Global Chromatography Reagents Market Size, Share & Forecast (2026–2032) – Valued at USD 8.75 Billion in 2025, Projected to Reach USD 18.21 Billion by 2032 at a CAGR of 11.04%

Overview

Chromatography Reagents Market Overview

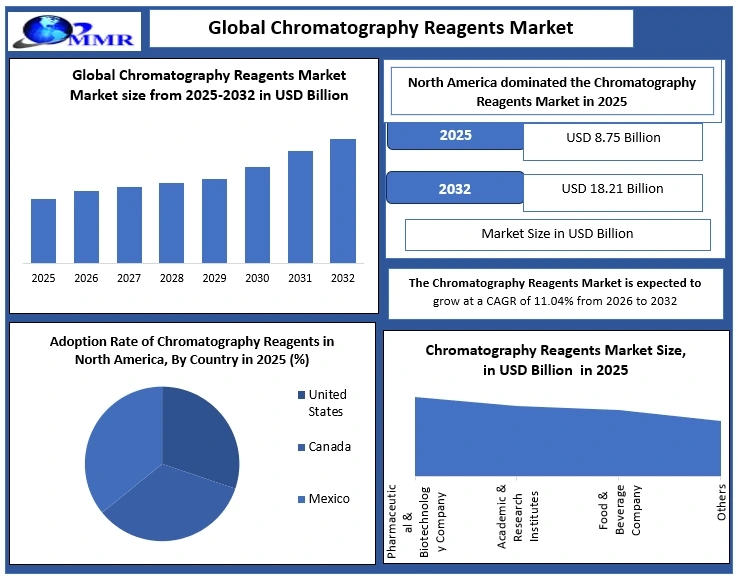

Before a single drug reaches a patient, it passes through chromatography dozens of times — purity confirmed, impurities profiled, stability validated. Chromatography reagents are the silent, unglamorous, and entirely non-negotiable foundation of modern pharmaceutical development, food safety testing, and environmental compliance. The Global Chromatography Reagents Market, valued at USD 8.75 billion in 2025, is projected to reach USD 18.21 billion by 2032 at a CAGR of 11.04% — a trajectory driven not by trend cycles, but by the structural expansion of pharmaceutical R&D pipelines, tightening regulatory purity standards, and the accelerating adoption of LC-MS and UHPLC techniques that demand ever-higher reagent specifications.

Key Highlights of Chromatography Reagents Market

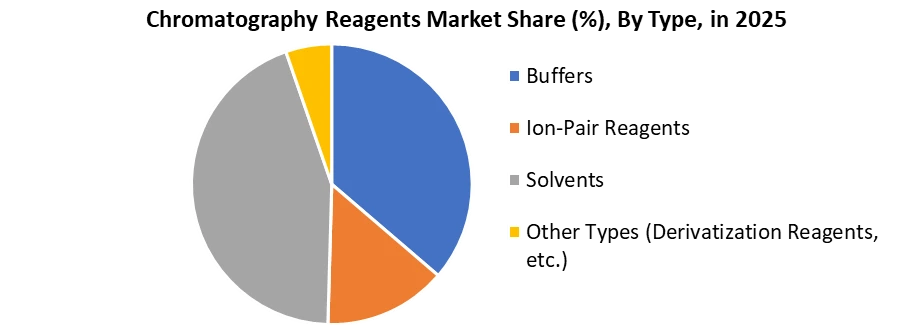

• The global chromatography reagents market reached USD 8.75 billion in 2025; solvents held the largest segment share, driven by their critical role as mobile phase components across HPLC, GC, and LC-MS workflows.

• Ion-pair reagents represent the fastest-growing segment in 2025, driven by expanding pharmaceutical chromatography and biochromatography applications requiring precision separation of ionic analytes.

• Over 70% of FDA-approved biologics have used HPLC-based methods for stability and purity characterisation — anchoring high-purity chromatography solvents as a non-discretionary procurement category for regulated pharma labs.

• Organised players — including Thermo Fischer Scientific, Merck KGaA, Agilent Technologies, and Waters Corporation — captured approximately 65% of global market share in 2025, with the balance held by regional and unorganised suppliers competing primarily on price in cost-sensitive segments.

• North America dominated the chromatography reagents market in 2025, supported by the world's largest pharmaceutical R&D investment base, high HPLC and LC-MS adoption rates, and a dense network of contract research and testing laboratories.

• Raw material price volatility — particularly for acetonitrile and speciality buffers — fluctuated 10–30% year-over-year, driving end-users toward long-term supply contracts and dual-sourcing strategies for critical reagents.

Why the Chromatography Reagents Market Is Entering Its Most Consequential Growth Phase

Chromatography reagents have always been essential. What has changed is the standard they must meet.

A decade ago, HPLC-grade purity was sufficient for the majority of pharmaceutical applications. Today, the migration to LC-MS/MS — where even trace-level ionic contamination can suppress signal and invalidate results — has raised reagent specification requirements to a level that eliminates entire tiers of the historical supply base. MS-grade solvents, ultra-low metal content buffers, and certified ion-pair reagents are no longer premium categories. They are becoming baseline requirements for regulated pharmaceutical and clinical laboratory work.

Simultaneously, the biologics and biosimilars revolution is driving demand for biochromatography reagents — buffers, resins, and speciality solvents for protein purification — that command significantly higher margins than traditional small-molecule HPLC solvents. And the green chemistry mandate is reshaping procurement, as regulatory and ESG pressure pushes laboratories to qualify low-toxicity, bio-based solvent alternatives across existing workflows.

The USD 18.21 billion market of 2032 is not simply a larger version of today's market. It is a structurally more complex, more specification-driven, and more margin-differentiated market — and the suppliers positioned to serve its most demanding segments are building advantages that commodity solvent providers cannot replicate.

To know about the Research Methodology :- Request Free Sample Report

Consumer Impact and Adoption Dynamics in Chromatography Reagents Market

Pharmaceutical & Biotechnology Consumers

Pharmaceutical companies had remained the largest consumers of chromatography reagents, especially HPLC reagents, LC-MS reagents, and high-purity chromatography reagents for drug discovery, impurity profiling, release testing, and quality control. As of 2025, over 70% of FDA-approved biologics approved in the preceding five-year period had utilised HPLC-based methods for stability characterisation and purity profiling — underscoring the non-negotiable role of high-purity chromatography reagents in regulated biologics development.

Adoption was driven by stringent regulatory requirements and high-value analytics needs, with some pharma R&D labs running thousands of chromatographic runs per week, each requiring consistent batches of solvents such as acetonitrile (HPLC grade), methanol (chromatography grade), and water (HPLC grade).

Biochromatography reagents for protein purification were central to biologics and biosimilars development, improving yield and reproducibility in protein separation workflows, critical where value per run could be USD 500–USD 1,500 in operational cost.

Food & Environmental Testing Laboratories

Demand for analytical grade solvents for chromatography and chromatography reagents for environmental analysis saw acceleration due to intensified food safety regulations and environmental quality mandates. The Comprehensive European Food Safety (CHEFS) database mined over 392 million analytical results from more than 15.2 million food samples between 2000 and 2024, underscoring extensive use of chromatographic analysis for regulatory compliance.

In North America, for example, testing labs expanded their routine chromatography usage to screen for contaminants such as pesticides and water pollutants, driving year on year reagent requests by double-digit percentages as compliance requirements tightened.

Academic & Research Institutions

Academic adoption of laboratory chromatography reagents was driven by grant-funded research and core facilities that supported multidisciplinary studies in chemistry, biology, environmental sciences, and materials sciences.

These institutions significantly influenced product innovation demand, especially where new methods such as ion exchange chromatography and size exclusion chromatography were first validated.

Chromatography Reagents Market Demand vs. Supply: Strategic Penetration and Constraints

Demand Outpacing Supply in Specialised Segments. The basic solvents saw broad availability, demand had outpaced supply in critical speciality categories particularly high purity reagents, GMP grade chromatography reagents, MS grade solvents for LC MS applications, and custom chromatography reagents. This happened because:

Regulatory agencies globally raised the bar for precision and reproducibility, requiring every reagent batch to meet tighter specifications.

Expansion in applications such as chromatography reagents for clinical diagnostics and chromatography reagents used in drug development increased overall usage intensity per laboratory.

Supply Challenges in the Chromatography Reagents Market

The chromatography reagent supply chain bore vulnerabilities related to raw material price volatility, especially for specialised buffers, ion pair reagents, and bio-based solvents, where costs could fluctuate 10–30% year over year with Chromatography Reagents market shifts.

Unplanned reagent shortages in specific solvents (e.g., acetonitrile) occasionally led to inventory delays in high-throughput labs, impacting throughput in pharmaceutical testing and quality control pipelines.

Organised vs. Unorganised Suppliers in Chromatography Reagents Market

Organized players such as Thermo Fischer Scientific, Agilent Technologies, Merck KGaA, Waters Corporation, and Sigma Aldrich dominated the high-end reagent space, ensuring stringent quality, batch traceability, and global distribution networks.

Organized players captured was 65% Chromatography Reagents Market share in 2025, while unorganised suppliers prevalent in parts of Asia and South America maintained a strong local presence but struggled to compete on quality certifications, GMP compliance, and global procurement contracts.

This dual structure meant that while unorganised suppliers served cost-sensitive segments, they faced barriers to entry in premium, regulated markets such as pharmaceuticals and clinical diagnostics.

Penetration of Automation and Analytical Trends in Chromatography Reagents Market

Automation & High Throughput Integration

Adoption of automated chromatography systems, especially those incorporating AI enhancements and real-time data analytics, directly drove sales of specialised mobile phase reagents and volatile agents like trifluoroacetic acid (TFA) and ammonium formate.

In 2025, 60% of leading laboratories had either integrated or were transitioning toward automation-compatible reagent platforms, optimising the accuracy of multi-site analytical operations.

Green Chromatography and Sustainable Practices

The shift toward sustainable chromatography solvents market and green chromatography reagents trends was not merely a branding exercise; it directly influenced procurement decisions in regulated sectors where environmental compliance was mandated.

Solvents such as low-toxicity isopropanol (IPA) and ethyl acetate began supplanting traditional reagents in certain workflows, particularly where disposal and lifecycle costs mattered to stakeholders.

Opportunities and Strategic Threats in Chromatography Reagents Market

Expansion in Emerging Regions

Emerging Chromatography Reagents Market, such as China, India, and Brazil had become priority targets due to rising investments in pharmaceutical R&D, enhanced regulatory oversight, and expansion of biotechnology initiatives. In China, local reagent producers were gaining traction as regulatory pressures and tariff changes incentivised domestic sourcing over imports.

Precision Medicine and Biopharma Workflows

The increasing importance of LC-MS reagents for proteomics and biomolecule separations opened opportunities in high-value niches like monoclonal antibody purification and targeted therapeutics, high-margin segments that demanded bespoke reagent blends.

Sustainable Chemistry Solutions

Growing demand for green chromatography reagents and biochromatography reagents provided a pathway for differentiation. As environmental compliance became strategic rather than merely regulatory, suppliers meeting these needs gained premium positioning.

Key Timeline for the Chromatography Based on Reagents and Methods

| Stage | Method of Analysis | Reagents Needed | Time Frame to Implement |

| Early-Stage (R&D) | Discovery & Drug Development | HPLC reagents, LC-MS reagents, Biochromatography reagents | Immediate start, due to the need for rapid high-purity testing. Research labs need reagents like acetone, acetonitrile, methanol, and water for development and early-stage testing. |

| Post-Discovery (Process Development) | Method Development & Optimization | Solvents for HPLC, Ion-pair reagents, Mobile phase reagents | Medium-term start, within 3-6 months from discovery, to integrate into new drug formulations. Reagents like butanol, methanol, and acetonitrile used for optimizing processes in both HPLC and LC-MS setups. |

| Manufacturing Stage | Manufacturing & Quality Control | Solvents for HPLC/UHPLC gradient, Analytical reagents | 6-12 months to scale production, focusing on high-quality solvents for analytical testing. High purity and consistency become critical, particularly in commercial-scale productions. |

| Final Product Testing | Clinical Testing and Quality Control | Solvents for LC-MS, HPLC (for final product purity and stability) | Immediate need once product batch is ready for clinical trials or market launch. Reagents such as acetone, methanol, and ethanol will be crucial at this stage for compliance. |

| Environmental & Compliance Testing | Wastewater and Environmental Control | Chromatography reagents for environmental analysis, Mobile phase reagents | Long-term ongoing needs. As pharmaceutical production grows, regulatory demands on environmental impact (via Chromatography solvents like methanol, acetonitrile) grow as well. |

| Sustainability Initiatives | Sustainable Product Development | Bio-based chromatography reagents, Green chromatography solvents | 1-2 years. Companies focusing on sustainability start integrating bio-based and low-toxicity reagents like ethyl acetate and 2-propanol into their operations for compliance. |

Raw Material Volatility and Price Pressure

Frequent fluctuations in key solvent and buffer feedstock prices threatened margin erosion for reagent suppliers and forced end users toward long term contracts or local sourcing strategies, challenging global supplier dominance.

Challenge: Skill Gaps and Operational Bottlenecks

The laboratories faced a skills gap in chromatography technique execution, a major hindrance that laboratories cited as a barrier to fully harnessing advanced reagents and technologies.

Chromatography Reagents Market: Key Technology Trends

HPLC & UHPLC: HPLC remains the most deployed chromatography technique globally. UHPLC adoption is accelerating at >600 bar operating pressures, enabling faster runs and lower solvent consumption — driving demand for ultra-high purity mobile phase reagents compatible with sub-2μm columns.

LC-MS/MS: Migration from HPLC to LC-MS/MS is the most impactful technology shift in the reagents market. MS-grade solvents with metal ion concentrations below 1 ppb are mandatory — structurally expanding the premium-grade reagent addressable market.

Biochromatography: Protein purification for biologics relies on ion-exchange, size-exclusion, and affinity chromatography — each requiring specialised buffers and elution reagents. Value per run can reach USD 500–1,500, making this the highest-margin reagent category.

Automation & AI: In 2025, 60% of leading laboratories had integrated or were transitioning to automation-compatible reagent platforms — amplifying batch-to-batch consistency requirements for volatile modifiers and mobile phases.

Green Chromatography: Low-toxicity solvents — IPA, ethyl acetate, bio-based alternatives — are progressively replacing halogenated solvents, driven by ESG mandates and rising disposal costs, particularly across European laboratories.

SFC: Supercritical Fluid Chromatography is the fastest-growing technique, gaining traction in pharmaceutical chiral separations — delivering faster runs, lower solvent waste, and a growing CO₂-based mobile phase reagent sub-category.

Chromatography Reagents Market Segment Analysis:

Solvents held the largest share in the chromatography reagents market in 2025, due to their critical role in mobile phase preparations for HPLC, GC, and LC-MS techniques. High-purity solvents like acetonitrile and methanol were essential for ensuring accurate and reproducible separations across various chromatographic methods.

The Ion Pair Reagents segment was identified as the fastest-growing segment in 2025, driven by increased use in pharmaceutical chromatography reagents and biochromatography reagents. These reagents enhance the separation of ionic analytes, which is crucial for complex pharmaceutical and biotechnology applications requiring high precision.

By Type — Buffers:

Buffers represented the second-largest type segment in the chromatography reagents market in 2025, essential for maintaining pH stability and ionic strength in liquid chromatography mobile phases — particularly in biochromatography workflows involving protein purification, antibody characterisation, and biosimilar development. Ammonium formate, ammonium acetate, and phosphate-based buffers are among the most widely consumed, with demand closely correlated to the expansion of LC-MS/MS applications in clinical diagnostics and pharmaceutical impurity profiling. GMP-grade buffer formulations command significant price premiums over standard analytical grade, driving revenue concentration in the regulated pharmaceutical and biologics segments.

By Physical State of Mobile Phase:

Liquid chromatography reagents dominated this segment in 2025, accounting for the largest share driven by the widespread adoption of HPLC, UHPLC, and LC-MS techniques across pharmaceutical, food safety, and environmental testing applications. Gas chromatography reagents maintained a stable position, particularly in volatile compound analysis, flavour and fragrance testing, and petrochemical quality control. Supercritical fluid chromatography (SFC) reagents, while currently the smallest sub-segment, are the fastest growing — supported by the pharmaceutical industry's adoption of SFC for chiral separation applications where traditional HPLC methods are less efficient and generate higher solvent waste volumes.

By Application: Pharmaceutical applications held the dominant share of the chromatography reagents market in 2025, driven by the industry's reliance on HPLC, LC-MS, and biochromatography techniques for drug discovery, process development, quality control, and regulatory submission. Some pharmaceutical R&D labs execute thousands of chromatographic runs per week, each requiring consistent, certified batches of high-purity solvents and buffers. Food and beverage testing represented the second-largest application, with the CHEFS database alone encompassing over 392 million analytical results from more than 15.2 million food samples — reflecting the scale of chromatographic analysis in food safety compliance. Water and environmental analysis is the fastest-growing application, driven by tightening global regulations on pesticide residues, pharmaceutical contaminants, and industrial pollutants in water systems.

Chromatography Reagents Market Regional Analysis

North America held the largest share due to its robust pharmaceutical and biotechnology sectors in 2025, advanced healthcare infrastructure, and high demand for precision analytical techniques. The region is driven by technological advancements in Chromatography Reagents, such as HPLC and LC-MS, along with the increasing adoption of automated chromatography systems in research and development. The U.S. leads with a significant Chromatography Reagents Market share, supported by large investments in drug discovery, quality control processes, and regulatory compliance. Furthermore, North America is a hub for major chromatography OEMs and research institutions.

Europe:

Europe represented the second-largest chromatography reagents market in 2025, anchored by Germany, France, the UK, and Switzerland — home to some of the world's largest pharmaceutical and specialty chemical manufacturers. Stringent regulatory frameworks including EMA guidelines and EU environmental directives drive consistent demand for high-purity, GMP-compliant reagents. The region is also a centre for green chromatography innovation, with European labs increasingly substituting traditional halogenated solvents with low-toxicity alternatives such as ethyl acetate and isopropanol to meet environmental compliance mandates.

Asia Pacific:

Asia Pacific is the fastest-growing chromatography reagents market, driven by rapid pharmaceutical R&D expansion in China and India, growing contract research and manufacturing (CRAM) sector activity, and increasing regulatory harmonisation with FDA and EMA standards. China represents the largest APAC opportunity, where domestic reagent producers are gaining regulatory approvals and competing with global players in the mid-tier segment. India's growing generic pharmaceutical export industry is a structural demand driver, with HPLC and LC-MS reagents essential for meeting USP and ICH quality standards required for U.S. and European market access.

Middle East & Africa:

The MEA chromatography reagents market remains at early penetration but is developing steadily, supported by GCC nations' investments in pharmaceutical manufacturing localisation, hospital laboratory expansion, and food safety infrastructure. The UAE and Saudi Arabia are establishing pharmaceutical regulatory frameworks aligned with international standards, progressively increasing demand for certified analytical and GMP-grade chromatography reagents. Africa represents a long-term frontier opportunity, currently constrained by laboratory infrastructure gaps and import dependency.

South America:

Brazil dominates the South American chromatography reagents market, driven by its large pharmaceutical manufacturing base, active generic drug sector, and expanding food and environmental testing networks supported by ANVISA regulatory requirements. Argentina and Colombia represent secondary growth markets. Price sensitivity and reliance on imported reagents — primarily from North America and Europe — create vulnerability to currency fluctuation and supply chain disruption, incentivising the development of regional reagent manufacturing capabilities over the forecast period.

Competitive Landscape in Chromatography Reagents Market:

The global chromatography reagents market is moderately consolidated at the premium end, with Thermo Fisher Scientific, Merck KGaA (MilliporeSigma/Sigma-Aldrich), Agilent Technologies, and Waters Corporation collectively commanding the majority of regulated market revenue. These players compete on batch traceability, GMP certification depth, global distribution reliability, and integrated reagent-instrument ecosystem positioning — factors that are increasingly decisive in pharmaceutical and clinical laboratory procurement.

Avantor and Danaher have strengthened their positions through strategic acquisitions and vertical integration across the reagent supply chain. Meanwhile, regional manufacturers in China, India, and Eastern Europe — including Loba Chemie and HiMedia Laboratories — are gaining share in cost-sensitive academic and food testing segments, leveraging competitive pricing and improving quality certification portfolios. The organised segment accounted for approximately 65% of market share in 2025, with unorganised suppliers maintaining a foothold in local Asian and South American markets through price advantage — constrained by their inability to meet GMP, ISO, and global procurement contract requirements of regulated end-users.

The in Chromatography Reagents Market Will Not Distribute Value Equally

Winners — GMP-Certified, MS-Grade Specialists: The suppliers who have invested in MS-grade solvent manufacturing, certified ion-pair reagent production, and biochromatography buffer portfolios are entering a demand cycle where their customers have no qualified alternatives and switching costs are prohibitively high. Regulatory validation of a new reagent supplier in a pharmaceutical QC workflow takes 6–18 months — a moat that is entirely supplier-created and entirely sustainable.

Challengers — Asian Manufacturers Closing the Quality Gap: Chinese and Indian reagent producers are advancing rapidly toward GMP certification and ISO accreditation, targeting the academic, food testing, and environmental segments where price sensitivity is high and quality requirements are lower than pharmaceutical-grade. The manufacturers who achieve international certification first will capture the mid-market before global incumbents can respond with competitive pricing.

At Risk — Unbranded Commodity Solvent Suppliers: Suppliers competing purely on solvent volume and price in standard HPLC-grade categories face accelerating margin compression as the market migrates toward higher specification grades. The commodity solvent business is not disappearing, but the value is moving upward in the specification hierarchy — and suppliers without the capability to follow will find their addressable market progressively shrinking.

Recent Developments in Chromatography Reagents Market:

• May 2025: Thermo Fisher Scientific launched a new range of bio-based chromatography solvents, providing sustainable solutions for pharmaceutical testing and biotech applications.

• June 2025: Agilent Technologies introduced an AI-powered chromatography system designed to optimise workflows with predictive maintenance and real-time data analytics.

• August 2025: Waters Corporation expanded its offering with new MS-grade solvents, targeting the growing proteomics and drug discovery markets.

Chromatography Reagents Market Scope: Inquire before buying

| Chromatography Reagents Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 8.75 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 11.04% | Market Size in 2032: | USD 18.21 Bn. |

| Segments Covered: | by Type | Buffers Ion-Pair Reagents Solvents Other Types (Derivatization Reagents, etc.) |

|

| by Physical State of Mobile Phase | Gas Chromatography Reagents Liquid Chromatography Reagents Super Critical Fluid Chromatography (SFC) Reagents |

||

| by Separation Mechanism | Adsorption Chromatography Partition Chromatography Ion-Exchange Chromatography Size-Exclusion Chromatography Affinity Chromatography |

||

| by Chromatography Technologies | HPLC UHPLC GC LC-MS/MS SFC Ion Chromatography Others |

||

| by Application | Pharmaceutical Food and Beverages Water and Environmental Analysis Other Applications (Forensic Analysis, Cosmeceutical Application, etc.) |

||

MMR Analyst Siddhi Dole’s View — What the Chromatography Reagents Market Data Is Really Telling You

An 11.04% CAGR in a reagent market — typically one of the most stable and slow-moving categories in life sciences supply — is a signal that something structural is happening, not just cyclical growth. That structural force is the specification upgrade cycle: as analytical techniques migrate from HPLC to UHPLC to LC-MS/MS, and as therapeutic pipelines shift from small molecules to biologics, the reagent requirements at every stage are becoming more precise, more costly, and more difficult to substitute.

The suppliers who understand this are investing in MS-grade manufacturing, GMP infrastructure, and biochromatography buffer portfolios. The ones who don't are watching their core HPLC solvent business grow nominally while the margin-accretive segments of the market migrate to competitors. For investors, the most durable positions in this market are in companies with certified, traceable, high-specification reagent portfolios serving pharmaceutical and clinical end-users — categories where price elasticity is low, switching costs are high, and growth is structurally compelled by regulatory requirements rather than discretionary spending cycles.

Chromatography Reagents Key Players

1. Thermo Fisher Scientific, Inc.

2. Merck KGaA (MilliporeSigma / Sigma-Aldrich)

3. Agilent Technologies, Inc.

4. Waters Corporation

5. Avantor, Inc.

6. Danaher Corporation

7. Shimadzu Corporation

8. PerkinElmer, Inc.

9. Bio-Rad Laboratories, Inc.

10. Phenomenex, Inc.

11. Regis Technologies, Inc.

12. Tosoh Bioscience GmbH

13. MACHEREY-NAGEL GmbH & Co. KG

14. Hamilton Company

15. JASCO

16. GL Sciences Inc.

17. Loba Chemie Pvt. Ltd.

18. GFS Chemicals, Inc.

19. KANTO KAGAKU

20. Sigma-Aldrich

21. Honeywell Burdick & Jackson

22. TCI Chemicals

23. Alfa Aesar

24. Tokyo Chemical Industry Co., Ltd. (TCI)

25. Honeywell Research Chemicals

26. Spectrum Chemical Manufacturing Corp.

27. FUJIFILM Wako Pure Chemical Corporation

28. SRL (Sisco Research Laboratories Pvt. Ltd.)

29. HiMedia Laboratories

30. CDH Fine Chemical

31. PanReac AppliChem

32. MP Biomedicals

33. Carlo Erba Reagents

Frequently Asked Questions

1. What drives the growth of the chromatography reagents market?

Ans: The growth is driven by the increasing demand for high-purity reagents in pharmaceutical testing, biotech, and environmental analysis, along with the adoption of automation and sustainable solvents.

2. What are the main challenges in the chromatography reagents market?

Ans: Challenges include high upfront costs, skilled personnel shortages, and financial constraints that limit the adoption of advanced reagents and technologies.

3. Which regions are growing the fastest in this market?

Ans: Asia-Pacific is the fastest-growing region due to increased investments in pharmaceuticals and biotech, with North America remaining a key leader.

4. Which chromatography reagents are in high demand?

Ans: HPLC reagents lead the market, followed by LC-MS reagents and sustainable chromatography solvents due to rising environmental and regulatory concerns.

5. What is the projected market size and growth rate of the Chromatography Reagents Market?

Ans: The global chromatography reagents market was valued at USD 8.75 billion in 2025 and is projected to grow at a CAGR of 11.04%, reaching USD 18.21 billion by 2032, supported by expanding pharmaceutical R&D activity, rising demand for high-purity LC-MS and HPLC reagents, and the accelerating adoption of automated and green chromatography workflows.