laboratories utilized diagnostics for variant monitoring and epidemiological studies.

Global COVID-19 Diagnostics Market Technological Innovation:

The transition from emergency approvals toward standardized FDA 510(k), CE-IVDR, and WHO Emergency Use Listing pathways is accelerating commercialization of multiplex respiratory diagnostic platforms, encouraging manufacturers to diversify beyond single-pathogen COVID-19 testing into broader infectious disease surveillance solutions.

Advancements in multiplex PCR, automation, digital diagnostics, and AI-assisted analysis improved testing throughput and efficiency. Advancements in multiplex PCR enabled simultaneous detection of up to six respiratory pathogens, increasing laboratory throughput by 30–50%. Automated PCR platforms now process up to 4,000 samples per day while reducing manual errors by nearly 80%. Digital diagnostics and AI-assisted analysis have further improved result turnaround times by 20–50% and enhanced surveillance responsiveness, significantly increasing testing efficiency and scalability.

Global COVID-19 Diagnostics Market Restraints

Despite sustained surveillance demand, the market continues to face structural normalization pressure as routine mass-testing volumes decline across mature healthcare systems. This transition is creating pricing pressure for diagnostic manufacturers, particularly those heavily dependent on high-volume antigen testing revenues generated during the pandemic peak years.

Declining Routine COVID-19 Diagnostics Testing Volumes

As vaccination coverage increased and infection severity declined, routine mass testing volumes reduced, impacting short-term demand in certain regions.

| Component / Cost | Cost Range (USD) |

| RT-PCR Test Kits (per test) | 15 – 50 |

| Rapid Antigen Test Kits (per test) | 3 – 15 |

| Molecular Diagnostic Instruments | 15,000 – 150,000+ |

| Sample Collection & Consumables | 2 – 10 |

| Laboratory Automation & Integration | 20,000 – 200,000+ |

High Cost of Molecular Diagnostics

Advanced PCR platforms, reagents, and automation systems involve high operational and infrastructure costs, particularly for low- and middle-income regions.

Supply Chain & Workforce Constraints

Shortages of reagents, consumables, and skilled laboratory personnel posed challenges during demand surges, highlighting vulnerabilities in diagnostic supply chains.

Table: Test Variation Parameters

| Parameter | Molecular Tests (PCR / NAAT) | Antigen Tests | Antibody (Serology) Tests |

| What the test detects | Viral genetic material (RNA) | Viral surface proteins (antigens) | Antibodies produced by immune response |

| Primary purpose | Confirm current COVID-19 infection | Rapid detection of active infection | Identify past infection or exposure |

| Sample type | Nasal swab, throat swab, saliva | Nasal or throat swab | Blood sample |

| Result type | Positive / Negative | Positive / Negative | Antibodies Present / Absent |

| Turnaround time | 20 minutes to several days (lab PCR); 13–120 minutes (rapid molecular) | 10–30 minutes | Same day to 1–3 days |

| Testing location | Certified labs, hospitals, point-of-care sites | Clinics, pharmacies, home settings | Clinical laboratories |

| Accuracy | Very high (gold standard) | Moderate; lower than molecular tests | Depends on timing after infection |

| False negatives | Rare; more likely later in illness | More common, especially in asymptomatic cases | Likely if tested too early |

| False positives | Very rare | Uncommon | Possible due to cross-reactivity |

| Use in early infection | Highly effective | Effective in first 5 days of symptoms | Not suitable |

| Use in asymptomatic screening | Effective | Not currently recommended | Not applicable |

| Key advantages | Highest sensitivity; reliable diagnosis | Fast, inexpensive, easy to use | Useful for surveillance & immunity studies |

| Key limitations | Requires lab infrastructure; longer turnaround | Lower sensitivity; confirmation often required | Cannot detect active infection |

COVID-19 Diagnostics Market Segment Analysis

Molecular diagnostics dominated the market in 2025 due to superior analytical sensitivity, regulatory preference for confirmatory diagnosis, and growing integration of multiplex PCR panels capable of detecting multiple respiratory pathogens simultaneously. Meanwhile, antigen testing emerged as the fastest-growing segment owing to affordability, rapid turnaround time, ease of decentralized deployment, and rising adoption of at-home self-testing kits across retail and pharmacy channels.

By Test Type

• Molecular Diagnostics (PCR): Held the largest COVID-19 Diagnostics Market share in 2025 due to accuracy, confirmatory testing requirements, and regulatory preference.

• Antigen Tests: Fastest-growing segment driven by rapid results, affordability, and point-of-care adoption.

• Antibody Tests: Used primarily for seroprevalence studies and research rather than active infection diagnosis.

By End User

• Hospitals & Diagnostic Laboratories: Largest share due to high testing volumes and confirmatory testing needs.

• Home Care & Point-of-Care Settings: Fastest-growing segment driven by self-testing kits and decentralized diagnostics.

COVID-19 Diagnostics Market Regional Analysis

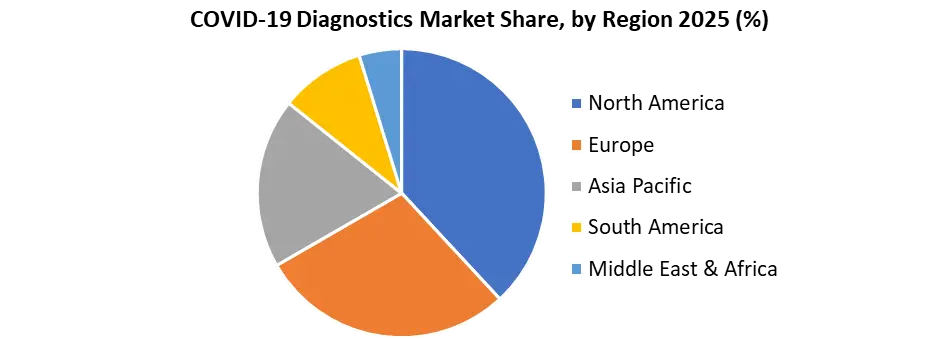

North America dominated the COVID-19 Diagnostics Market in 2025 due to strong reimbursement frameworks, advanced molecular testing infrastructure, and sustained investments in pandemic preparedness programs across the United States and Canada. The region also benefits from the presence of major diagnostic manufacturers including Roche, Abbott, Thermo Fisher Scientific, and Danaher Corporation, strengthening domestic production capabilities and rapid commercialization of advanced respiratory testing platforms.

Asia-Pacific is projected to witness the fastest growth during the forecast period owing to expanding local manufacturing capacity in China and India, rising public health investments, growing adoption of decentralized diagnostics, and government-led infectious disease surveillance initiatives. Countries such as China, India, South Korea, and Japan are increasingly integrating multiplex respiratory diagnostics into long-term healthcare preparedness strategies.

Recent Developments

June 2024: Roche’s cobas Liat SARS-CoV-2, Influenza & RSV multiplex PCR received FDA EUA allowing simultaneous respiratory virus detection in ~20 min.

Sept 2024: Roche launched a broader respiratory panel (up to 12 viruses) leveraging advanced PCR technology, expanding diagnostics beyond COVID-19.

COVID-19 Diagnostics Market Scope: Inquire before buying

| COVID-19 Diagnostics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 64 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 7.9% | Market Size in 2032: | USD 109.03 Bn. |

| Segments Covered: | by Test Type | Molecular Tests Antigen Tests Antibody Tests |

|

| by Product Type | Instruments Reagents & Kits Consumables & Accessories |

||

| by Technology | Polymerase Chain Reaction (PCR) Next-Generation Sequencing (NGS) ELISA Lateral Flow Assays CRISPR-based Diagnostics Microarray Technology |

||

| by Sample Type | Nasopharyngeal Swabs Oropharyngeal Swabs Saliva Blood / Serum Others |

||

| by Testing Setting | Laboratory-Based Testing Point-of-Care (PoC) Testing At-Home / Self-Testing |

||

| by End User | Hospitals & Clinics Diagnostic Laboratories Academic & Research Institutes Home Care Settings Government & Public Health Laboratories |

||

| by Distribution Channel | Government Tenders / Public Procurement Retail Pharmacies Online Platforms Diagnostic Service Providers |

||

Global COVID-19 Diagnostics Market Key Players

1. Abbott Laboratories

2. F. Hoffmann-La Roche Ltd (Roche Diagnostics)

3. Thermo Fisher Scientific Inc.

4. Siemens Healthineers AG

5. Danaher Corporation (Cepheid)

6. Bio-Rad Laboratories, Inc.

7. BioMérieux SA

8. PerkinElmer Inc.

9. Hologic, Inc.

10. QIAGEN N.V.

11. Beckman Coulter, Inc.

12. Cardinal Health (Diagnostics Division)

13. Quest Diagnostics Incorporated

14. Seegene Inc.

15. Luminex Corporation

16. Altona Diagnostics GmbH

17. OraSure Technologies / Sherlock Biosciences

18. QuidelOrtho Corporation

19. Guangzhou Wondfo Biotech Co., Ltd.

20. Beijing Wantai Biological Pharmacy Enterprise Co., Ltd.

21. Hangzhou AllTest Biotech Co., Ltd.

22. ACON Laboratories (Flowflex Rapid Tests)

23. SureScreen Diagnostics (UK)

24. NG Biotech

25. Sugentech, Inc.

26. Cellex, Inc.

27. Newfoundland Diagnostics

28. Mylab Discovery Solutions Pvt. Ltd. (India)

29. Anhui DeepBlue Medical Technology Co., Ltd.

30. myLAB Box, Inc.

31. Others

Frequently Asked Questions

1. What is the size of the Global COVID-19 Diagnostics Market?

The market is projected to grow from USD 64.00 billion in 2025 to USD 109.03 billion by 2032, at a CAGR of 7.9%, driven by rising demand for advanced diagnostics.

2. What are the key applications of COVID-19 diagnostics in Global COVID-19 Diagnostics Market?

COVID-19 diagnostics are widely used for clinical infection confirmation, hospital admission screening, public health surveillance, travel testing, workplace screening, respiratory disease differentiation, and variant monitoring programs.

3. Which technologies are used in COVID-19 diagnostics in Global COVID-19 Diagnostics Market?

Major technologies used in COVID-19 diagnostics include RT-PCR, rapid antigen testing, antibody-based serology testing, CRISPR-based diagnostics, ELISA, multiplex molecular diagnostics, and next-generation sequencing (NGS) for variant detection.

4. What are the benefits of advanced COVID-19 diagnostic technologies in Global COVID-19 Diagnostics Market?

These technologies offer high sensitivity, faster turnaround times, multiplex testing, and support precision medicine approaches.

5. What factors are driving the Global COVID-19 Diagnostics Market growth?

Market growth is driven by technological advancements, regulatory support, increased testing demand, and the adoption of high-throughput diagnostic platforms.