Core Materials for Composites Market Size by Type, End Use Industry, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

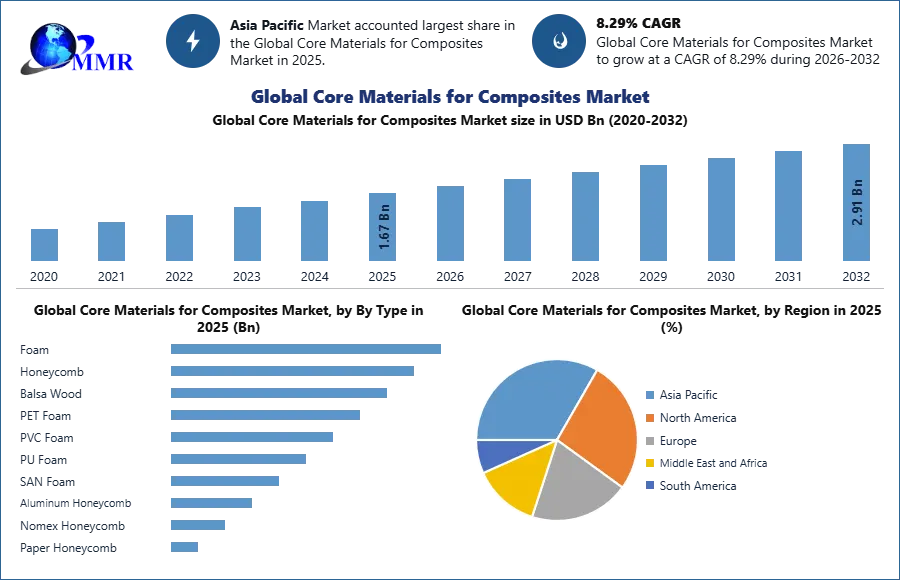

Global Core Materials for Composites Market was valued at USD 1.67 Bn in 2025 and is expected to reach USD 2.91 Bn by 2032, growing at a CAGR of 8.29% during the forecast period.

Core Materials for Composites Market Overview:

Core materials for composites are light-weight materials utilized in sandwich structures to offer strength and rigidity while reducing weight. These materials, like balsa wood, honeycomb, and PVC foam, play a key role in boosting the performance of composite products across many industries, including automotive, aerospace & defence, and construction.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Core Materials for Composites Market: Supply Side and Demand Side Research Approach

Supply Side Research Approach:

The supply side research approach includes data collection across region like North America, Europe, Asia Pacific, Middle East & Africa and South America for 15-20 Core Materials for Composites E-commerce website (5-10 websites per market) and consumer survey reports. It also includes data from department stores, and marketplace sites. The data has been also collected from Key industry players: major Core Materials for Composites key players and National / regional nutrition industry associations.

Demand Side Research Approach:

Demand Side Research Approach phase was included an in-depth survey of some questions related to consumer attitudes and behaviours on e-commerce sites. The some of the Survey questions covered major areas as Core Materials for Composites products shopping behaviours (e.g., categories, barriers, expectations, etc.) General shopping behaviours and retail website user experience and checkout preferences.

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 06 March 2026 | VisionWave Holdings / C.M. Composite Materials | C.M. Composite Materials executed a non-binding Memorandum of Understanding (MOU) with a major Indian industrial group to explore a joint venture for aerospace and defense composite manufacturing. | The proposed venture aims to establish a regional manufacturing hub for structural composite components, strengthening the supply chain for advanced industrial markets across India and Southeast Asia. |

| 23 January 2026 | Gurit Holding AG | Gurit announced the successful completion of its strategic transformation program, including a planned exit from the non-core carbon fiber pultrusion business to focus exclusively on high-performance core materials. | This realignment prioritizes OptiCore™ and Corecell™ technologies, enabling the company to secure major long-term supply agreements with leading Western wind turbine and subsea OEMs. |

| 09 January 2026 | Karman Space & Defense | Karman announced a $220 million definitive agreement to acquire Seemann Composites and Material Sciences, leaders in advanced resin infusion and composite core engineering. | The acquisition expands Karman’s production capacity for next-generation maritime propulsion and shielding systems, specifically targeting high-priority national security programs like Columbia and Virginia-class submarines. |

| 23 September 2025 | Hexcel Corporation | Hexcel and HyPerComp unveiled an advanced Type IV composite pressure vessel utilizing HexTow® IM11-R carbon fiber and structural core technologies. | This development provides a high-strength, lightweight hydrogen storage solution for next-generation marine and aerospace propulsion systems, accelerating the transition to zero-emission transportation. |

| 15 May 2025 | 3A Composites Core Materials | The company formally declared its BALTEK® SBC balsa wood product line as FSC™ MIX certified across all global markets. | By extending certification to end products, 3A Composites enables customers in the wind energy and marine sectors to meet increasingly strict ESG reporting and sustainable sourcing requirements. |

| 12 March 2025 | Toray Industries, Inc. | Toray announced a major expansion of its composite production capacity in Japan to produce specialized core-compatible carbon fiber prepregs. | The expansion is designed to meet the rising global demand for lightweight sandwich structures in commercial aerospace and EV battery enclosures. |

Core Materials for Composites Market Trends:

Leading trend in the Core Material for Composites market is the industry's growing focus on eco-friendliness and sustainability. There's a rising shift towards adopting and developing core materials that are environmentally recyclable, sustainable, and possess reduced carbon footprints. This trend aligns with worldwide efforts to reduce environmental impact within industries. Companies are exploring bio-based alternatives, natural fibres, recycled materials, and renewable resources for core materials, pointing to create composites with lower environmental impact through their lifecycle.

Global Core Material for Composites market is the rapidly pursuit of high-performance and lightweight core materials. Industries like automotive, aerospace, and wind energy demand core materials that provides exceptional stiffness, strength-to-weight ratios, and durability. Advances in material sciences and manufacturing technologies drive the development of advanced cores, like foam composites, honeycomb structures, and engineered textiles, aimed at reaching lighter weight and enhanced structural integrity. The aerospace industry drives the requirement for cutting-edge core materials that contribute to lighter aircraft components without flexible strength or safety standards. Furthermore, the automotive sectors seek lightweight core materials to enhance fuel efficiency and reduce emissions in automobiles.

Core Materials for Composites Market Dynamics:

The MMR report covers all the trends and technologies playing a major role in the growth of the Core Materials for Composites Market over the forecast period. It highlights the drivers, restraints, and opportunities expected to influence the Core Materials for Composites Market growth during 2025-2032.

Drivers in Core Materials for Composites Market:

The Core Materials for Composite Market is experiencing robust growth driven by various key factors. Rising investments in renewable energy projects, specifically in wind turbines and solar power infrastructure, are driving demand for composite materials that offers durability and strength to these structures. Lightweight materials are also acquiring prominence across industries like automotive, aerospace, and construction thanks to their ability to improve fuel efficiency, enhance performance, and reduce overall costs. As sustainability becomes an importance, the acceptance of lightweight composites is accelerating, mainly in the automotive industry, where they help meet stringent emission regulations, and in aerospace, where weight decrease translates to substantial fuel savings. Additionally, developments in manufacturing technologies, like automated fibre placement and infusion techniques, are aiding the production of complex designs with improved precision and efficiency. These drivers collectively underscore the Core Materials for Composite Market’s strong potential for growth and innovation.

Challenges Facing the Core Materials for Composite Market:

The Core Materials for Composites Market faces major challenges in achieving sustainability and cost-effectiveness without compromising performance. High performance core resources often acquire elevated production costs due to manufacturing processes, expensive raw materials and advanced technologies which pose affordability concerns, mainly in cost-sensitive industries such as automotive. Concurrently, addressing environmental concerns needs substantial investment in acquiring eco-friendly alternatives, for instance recyclable or bio-based materials, while continuing the required mechanical properties. The disposal and end-of-life management of composite materials advance complicate sustainability efforts, prominence the need for innovative solutions to decrease environmental impact and align with worldwide sustainability goals.

Core Materials for Composites Market Segmentation Insight:

In 2025, the Foam segment accounts for the highest demand in the core materials for composites market due to its lightweight structure, excellent mechanical properties, and superior fatigue resistance. Foam cores such as PVC, PET, and polyurethane are widely used in wind turbine blades, marine vessels, and aerospace components because they enhance structural strength while reducing overall weight. Honeycomb materials are also widely utilized, particularly in aerospace and defense applications, due to their high strength-to-weight ratio and excellent stiffness. Meanwhile, Balsa wood cores continue to be preferred in marine and wind energy applications because of their natural strength, sustainability, and cost-effectiveness, though their demand is more niche compared with foam materials.

Based on End-Use Industry, Wind Energy represents the most significant demand segment in 2025. The rapid expansion of renewable energy projects and increasing installation of large-scale wind turbines have significantly increased the need for lightweight and durable composite core materials used in turbine blades. Aerospace and Defense also remains a major segment, as manufacturers increasingly use composite materials to reduce aircraft weight and improve fuel efficiency. The Marine sector continues to adopt composite cores for hulls and deck structures due to their corrosion resistance and structural performance. Additionally, industries such as Construction, Automotive, and Consumer Goods are gradually increasing their use of composite core materials for lightweight structural components and improved durability.

Aerospace Industry Growth Fuels Demand in the Core Materials for Composites Market

Global Core Materials for Composites Market is experiencing growth along the aerospace sector owing to the unique properties of these materials, like radar transparency, high strength, exceptional flexibility, and low thermal conductivity. These characteristics make them indispensable in the production of flight vehicles, UAVs (unmanned aerial vehicles), and airships. Moreover, the core materials for composites market's growth is driven by the use of diverse materials to construct the demanded sandwich structures while incorporating further functional features.

| Global Core Materials for Composites Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 1.67 USD Bn |

| Forecast Period 2026-2032 CAGR: | 8.29% | Market Size in 2032: | 2.91 USD Bn |

| Segments Covered: | By Type | Foam Honeycomb Balsa Wood PET Foam PVC Foam PU Foam SAN Foam Aluminum Honeycomb Nomex Honeycomb Paper Honeycomb Others |

|

| By End-Use Industry | Aerospace and Defense Marine Construction Wind Energy Automotive Consumer Goods Transportation Sports and Leisure Industrial Others |

||

| By Application | Sandwich Panels Structural Components Interior Panels Blades and Turbines Decks and Hulls Aircraft Structures Automotive Components |

||

Core Materials for Composites Market Regional Insight:

Globally, North America region held the dominant position in the core materials for composites market. North America has a largest share of the core materials for composites at a share of more than 35.34%, Followed by Europe and Asia Pacific. This is growth is attributed to strong demand in aerospace and automotive sectors in the USA.

The United States core materials for composites market is sustained by its robust automotive, aerospace, construction and marine industries. The country's aerospace Industry, the largest worldwide, is experiencing growth in its commercial aircraft fleet, fuelled by growing air cargo demand and fleet modernization. The automotive sector is also growing, supported by investments from major companies. Furthermore, the construction industry benefits from increasing home sales and office space development, further fuelling demand for core materials. The wind energy industry, with substantial contributions from prominent manufacturers such as Vestas, GE Renewable Energy, and Siemens, also plays a key role in this core materials for composites market's growth.

Asia Pacific is expected to hold the largest market share during the forecast period thanks to growing demand from end-use. Increased demand for automobiles because of increasing disposable income and an expanding population is the cause of the growth. Additionally, the region's rising industrialization and government shots to improve the infrastructure are predicted to fuel product use across a range of applications.

Core Materials for Composites Market Industry Development:

The Core Materials for Composites market is witnessing significant industry developments driven by technological advancements and growing applications across various sectors.

• The Core Material for Composites market expected witnessed continued increases in sustainable core materials. R&D efforts in this period may have focused on initiating eco-friendly alternatives, with bio-based, recycled, or renewable core equipment. Such as, In Dec 2022, 3A Composites Core Materials, a worldwide leader in development and manufacturing high-performance core materials for composite applications, initiated a new product line, Engicore core materials.

• In the Core Material for Composites market likely cantered on advances in lightweight core structures. Engineers and material scientists are constantly studying new designs and materials to achieve lighter, stronger, and more efficient core structures.

Core Materials for Composites Suppliers and Market Shares:

In this globally competitive Market, several key players such as, Solvay S.A., BASF SE, SABIC, Hexcel Corporation, etc. dominate the market and contribute to industry’s growth and innovation. These players capture highest Core Materials for Composites Market share.

Companies in the Core Materials for Composites Market compete based on product quality offered. Major players in Core Materials for Composites Market focus on developing their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. With these strategies core material companies cater increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the core material companies profiled in this report includes.

• Hexcel Corporation

• Owens Corning

• Huntsman Corporation

• DuPont de Nemours, Inc.

• 3M Company

• Albaugh LLC

Above Key players have established themselves as leaders in the Market with extensive product portfolios, global presence, and strong R&D capabilities. They repeatedly strive to enhance Market positions through strategic partnerships, mergers and acquisitions, and product innovations.

Market share dynamics within the global market are evolving, with the entry of new players and the emergence of advanced technologies. Furthermore, collaborations between material manufacturers, suppliers, and end-users are adopting technological advancements and growing Market opportunities.

Core Materials for Composites Market Scope:Inquire Before Buying

Core Materials for Composites Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, and Rest of APAC)

Middle East and Africa (South Africa, GCC, and Rest of the MEA)

South America (Brazil, Argentina, and Rest of South America)

Key Players /Competitor Profiles Covered in the Global Core Materials for Composites Market Report from a Strategic Perspective.

- Hexcel Corporation

- Owens Corning

- Gurit Holding AG

- DIAB Group

- 3A Composites

- Evonik Industries AG

- Armacell International

- Saudi Basic Industries Corporation

- BASF SE

- Toray Industries

- Teijin Limited

- Mitsubishi Chemical Group

- Solvay SA

- Huntsman Corporation

- 3M Company

- Plascore Inc

- Euro Composites SA

- The Gill Corporation

- CoreLite Inc

- ATC Manufacturing

- Carbon Core Corporation

- Changzhou Tiansheng New Materials

- General Plastics Manufacturing Company

- Polyumac Inc

- Schweiter Technologies