Carbon Capturing and Storage Technology Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2034

Overview

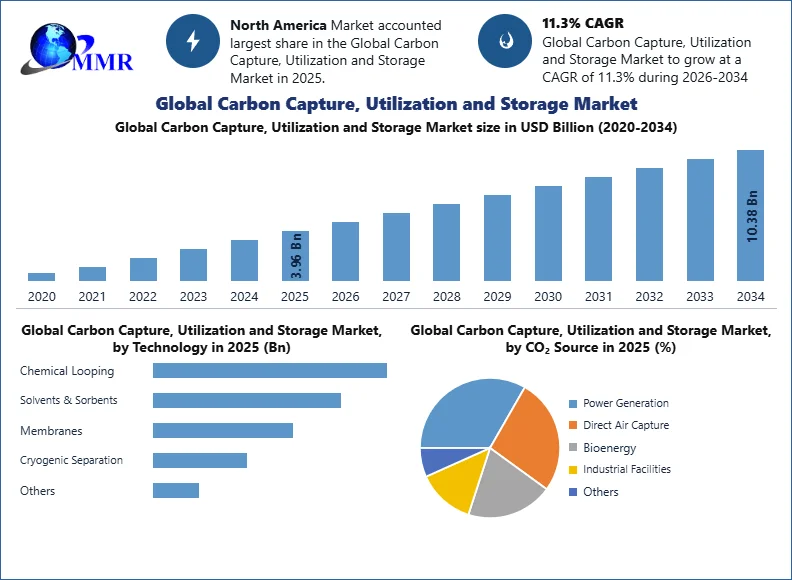

Carbon Capturing and Storage Technology Market was valued USD 3.96 Bn. in 2025 and is expected to reach USD 10.38 Bn. by 2034.

Carbon Capturing and Storage Technology captures carbon dioxide formed during power generation and industrial processing and stores it ultimately saving the carbon emission in the environment. The capturing of the carbon dioxide is done through various procedures such as Pre-Combustion, Post Combustion, Oxy-Fuel Combustion, and Industrial Separation. The captured carbon dioxide is compressed into a liquid state and then transported to the storage site. The transportation is carried out through pipelines, ships, and roads to various locations where it is required.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The report covers the detailed analysis of global carbon capturing and storage technology with the classifications of the market on the product type, applications, and region. Analysis of past market dynamics from 2025 to 2034 is given in the report, which will help readers to benchmark the past trends with current market scenarios with the key player's contribution in it.

The report has profiled eighteen key players in the market from different regions. However, the report has considered all market leaders, followers, and new entrants with investors while analysing the market and estimation the size of the same. Manufacturing the environment in each region is different and focus is given on the regional impact on the cost of manufacturing, supply chain, availability of raw materials, labour cost, availability of advanced technology, trusted vendors are analysed and the report has come up with recommendations for a future hot spot in APAC region. The major country’s policies about manufacturing and its impact on storage technology demand are covered in the report.

Carbon Capturing and Storage Technology Market Dynamics-

Increasing demand for clean power technologies and growing concerns about climate change are the major factors driving the Global Market. Though many alternate technologies like wind, solar and nuclear energy are used but carbon capturing and storage technology is the most feasible technology available, which decreases greenhouse gas emissions that occur from large scale usage of fossil fuel.

Government regulations and policies to limit the greenhouse gases emission across the economic sectors with the involvement of regulators will further, stimulate the growth of carbon capture and storage industry over the forecast period.

The high cost of implementation acts as restraints to the growth of Global Carbon Capturing and Storage Technology Market. The cost associated with the equipment and energy needed for the capturing is very high. The technology used for storage of carbon materials is in developing phase and require more high-cost technological advancement.

Increasing importance for bioenergy carbon capture and storage is likely to act as an opportunity in the future. Increasing demand for carbon dioxide injection also acts as an opportunity for Global Market. It is seen that carbon dioxide injection is a good transferring agent for the oil recovery services.

Carbon Capturing and Storage Technology Market Segment analysis-

The report groups the Global Market in different segments by capture technology, by application, by type, by service type, and by region to forecast the revenues and analyse the Market share of each segment over the forecast period.

Based on capture technology, Pre combustion capture technology was dominant in 2025 and is expected to command the market share of 30.4% by 2025. Advantage of this technology is that it incurs less energy penalty. Pre combustion capture technology involves the removal of carbon dioxide from fossil fuels before combustion. It is considered as more efficient capture technology compared to post-combustion, which is contributing to the growth of Global Carbon Capturing and Storage Technology Market.

By Application, Oil and Gas segment is expected to grow at 13.8% by 2034, which is fastest among other sub-segments. Increasing demand for crude oil and natural gas has increased the investment in oil and gas refineries. Carbon capture and storage technology are helping the oil and gas industry to reduce the greenhouse gases emission in the atmosphere. Carbon dioxide captured and stored is also used in enhanced oil recovery, which has been developed in the oil and gas industry. The stringent government rules and regulations for the reduction of emissions from the oil and gas sector have led to an increase in demand for carbon capture and storage technology.

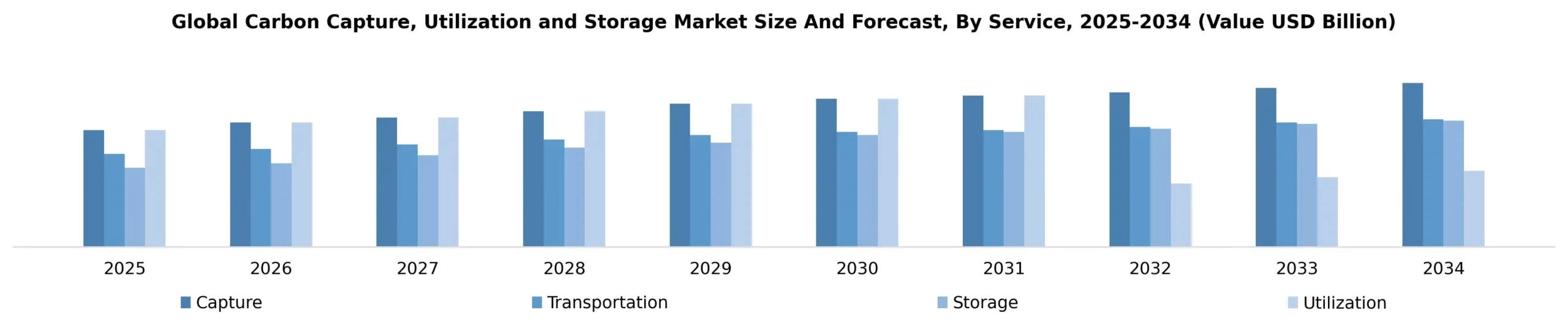

Based on Service, the Carbon Capture, Utilization and Storage (CCUS) Market is segmented into Capture, Transportation, Storage, and Utilization. The Capture segment held the largest Carbon Capture, Utilization and Storage Market share in 2025. The dominance of this segment is attributed to the increasing deployment of carbon capture technologies at large industrial facilities and power plants to reduce greenhouse gas emissions before they enter the atmosphere. Capture accounts for the highest share of total CCUS project investment due to the installation of specialized equipment, including absorption systems, compressors, and gas treatment units. Stringent emission reduction regulations, growing carbon pricing mechanisms, and increasing investments in decarbonization projects across energy-intensive industries continue to accelerate the adoption of carbon capture technologies worldwide.

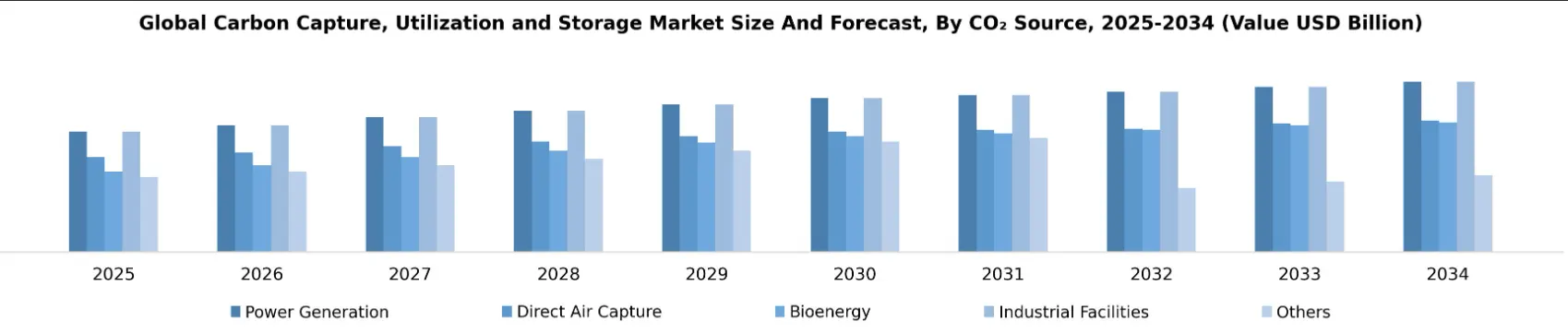

Based on CO₂ Source, the Carbon Capture, Utilization and Storage Market is segmented into Power Generation, Direct Air Capture, Bioenergy, Industrial Facilities, and Others. The Power Generation segment held the largest Carbon Capture, Utilization and Storage Market share in 2025. Fossil fuel-based power plants remain among the largest contributors to global carbon dioxide emissions, driving the widespread deployment of carbon capture systems to support emission reduction targets. Governments and utilities are increasingly investing in CCUS-equipped thermal power plants to comply with climate regulations while maintaining energy security. Continued investments in low-carbon power generation and retrofitting of existing coal- and gas-fired plants further strengthen the dominance of the power generation segment.

Based on Project Type, the Carbon Capture, Utilization and Storage Market is segmented into Greenfield and Brownfield. The Brownfield segment held the largest Carbon Capture, Utilization and Storage Market share in 2025. The growth of this segment is driven by the increasing retrofitting of existing industrial facilities, refineries, power plants, and petrochemical complexes with carbon capture systems. Brownfield projects offer lower capital costs, shorter implementation timelines, and the ability to utilize existing infrastructure compared to new developments. As governments introduce stricter carbon emission regulations, industries are prioritizing retrofit projects to reduce emissions while extending the operational life of existing assets.

Based on Technology, the Carbon Capture, Utilization and Storage Market is segmented into Chemical Looping, Solvents & Sorbents, Membranes, Cryogenic Separation, and Others. The Solvents & Sorbents segment held the largest Carbon Capture, Utilization and Storage Market share in 2025. The segment dominates the market due to its proven commercial deployment, high carbon capture efficiency, and compatibility with a wide range of industrial processes. Solvent-based absorption technologies, particularly amine-based systems, are extensively used in power generation, natural gas processing, and chemical manufacturing because of their maturity and scalability. Continuous research into advanced solvent formulations and solid sorbent materials is improving energy efficiency and reducing operating costs, further driving market adoption.

Based on End-Use Industry, the Carbon Capture, Utilization and Storage Market is segmented into Oil & Gas, Power Generation, Chemical & Petrochemical, Cement, Iron & Steel, and Others. The Oil & Gas segment held the largest Carbon Capture, Utilization and Storage Market share in 2025. The dominance of this segment is driven by the industry's increasing investment in carbon capture technologies to reduce operational emissions while supporting enhanced oil recovery (EOR) operations. Captured carbon dioxide is widely injected into mature oil reservoirs to improve hydrocarbon recovery, providing both environmental and economic benefits. Additionally, stringent government regulations on industrial emissions, corporate net-zero commitments, and growing investments in low-carbon oil and gas production continue to accelerate the deployment of CCUS technologies across upstream, midstream, and downstream operations, reinforcing the segment's leading position in the global market.

North America is expected to command largest market share of by 2034

Government regulations and environmental concerns in North America for a clean environment because of an increased number of oilfields is the major driving factor for the growth of Global Market. North America has the largest carbon capture, storage and utilization market because of the presence of a large number of carbons capturing and storage facilities in the US and Canada. Around 14 projects of carbon capture and storage are operational in North America.

The objective of the report is to present a comprehensive analysis of the Global Carbon Capturing and Storage Technology Market to the stakeholders in the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that includes market leaders, followers, and new entrants. PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding Global Carbon Capturing and Storage Technology Market dynamics, structure by analyzing the market segments and project the Global Carbon Capturing and Storage Technology Market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the Global Carbon Capturing and Storage Technology Market make the report investor’s guide.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 27 February 2026 | Air Liquide | Signed an agreement with Holcim to decarbonize cement production in Belgium using Cryocap™ OXY carbon capture technology. | The project enables high-rate CO2 capture at scale for hard-to-abate industrial sectors. |

| 20 May 2025 | U.S. Department of Energy (DOE) | Announced the achievement of a carbon capture cost reduction milestone, reaching the target of under $40 per ton. | Lowering capture costs significantly increases the economic viability of large-scale commercial CCS projects. |

| 05 May 2025 | Northern Lights (Equinor, Shell, TotalEnergies) | Received the world's first shipment of liquefied CO2 from Heidelberg Materials for sequestration. | This marks the operational start of cross-border CO2 transport and storage infrastructure in Europe. |

| 18 March 2025 | TotalEnergies | Announced the Final Investment Decision (FID) for Phase 2 of the Northern Lights project with its joint venture partners. | The expansion will increase total transport and storage capacity to over 5 million tonnes of CO2 per year. |

| 22 January 2025 | Green Plains Inc. | Commenced operations at its Nebraska CCS project using a post-combustion capture approach. | The facility is designed to capture and store 1.2 million tons of carbon annually from ethanol production. |

| 15 January 2025 | Chevron | Entered a strategic partnership with Engie and GE Vernova to develop a 4 GW natural gas plant integrated with CCS. | The collaboration aims to demonstrate low-emission power generation through large-scale carbon sequestration. |

Competitive Analysis

The CCUS competitive landscape is dominated by integrated energy majors such as Shell, ExxonMobil, Equinor, Occidental Petroleum, Chevron, and TotalEnergies. These companies lead through storage acreage, transport networks, project financing, industrial-emitter partnerships, and subsurface expertise. Shell, Equinor, and TotalEnergies strengthened their European position through the Northern Lights project, where the partners approved a 2025 expansion to increase annual CO₂ injection capacity from about 1.5 million tonnes to more than 5 million tonnes. ExxonMobil also expanded its U.S. Gulf Coast strategy in 2025 by signing an agreement with Calpine to transport and store up to 2 million metric tons of CO₂ per year from a power generation project. These companies shape the market by building full-chain CCUS infrastructure rather than offering only individual capture or storage services.

Technology and EPC players such as Mitsubishi Heavy Industries, SLB Capturi, Linde, Honeywell, Fluor, Saipem, Baker Hughes, Halliburton, Sulzer, JGC Holdings, and Hitachi Industrial Products compete through capture systems, solvents, modular plants, compression equipment, engineering delivery, and lifecycle services. SLB Capturi strengthened its modular carbon capture position in 2025 by commissioning and handing over a plant at Twence in the Netherlands with capacity to capture up to 100,000 metric tons of CO₂ annually. Mitsubishi Heavy Industries continues to lead in post-combustion capture licensing, while Honeywell expanded its utilization-linked role in 2025 through its agreement with AM Green in India for CO₂-to-fuels and green methanol opportunities. These companies drive market growth by helping industrial emitters move from pilot projects to commercially deployable capture systems.

Specialist carbon-removal and utilization companies such as CarbonCapture Inc., Carbon Clean, Climeworks, LanzaTech, Zero Carbon Systems, Carbon Engineering, CarbFix, CarbonFree, CarbonCure, Charm Industrial, Graphyte, and Greenlyte Carbon Technologies compete through direct air capture, modular capture, mineralization, concrete curing, bio-oil storage, and CO₂ utilization technologies. Carbon Clean advanced its utilization positioning in 2025 when its NTPC project in India produced methanol using captured CO₂, showing how CCUS is moving toward revenue-generating carbon utilization. Climeworks also strengthened its direct air capture position in 2025 by raising funding and signing a carbon removal agreement with SAP covering removals through 2034. Overall, the market is shifting toward companies that can combine capture technology, transport, storage verification, carbon accounting, and long-term liability management into one integrated CCUS solution.

Scope of the Carbon Capturing and Storage Technology Market- Inquire before buying

| Carbon Capturing and Storage Technology Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 3.96 USD Bn |

| Forecast Period 2026-2034 CAGR: | 11.3% | Market Size in 2034: | 10.38 USD Bn |

| Segments Covered: | by Project Type | Greenfield Brownfield |

|

| by Capture Technology | Pre-Combustion Post Combustion Oxy-Fuel Combustion Industrial Separation |

||

| By CO₂ Source | Power Generation Direct Air Capture Bioenergy Industrial Facilities Others |

||

| by Service | Capture Transportation Utilization Storage |

||

| By Technology | Chemical Looping Solvents & Sorbents Membranes Cryogenic Separation Others |

||

Carbon Capturing and Storage Technology Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key players/competitors profile covered in Carbon Capturing and Storage Technology Market report in strategic perspective

- Shell plc

- ExxonMobil

- Equinor ASA

- Occidental Petroleum Corporation

- Linde plc

- Mitsubishi Heavy Industries Ltd.

- CarbonCapture Inc.

- Fluor Corporation

- Chevron

- SLB Capturi

- Honeywell International Inc.

- Baker Hughes Company

- Halliburton

- Saipem

- Carbon Clean

- Climeworks

- LanzaTech

- Zero Carbon Systems

- Carbon Engineering

- CarbFix

- Japan CCS Co. Ltd.

- Sulzer Ltd.

- JGC Holdings Corporation

- Hitachi Industrial Products, Ltd.

- CarbonCure Technologies Inc.

- Charm Industrial

- Graphyte, Inc.

- Greenlyte Carbon Technologies

- TotalEnergies SE

Others