Carbon Capture, Utilization and Storage Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

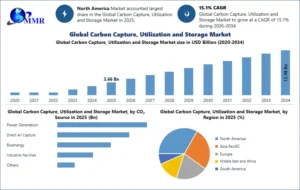

Carbon Capture, Utilization and Storage Market was valued at USD 3.66 Billion in 2025, and is expected to reach USD 12.96 Billion by 2034, exhibiting a CAGR of 15.1% during the forecast period (2026-2034)

Carbon Capture, Utilization and Storage Market Overview

The global carbon capture, utilization and storage market is expected to get boost from large consumer base in developed as well as developing economies. North America and Europe are developed markets with well-established systems for dealing with industrial gases as better infrastructure for industrial gases could provide better processing, storage and transport facilities that could help lower cost of production.

Developing regions such as Asia-Pacific, the Middle East and Africa, are fast-growing markets. The carbon capture, utilization and storage market globally is witnessing increases in growth due to technological advancements, high industrial activity, large investments and high demand for industrial processes, leading to a rise in industrial gas market.

The carbon capture, utilization, and storage market consist of sales of carbon capture, utilization, and storage technologies by business entities (organizations, sole traders, and partnerships) that are engaged in providing clean and efficient energy solutions. Carbon capture, utilization, and storage (CCUS) involves a number of methods and technologies for removing carbon dioxide from flue gas and the atmosphere, recycling it for use, and establishing safe and long-term storage choices. CCUS reduces global carbon dioxide emissions, helps mitigate global warming and reduces the cost of tackling the climate crisis.

The Carbon Capture, Utilization, and Storage (CCUS) market has transitioned from a climate goal to a critical geopolitical hedge as the 2026 Middle East crisis persists. With the Hormuz blockade driving crude to $120/bbl, the 30% spike in energy-intensive processing costs is being offset by AI-optimized carbon recycling. Leaders are deploying near-shored modular capture units to bypass 400% freight surcharges, securing industrial resilience against historic energy-driven volatility.

To know about the Research Methodology:- Request Free Sample Report

Carbon Capture, Utilization and Storage Market Trends

Carbon Dioxide Supply to Greenhouses: Carbon capture, utilization and storage companies should consider supplying to greenhouses. It is important for the owners of greenhouses to regulate the levels of CO2 in greenhouses. Carbon dioxide manufacturers are exploring opportunities to supply industrial greenhouses.

The essential process of photosynthesis for plant growth requires CO2. Throughout any given day, there is a variation in the levels of CO2 concentration depending on the time of day, the season, and the number of CO2 producing industries. Hence, it is important for the levels of CO2 to be regulated within the greenhouse, the carbon dioxide level may reduce to 150-200 parts per million in the daytime in a sealed greenhouse.

Artificial Intelligence (AI) in Carbon Reduction: Carbon capture, utilization and storage companies should focus on investing in AI based technology that will drive innovation and cater to a wider customer base. AI’s ability to deliver deep insights into multiple aspects of a company’s carbon footprint and quick cost-cutting offers a promising route to accelerating sustainable transformation and reducing expenses in a time of need.

Companies are leveraging artificial intelligence to create separation materials for Co2 which are more efficient and can reduce the current costs of carbon capture. Using molecular generative AI modeling, IBM identified several hundred molecular structures that could enable more efficient and cheaper alternatives to existing separation membranes for capturing CO₂ emitted in industrial processes.

Carbon Capture, Utilization and Storage Market Dynamics

Supportive Government Initiatives to Drive the Carbon Capture, Utilization and Storage Market Growth

The Carbon Capture, Utilization and Storage Market is expected to be supported by government initiatives in the forecast period. For example, the US Department of Energy’s (DOE) Office of Fossil Energy and Carbon Management (FECM) announced up to $96 million in federal funding for projects that will develop point-source carbon capture technologies for natural gas power plant and industrial applications capable of capturing at least 95% of carbon dioxide (CO2) emissions generated.

At the United Nations Climate Change Conference in Glasgow (COP26), a group of 50 countries pledged to create climate resilient and low-carbon health systems in response to mounting evidence of climate change's impact on people's health.

- In Union Budget 2026-27, there is an allocation of USD 2.38 billion for the next five years for the fast commercialization of CCUS technology in India. This budget is planned to be utilized in the application of CCUS technology in five industries which emit carbon. Also, the CCUS technology roadmap of India has projected that the technology would capture 750 million tons of CO₂ per year till 2050 from hard-to-decarbonize industries. Currently, there are around 50 CCUS plants in the world capturing 50 million tons of CO₂ per year; 44 are under construction, and more than 500 projects is announced.

Carbon Capture Providing Financially Lucrative Opportunities to Drive the Carbon Capture, Utilization and Storage Market Growth

Carbon capture provides financially lucrative opportunities and is expected to drive the Carbon Capture, Utilization and Storage Market. CO2 production through carbon capture costs more than conventional production, making it difficult for companies using this method to compete in the market. However, the increasing carbon price plays a major role in opening up new lucrative opportunities for carbon capture and utilization (CCU). Companies with sustainable practices and products have increased access to various financing options. As carbon pricing increasingly impacts the profitability of these companies and plants, companies that are using CCU technology as leverage have the additional funds to invest in innovation and R&D.

Growing Demand from the Oil and Gas Industry to Drive the Carbon Capture, Utilization and Storage Market Growth

The Carbon Capture, Utilization and Storage Market was supported by growing demand from oil and gas industry, due to growing applications of carbon dioxide for enhanced oil recovery process (EOR). The process is a tertiary crude oil production process which allows the producers to produce 30-60% more oil than through primary and secondary recovery processes.

Gas injection EOR which uses carbon dioxide is the most commonly practiced oil recovery process, with around 60% of total EOR process in the US is conducted by gas injection. The process involves the use of gases such as natural gas, nitrogen, or carbon dioxide that expand in a reservoir to push additional oil to a production wellbore or dissolve other gases that dissolve in the oil to lower its viscosity and improve its flow rate.

- The GCC has an estimated 44.01 gigatonnes (Gt) of geological CO₂ storage capacity, making it one of the world's most promising regions for large-scale Carbon Capture, Utilization and Storage (CCUS) deployment.

Implementation of COP26 to Limit Global Warming to Drive the Carbon Capture, Utilization and Storage Market Growth

The implementation of the United Nations Climate Change Conference, more commonly referred to as COP26 is expected to drive the demand for carbon capture utilization and storage. Innovation is making carbon capture viable for a huge number of businesses globally. To accelerate adoption, 5 billion tons of carbon dioxide must be removed from the atmosphere by 2050. But to meet net zero ambitions by 2050, there needs to be a 500-fold increase in global CCUS equipment capacity. By the time World Energy Outlook was published, more than 120 countries announced new targets for emissions reductions by 2032, and governments representing about 70% of global carbon dioxide (CO2) emissions had pledged to bring those emissions to net zero by 2050.

Carbon Capture, Utilization and Storage Market Restraints

High Capital Cost to Restraint the Carbon Capture, Utilization and Storage Market Growth

The high cost for capturing, and transporting carbon dioxide is a major challenge in the market. Carbon dioxide can be transported in gas form via various means including railway, ship and pipelines. Transporting carbon dioxide requires more energy compared with other alternatives and increases overall cost of production. The carbon dioxide for ship transport and compression for pipeline transport requires abundant electrical energy. For example, capital costs per net MW of electricity with CO2 capture are on average 14% higher than for the bituminous coal plants.

Globally, government agencies have formulated various regulations for the proper storage and transportation of carbon dioxide. These regulations also affect the cost of transportation. The high cost of transportation is expected to affect profit margins of carbon capture, utilization and storage companies and limit the growth of the market.

Russian-Ukrainian War to Restraint the Carbon Capture, Utilization and Storage Market Growth

The Russia-Ukraine war is expected to hamper the growth of the carbon capture market during the forecast. The political turmoil between the two nations has led to material shortage and supply disruptions, causing anxiety among manufacturers due to fear of shortage of supplies. Russia's invasion of Ukraine is expected to increase fossil fuel demand and carbon emissions, which means more companies will need carbon credits to offset their emissions, eventually resulting in higher carbon prices. The US imposed sanctions on Russian fossil fuels, while the UK said it will stop buying Russian oil. The EU announced plans to cut Russian gas imports by 80% 2025 and phase out the rest, including coal and oil, by 2027.

The volatility impacted carbon markets around the world, including regional carbon markets Alternative energy sources are likely to mean shipping in more seaborne LNG and ramping up coal-fired power generation, all of which are more emission intensive options, thus, impacting the market in the forecast period. The detailed analysis of the Russian-Ukrainian war is covered in the Carbon Capture, Utilization and Storage Market report.

Carbon Capture, Utilization and Storage Market Segment Analysis

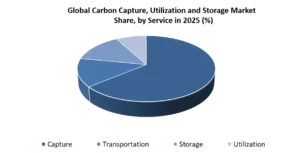

By Service

Capture is the dominated segment in the Carbon Capture, Utilization and Storage (CCUS) Market in 2025 and is projected to retain its position for the forecast period. Capture forms the first and the most essential step in the CCUS value chain and also constitutes the highest cost investment within the project. Increased usage of post-combustion capture systems in power plants and industries, coupled with stricter carbon emissions norms and incentives from the government for reducing carbon emissions, will continue to fuel demand in the segment. On the other hand, Utilization is projected to be the fastest-growing segment during the forecast period on account of increased commercial application of captured CO₂ for producing sustainable fuels, chemicals, artificial materials, and construction materials.

By CO₂ Source

Industrial facilities are the dominating segment in 2025 due to increased deployment of CCUS within industrial sectors that have high levels of difficult-to-abate emissions, including cement, iron and steel, chemical production, refineries, and fertilizer manufacturing sectors. There are many policies and pledges to reach net zero emission from these industries, which is boosting the growth of investments in carbon capture technologies. The DAC segment is predicted to be the fastest-growing segment during the forecast period due to technology advancement, decreasing capture costs, growing carbon removal pledges, and increased demands for carbon dioxide removals.

By Project Type

In 2025, the Brownfield category held the largest share of the market since more industries were retrofitting their existing power plant or industrial installations with carbon capture technology than constructing new power plants or facilities. Such retrofits help companies reduce emissions and utilize the existing infrastructure with minimal capital investments. It is expected that the Greenfield category will experience the highest CAGR over the forecasted period since more investments are made in the construction of newly designed projects in hydrogen, ammonia, renewable energy, and other industries with integrated CCUS technology.

By Technology

The Solvents & Sorbents category it's the dominant in 2025 due to the commercial availability, efficiency of carbon capturing, and use in power generation, oil & gas, cement, and chemical industries. The technology is proved to be efficient and effective with continuous improvements in the industry. The Membranes category is projected to grow the fastest over the forecast period due to to its modularity, low energy consumption, small size, and increased usage in natural gas, hydrogen, and other industries.

By End-Use Industry

Oil & Gas accounted for the leading share of the market in 2025 owing to extensive use of CCUS for EOR processes, natural gas processing, and emission reduction in all upstream, midstream, and downstream processes. Increasing capital investment from leading players operating in the oil and gas industry for construction of carbon capture facilities continues to drive the market growth. The Cement industry segment is expected to witness the highest CAGR throughout the forecast period owing to cement production being one of the carbon-intense sectors wherein CCUS is one of the few available options to reduce process emissions.

Carbon Capture, Utilization and Storage Market Competitive Analysis

The Global Carbon Capture, Utilization and Storage (CCUS) Market is extremely competitive with participants from integrated energy majors, engineering, industrial gases producers, and carbon capture technology providers. Leading players in the market are Mitsubishi Heavy Industries, ExxonMobil, Fluor Corporation, Honeywell International, SLB, Shell, Siemens AG, TotalEnergies, Equinor, Aker Solutions, Linde, Hitachi, JGC Holdings, Japan CCS, C-Capture, Carbicrete, Carbon Centric, Carbon GeoCapture, Elysian Carbon Management, Octavia Carbon, Zero Carbon Ventures, Carbon EX, Tanda (Shenzhen), Powered Carbon, Sinotech, Tandem Technical and others. All these companies are making huge investments in commercial scale projects for industrial decarbonization and reaching net-zero emissions.

Competitive rivalry occurs because of the technological superiority of capture systems, cost-effectiveness, project implementation capabilities, CO₂ transport and storage networks, as well as partnerships with industries emitting CO₂. Integrated energy majors like ExxonMobil, Shell, TotalEnergies, and Equinor use their expertise in oilfield services and geology to create integrated CCUS platforms, whereas technology majors such as Mitsubishi Heavy Industries, Honeywell, Fluor, Siemens, SLB, Aker Solutions, Hitachi, JGC Holdings and Linde use their proprietary capture technologies, EPC services, process integration, and digital solutions. Constantly ongoing R&D is aimed at increasing the rate of carbon capture and minimizing expenses.

Further reinforcement comes from new players such as C-Capture, Carbicrete, Carbon Centric, Octavia Carbon, Carbon GeoCapture, Elysian Carbon Management, Carbon EX, Powered Carbon, and Zero Carbon Ventures, who are engaged in providing advanced solvents, direct air capture, carbon mineralization, carbon utilization, and carbon removal technologies respectively. As more funding sources and carbon pricing initiatives become available through the efforts of governments, the players within the market are now making concerted efforts to form joint ventures and license technologies among others in order to reinforce their market positioning.

Carbon Capture, Utilization and Storage Market Regional Insights

North America dominated the Carbon Capture, Utilization and Storage Market in 2025, with the largest revenue share and is expected to hold the highest market share during the forecast period. North America Carbon Capture, Utilization and Storage Market is estimated to grow at a significant CAGR of 10.8% over the forecast period. U.S. dominated the North America Carbon Capture, Utilization and Storage Market in 2025 and is expected to witness the highest growth during the forecast period.

The growing demand for clean technology, accompanied with the growing use of CO2 in EOR practices, is likely to drive the Carbon Capture, Utilization and Storage Market in the United States. Chemical production, hydrogen production, fertilizer production, natural gas processing, and power generating are among the industries where CO2 is captured and injected in the United States. Furthermore, the country has a first large-scale carbon capture plant.

Asia Pacific region was the second largest region in the Carbon Capture, Utilization and Storage Market in 2025, grew at a CAGR of 3.7%. Asia Pacific Carbon Capture, Utilization and Storage Market is expected to grow at the fastest rate of 17.2% and is expected to hold the second- largest revenue share of the Carbon Capture, Utilization and Storage Market during the forecast period. In the Asia-Pacific region, China held the largest market share in 2025 and is expected to grow at a significant rate during the forecast period. China, the world's biggest CO2 emitter, pledged to reach carbon neutrality by around 2060. To achieve this target, as much as 1.82 billion tonnes of CO2 needs to be cut via CCUS each year by that time, according to a study conducted by a research institute affiliated to China's environment ministry.

China also recognizes that carbon capture and storage is the only clean technology that can be applied to decarbonize major industries and has the added significant potential to create new revenue streams, which enable economic growth. As a result of China’s carbon neutrality pledge, various Chinese Government ministries have become more active in building understanding of CCS’s role in decarbonization, laying the groundwork for policy development. Among many other factors, above mentioned factors are expected to drive the growth of Asia Pacific Carbon Capture, Utilization and Storage Market during the forecast period.

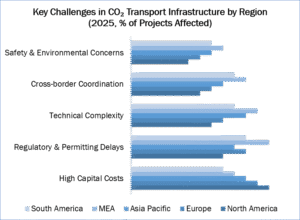

Key Challenges in CO₂ Transport Infrastructure by Region (2025, % of Projects Affected)

The graph depicts the major risks associated with CO₂ transportation infrastructure in North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and South America. High capital expenditure is the most important risk on a global scale, due to the high cost of developing the infrastructure for pipeline, compression, and transport. Regulatory and permitting risks are other barriers to development of CCUS projects, especially in MEA and Europe, with environmental permits and long permitting process being expensive and time-consuming.

Technical risks associated with multinationals and offshore storage of CO₂, in addition to cross-border collaboration issues are particular problems in Europe due to the need for unified regulatory framework and infrastructure development. Safety and environment risks are vital in North America and Europe due to high requirements regarding integrity of the infrastructure, and environmental impact on the region.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 18 March 2026 | Schlumberger (SLB) | Collaborated with Microsoft to launch an AI-based monitoring platform for real-time risk assessment in geological CO2 storage. | Enhances operational reliability and safety validation for long-term sequestration projects globally. |

| 02 December 2025 | Department of Science and Technology (India) | Officially launched the first National R&D Roadmap for CCUS to enable the country's Net Zero targets by 2070. | Creates a structured funding and regulatory framework to accelerate technology deployment in the Asia-Pacific region. |

| 02 July 2025 | Carbon Clean | Opened a new Global Innovation Centre (GIC) in Navi Mumbai, featuring one of the world's largest dedicated carbon capture research facilities. | Strengthens solvent development and testing capabilities to lower the cost of industrial capture applications. |

| 22 May 2025 | Mitsubishi Heavy Industries (MHI) | Commenced operations of a CO2 capture pilot plant at the Himeji No. 2 power plant to test flue gas from gas turbines. | Demonstrates the feasibility of next-generation capture technologies specifically for gas-fired power generation. |

| 15 April 2025 | Climeworks | Broke ground on the Mammoth Direct Air Capture (DAC) plant in Iceland, designed to capture 36,000 tons of CO2 per year. | Scales up commercial DAC viability and helps reduce the per-ton cost of atmospheric carbon removal. |

| 03 March 2025 | Malaysian Government | Unveiled the Carbon Capture, Utilization, and Storage (CCUS) Bill 2025 to provide a comprehensive legal framework for the industry. | Establishes legal certainty for investors and sets a precedent for regulatory standards in Southeast Asian markets. |

Carbon Capture, Utilization and Storage Market Scope: Inquire before buying

| Global Carbon Capture, Utilization and Storage Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 3.66 USD Billion |

| Forecast Period 2026-2034 CAGR: | 15.1% | Market Size in 2034: | 12.98 USD Billion |

| Segments Covered: | By Service | Capture Pre-Combustion Oxy-Fuel Combustion Post-Combustion Others Transportation Onshore Pipeline Offshore Pipeline Ships Others Storage Saline Formation CO2-EOR Depleted O&G Wells CO2-enhanced coalbed methane (CO2-ECBM) Utilization CO2 to Fuels CO2 to Chemicals Building Materials Others |

|

| by CO₂ Source | Power Generation Direct Air Capture Bioenergy Industrial Facilities Others |

||

| by Project Type | Greenfield Brownfield |

||

| by Technology | Chemical Looping Solvents & Sorbents Membranes Cryogenic Separation Others |

||

| by End User Industry | Oil & Gas Power Generation Chemical & Petrochemical Cement Iron & Steel Others |

||

Carbon Capture, Utilization and Storage Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Carbon Capture, Utilization and Storage Market Report in Strategic Perspective:

- Shell plc

- ExxonMobil

- Equinor ASA

- Occidental Petroleum Corporation

- Linde plc

- Mitsubishi Heavy Industries Ltd. (MHI)

- CarbonCapture Inc.

- Fluor Corporation

- Chevron

- SLB Capturi

- Honeywell International Inc.

- Baker Hughes Company

- Halliburton

- Saipem

- Carbon Clean

- Climeworks

- LanzaTech

- Zero Carbon Systems

- Carbon Engineering (Occidental Petroleum)

- CarbFix

- CarbonFree

- Japan CCS Co. Ltd

- Sulzer Ltd.

- JGC HOLDINGS CORPORATION

- Hitachi Industrial Products, Ltd.

- CarbonCure Technologies Inc

- Charm Industrial

- Graphyte, Inc

- Greenlyte Carbon Technologies

- TotalEnergies SE

- Others

Frequently Asked Questions

1. What is the projected size and growth rate of the Carbon Capture, Utilization and Storage Market?

Ans. The market valuation was USD 3.66 billion in 2025, reaching USD 12.96 billion by 2034. This represents a 15.1% CAGR, driven by global industrial decarbonization and sustainability.

2. Which region currently leads the Carbon Capture, Utilization and Storage Market share?

Ans. North America dominates the 2025 market share due to established industrial gas infrastructure, 45Q tax incentives, and extensive deployment of CO2 for Enhanced Oil Recovery.

3. How is Artificial Intelligence impacting Carbon Capture, Utilization and Storage Market trends?

Ans. AI accelerates innovation by identifying efficient molecular structures for CO2 separation, optimizing storage monitoring, and reducing capture costs through predictive generative modeling and real-time analytics.

4. What role does the Oil and Gas industry play in CCUS market growth?

Ans. The sector drives demand through Enhanced Oil Recovery applications, utilizing captured CO2 to boost production by 30-60% while significantly reducing lifecycle carbon emissions for producers.

5. How does Bio-energy CCS (BECCS) contribute to the Carbon Capture, Utilization and Storage Market?

Ans. BECCS leads technology segments by generating negative emissions, capturing carbon from biomass combustion or fermentation, and sequestering it to meet critical net-zero climate targets globally.

6. What are the primary cost challenges facing the Carbon Capture, Utilization and Storage industry?

Ans. High capital expenditures for specialized transport pipelines and energy-intensive compression processes remain major restraints, impacting profit margins for large-scale industrial carbon sequestration projects.

7. How are government initiatives influencing the Carbon Capture, Utilization and Storage Market forecast?

Ans. Federal funding for point-source capture and COP26 pledges drive adoption, providing the regulatory certainty and financial subsidies necessary for infrastructure expansion through 2034.